Hi Nonetheless, we’re definitely comparing with the system I posted, although there is a slight variation in the If C1 and If C2, as mentioned. (Not sure where that <span class=”difference”>shortonmarket etc </span>came from? It didn’t appear to make any difference in the profits if I replaced my system C1/C’2’s with your “If c1 and c2” statements. It warns that tick by tick (tbt) testing cannot be done too, despite the yellow triangle saying that tests after after the 1st Aug 2010 will be done tbt. Still waiting for IG’s response to that.

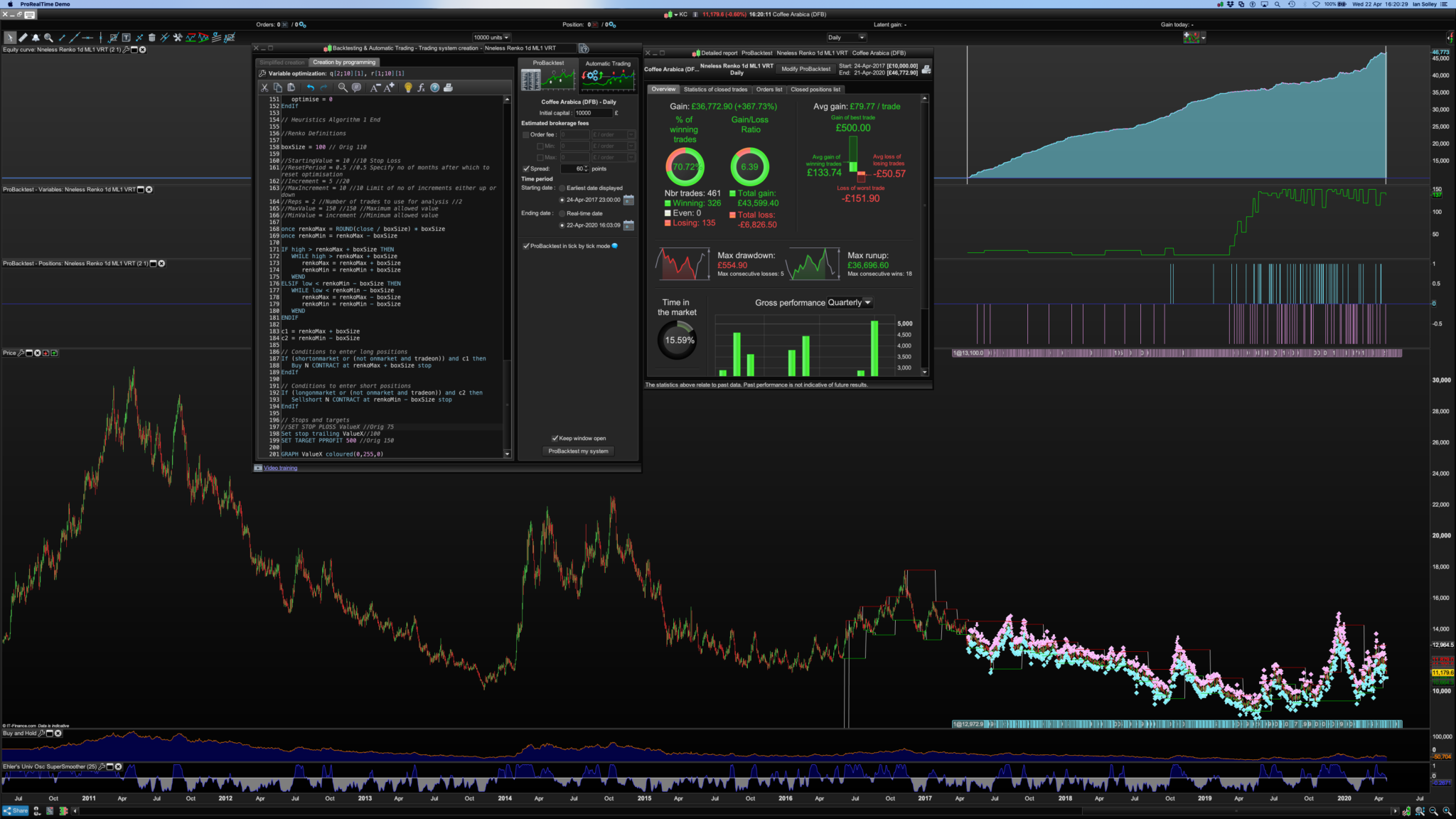

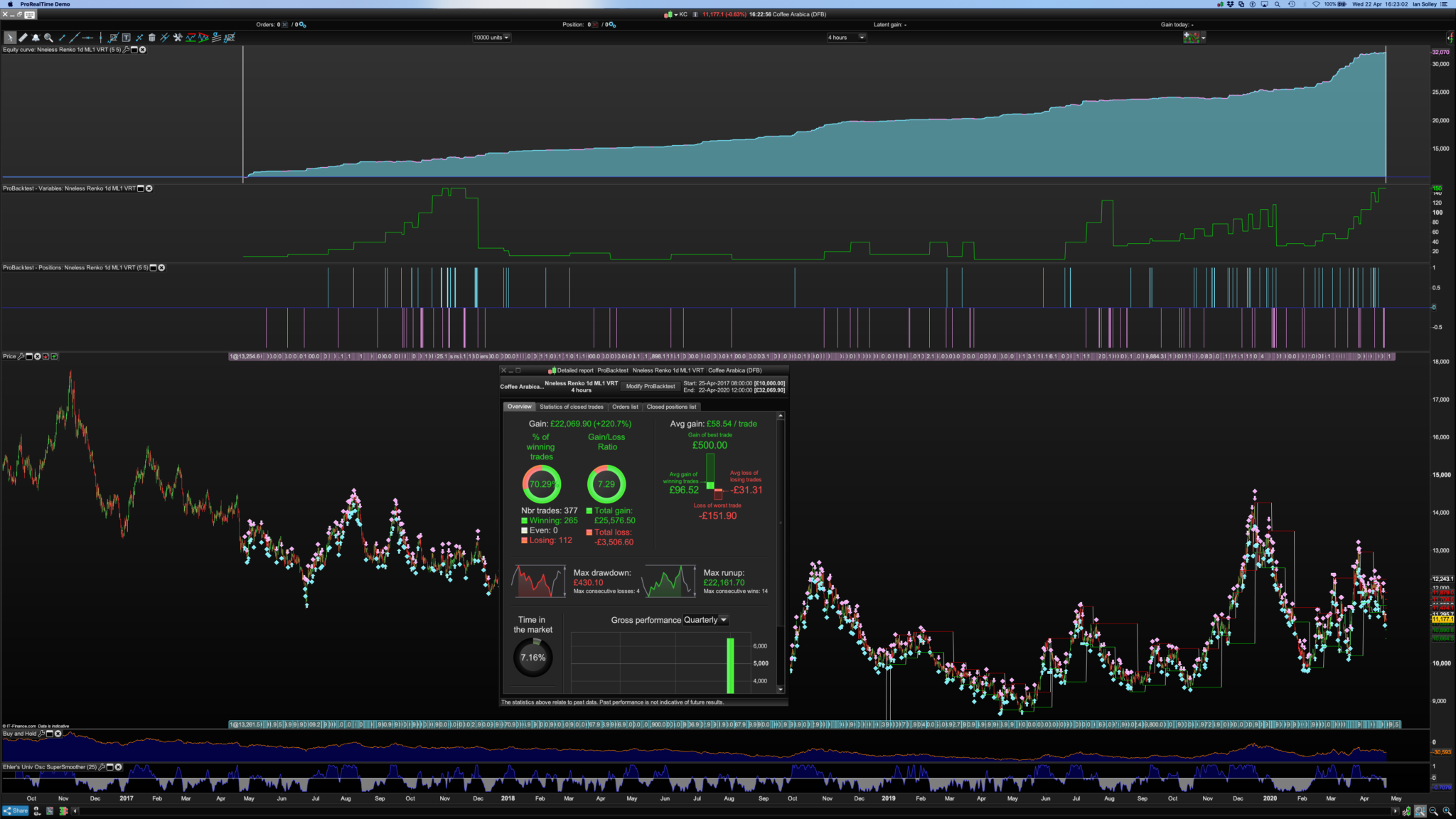

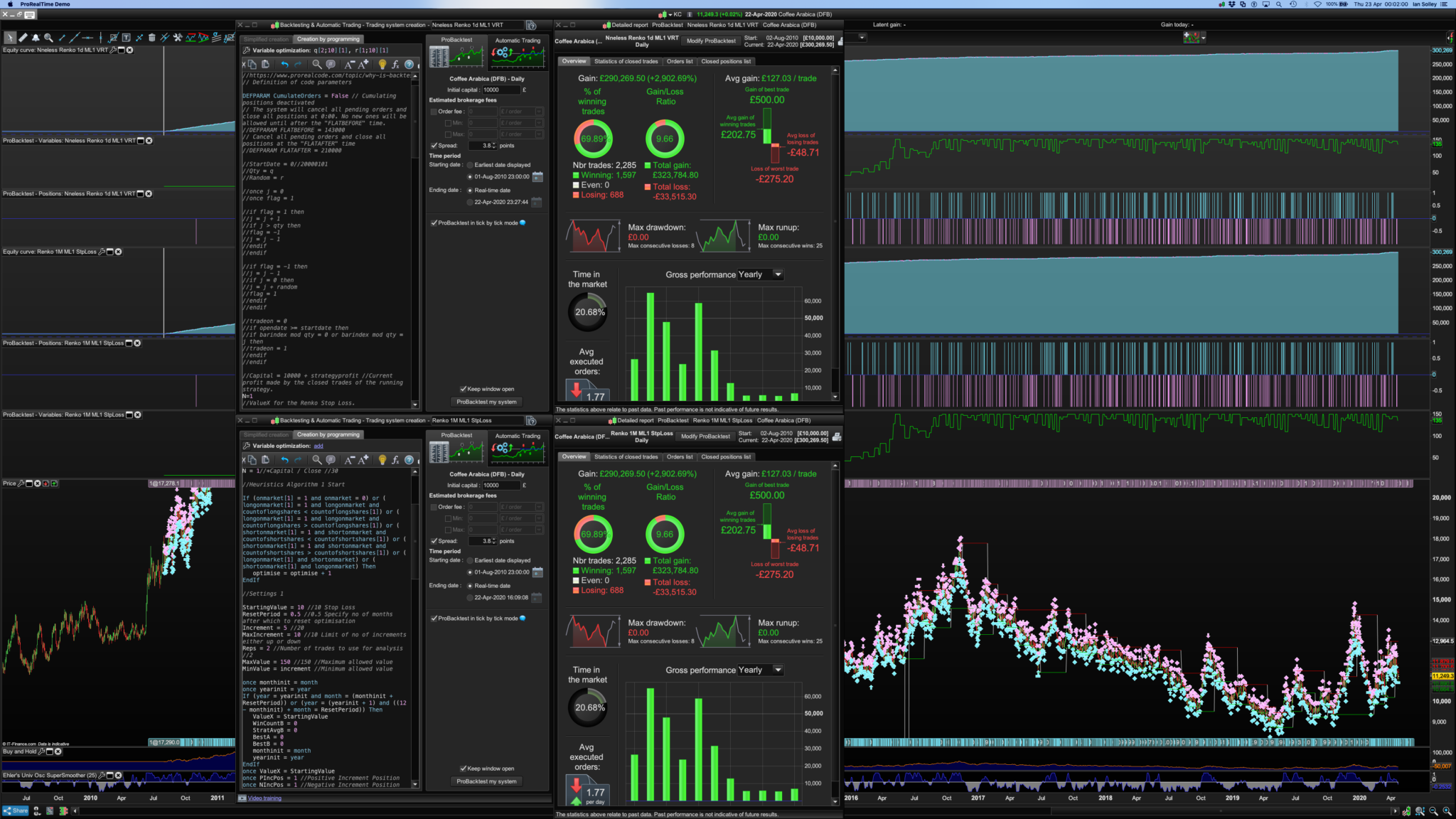

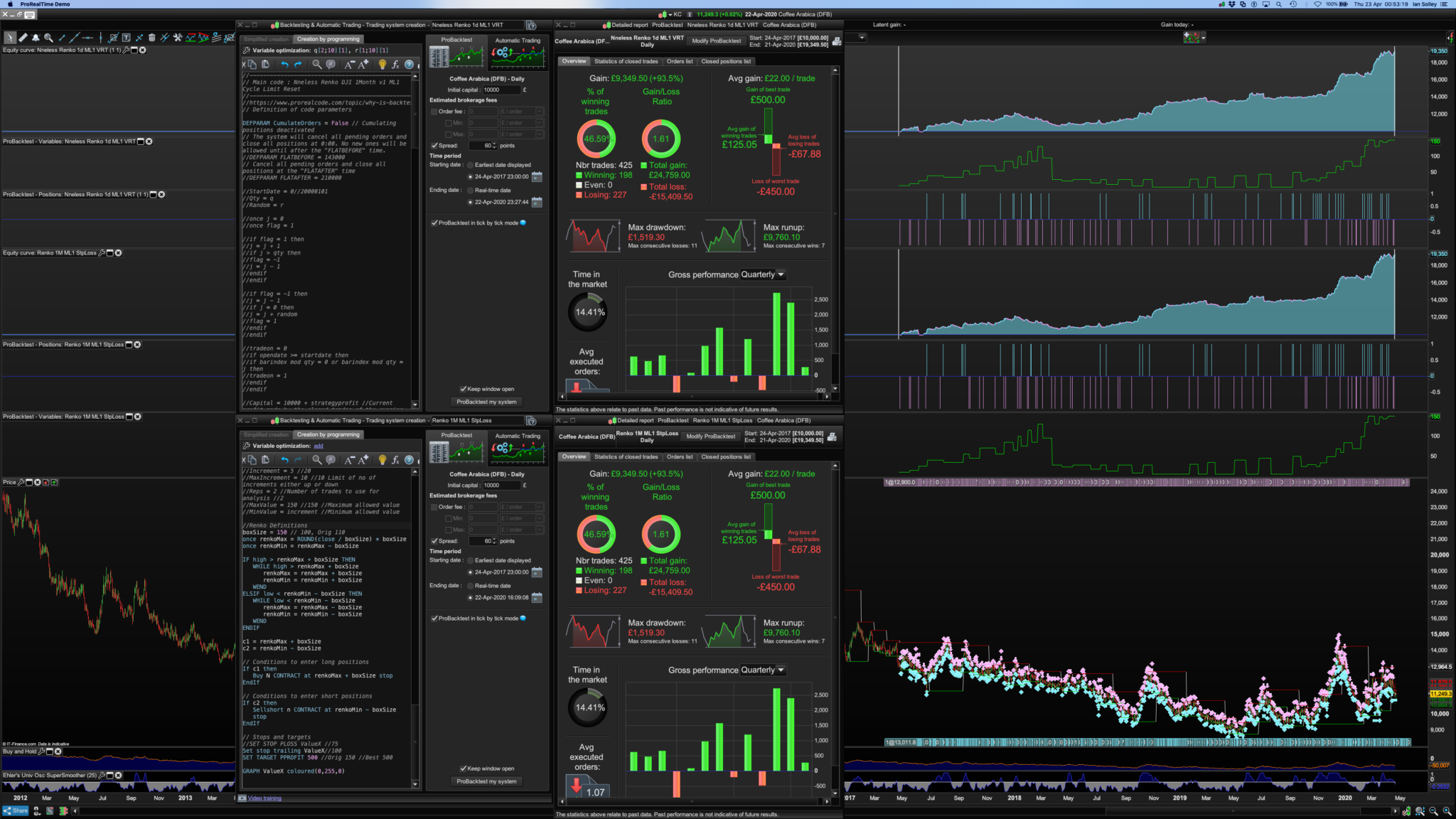

With the “same” code (although yours has VRT) it gives different results and different stop loss GraphX’s. Pls see results image #1. All other things being equal, it is the VRT code effecting the results because when the VRT is rem’d out our results are identical: Pls see results image #2. Wondered if you might know why that is @Vonasi?

The interesting thing about this comparison test between our systems is that when I ran the identical dates: 24/04/17-22/04/20, as your posted results screen above, with the new 60 spread, your system did not show a warning that tbt testing couldn’t be done. Mine did, and the results are not the same. My code also takes about 4 to 5x’s longer to display results…

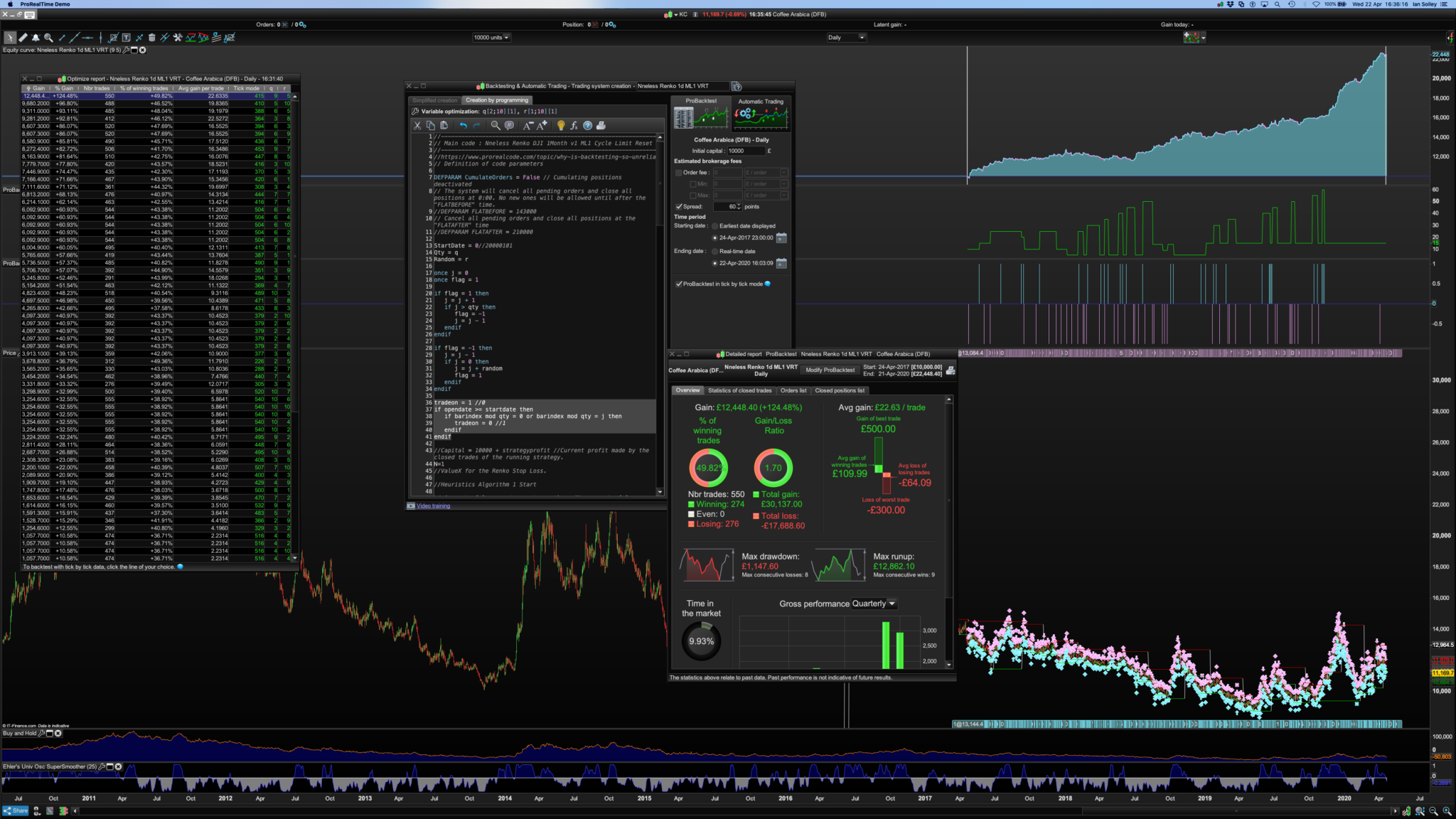

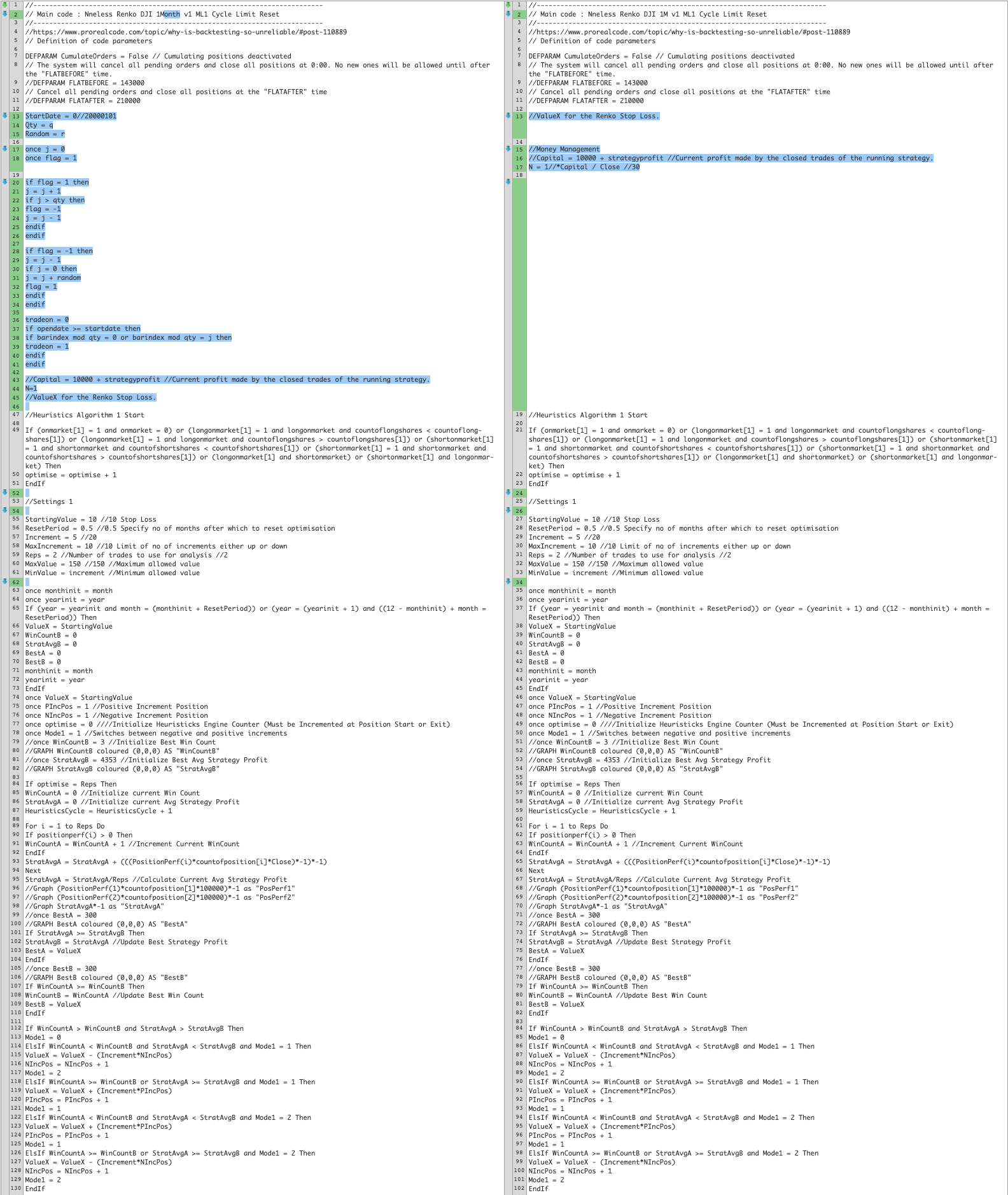

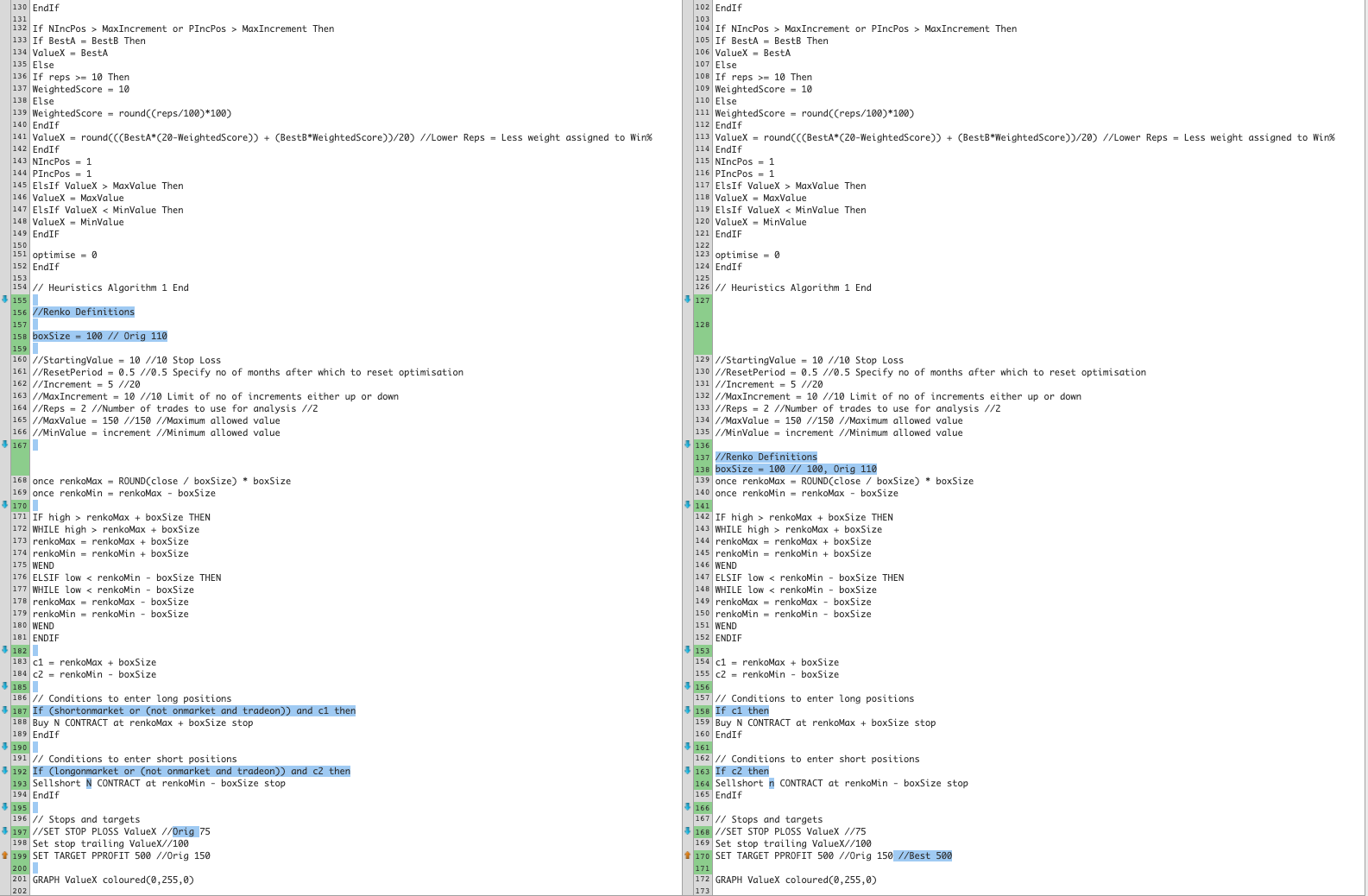

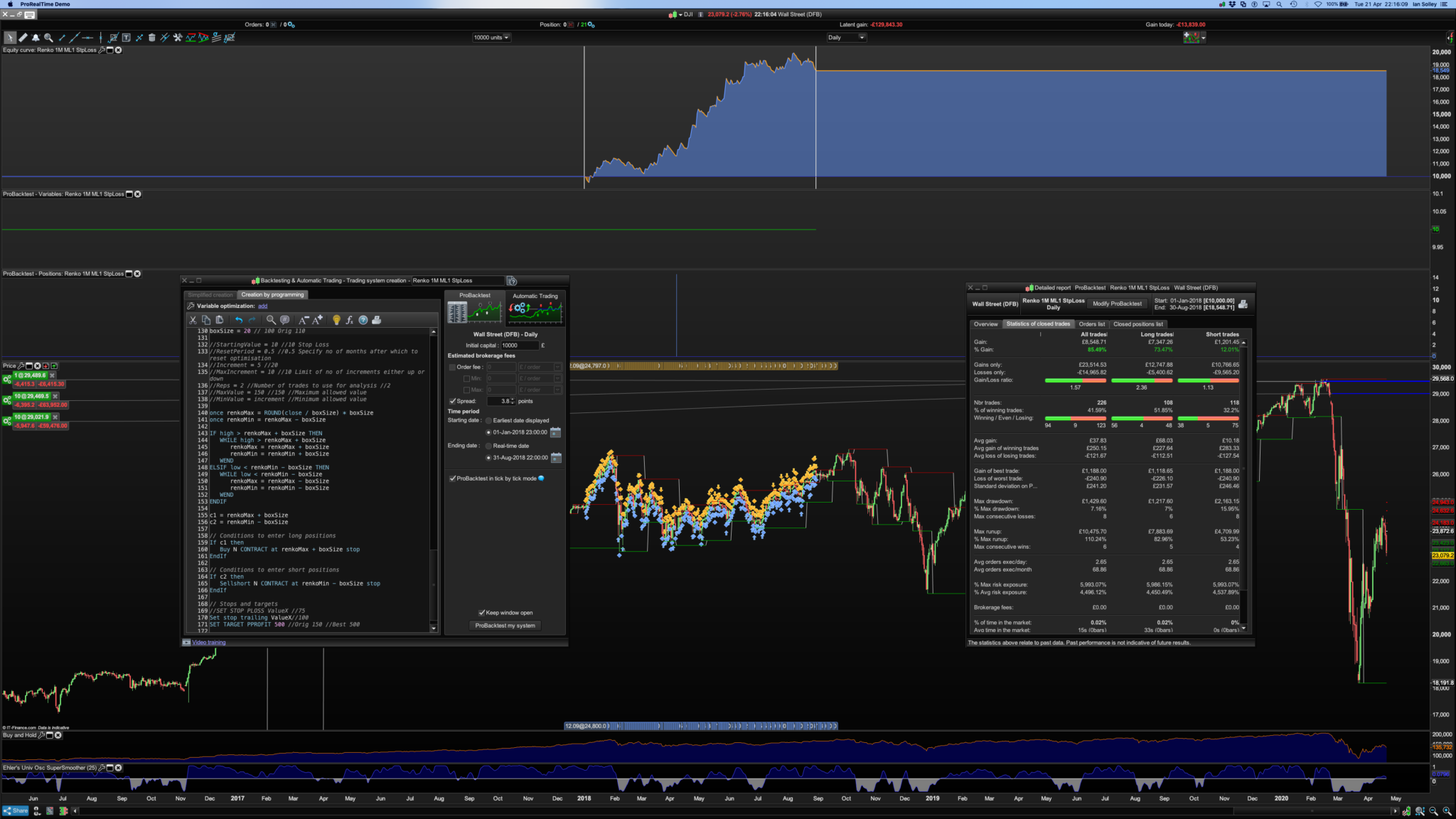

The code is now identical (I’ve checked it 3x’s in the text-compare.com comparison tool). There is no VRT, the dates are the same, the spread is the same, the boxsize is the same and the results were different… the only way I “fixed it” was to change the TF to 4 hours, then I got identical test results, and then I went back to Daily, and then finally the results were the same…Umm. I’ve deleted my slow 1M ML1 StpLoss system and recoded it.

@Nicolas, I wonder if you would know why the tick by tick (tbt) warning didn’t come up for Nonetheless’s version but did for my version when they have the same system code and parameters? I’ve had this tbt warning problem repeatedly, where sometimes it does and sometimes it doesn’t appear, even though I’m testing the same date ranges? Why would it now suddenly not be able to do a tbt test if all I’ve done is change a boxsize from 100 to 50? I also would be interested if you know or could find out how far back the tbt data actually goes for coffee (KC)? Thanks very much.

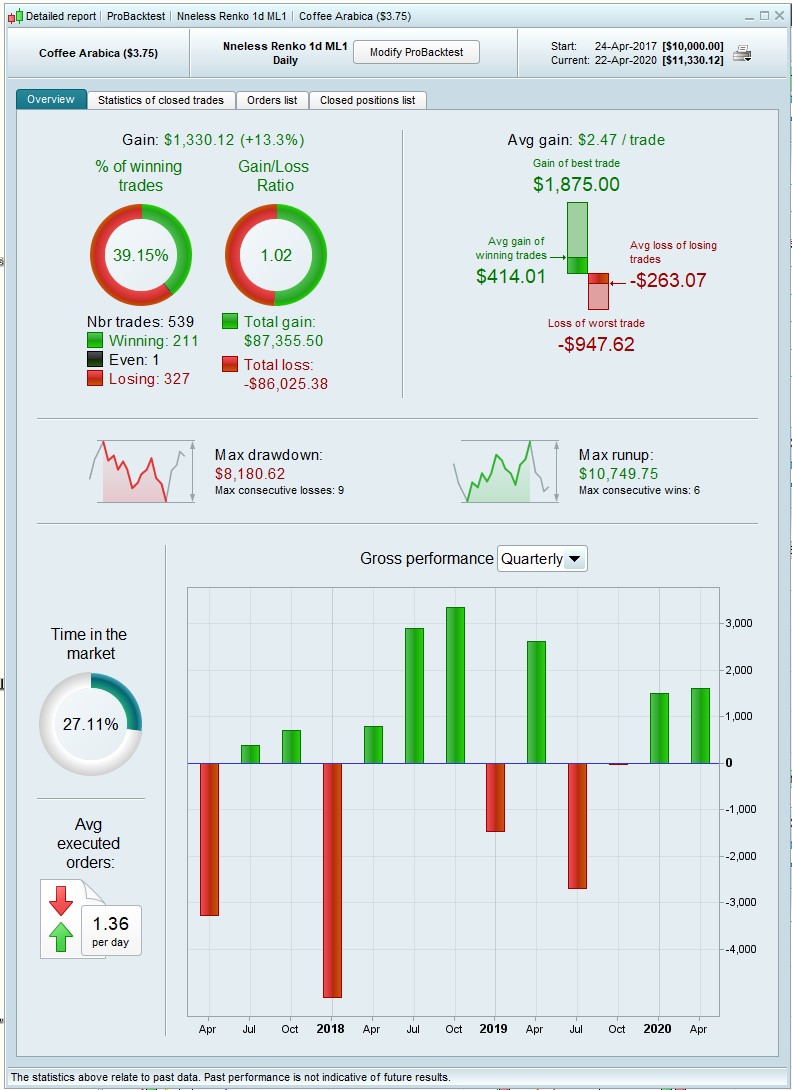

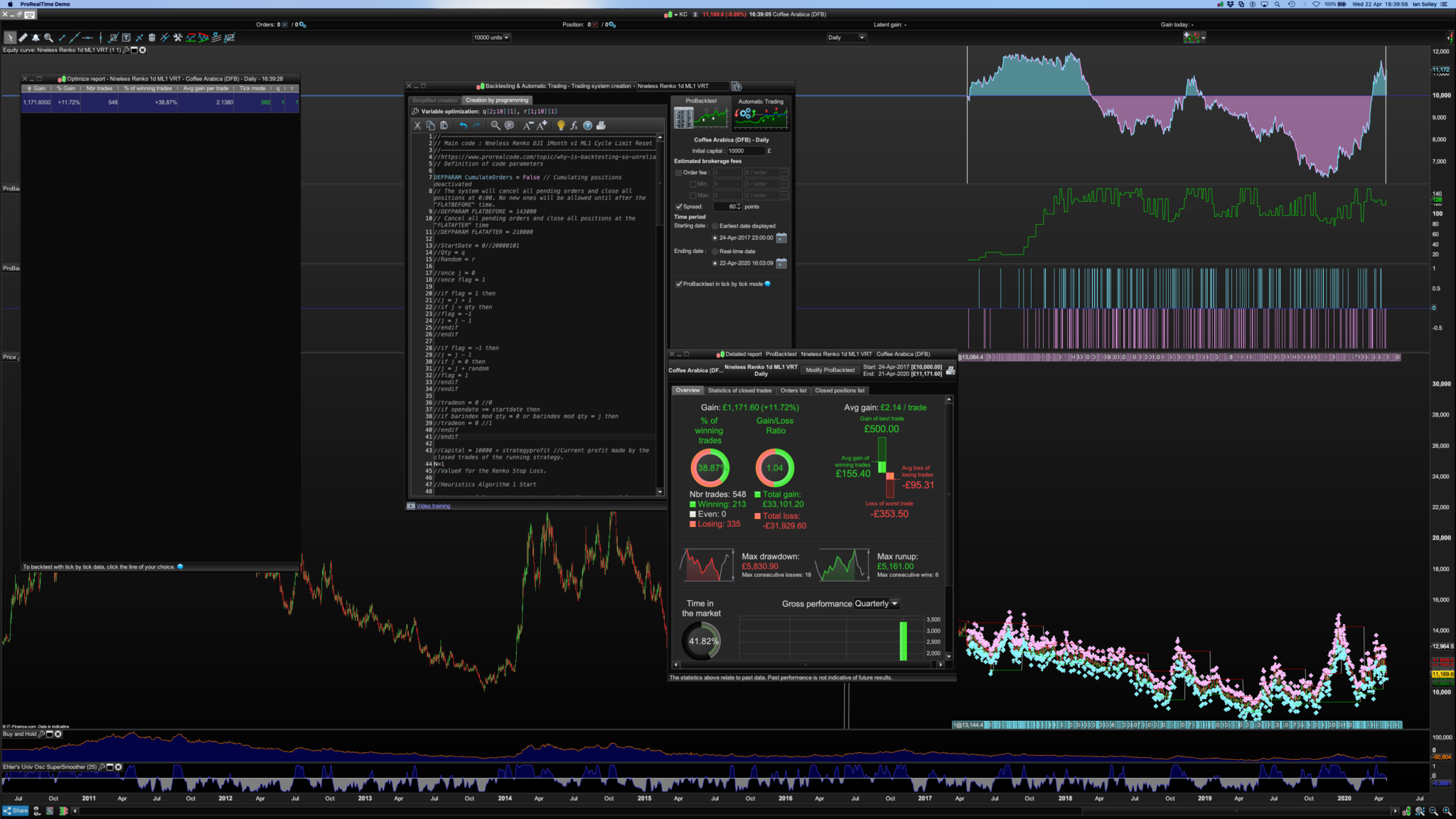

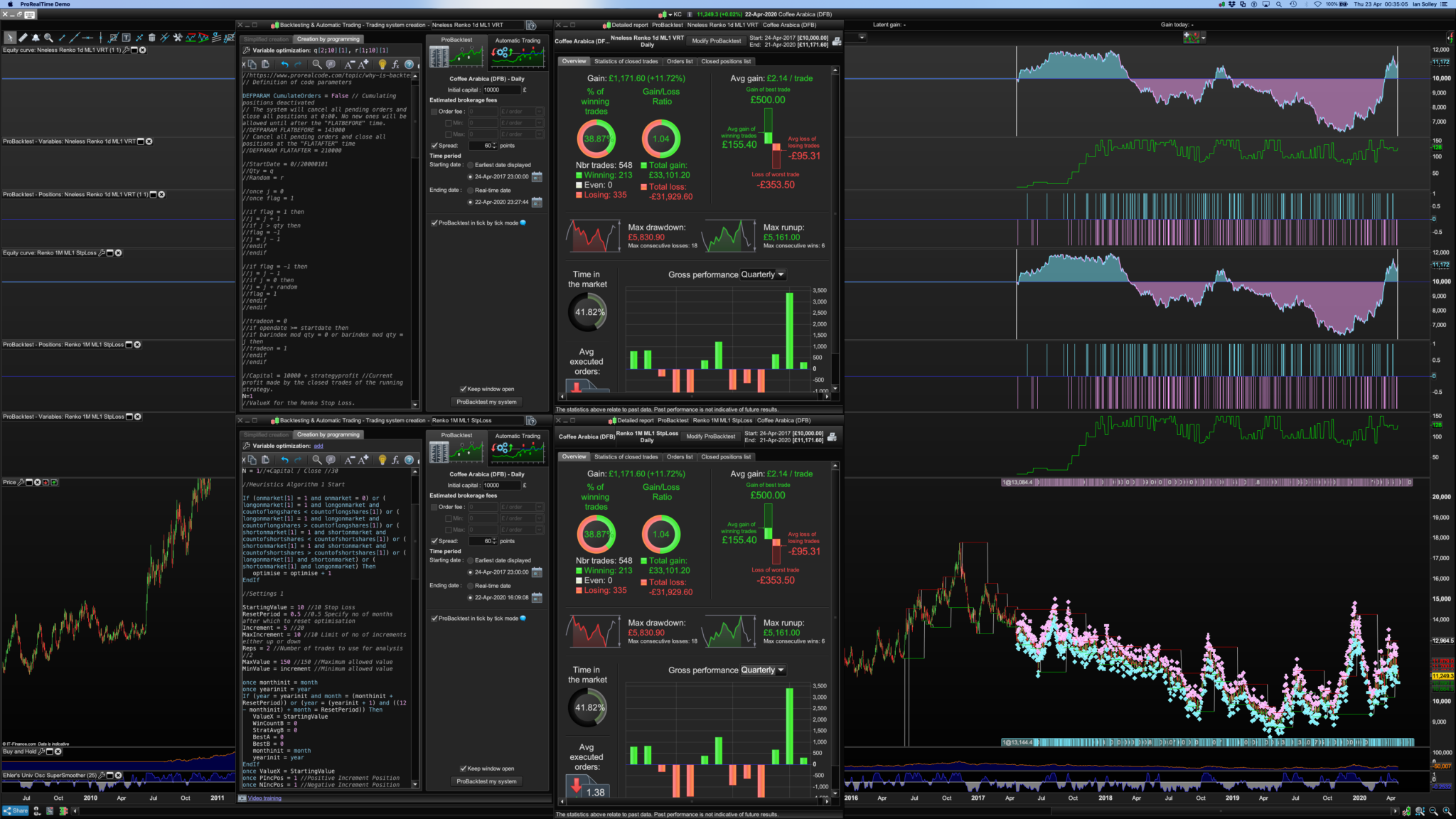

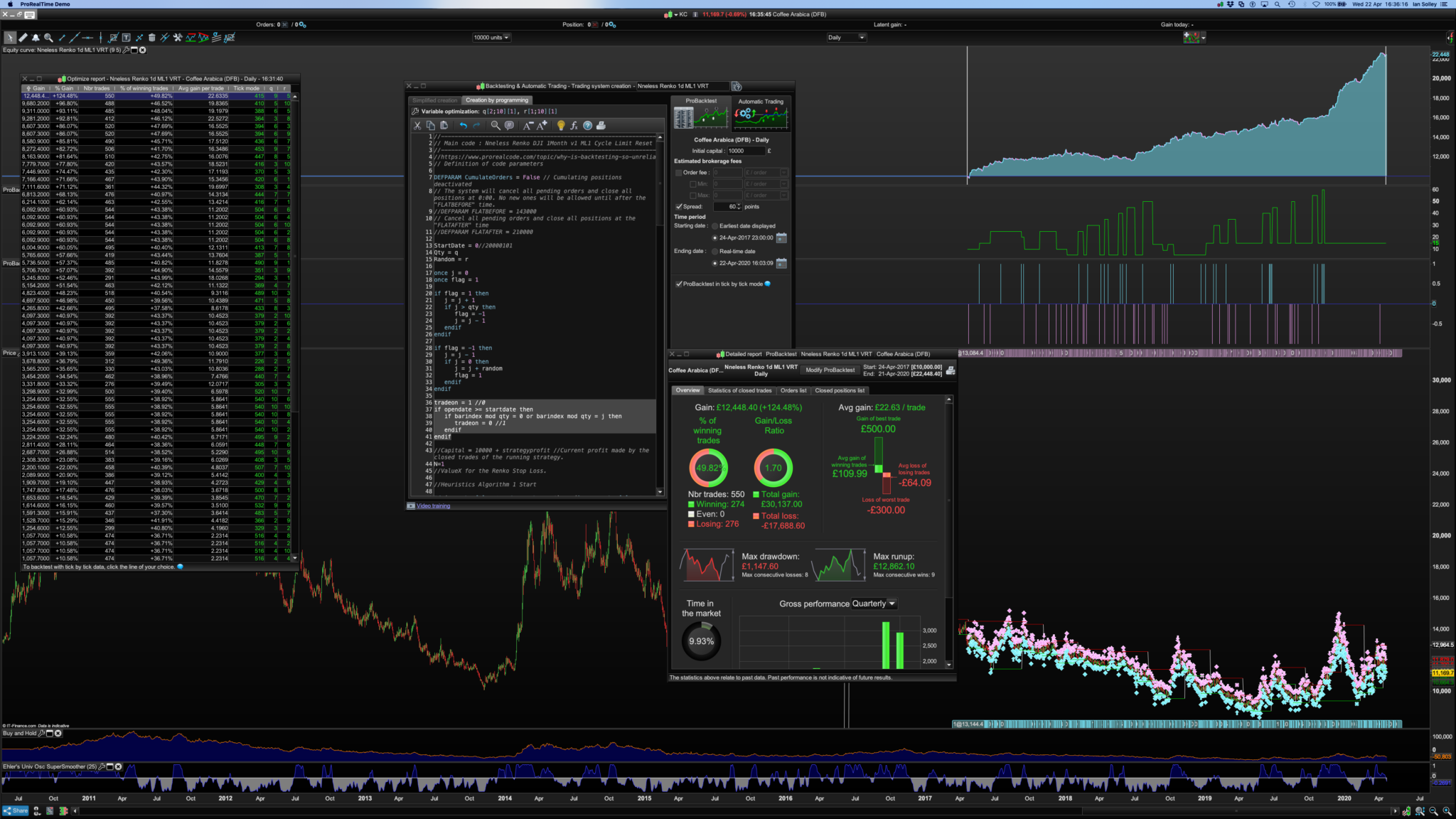

The possible solution to that low gain/loss and low profit above is to either use different date ranges (I’ve not created a daily system that lasted longer than 12 yrs) or increase the boxsize from 100 to 150 as mentioned for the daily, (I hadn’t seen your “I was working with this code..” comment when I posted). Pls see two images after this post; box =100 and box =150. Increasing the Money Mgt still works. The question of whether this is truly tbt testing, will hopefully be answered here or by IG/PRT. I’ll update as soon as I hear.

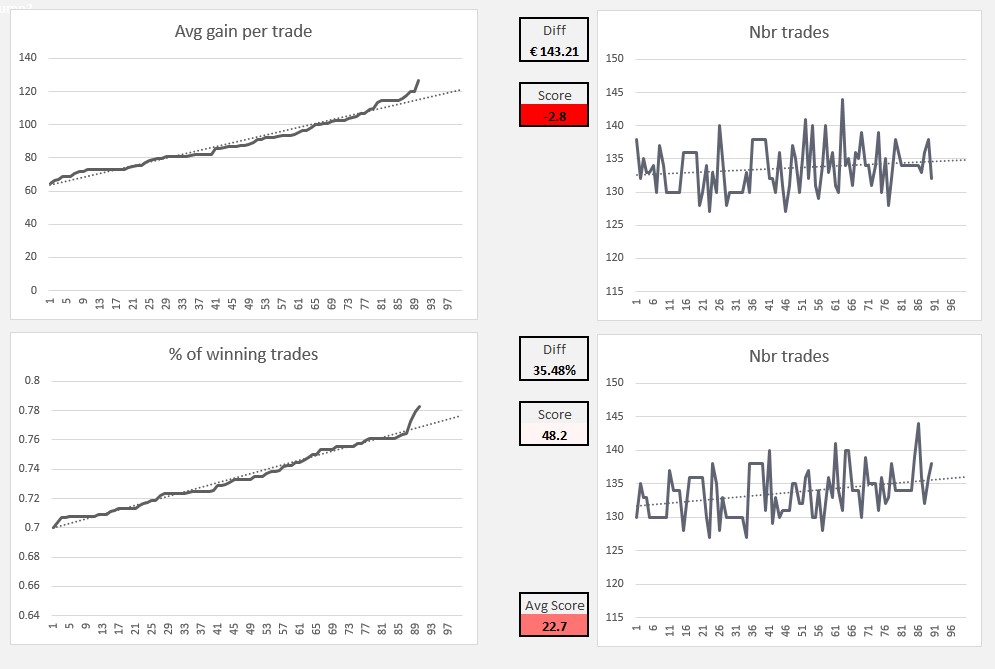

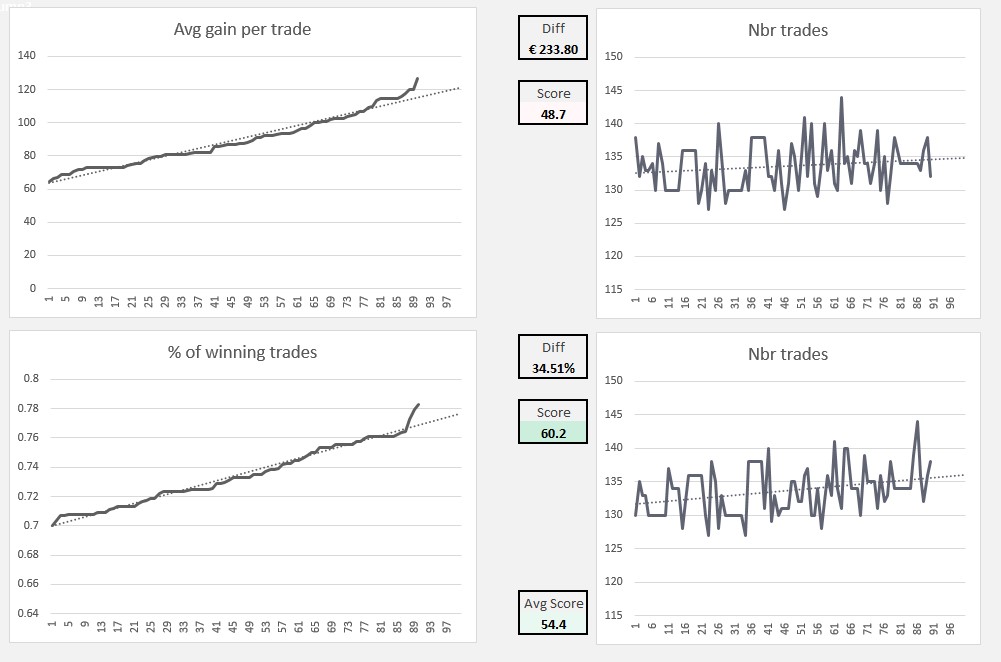

I will get the VRT tests sorted too, once I’ve got the data to load into the “very user friendly” Excel correctly. I get gain and win graphs, but not scores?

I also have a ML2 version from last week that so far looks good and I will post that. It uses ValueX for the boxsize and ValueY for the trailing stop loss, but its not graphing X and Y correctly – despite good profits and the fact that the X and Y algo codes are identical (apart from settings) to the correctly graphing Ehler’s Universal Oscillator posted earlier.

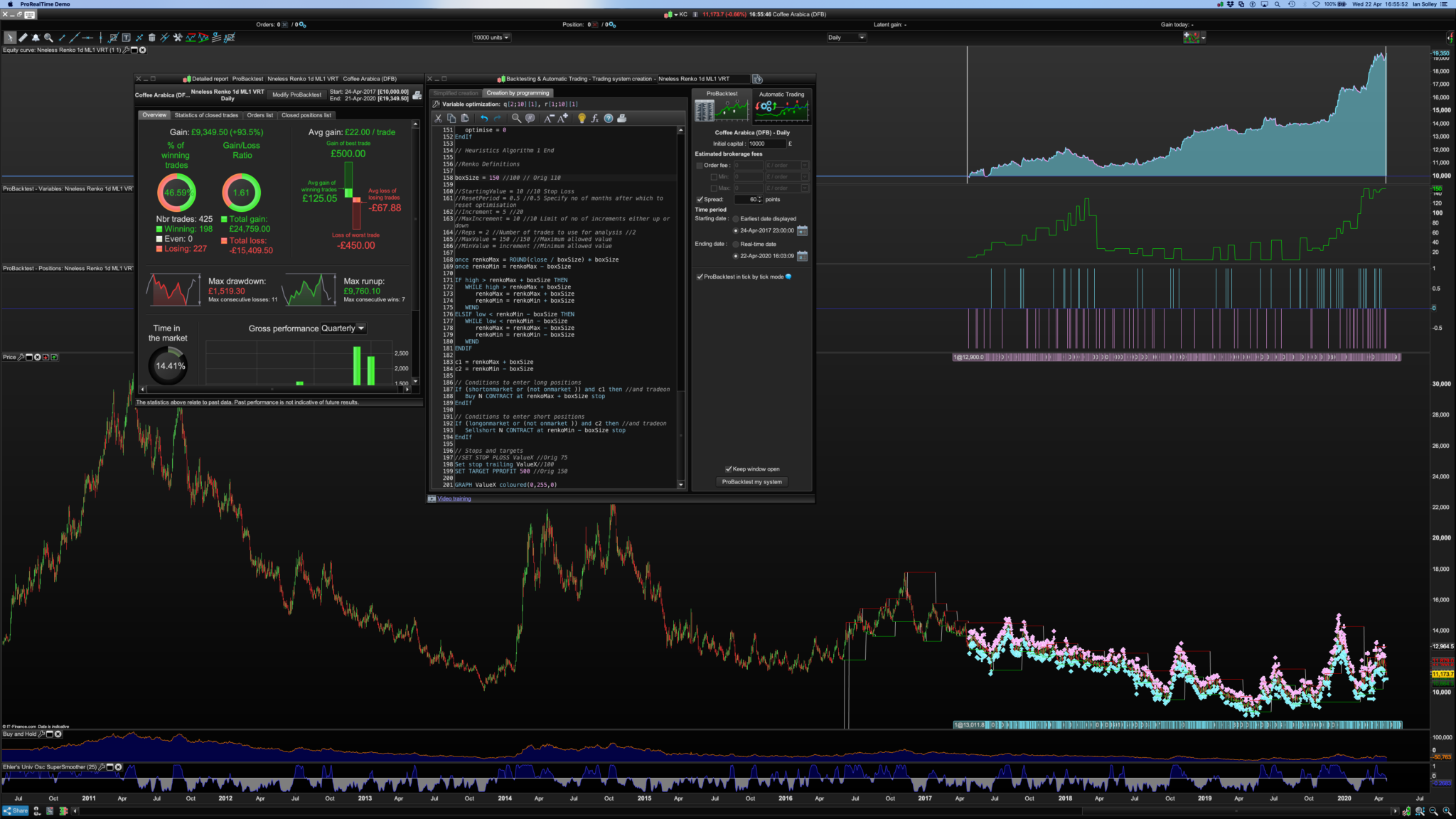

The bottom line is that this system still makes profits (with a 100 and 150 boxsize), with certain date ranges, particularly in the last years and last few months, but until coffee returns to normal spreads, it’s probably better to use this Renko ML1 system on instruments like low spread currencies and indices. See image #3 below this post.