Leo

LeoParticipant

Veteran

spread=0.7

IF TIME < 060000 THEN //(germany time)

spread=1.7*spread

ELSIF TIME>214500 THEN //(germany time)

spread=1.7*spread

ENDIF

Hi all,

I am working at the moment in others project but I am following this thread.

here is how I manage the spread issue, maybe is working for you as well

Thanks Leo maybe it is me being dim, but I don’t understand?

Spread is imposed upon us by IG / our broker, we can’t influence / change spread from within / by the code?

Aha I know you mean if we set stop / limit orders then we add / subtract spread appropriate to the trading hours for fixed spread markets, e.g. DAX.

No good for variable spread markets where spread flash widens 24 hours a day e.g. eurusd.

GraHal

LeoParticipant

Veteran

Yes,

sometime like I add orders like

BUY n CONTRACTS AT close+0.5*spread*pipsize STOP

And then stop loss + spread.

just be careful if you are using the market values or calculating by pips

So why should we expect results to be the same when we are ending / calculating variables / trade entry, exits at different points in time??

If you move the start point by just a few seconds and then suddenly a profitable strategy becomes a losing strategy then it is absolute proof that it is totally curve fitted. What you have with the two tests that start just a few seconds apart is an in sample and an out of sample test. So deciding on 30 seconds and ensuring that everyone is starting at the same round numbers will not suddenly make it a working strategy it will just mean that you are all using the same IS and OOS and trying to persuade yourselves that it works.

Vonasi … trying to persuade ourselves that it works … no more or less so than any other Strategy on here, be it 5 min / 1 hour / Daily / whatever??

Clearly we need to also do OOS testing / Walk Forward etc.

We weren’t planning to say … right everybody start now … it’s 190000 on Tue 19 Feb 18?? Oh aren’t we clever it works 🙂 🙂

Am I missing something in what you said / intended??

@ Grahal,

In response to your request, I studied 2 versions:

– a version on TF 1min the V5.10 (debugging on 40,000 units) 8 trades / day

– a version on TF 30sec the V5.12 (debugging on 20,000 units) 20 trades / day

if we want to compare the V5.10 to a strategy 1 trade / day it would take 320,000 units.

if we want to compare the V5.12 to a strategy 1 trade / day it would take 400,000 units.

if you want out of curiosity to push the V5.10 to 100,000 units it’s as if you were testing a 1 trade / day strategy on 800,000 units, which nobody can do on PRT. on the V5.12 the problem does not arise you have not more than 20.000 units of history.

@Gertrade

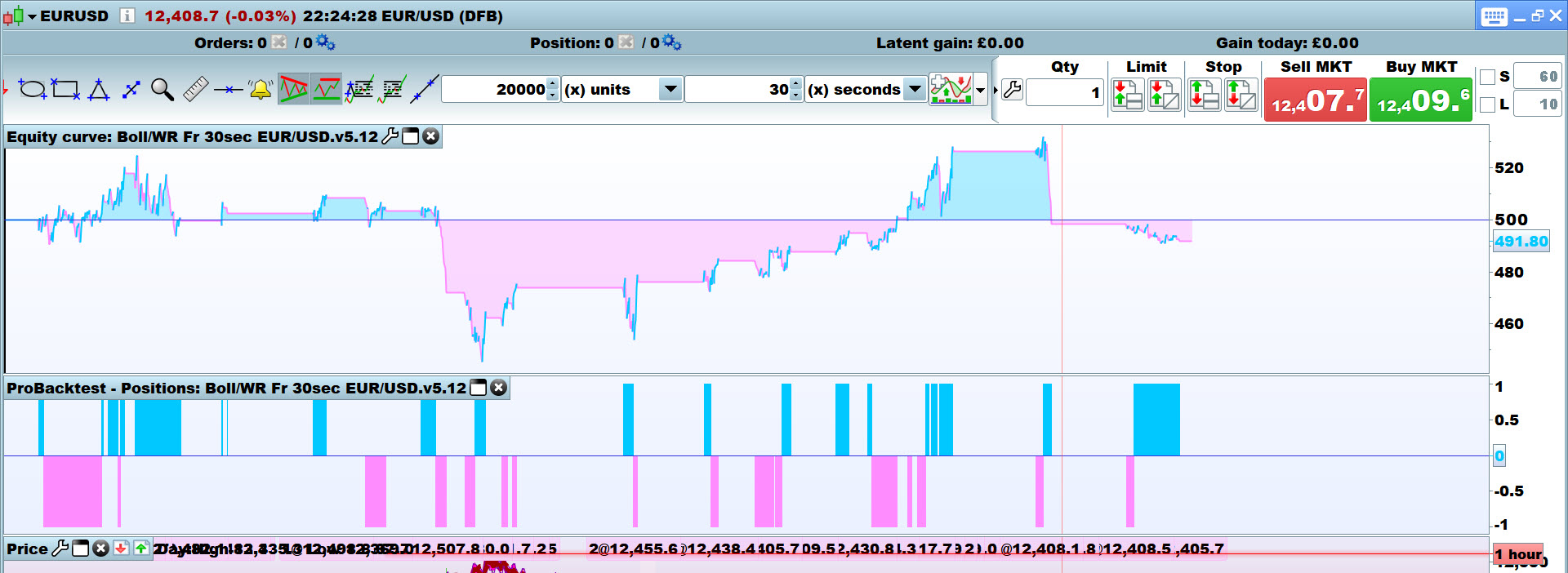

Are your equity curve and profit figures acceptable for the above 2 x Algos?

Below is what I get over 20,000 bars on the 30 Sec version.

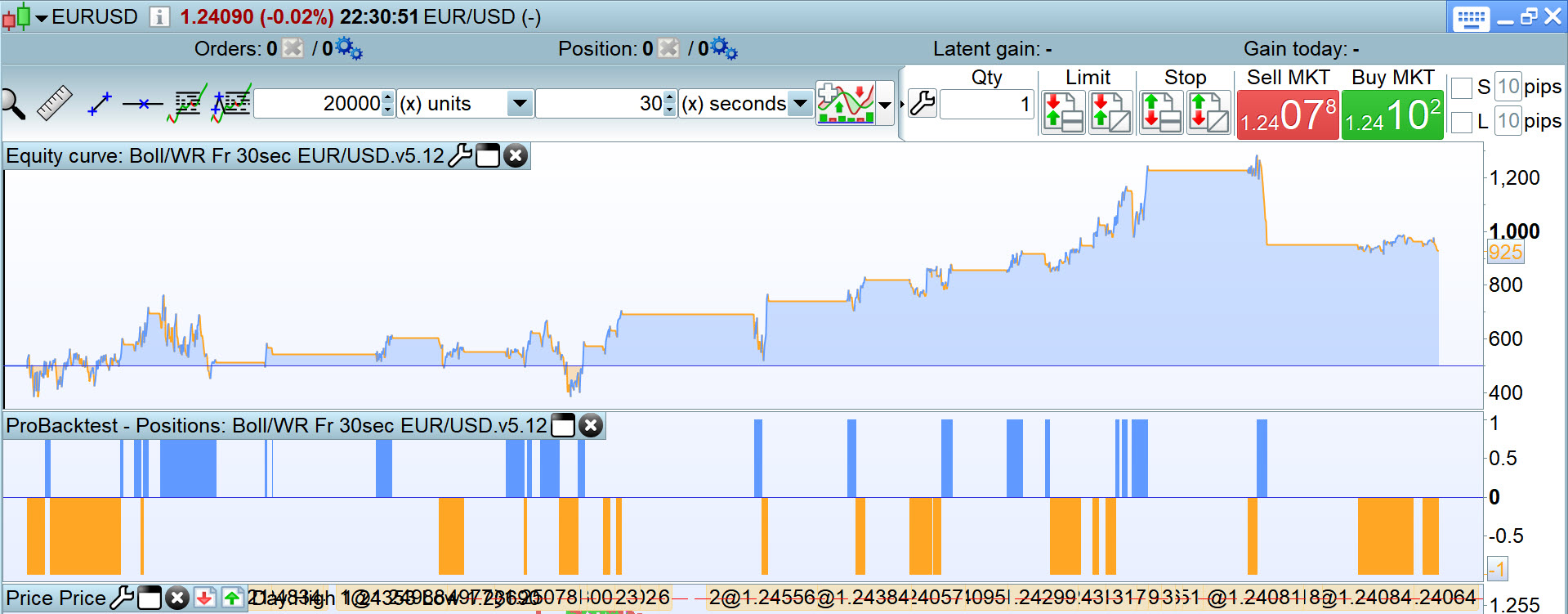

You are running CFDs right and I am running spreadbet.

I will try on CFDs also … hang on.

GraHal

PS The good results are on CFDs!!!

So there is a big difference between CFD and spreadbet … this will be the same for all Algos, but probably more pronounced difference the lower the Timeframe

Am I missing something in what you said / intended??

You are possibly missing something but I cannot think of a better way to explain it 🙂

If you write a strategy and backtest it and it works and then simply move the start point and it doesn’t then you have just done an IS test followed by an OOS test and the results tell you it is a failed strategy. Do lots of tests from lots of different random start points and if more sample periods are profitable than there are sample periods that make a loss and the cumulated profits are bigger than the cumulated losses then it might be worth continuing with. Obviously the length of test period is a major factor in your decision making and with 30/28 second strategies your testing period is severely limited so most test results should be looked at rather sceptically in the first place.

At the moment from my reading of this thread there seems to be a lot of discussion regarding time frames and if you have to rely on a time frame as a critical variable to make a profit then you are in my humble opinion barking up the wrong tree. Wouldn’t it be lovely if the difference between making a big profit or not was simply down to the difference between 30 seconds or 28 seconds? Forget all about the simple mathematics of probability we just need to wait two seconds before we start!

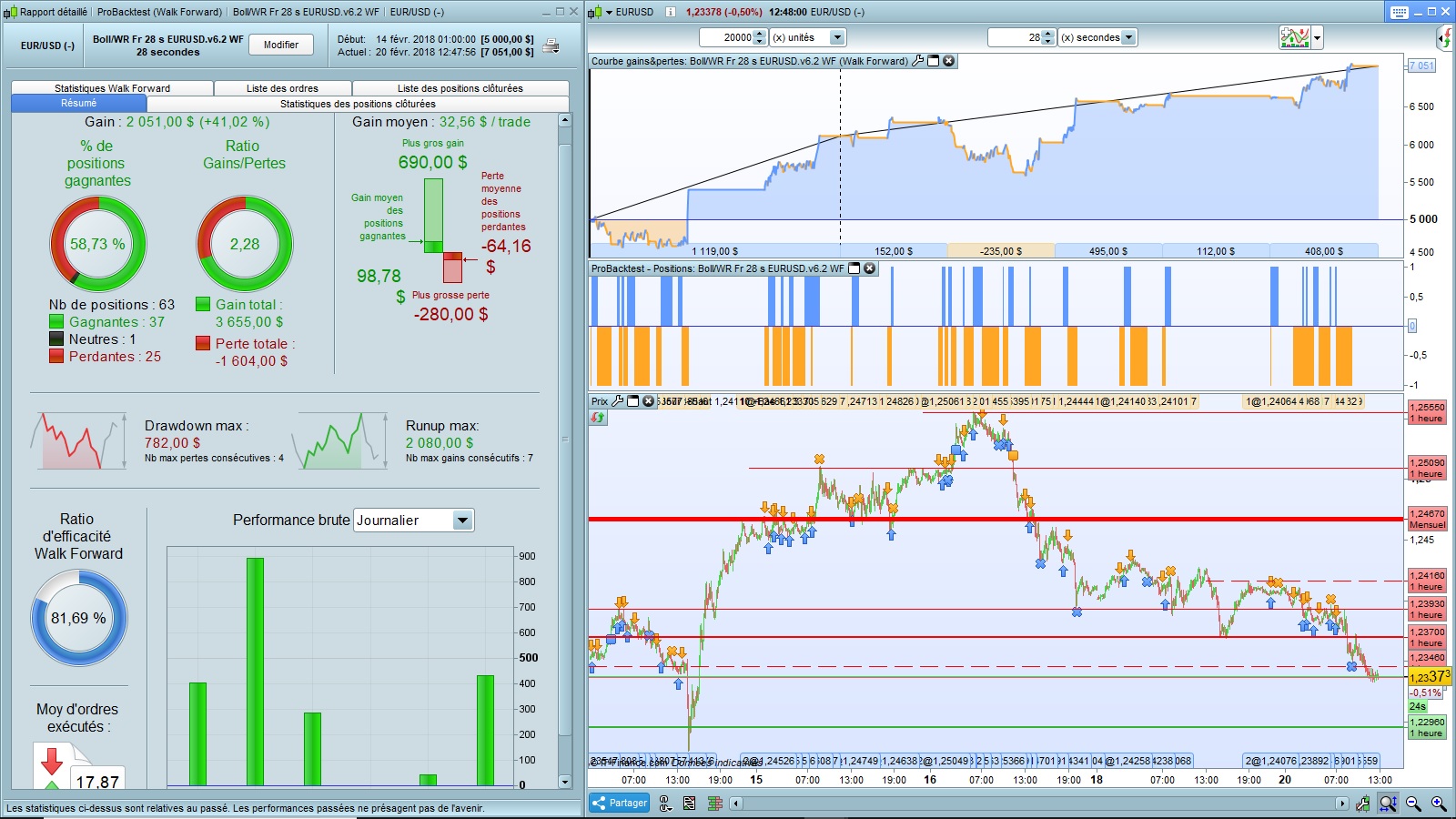

Hi everybody,

Today is a big day ! I think I have the finished version that I wanted to get. I have an indication that gives me the health of a version, it’s my MaxOrders variable related to Money Management. Of all published versions, I had never exceeded 9 lots. On V6.1, the MaxOrders variable is mounted to 36 lots.

I stayed on a TF 28 sec, for the simple reason that I’m in a progressive approach and we do not change a winning team in the process.

I give you this version, which I hope will not contradict me on ProOrder.

And here is his little sister the v6.2 with an additional time slot from 10h to 11h with graphics and their results (Equity Curve and Walk Forward on 20,000 units).

Good trades to all.

Wouldn’t it be lovely if the difference between making a big profit or not was simply down to the difference between 30 seconds or 28 seconds? Forget all about the simple mathematics of probability we just need to wait two seconds before we start!

Thank you for the point well made and I agree!

My thoughts were that using a maverick TF – in this case 28 sec – means that we introduce one further issue into the mixing pot. With 28 sec TF we almost certainly would never be trading / backtesting / enter / exit on the same bar so it saps enthusiasm to find out what / where the issues are if results are not comparable between users / Platforms etc.

Looking at the chart and placing orders in real time, I realized that many of my buy or sell signals were ahead of the trend of a few bars. So I decided to delay these signals from 1 to 4 bars as needed. The gain is consistent and represents + 20%.

It is the V6.4 that carries these improvements.

Hi guys – Been absent for a while working on other things so observing with interest, back in the saddle now though. Liking the discussion here of new ideas. Thanks to Jusmih1 for kicking it off and Grahal and Gertrude for running with it.

I have to say that I tend to agree with Vonasi in that with this short a time frame as 28s, it’s a roulette wheel. I’m not sure with this limited amount of data and the difference in calculation periods as discussed above, that there is any merit in the results that would give you confidence in the long run. I have tested it in live (v 4 & 4.5) and none of the live results matched up with the backtests or were profitable. Sure, sometimes they made money but in the end it was always negative. I’m testing the 5m version which have more history to go and although they initially showed some promise they too are underwater. But I am likely to let those run for a bit to give them time too breathe. Will post on here if any results look promising.

Happy to be proven otherwise that the 28s one does indeed provide consistent results in live, that would be great 😉