Correction re my reply to Jan’s question

adjust the setting of the variables automatically given the structure of price movements ?

It is adjust the setting of the variables automatically in relation to the results of the last 3 trades?

Trade4 would be used together with Trade3 and Trade 2 to repeat above.

Yes above is nearly correct … the last 3 Profitable Trades on a rolling basis (makes good sense) … due to code below at Lines 83 and 84 …

For i = 1 to Reps Do

If positionperf(i) > 0 Then

Jan

JanParticipant

Veteran

Grahal,

thanks a lot for your explanations.

Does anybody know what the *100000 is doing in the code below …??

I know positionperf is a %, but to then x by 100K it ends up making StratAvgA = figures that bear no relation to the strategy average profit which is more like 50 for Paul’s 1 second TF System?

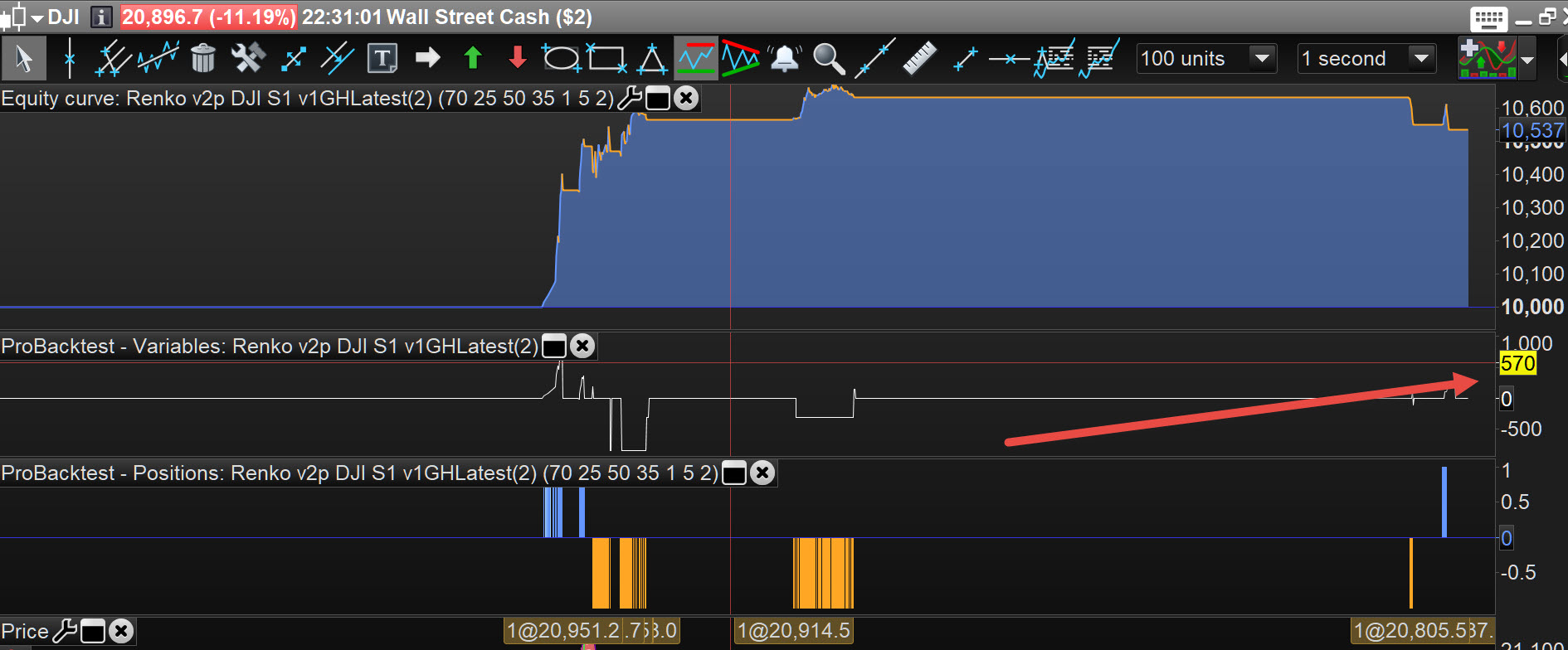

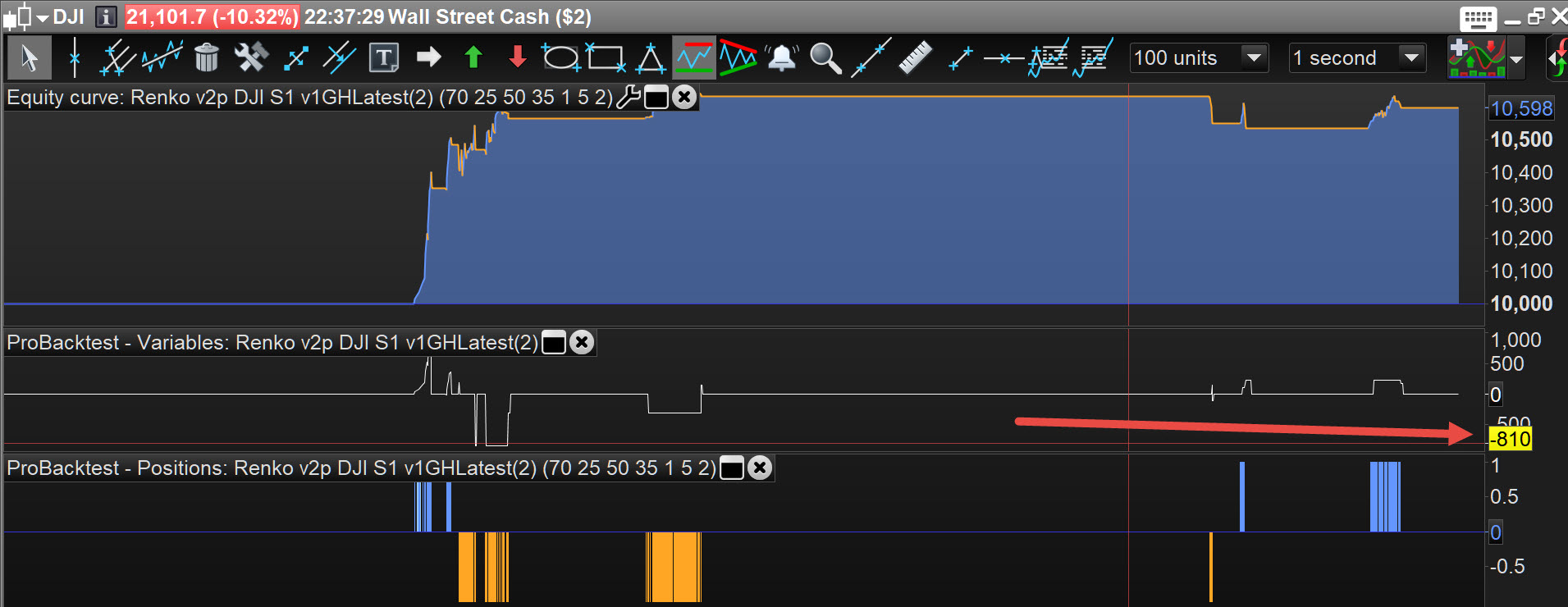

See the attached at the red arrowhead … 570 ??

Then on the next trade (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1) = – 810

Are we sure the Halgo is working correctly??

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

JanParticipant

Veteran

Good evening Grahal,

As far as I understand it, StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1) as coded in https://www.prorealcode.com/topic/machine-learning-in-proorder/page/3/ count the total profit of 3 trades of Strategy A and averages it ,

but the 100.000 seems to much to me.

You can graph PositionPerf to check whether you really need this fraction to multiply by 100.000

By the way, in the code of Juanj I can not find a strategy at all, I miss StratAvgA

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

//Graph (PositionPerf(1)*countofposition[1]*100000)*-1 as "PosPerf1"

JanParticipant

Veteran

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*–1)*–1)

As Reps = 3 , is this line of code summing the last 3 PositionPerf x resp. the last 3 count of position x 100.000 to the stratAvgA

I would agree Jan that is what is intended, but surely the multiplier should be the instrument price (as in DJI 21,600 currently)? Reason: positionperf is the % gain of postion(n).

As an aside … this is interesting for me to see how you guys (far far better than me at coding) do not find it easy to interpret another author’s code?

Reason: positionperf is the % gain of postion(n).

Correct myself again … when I use positionperf in the optimiser, I do always convert the fractional part (in my head) to a % to get a better feel for the gain relative to the TF … to gauge if it has reasonable expectancy to deliver on a regular ongoing basis.

Anyyywayyyy … a positionperf = 0.1 when converted to money would be 0.1 x 25600 = £256 (if on DJI at 25600 at £1 per point and lot size = 1).

So how / where the eff does the x 100,000 get into below …

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*–1)*–1)

in the code of Juanj I can not find a strategy at all

A basic strategy is in the post below …

I created a basic strategy on a second timeframe for testing

But below is a more complex strategy that began on this Topic but got split-off to it’s own Topic … best read the whole Topic to get the full picture?

for testing

would be 0.1 x 25600 = £256

save anyone correcting me … that should have read … 0.01 x 25600 = £256 (1% of 25600)

Hi Everyone, apologies for not being able to answer all the questions!

I am a full time trader and as you can imagine the markets have kept me very occupied the last week.

I will attempt to make some time tonight to address some of the unanswered questions here.

@GraHal thank you for the assistance here. With regards to:

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*–1)*–1)

This quite simply calculates the “capital” value of the performance multiplying the points value with the position size * the index/forex decimal point value (so yes it can be different from one market to the next)

100000 was used for the ZAF40 market

Bard

BardParticipant

Master

The HAlgo is a bit tricky to get working correctly, maybe – in Paul’s version you refer to – the HAlgo wasn’t working?

A few of us spent some time on it, but seems we put it on the back burner for a while? Other things pulling on our time I guess?

Be great if you could come up with a System where it clearly makes a big difference? A single variable System may be good?

The HAlgo can be duplicated and used on 2 (or even more variables) but it needs some dedication to get it all hanging together fully functional.

I did it with 2 variables and planned to try 3, but for no good or bad reason, my momentum slowed / fell by the wayside.

BardParticipant

Master

Interesting results

@Francesco! How do you measure / do a robustness test?

Interesting results @francesco! How do you measure / do a robustness test?

Take a look here

https://www.prorealcode.com/topic/day-month-year-strategy-robustness-tester/

You have to read and study most part of the pages in order to understand how it works.

Thanks to Vonasi’s work 🙂