Ah ok never noticed that, i set v1 running on sat night, and then set v3 running sunday night, but market was closed, would that still make a diffrence to live results.

just wanted to say thanks to you all, really enjoying the conversations going back and forward😀

aha it didn’t click with me it was Sat and Sun I just saw dates that were not same. In that case (market closed) the difference in time running shouldn’t make any difference?

I managed to master this difficult day of trading. I reviewed each variable of the Strat and optimize each of them on 20,000 units including the day of 05/02.

below the chart of the backtest of the day of 05/02 as well as a new version V2.3.

Hi everybody,

I am satisfied this morning with V2.3, even if it is still early.

I did the validation tests (OOS) with the WF module, it’s good.

(below WF Graph)

Thank you for your participation. I am also satisfied with this collaboration.

I am always satisfied with my results of V2.3 today in backtest, that corresponds to my expectations.

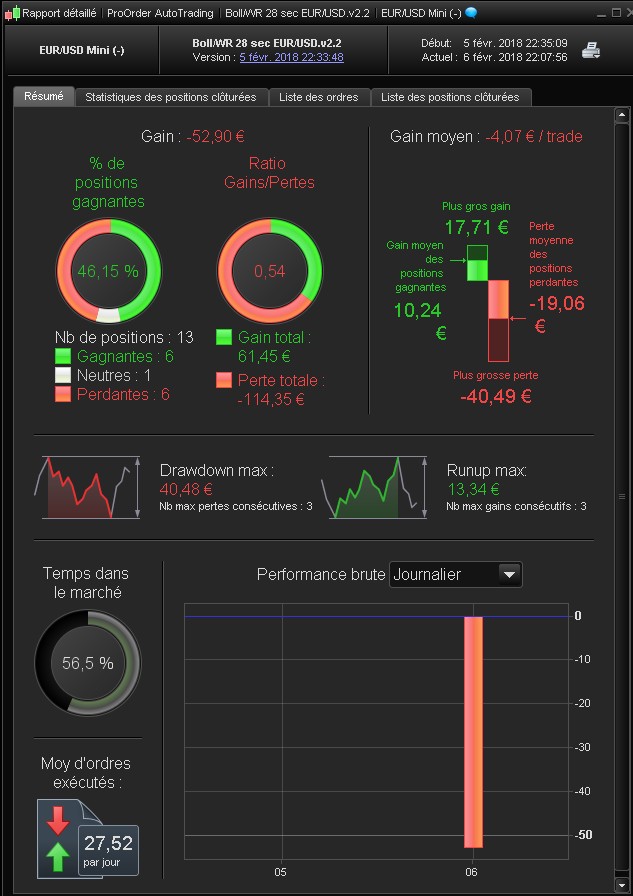

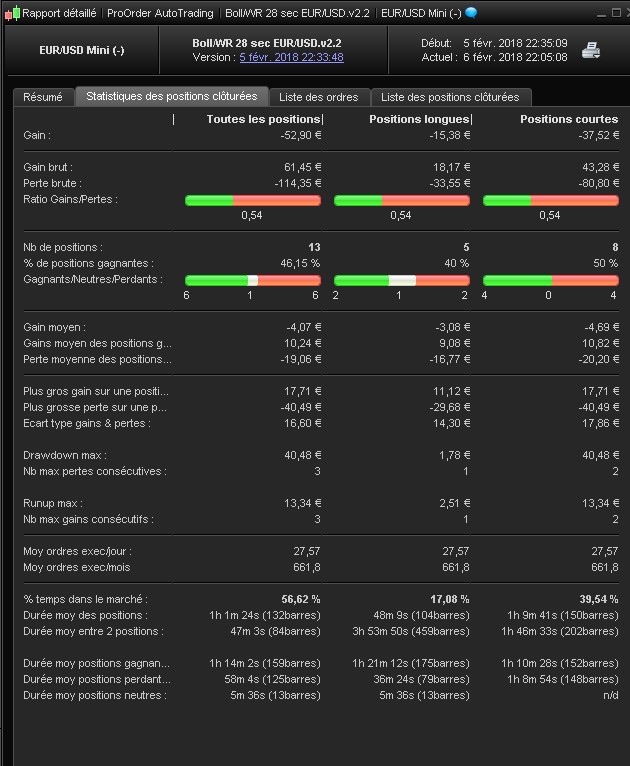

On the other hand, there is a problem with the Live Proorder Account Demo, it does not correspond to the backtest, there are orders in addition, others which are absent.

All this to tell you that it is a catastophe in terms of Proorder results.

I do not know what to do, only Prorealtime can intervene.

below as an attachment:

– the Backtest is the graph at the top

– the Live Proorder demo account is located on the graph at the bottom

I’m sorry, I made a mistake in the top graph the V2.3 has a TF of 18s and that gives good results.

It is not possible to compare a backest on TF 18s with Proorder on TF 28s

I have the system in real time since today 00:24:50

Bad Performance till now: 10 Trades 5 wins, 5 lost, -47$…. I´ll let it run 24 hours. But I don´t think it will have good results at the end of the day.

I hope it’s on a demo account, it’s a little early to risk your own money.

I am studying the V2.3 on the TF18s. The results (OOS) on WF are good (see Graph below).

The gain on 20,000 units (max history) is lower, but what matters is the durability of the Strat.

A few thoughts on a straightforward / easy way to use WF, taking 20,000 bars as an example …

For 20,000 bars then a Strat should be optimised (not using WF) over the oldest 14,00 bars and then run using WF (setting at 70% / 30%) over the full 20,000 bars.

The most recent 6,000 bars then would be the best approximation to what might be expected in Live Trade as the 6,000 bars are a true Out of sample set of data (due to not being part of the optimised period).

If optimising is done over the 20,000 bars then there is no Out of Sample period over which to check for robustness of the Strat.

How are we using WF to test Strats on this Thread?

GraHal

Hey GraHal, your thoughts are good. This is the easiest way to produce reliable optimization, manually. The WFA tool is only an automatic tool to make it multiple times in the past, but you can also make only 1 iteration (1 IS+1 OOS) and it would be the same as the manual process you are talking about.

Hi everybody,

Thanks for that interesting strategy ; I hope we’ll get something good at the end !

I run the 2.2 version in real time since yesterday 22:35 (on a IG demo account).

With the low IG spread (0.6 daytime), I have bad performance too. Average losses are much bigger than profits. Notice that the gain/losses ratio is quite the same for short and long position.

I confirm that my backtests were great too. We now have to find out why there are so much differences between backtests and real results.

Regards

Are we backtesting on data / bars that have not been part of the optimising period?

If the backtest period is part of the optimised period then when we run it Live or Demo Real Time Trade (going forward from the optimised period) and results are not good then we have curve fitted to a set of scenarios / bars / triggers that give good results??

The same scenarios / bars / triggers (that we optimised for) are not occurring in the up / down / sideways cycle of price movement to give those same good results.

GraHal

@ GraHal

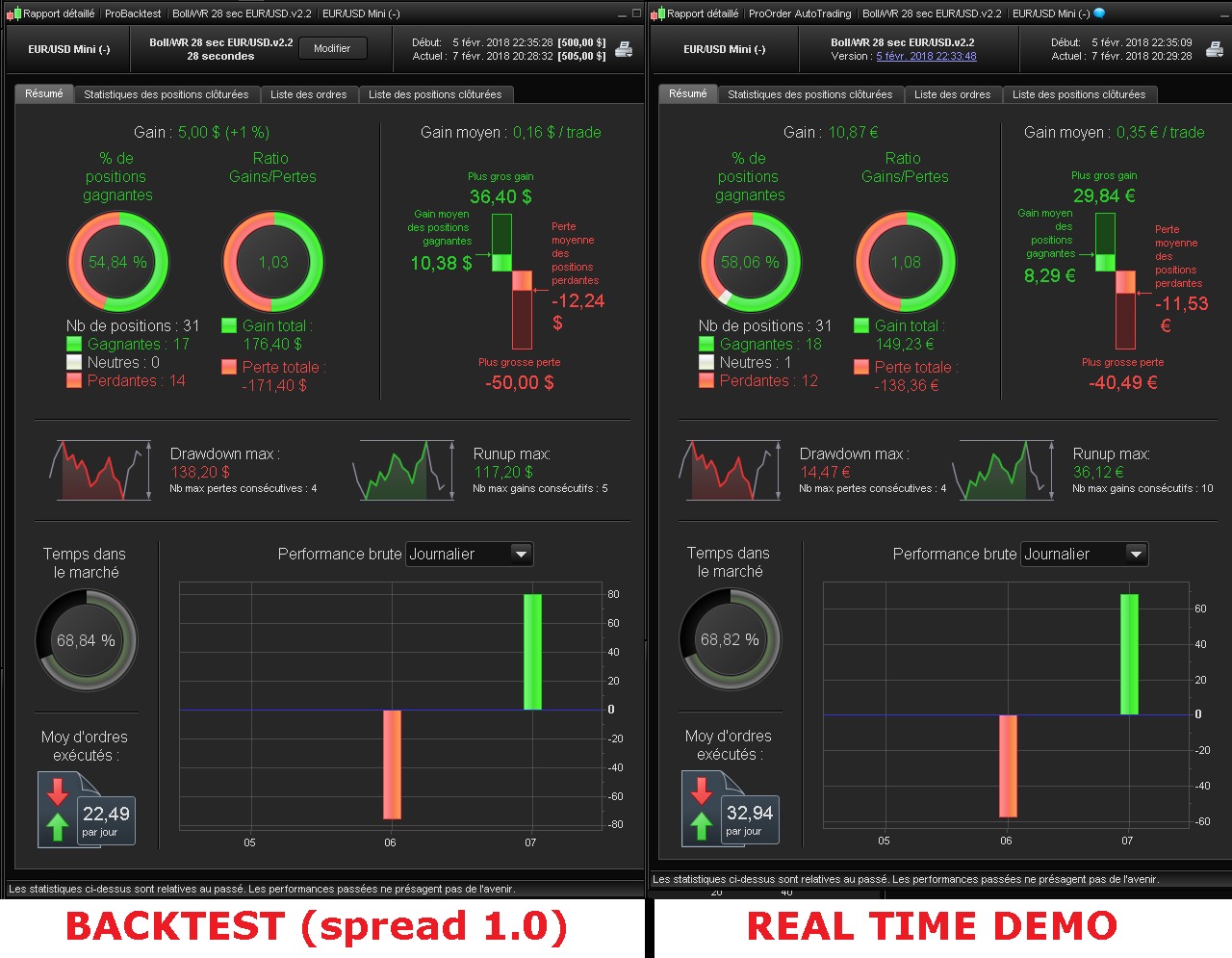

After two days of demo real time trade, I have compared real time performance with backtest, FOR EXACTLY THE SAME PERIOD (see the picture).

Good news : performance is quite the same (for the backtest I put a spread of 1.0, for the real time on a demo account, spread with IG goes from 0.6 to 1.5).

Maybe we just lived 1 bad day with loss (yesterday) and 1 better day with profit (today). So I keep it running and will tell you what’s going on.

Regards

Cyril

@ Cyril 21

This comparison is interesting. We would all like ProOrder live to generate the same results as our Backtests.

It’s good to have chosen the V2.2 is that of all versions of this Strat that I studied, which in Backtest produces the best gain with a fair equity curve.

What I criticize V2.2 is its large drawdown that can become unbearable for a small starting capital.

That’s why, I wondered about the interest of staying in position from 01h to 23h.

There are too many negative periods for my taste in a day of trading.

I studied 2 versions for one a 18s TF and the other a 28s TF, they have a big advantage is to generate gains by staying less in position on each day of trading.

The gain is reduced, but the starting capital lower than V2.2, given a drawdown much lower. Anyway, the loss of gain is catching up by playing on 2 variables to optimize (MaxOrders, limite).

I give you these two versions below. I look forward to your comments.

@ Gertrade

I agree with you ; the problem with V 2.2 is that sometimes the losses are so big that they cancel much of the gains, with a dangerous drawdown.

Thanks a lot for your 2 versions ; I run them and will let you know.