@ Cyril 21,

If your results are not good, it comes from using the MaxOrders variable. It’s my fault, I did not give any information on my method of getting started on ProOrder. Indeed, before launching the strategy, I launch an optimization of the variable MaxOrders from 1 to 100, and I choose the most profitable number. Like the 558 which is a copy V2.2.2 with 4 contracts. All other versions were more profitable by leaving the Maxorders vaticable at 1. Sorry, this wasted time due to lack of information. In any case, this warns us about the use in Money Management strategies. All strategies are not made for that. When the difference between the EURUSD and the EURUSD Mini, I’m afraid you’re right, there is a study to do, candlesticks must be different. It’s a pity that you have not started on ProOrder V5.6 which is the culmination of our work in this forum.

I thank you all for your investment in this work which is very useful to me.

Thx Gertrade and GraHal for your replies.

So I try to backtest and run the V.5.6, leaving the MaxOrders to 1, on EUR/USD (not Mini).

Sorry for all these questions, but there is something I can’t understand on this 5.6 version : the FlatBefore 1h and FlatAfter 10h in the morning are set to get lower spreads. But I thought that the spread is lower at daytime. So why is it better to have positions only from 1 to 10 AM ?

@Cyril 21 the EURUSD spread varies 24 hours a day as it flash widens for 1 second or so many many times per minute. On average, it may spend more time at 0.6 as you say? be good if we could get some figures / authority from somewhere?

I would say Gertrade has optimised for Hours 01 to 10 as with the settings he uses for variables these are the hours that give him highest profit? Gertrade correct me if I’m wrong?

The most liquidity / trades done on eurusd is from Hours 07 to 20 (GMT / UTC + 0) and this is generally accepted as best time to trade?

https://www.thebalance.com/best-time-to-day-trade-the-eur-usd-forex-pair-1031019

GraHal

@ Cyril21,

On the V5.6 I trade only from 01h to 10h (I stop the launch of trade at 08h) because I made a backtest on the V5.5 which is profitable with a spread of 0.6 (not realistic) , but whose equity curve falls with a spread of 2.0 (realistic). So I created a V5.6 that trades only from 01h to 8h (10h to close) to maintain an increasing equity curve. I think that we could create a new version by implementing an additional slot. Maybe 19h-22h, who knows? For the moment, I do not know how to implement this additional code to open a 2nd time slot without disturbing the rest of the code of the strategy.

Conclusion: the average profit on this strategy is surely greater from 01h to 08h for the equity curve is impacted up (it allows to offset a spread of 2).

Thank you for your thoughts!

To allow trades at 2 different time periods you can do …

If (Hour > 01 AND Hour < 08) OR (Hour > 17 AND Hour < 22) AND Condition(s) Then

Buy at Market

Endif

Thank you Grahal,

I will implement this in a future version.

PS: That no one is sorry to see a new version arise, I am in a progressive approach (without degrading past versions).

why did you leave 5 minutes strategies ?

@ Mau973,

I removed from ProOrder the strategies on TF 5mn because they were not profitable.

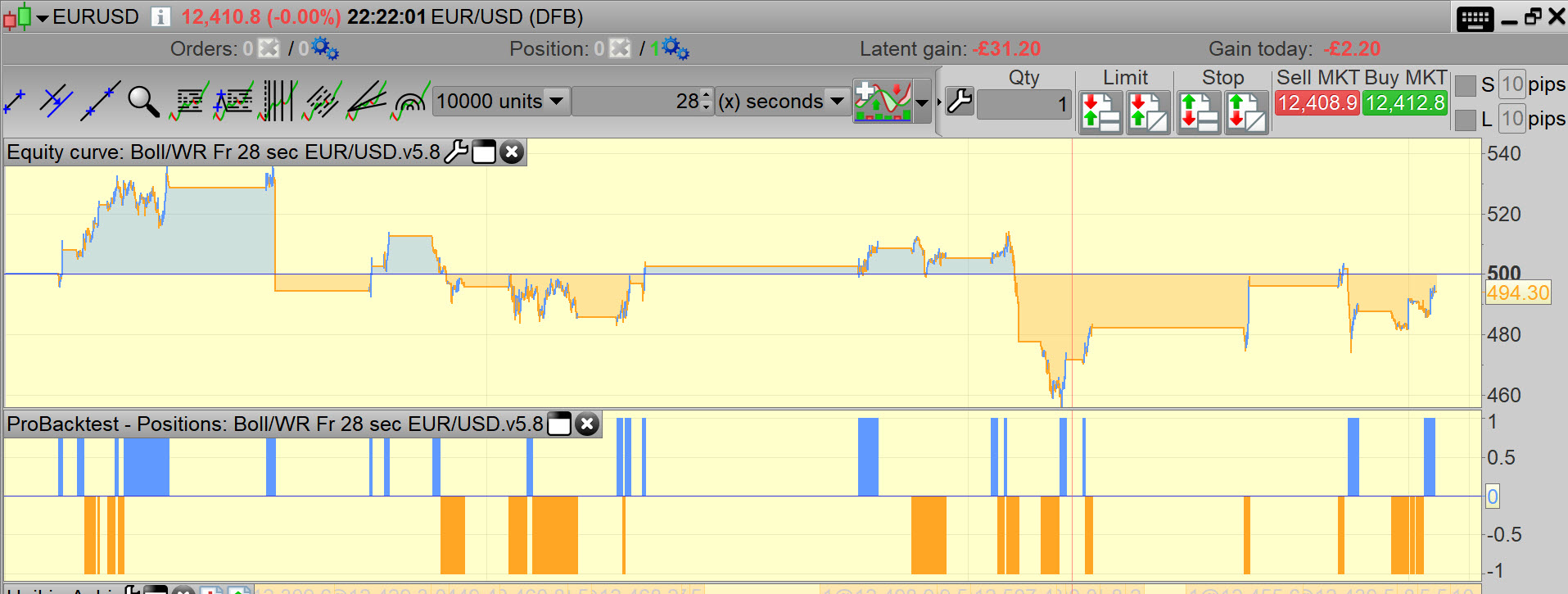

I just finished studying this latest multi-slot version.

This version is called V5.8

Good week !

@Gertrade thank you!

Do we have a difference between CFDs and Spreadbetting?

Attached is what I get for 100,000 bars. Am I missing something or any thoughts?

GraHal

@ Grahal,

I do not understand why this graph … I put myself in the same conditions: 10,000 units on TF28s with a spread of 2 on the EURUSD.

below my result.

@Gertrade … reason why I think 28 sec TF is flawed …

In bed I thought deeper about 28 sec TF (and any number of seconds that does not divide equally into 1 minute) …

If you start your Algo at 101500 then your first 28 sec period ends at 101528 (then 101528 + 28 secs etc)

If I start my Algo at 101600 then my first 28 sec period ends 101628.

At 101628 your nearest 28 sec time period will be ending at 101624 (101528 + 28 + 28 secs)

So why should we expect results to be the same when we are ending / calculating variables / trade entry, exits at different points in time??

Above anomaly does not occur if TFs of 1 sec, 5 sec, 15 sec, 30 sec are used.

I believe what you are doing is optimising / finding values of variables that fit (only) your 28 sec periods on your particular backtests?

Comments appreciated. I stand to be corrected? Or a different view / basis of using 28 sec TF?

GraHal

You are right, Grahal, with this timeframe, backtests that have not the same begining, have not the same candles and indicators calculation, until the end of the backtest. This makes an interesting “out of sample”, even for the same days, to test a strategy.

Thanh you GraHal , can you set 30-second timeframe? is the strategy profitable?…

Thanks guys … over many posts I have been trying to ‘persuade’ Gertrade to adopt 1, 5, 15 or 30 second TF. It has made for interesting discussion and will benefit others in the future,

I will admit to having tried ‘maverick TFs’ (similar to 28 secs etc) in my early days coding / optimising and I still seek that elusive short TF Strategy for quick in and out profit! 🙂

Maybe Gertrade will optimise his Strats for 30 sec TF and we can then see if there is any better consistency??

Cheers

GraHal

PS It’s been stimulating, I’ve ‘enjoyed the crack’ as we say in UK! 🙂 😉