I played around with settings Paul and simplified the entry and exit and re-added Reset Period for better performance. I’ll check out your latest v4 TS tonight or tomorrow. Cheers for posting it!

Is Once ValueX and Once ValueY doing anything?

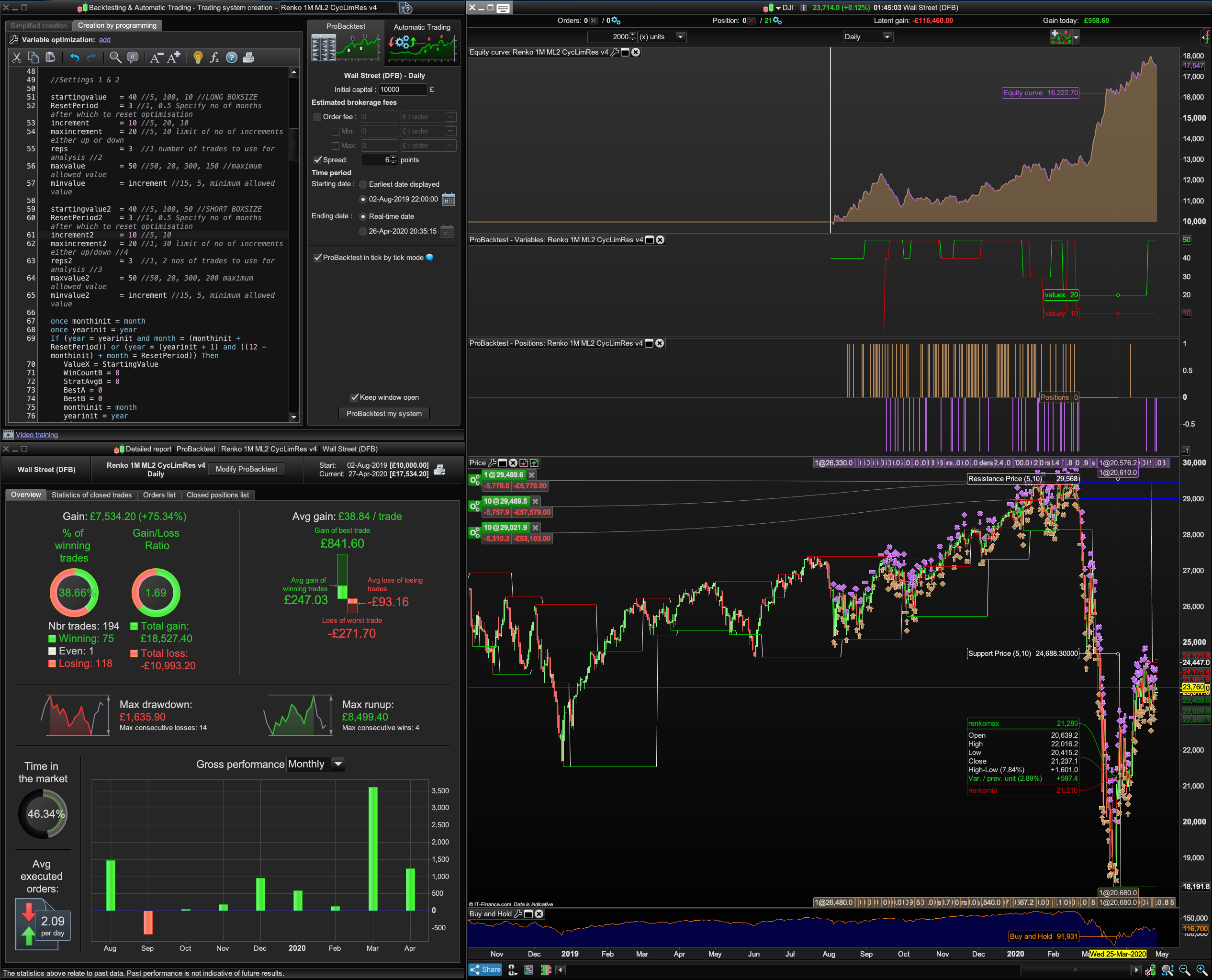

I also wonder with the fact that starting value =40 and max value = 50 how can the green graph show a ValueX and ValueY Boxsize to be smaller than that, at 20 and 10 respectively in this screenshot 1 below:? The gap between that starting value and max value is the basis of the ML stepping through values to find the right ones.. unless from optimisations and experience you can narrow it down to 40 to 50 boxsize from the get go. (It seems, based on optimisations to be 10 and 20 for both the BoxSize and the Trailing Stop).

//-------------------------------------------------------------------------

//main code : Paul/Bard Renko 1M ML2 v4b machine learning (ml2)

MLx2 applied to Long and Short Boxsize

//https://www.prorealcode.com/topic/machine-learning-in-proorder/page/3/#post-121130

//-------------------------------------------------------------------------

//https://www.prorealcode.com/topic/why-is-backtesting-so-unreliable/#post-110889

//definition of code parameters

defparam cumulateorders = false // cumulating positions deactivated

defparam preloadbars = 1000

//once mode = 0//1 // [0] with minimum distance stop; [1] without

//once minstopdistance = 20

//once percentage = 0 // [1] percentage; [0] points

//Money Management

//Capital = 10000 + strategyprofit //Current profit made by the closed trades of the running strategy.

N = 1//30*Capital / Close

heuristicscyclelimit = 2

once heuristicscycle = 0

once heuristicsalgo1 = 1

once heuristicsalgo2 = 0

if heuristicscycle >= heuristicscyclelimit then

if heuristicsalgo1 = 1 then

heuristicsalgo2 = 1

heuristicsalgo1 = 0

elsif heuristicsalgo2 = 1 then

heuristicsalgo1 = 1

heuristicsalgo2 = 0

endif

heuristicscycle = 0

else

once valuex = startingvalue

once valuey = startingvalue2

endif

if heuristicsalgo1 = 1 then

//heuristics algorithm 1 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise = optimise + 1

endif

//Settings 1 & 2

startingvalue = 40 //5, 100, 10 //LONG BOXSIZE

ResetPeriod = 3 //1, 0.5 Specify no of months after which to reset optimisation

increment = 10 //5, 20, 10

maxincrement = 20 //5, 10 limit of no of increments either up or down

reps = 3 //1 number of trades to use for analysis //2

maxvalue = 50 //50, 20, 300, 150 //maximum allowed value

minvalue = increment //15, 5, minimum allowed value

startingvalue2 = 40 //5, 100, 50 //SHORT BOXSIZE

ResetPeriod2 = 3 //1, 0.5 Specify no of months after which to reset optimisation

increment2 = 10 //5, 10

maxincrement2 = 20 //1, 30 limit of no of increments either up/down //4

reps2 = 3 //1, 2 nos of trades to use for analysis //3

maxvalue2 = 50 //50, 20, 300, 200 maximum allowed value

minvalue2 = increment //15, 5, minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once valuex = startingvalue

once pincpos = 1 //positive increment position

once nincpos = 1 //negative increment position

once optimise = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode1 = 1 //switches between negative and positive increments

//once wincountb = 3 //initialize best win count

//graph wincountb coloured (0,0,0) as "wincountb"

//once stratavgb = 4353 //initialize best avg strategy profit

//graph stratavgb coloured (0,0,0) as "stratavgb"

if optimise = reps then

wincounta = 0 //initialize current win count

stratavga = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i = 1 to reps do

if positionperf(i) > 0 then

wincounta = wincounta + 1 //increment current wincount

endif

stratavga = stratavga + (((positionperf(i)*countofposition[i]*close)*-1)*-1)

next

stratavga = stratavga/reps //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2"

//graph stratavga*-1 as "stratavga"

//once besta = 300

//graph besta coloured (0,0,0) as "besta"

if stratavga >= stratavgb then

stratavgb = stratavga //update best strategy profit

besta = valuex

endif

//once bestb = 300

//graph bestb coloured (0,0,0) as "bestb"

if wincounta >= wincountb then

wincountb = wincounta //update best win count

bestb = valuex

endif

if wincounta > wincountb and stratavga > stratavgb then

mode1 = 0

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 1 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 1 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 2 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 2 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

endif

if nincpos > maxincrement or pincpos > maxincrement then

if besta = bestb then

valuex = besta

else

if reps >= 10 then

weightedscore = 10

else

weightedscore = round((reps/100)*100)

endif

valuex = round(((besta*(20-weightedscore)) + (bestb*weightedscore))/20) //lower reps = less weight assigned to win%

endif

nincpos = 1

pincpos = 1

elsif valuex > maxvalue then

valuex = maxvalue

elsif valuex < minvalue then

valuex = minvalue

endif

optimise = 0

endif

// heuristics algorithm 1 end

elsif heuristicsalgo2 = 1 then

// heuristics algorithm 2 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise2 = optimise2 + 1

endif

//Settings 2

once monthinit2 = month

once yearinit2 = year

If (year = yearinit2 and month = (monthinit2 + ResetPeriod2)) or (year = (yearinit2 + 1) and ((12 - monthinit2) + month = ResetPeriod2)) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

monthinit2 = month

yearinit2 = year

EndIf

once valuey = startingvalue2

once pincpos2 = 1 //positive increment position

once nincpos2 = 1 //negative increment position

once optimise2 = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode2 = 1 //switches between negative and positive increments

//once wincountb2 = 3 //initialize best win count

//graph wincountb2 coloured (0,0,0) as "wincountb2"

//once stratavgb2 = 4353 //initialize best avg strategy profit

//graph stratavgb2 coloured (0,0,0) as "stratavgb2"

if optimise2 = reps2 then

wincounta2 = 0 //initialize current win count

stratavga2 = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i2 = 1 to reps2 do

if positionperf(i2) > 0 then

wincounta2 = wincounta2 + 1 //increment current wincount

endif

stratavga2 = stratavga2 + (((positionperf(i2)*countofposition[i2]*close)*-1)*-1)

next

stratavga2 = stratavga2/reps2 //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1-2"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2-2"

//graph stratavga2*-1 as "stratavga2"

//once besta2 = 300

//graph besta2 coloured (0,0,0) as "besta2"

if stratavga2 >= stratavgb2 then

stratavgb2 = stratavga2 //update best strategy profit

besta2 = valuey

endif

//once bestb2 = 300

//graph bestb2 coloured (0,0,0) as "bestb2"

if wincounta2 >= wincountb2 then

wincountb2 = wincounta2 //update best win count

bestb2 = valuey

endif

if wincounta2 > wincountb2 and stratavga2 > stratavgb2 then

mode2 = 0

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 1 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 1 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 2 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 2 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

endif

if nincpos2 > maxincrement2 or pincpos2 > maxincrement2 then

if besta2 = bestb2 then

valuey = besta2

else

if reps2 >= 10 then

weightedscore2 = 10

else

weightedscore2 = round((reps2/100)*100)

endif

valuey = round(((besta2*(20-weightedscore2)) + (bestb2*weightedscore2))/20) //lower reps = less weight assigned to win%

endif

nincpos2 = 1

pincpos2 = 1

elsif valuey > maxvalue2 then

valuey = maxvalue2

elsif valuey < minvalue2 then

valuey = minvalue2

endif

optimise2 = 0

endif

// heuristics algorithm 2 end

endif

//

boxsizel = ValueX

boxsizes = ValueY

//

renkomaxl = round(close / boxsizel) * boxsizel

renkominl = renkomaxl - boxsizel

renkomaxs = round(close / boxsizes) * boxsizes

renkomins = renkomaxs - boxsizes

//

if high > renkomaxl + boxsizel then

renkomaxl = renkomaxl + boxsizel

renkominl = renkominl + boxsizel

endif

if low < renkomins - boxsizes then

renkomaxs = renkomaxs - boxsizes

renkomins = renkomins - boxsizes

endif

// Conditions to enter long positions

Buy N CONTRACT at renkoMaxL + boxSizeL stop

// Conditions to enter short positions

Sellshort N CONTRACT at renkoMinS - boxSizeS stop

//

//if percentage then

//set stop %loss 0.25 %trailing 0.5

//set target %profit 2

//else

set stop ptrailing 50 //50 + 100

set target pprofit 500

//endif

//

graphonprice renkomaxl + boxsizel coloured(0,200,0) as "renkomax"

graphonprice renkomins - boxsizes coloured(200,0,0) as "renkomin"

graph ValueX coloured(0,255,0)

graph ValueY coloured(255,0,0)

I wrote the above last night, didn’t get round to finishing more testing before commenting. Now I’ve spent the day testing and thinking about what are we really best suited to apply our ML code to?

Is 1 x ML better than 2 x ML? (Depends if it’s the Ehlers Univ Oscillator, in that case ML2 is better, but with Renko I think ML1 is better).

But, after tons of optimisations I keep seeing low Boxsizes of 10 or 20 and ditto for the Trailing Stop. Is that achievable in the Demo/Live environment?

If so what’s the point of setting the starting value at 100 and Max Value to 200 if the ML would do better at figuring out if it’s better to use 10 or 20 in increments of 5?

Hence Paul’s tight Settings values of 40 and 50 appear to perform better.

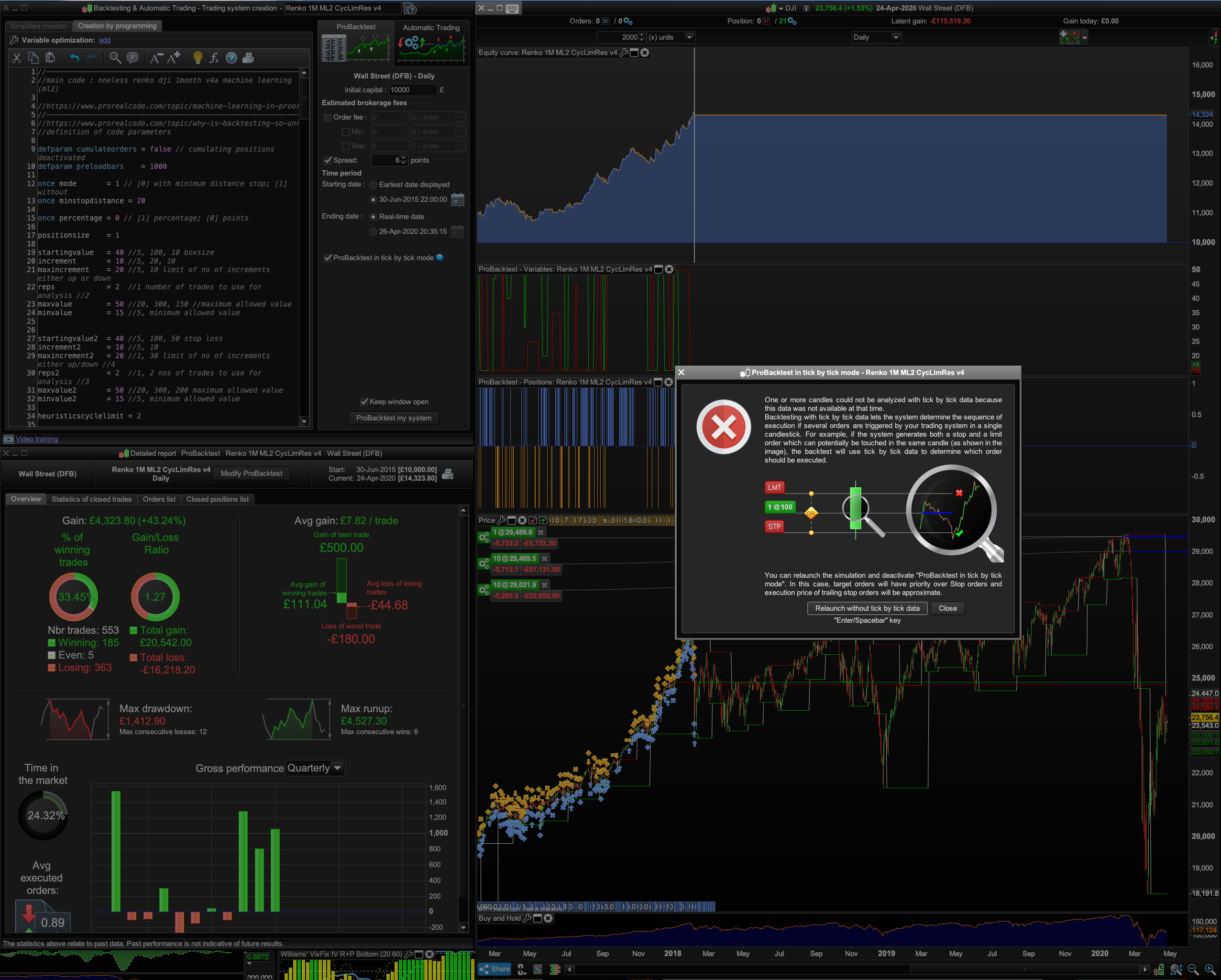

Note: testing with 100 for Boxsize and 100 for Trailing Stop and testing over very short Daily date ranges like Feb to April 2010, it doesn’t produce tbt warnings and the equity curves actually look more realistic: Renko TP ML1 ITF attached (set those values to Boxsize =10o and Trailing Stop =10o).

So… that just leaves the static “500” figure for Take Profit (TP) that I settled upon after lots of manual tests on different instruments like the Dow, £/$, Brent Crude etc.

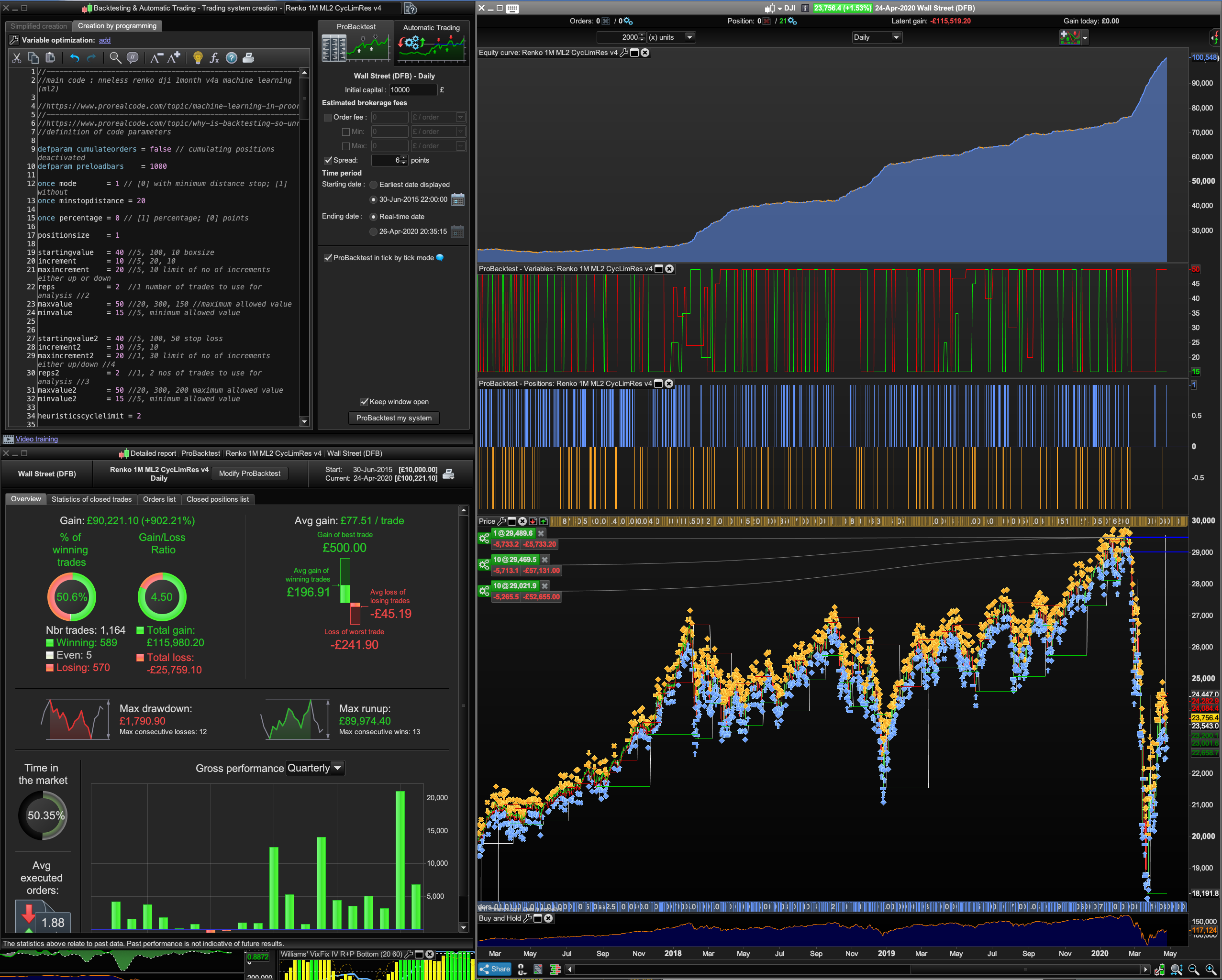

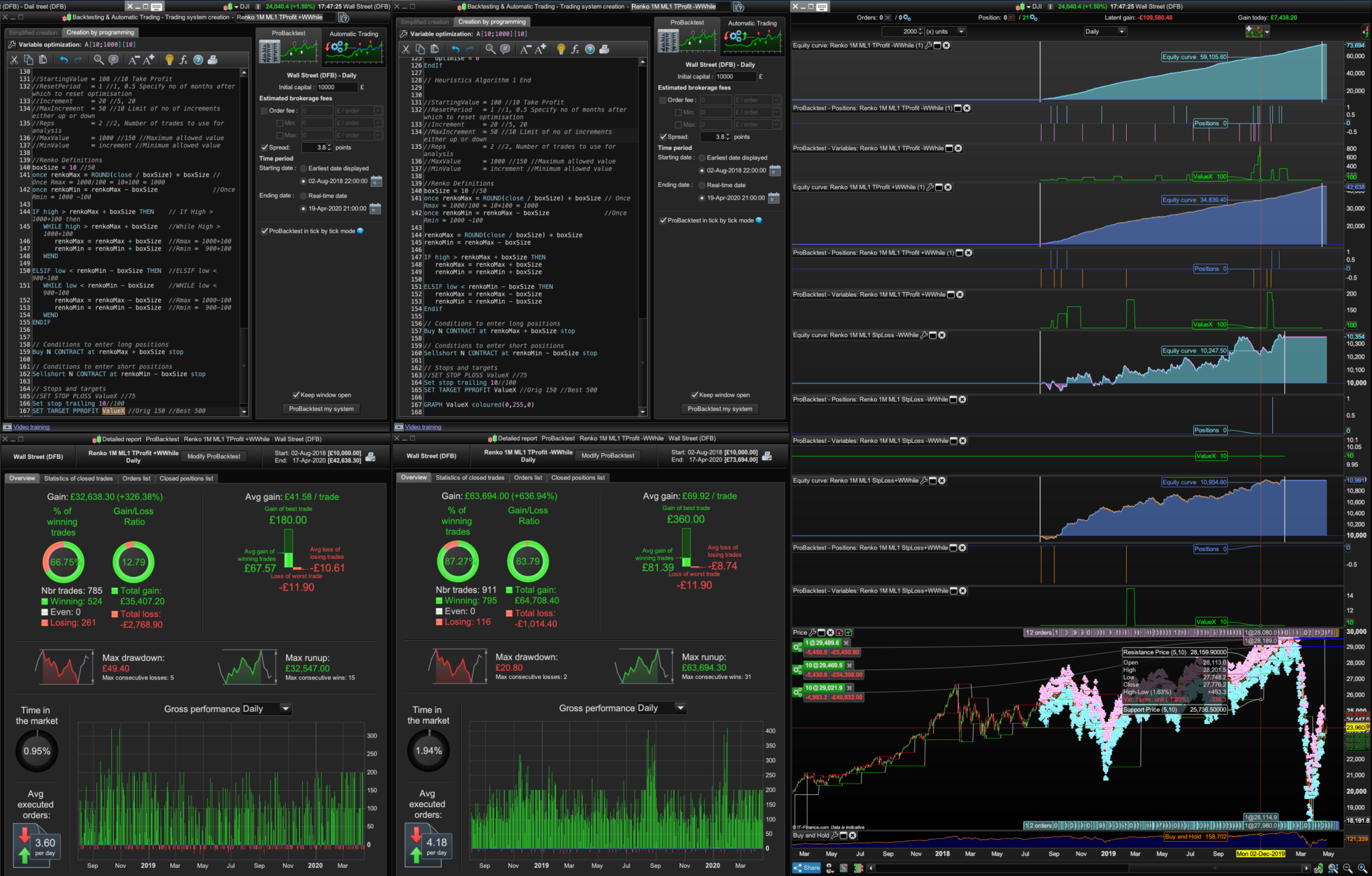

Well what if you apply ML1 to the TP whilst fixing the Boxsize and Trailing Stop at 10 (or 20) each? Please see screenshot 2 – ignore bottom two equity curves.

Now obviously this was a fully intentioned tbt test, but judging by the smoothness of the equity curve just didn’t turn out to be a tbt test or give you a warning.

Sometimes, however, if you keep playing with the date ranges — and eventually get that tbt failure warning, and if you’re lucky the offending Renko box that caused the tbt test to fail is at the end of your test dates, and if you hit “close” instead of “launch non tbt” test — you’ll still get to see what the system can do.

The point is even with these fantasy results the win ratios, the gain/loss ratio and profits are far higher targeting ML1 on the TP value than anything else I’ve seen fantasy result of!

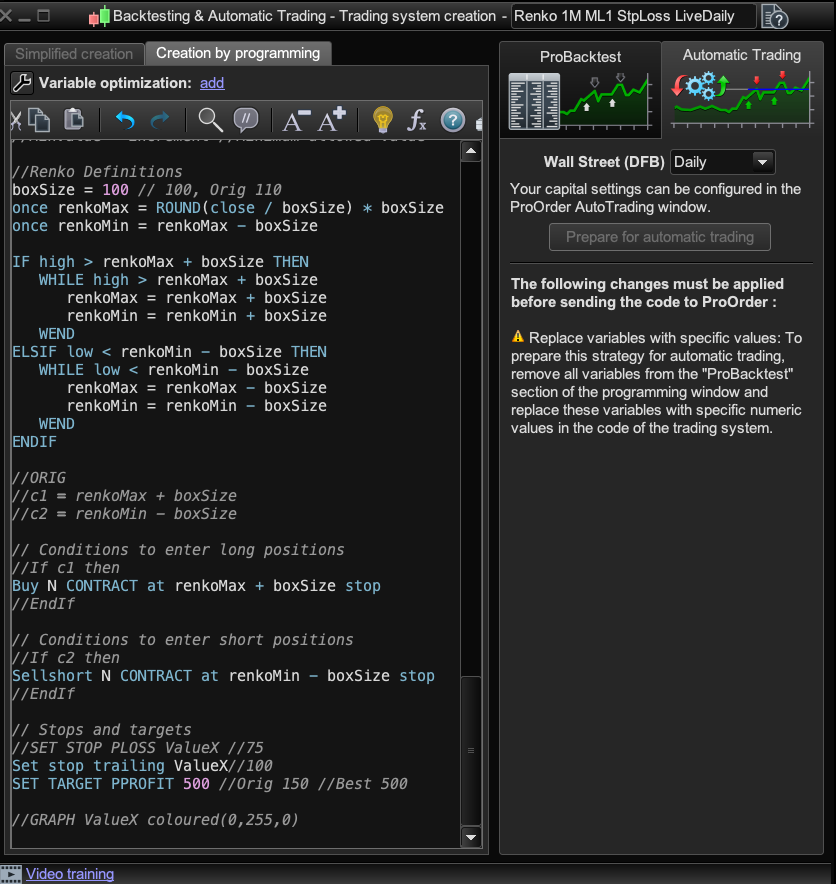

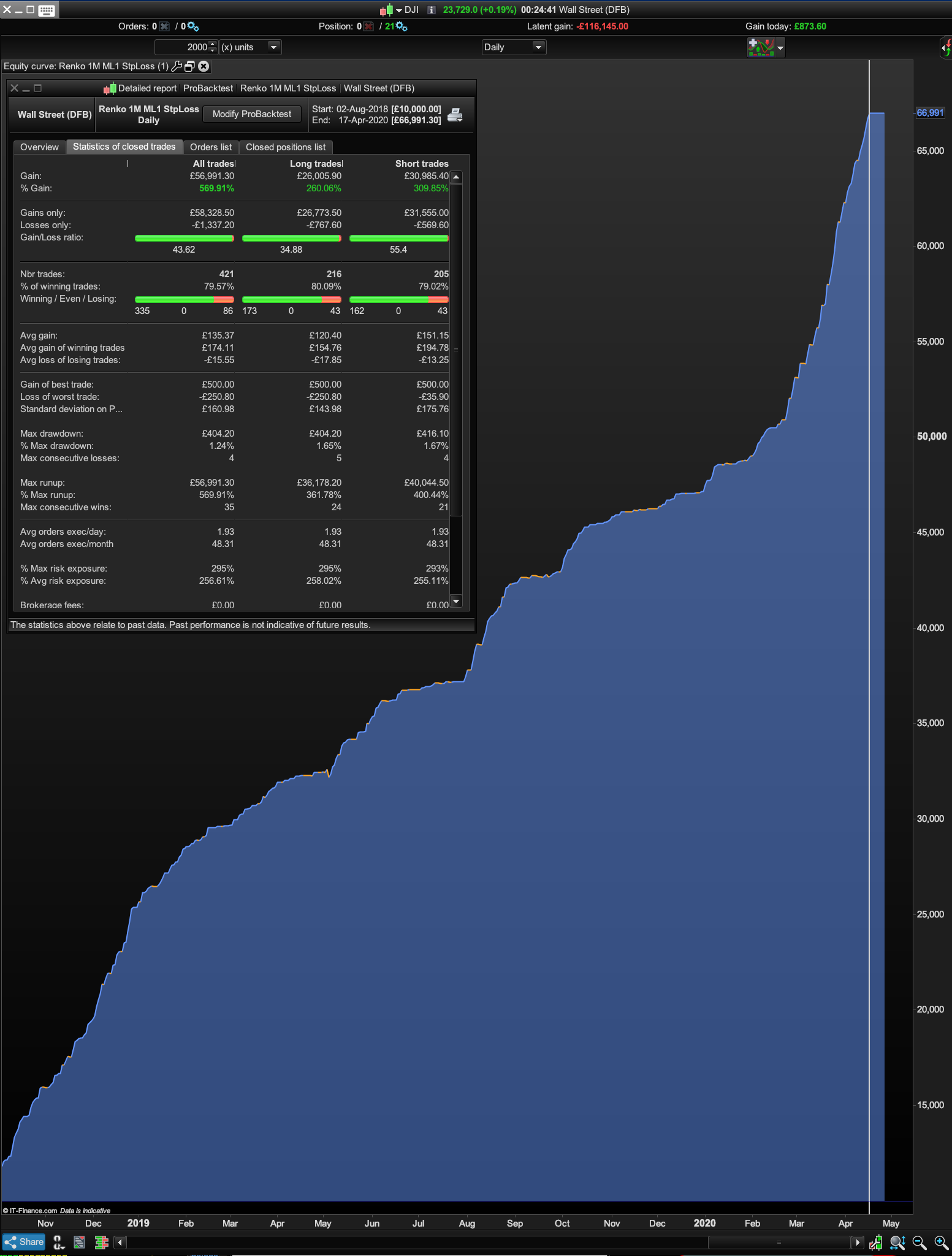

I also found that the Wend/While was better when ML1 was applied to the Stop Loss system but not always when using Wend/While on the TP system. Depends on the date ranges, if you set the dates to like £/$ Daily 02/03/ to present, the Wend While wins. If you set if to the last 5 months the without Wend/While system wins. So, is it worth applying ML to work out and switch between a system with Wend and While or without Wend and While, can that be done?

Right, that’s a lot to take in, but it’d be good to get peoples feedback and ideas. Cheers.