wp01

wp01Participant

Master

@GraHal

In the ASX the first bar of the BT just popped up. (exactly with one day delay). I guess you should also see it now.

Patrick

Thank you Patrick and MichiM … mystery solved and also something new learned (24 hour delay on daily backtest) and I’m on track now! 🙂 Yes I can see the entry trigger now on my Platform.

This is a very very interesting Thread / Strategy, huge thank you to Reiner for sharing and also thanks to you guys on the ‘optimising team’.

Best Regards to All

GraHal

wp01Participant

Master

@Reiner and others.

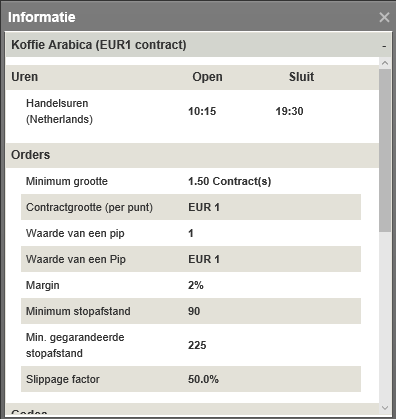

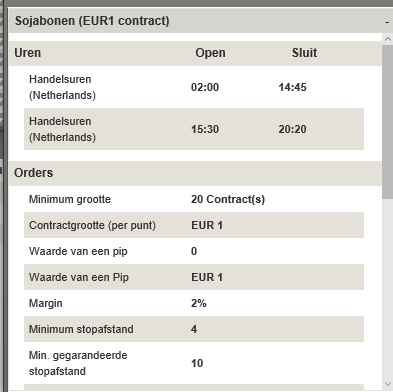

Not all commodities are 24 hours per day tradable. For example Coffee trades between 10.15 hours and 19.30 hours CET. Soyabeans on the other hand has two different

tradinghours per day. Attached a print as an example. When you are using automatic trading from IG i think it will be a problem to effect these trades. They will probably be

rejected. So my suggestion is to but these hours in the codes. I see for example in Soyabeans PF_Soybeans_Daily_Jan2-Feb2 that in the BT on 2nd. of February a trade is effected

at 02:00 hours, but if the signal is at 01.00 hours, it will be rejected for an hour and that Coffee maybe not be effected at all.

Regards,

Patrick

Hi Patrick,

I agree. The best way would be to change the algos from daily to hourly timeframe. With this approach we could better control at what time we trade e.g. if the spreads are acceptable. I’ll check this.

Best, Reiner

wp01Participant

Master

Thanks Reiner.

You once said that the signal comes at 01.00 a.m.

Is this something you created yourself or is this something that comes with daily charts in PRT?

Patrick

Patrick, the time is indicated by the daily timeframe. Daily timeframes are all synchronized at 01.00 a.m. local timezone and in my opinion this can’t be changed.

wp01Participant

Master

I’ve added the trading hours and the minimum amount of contracts to the Roadmap Excel file. Maybe someone find this handy.

It is the commodities that have divergent times and are not quoted 24 hours a day. This causes problems when you

activate these for automatic trading.

The indices do have 24 hours a day quotes but have divergent spreads of course outside the normal trading hours.

This is not an issue for automatic trading, but for example the ASX this week was activated at 14.00 hours CET. The only thing i can think of is that

it is 10 hours time difference, which means that the signal for the ASX was at 00.00 O’clock the next day.

Patrick

Hi Reiner, and the others,

Another stupid question 😉 Have you ever tried to adapt the pathfinder pattern to short time sessions? Like 15 min positions for example? Of course, performance would not be the same….And seasonality multiplier would be certainly useless….

Winniw37

Look at my post in the original pathfinder thread:

Pathfinder Trading System

ALE

ALEModerator

Master

There’s a version of 15 m on the other topic..

I know there are already a lot of pathfinder pattern available. For my own, i run daily swing and h4 hall of fame.

Would we have some interest in developing a portfolio with several pathfinder system like dax15 min from Joachim, for automatic short term trading, with low drawdown?

what are you thinking about it? Good idea or not? (sorry, i should have posted in the other topic…)

Personally I think it´s good to combine both short and longterm trading systems but it all depends of your portfolio size. I have 11 systems running right now, from 5m to daily.

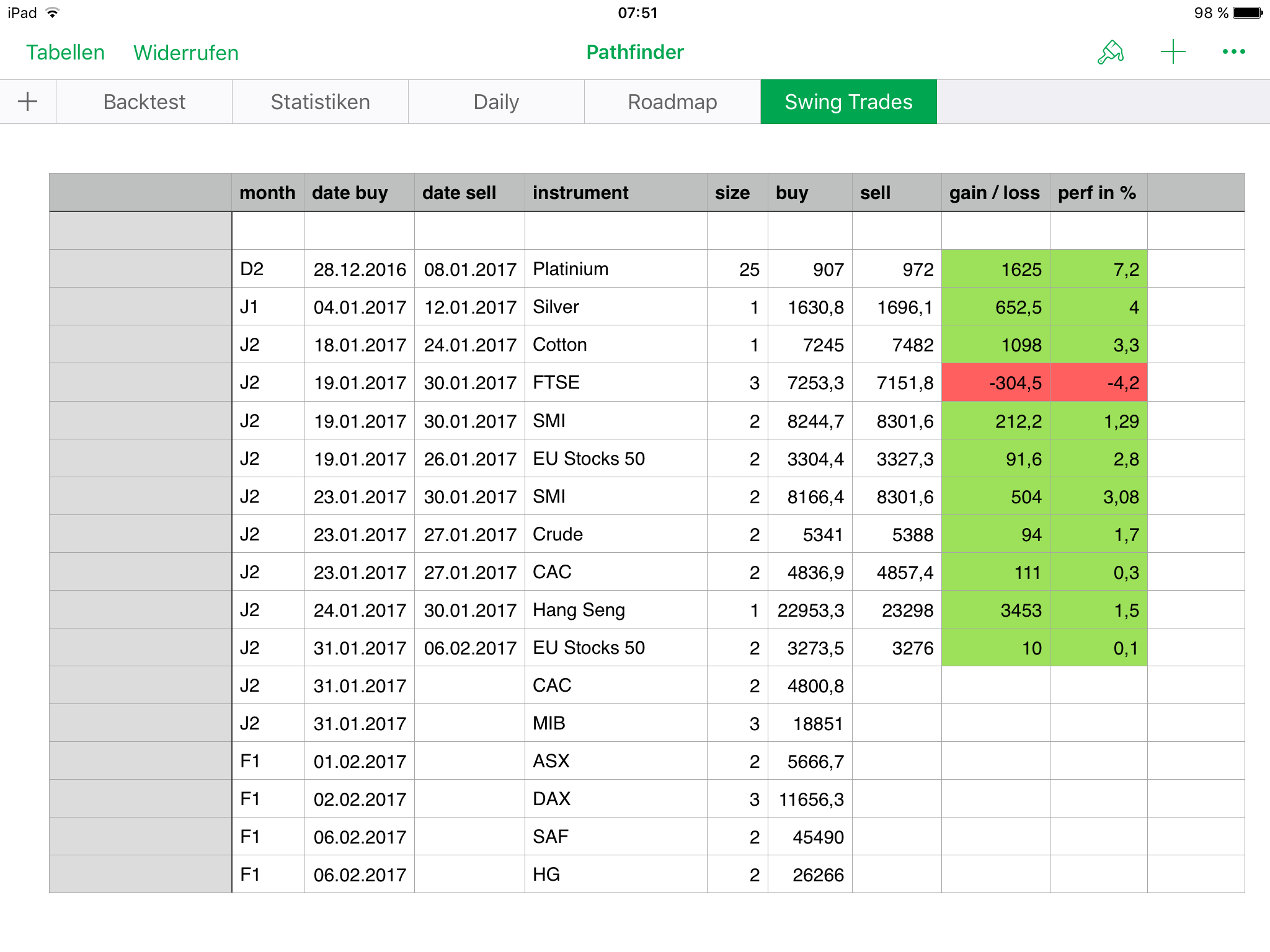

Euro Stoxx 50 was closed, SAF and Copper opened each a long position, please find attached the details

Hmm .. I didnt get a close signal for Euro Stoxx 50 in live, but these long signals:

06 Feb 2017 02:46 “EU Stocks 50 Kassa (2EUR)” long 1x @ 3279 @ live system

06 Feb 2017 01:00 “Südafrika 40 Kassa (10ZAR)” long 2x @ 45490 @ live system

06 Feb 2017 01:00 “Hochwertiges Kupfer (1EUR)” long 2x @ 26266 @ live system