@grahal, thank you for your answer.

I could not resist the temptation to visualize if the results were good with a money management.

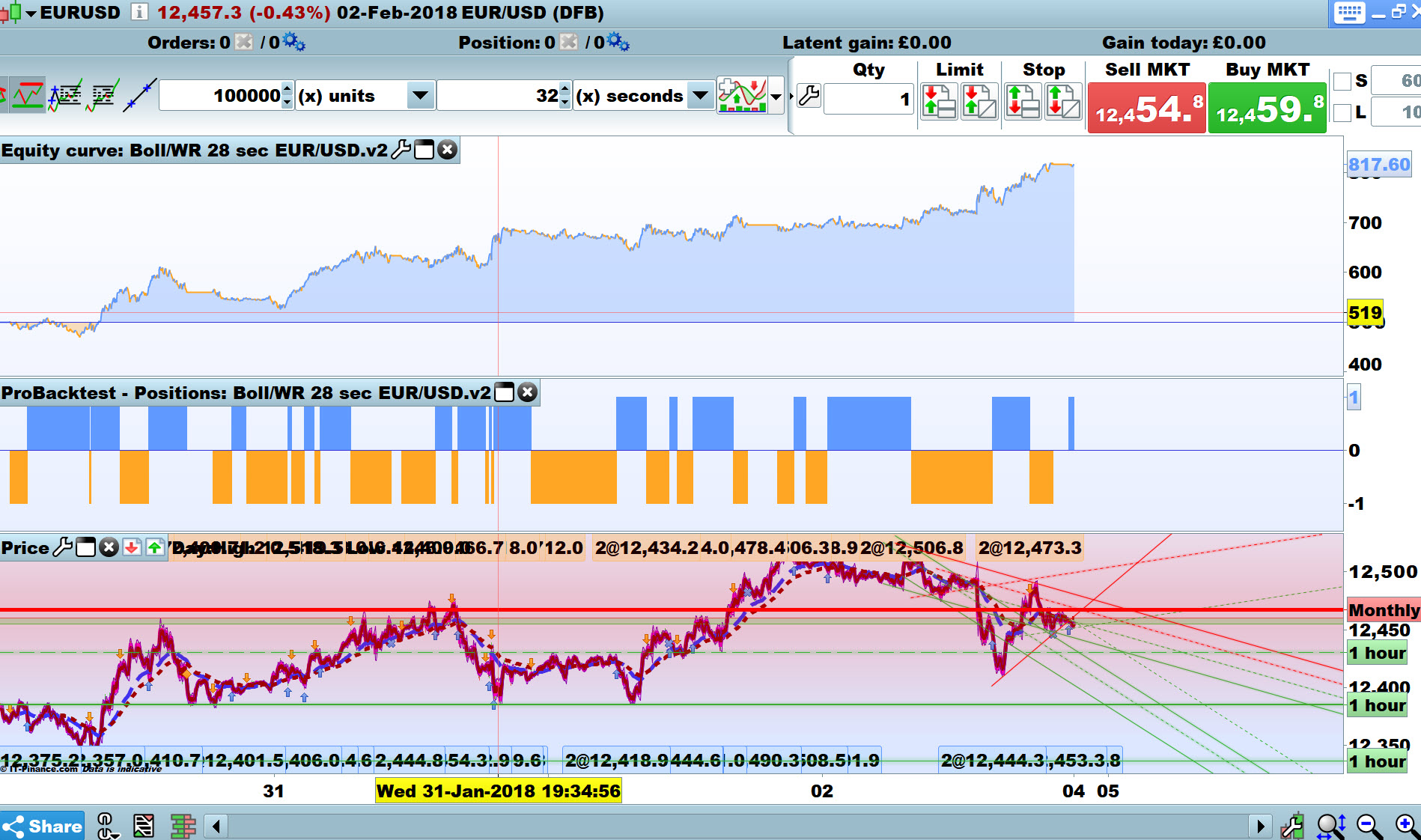

With 1 lot and a TF of 28 sec, the results seem correct.

I confirm that a TF greater than 15 sec works with ProOrder.

When it comes to my portfolio, I am taking an intermediate solution that will implement this excellent strategy with reasonable money management.

Can’t believe nobody’s got some ‘gems’ to offer re 28 sec TF so much more successful than 30 sec TF … see post #61332 .

What I suggested wouldn’t be the reason as every 28 seconds the gap between 28 and 30 would get bigger … 28, 56, 84, 112 etc. Although it would come back to 2 secs again at some point!

Go on have a go, doesn’t have to be accurate or tested, brainstorm anybody!? 🙂

GraHal

Go on have a go, doesn’t have to be accurate or tested, brainstorm anybody!?

Just happens to fit? A good test of curve fitting is to check results either side of the optimized variable (in this case time) and if the strategy suddenly fails it tells you that it is curve fitted. Just a guess but it would be enough to tell me to give up on the strategy and put my efforts elsewhere. IMHO.

Here’s a few either side.

I am leaning towards … just happens to fit or not fit … mainly cos I can’t think of anything better 🙂

Back to the code I guess to see if feasible that conditions are met / not met / met again every few seconds. Price goes up and down making it possible?

I do not understand why the TF 28 sec is better than the TF 30 sec, it is just a search for optimization that let me to choose the TF 28 sec.

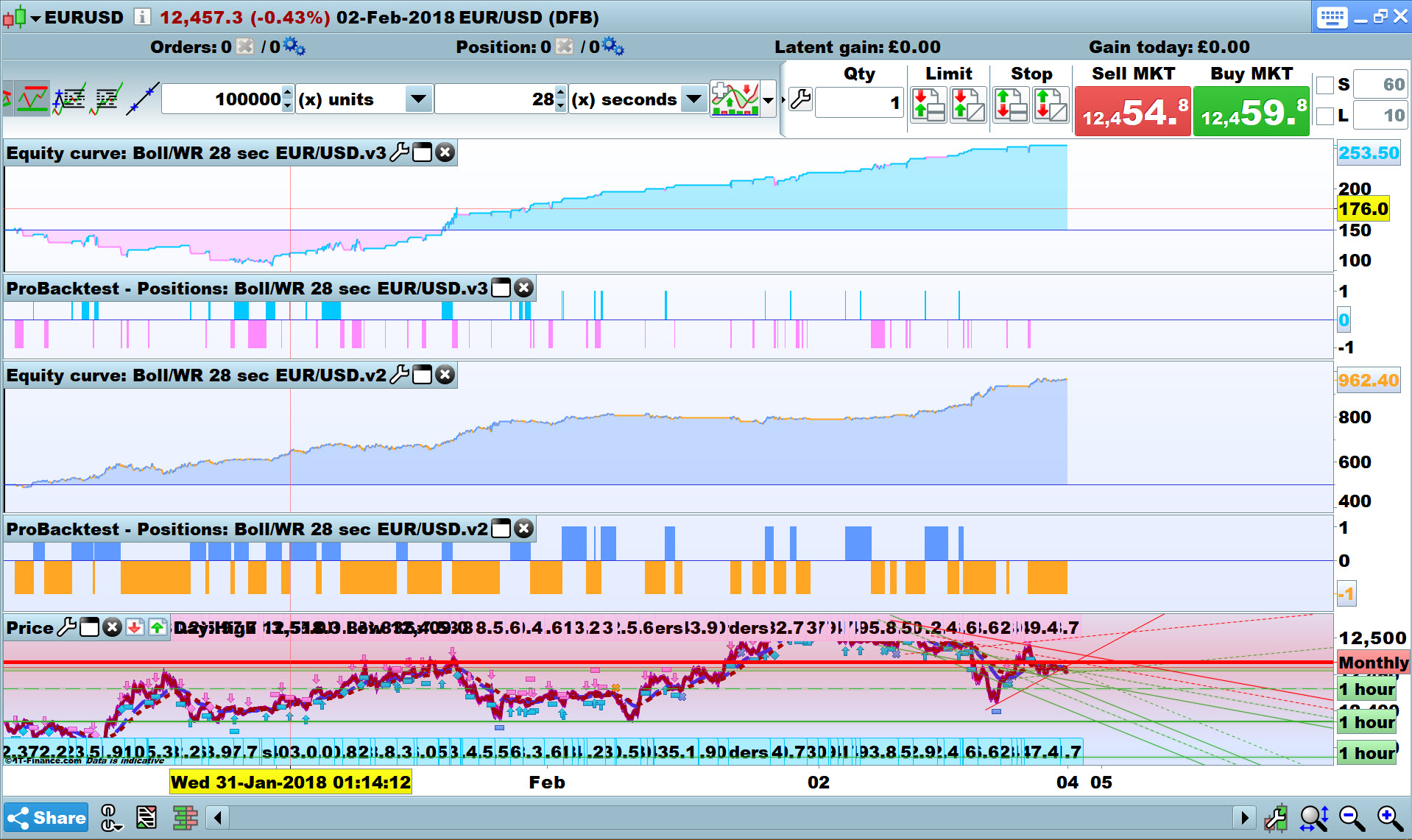

I progressed in this search and implemented some code concerning trailing stop and take profit as well as an exit for all trades.

the improvement is noticeable on several parameters:

– the starting capital has been lowered to 150 €

– the gain has progressed

– the drawdown has been reduced

– the runup has been increased

– the equity curve seems better

– the maximum number of lots has been fixed at 20 (variable MaxOrders to be positioned according to your choice from 1 to x lots)

– the progression of number of lots from 1 to 20 is more progressive

I look forward to your comments on this optimization.

It’s not about time but about price. Comparing a 28 seconds timeframe to a 30 seconds one is like comparing a 5 minutes one with a 15 minutes one. They’re not the same. Remember that indicators calculation are based on periods.

Remember that indicators calculation are based on periods.

So then technically it is about time! 🙂

@Gertrade if I change lot size to 1 (for comparison) then results are not as good V3 compared to V2?

@Gertrade please could you post Walk Forward results on here?

Pick the variable that makes the most changeable difference to results?

@grahal ,

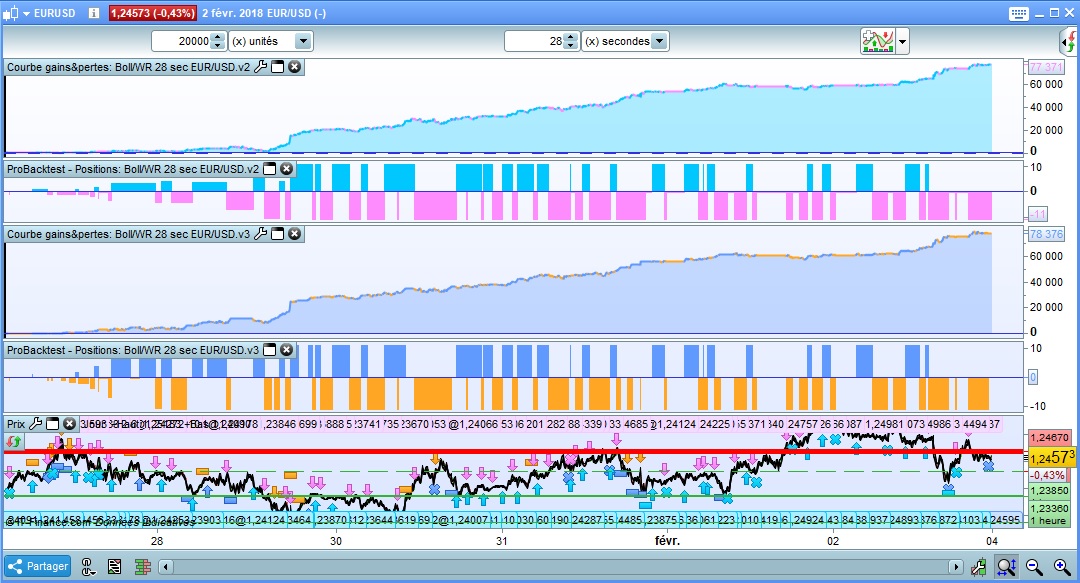

I compared the V2 with the V3, the V3 exceeds the V2 with a variable MaxOrders > 10 (see graph below)

I tested the V3 in WF mode by taking the variable -99 from line 50

I get a WF efficiency ratio of 98%, which looks good (see graph below)

I am waiting for your comments

So then technically it is about time!

Indeed! I wanted to point out that, for a single candle different, the calculation of an indicator is completely different and since the strategy is based on informations of indicators and not direct price, it is logical that the results are also different.

logical that the results are different … agreed / expected but kinda scary / unexpected they are sooo different?

To enter many trades 2 seconds later and get such difference in results between good (28 sec TF) and rubbish (30 sec Tf) … that’s the conundrum.

The acid test will be during Live Trades … as always.

@Gertrade re … I don’t know OOS … have you read below?

https://www.prorealcode.com/blog/learning/strategy-optimisation-walk-analysis/

https://www.prorealcode.com/blog/learning/prorealtime-walk-analysis-tool/

Results of all versions of this Strat seem to good to be true so they have to be surely??

GraHal

@Grahal,

Thanks for the explanation of the term OOS(Out Of Sample). This is included in the WF method.

The results are apparently good in WF. It remains only the test on Proorder Demo account to validate this strat.