Jusmih1 says … surely mid morning the spread should be consistant at 0.6

The EURUSD is 0.6 for the majority of time but regularly ‘flash widens’ to 1.5, 2.0 or even more … lasts less than 1 second then goes back to 0.6.

The flash widen happens at times of high volatility as in when it looks like price is going to break up or down / move up or down swiftly after being quiet etc.

If you add the Indicator ‘bid ask spread’ on same Chart as the price curve then you will see it flash widen loads of times during the trading period.

Cheers

GraHal

is 0.6 for the majority of time but regularly ‘flash widens’ to 1.5, 2.0 or even more … lasts less than 1 second then goes back to 0.6.

Which is why backtesting scalping strategies on PRT is a pretty pointless exercise in futility!

The ‘bid ask spread’ indicator is something that I have on every chart that I am looking at. It gives you a perspective of actual chart action in relation to spread. Amazing how many times you can look at a short time frame chart and think how easy it looks to pick entry and exit points and then find that the actual range is barely breaking out of the bid ask spread. It also gives you a good line to look back to the left of the chart and see if anything has happened at those prices in the past.

Jusmih1 the Live losing trade exit at 11:56 was the same trade I mentioned in post #62109 that I exited manually at about 10:10 … more or less same time as the your profitable backtest trade.

The Take profit needs to be lowered to 12, or 11 even to be safer for a profitable exit. Individual markets move in different ways and in the case of EURUSD a run of 12 can be common then a retrace. Factoring in a flash widen of the spread and it may never make a 13 TP.

For me, I’d rather be in and out in a few bars rather than wait a few dozen bars stressing while price meanders up and down and maybe never quite get to that optimised most profitable value.

This an example of where it is probably better never to take / use the top profitable result from the Optimiser … unless you have been pessimistic with the spread value used in the Optimiser … as in wider / bigger than it ever might be??

In the case of EURUSD that wider than ever spread value would need to be 2.5 or even 3 in my opinion. But then we would see disappointing results for profit in the Optimiser as mostly the spread would be 0.6. So a better way is to not choose the top profitable result from the Optimiser and / or amend the value in the code after observing real Live trading.

Jusmih1 I know you may have already done all of above, I am bothering to spell it out for the benefit of any newbie coders who may read this.

Cheers

GraHal

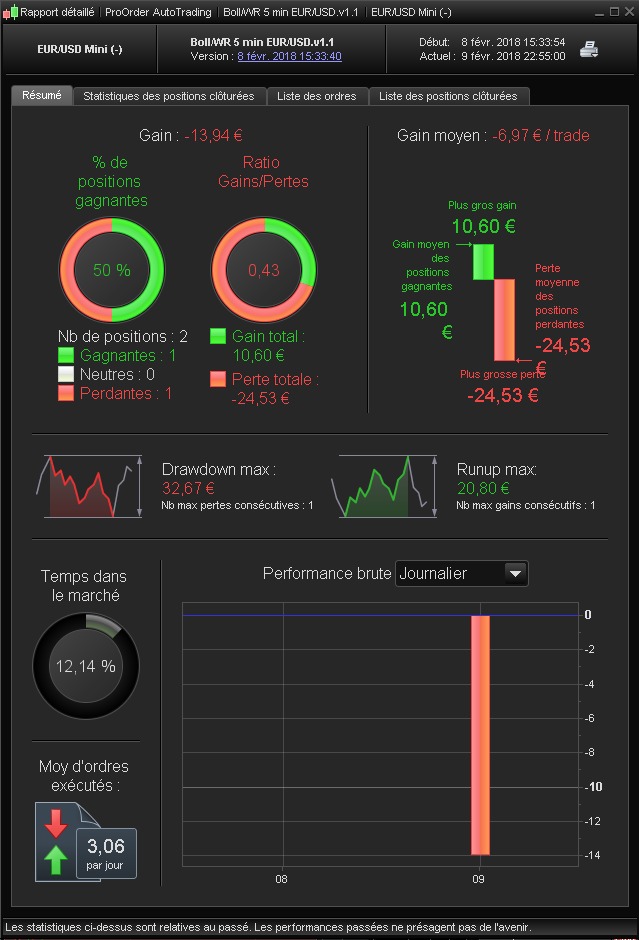

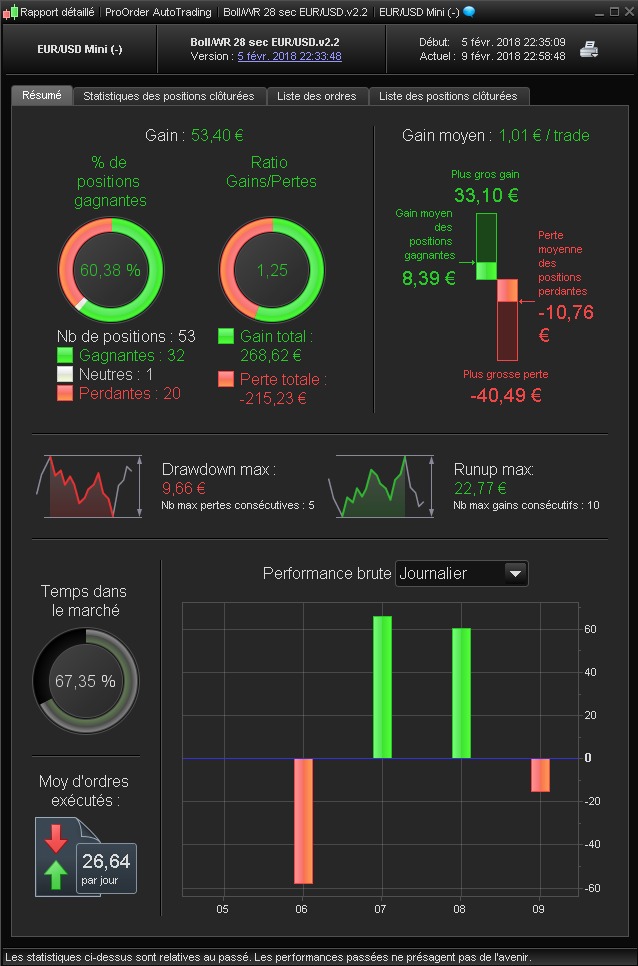

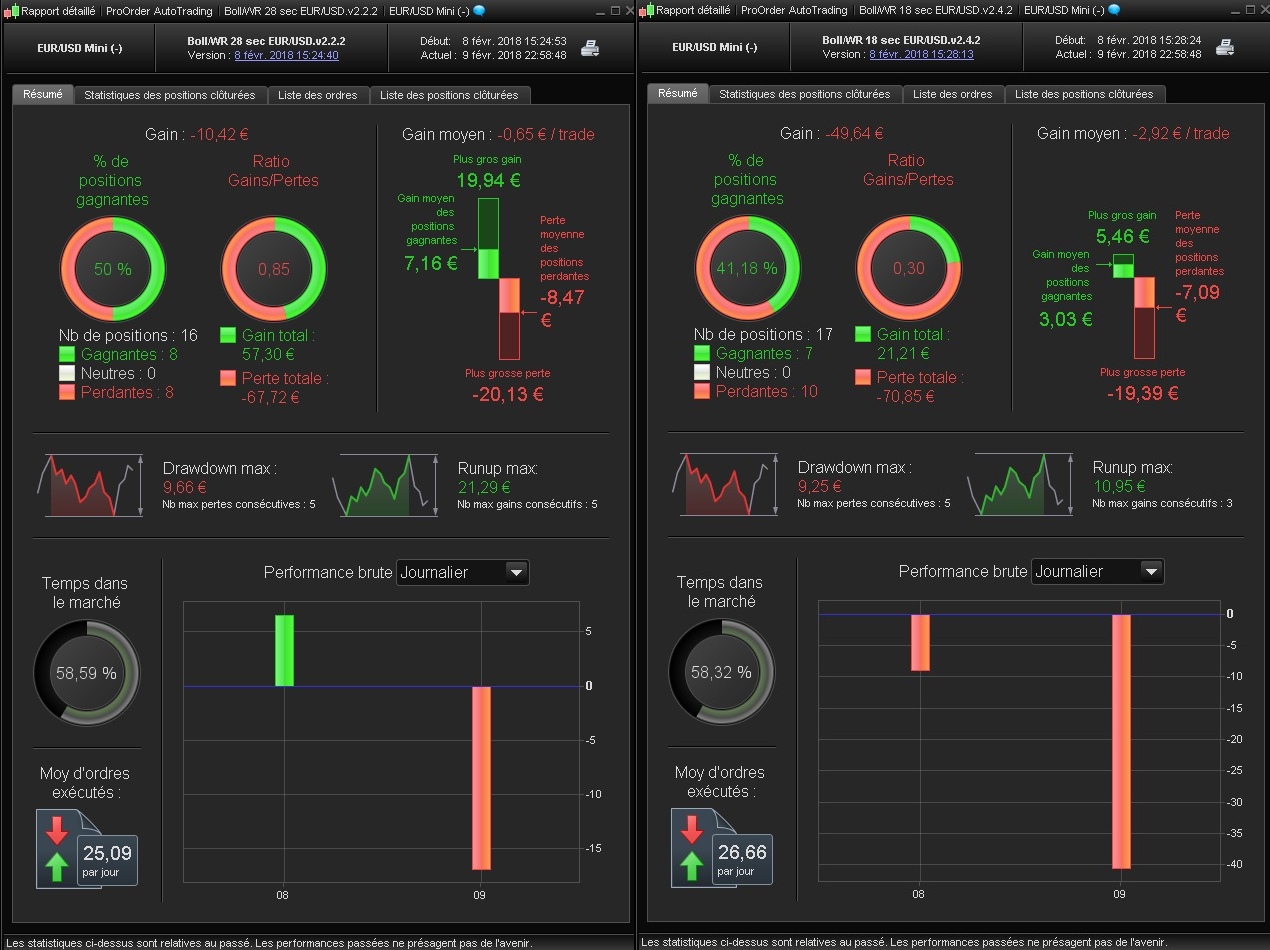

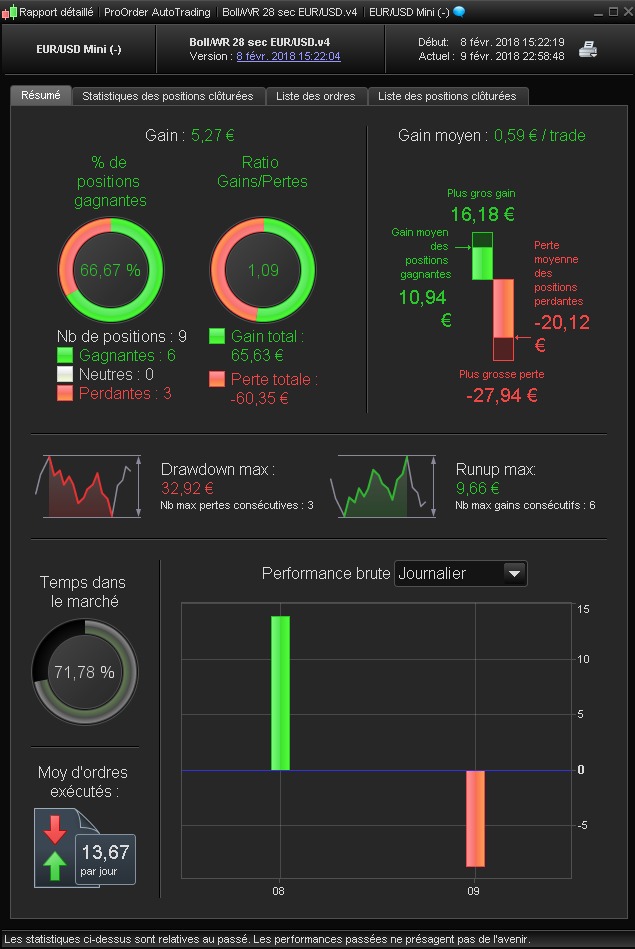

Hi everybody,

Here are some live performances for the v1.1, v2.2, v2.2.2, v2.4.2 and v4, from thursday 8th until close on friday 9th (except for the 2.2 that I run from monday 5th).

I did not make any modification on these 5 strategies, to get fair results.

The 2.2 has little gain (but I run it from a longer time than the others). For the other versions, that I run from thursday only, the only one that has gain is the v4.

Friday 9th has been “bloody” for all the versions I run.

I did not test the original V1 version. I see that @Jusmih1 has good results with this version, that he runs from monday 5th too, and he does not have loss on friday 9th.

I noticed that with a spread of 1.0 for the backtests, I don’t have big differences with live performances, even if the positions are not still similar.

Let me know if you need more details about positions for a particular strategy.

Hi Cyril 21,

Thank you for publishing your results.

I communicate mine on the ProOrder interface from 05/02 to 09/02.

I also ship the V4.5 TF28s on the EURUSD and AUDUSD.

The above results on ProOrder are on the EUR / USD while the results of Cyril 21 are on the EUR / USD Mini.

There is a ratio of 10 between the 2.

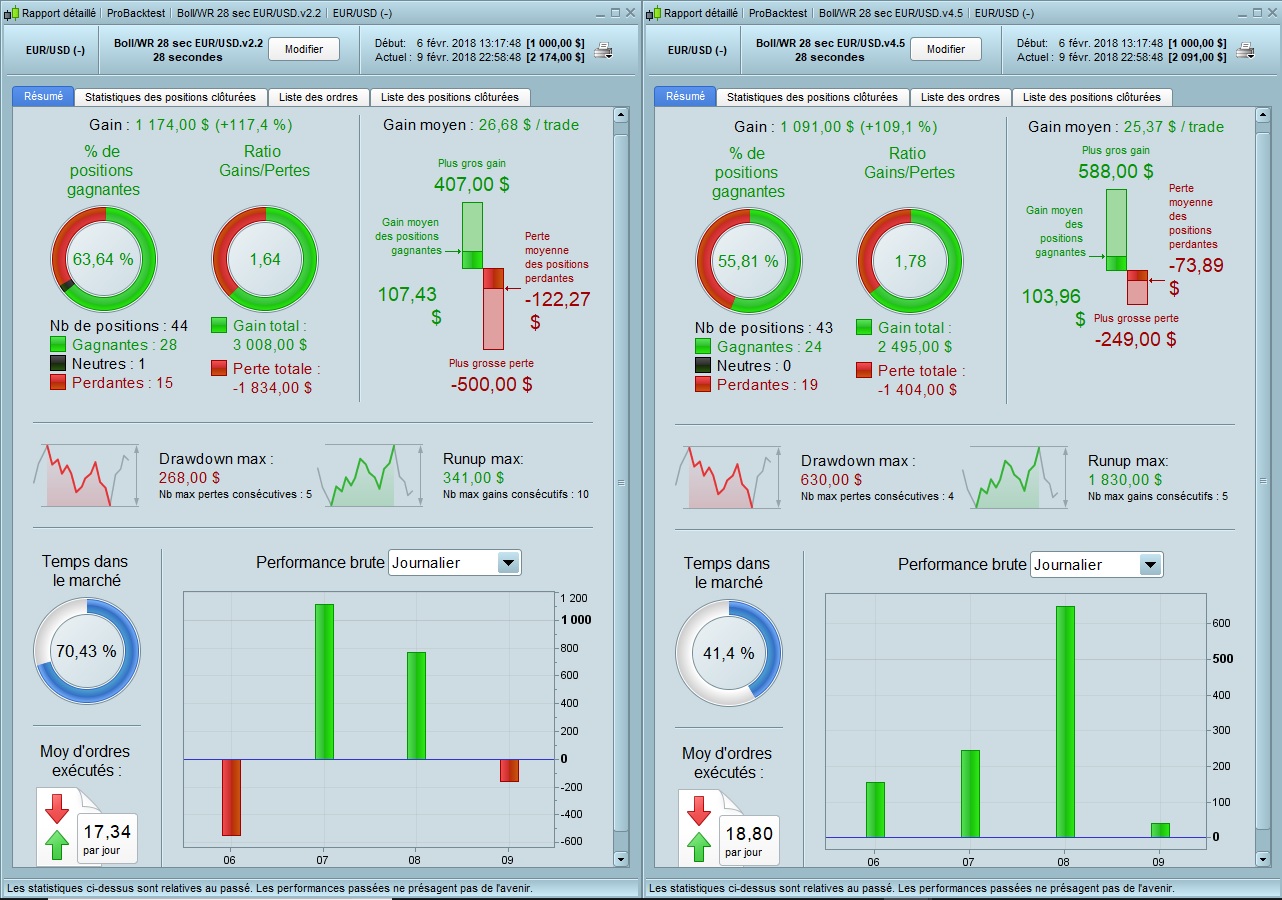

Following the publication of the results of Cyril 21 and the performance of V2.2 I have just compared in Backtest V2.2 to V4.5 from 06/02 to 09/02.

The gains are almost identical, the number of trades too, but what concerns me is the drawdown of V2.2 which is much lower and it is very interesting.

I look forward to next week’s results on these 2 versions that are now in competition.

Surprising ???

I just made the comparison again a few minutes apart between V2.2 and V4.5.

All results are the same except for the drawdown which is now V4.5 friendly.

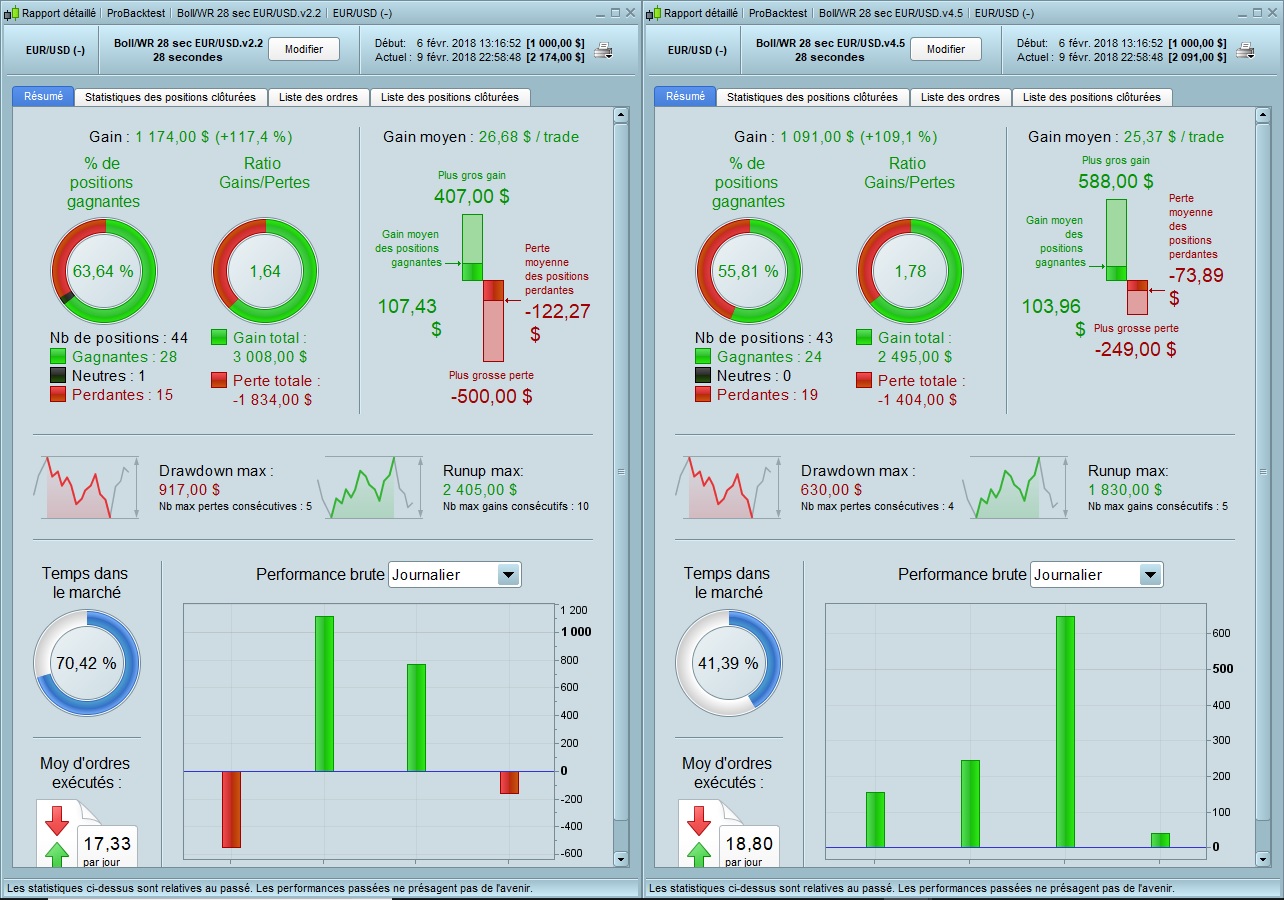

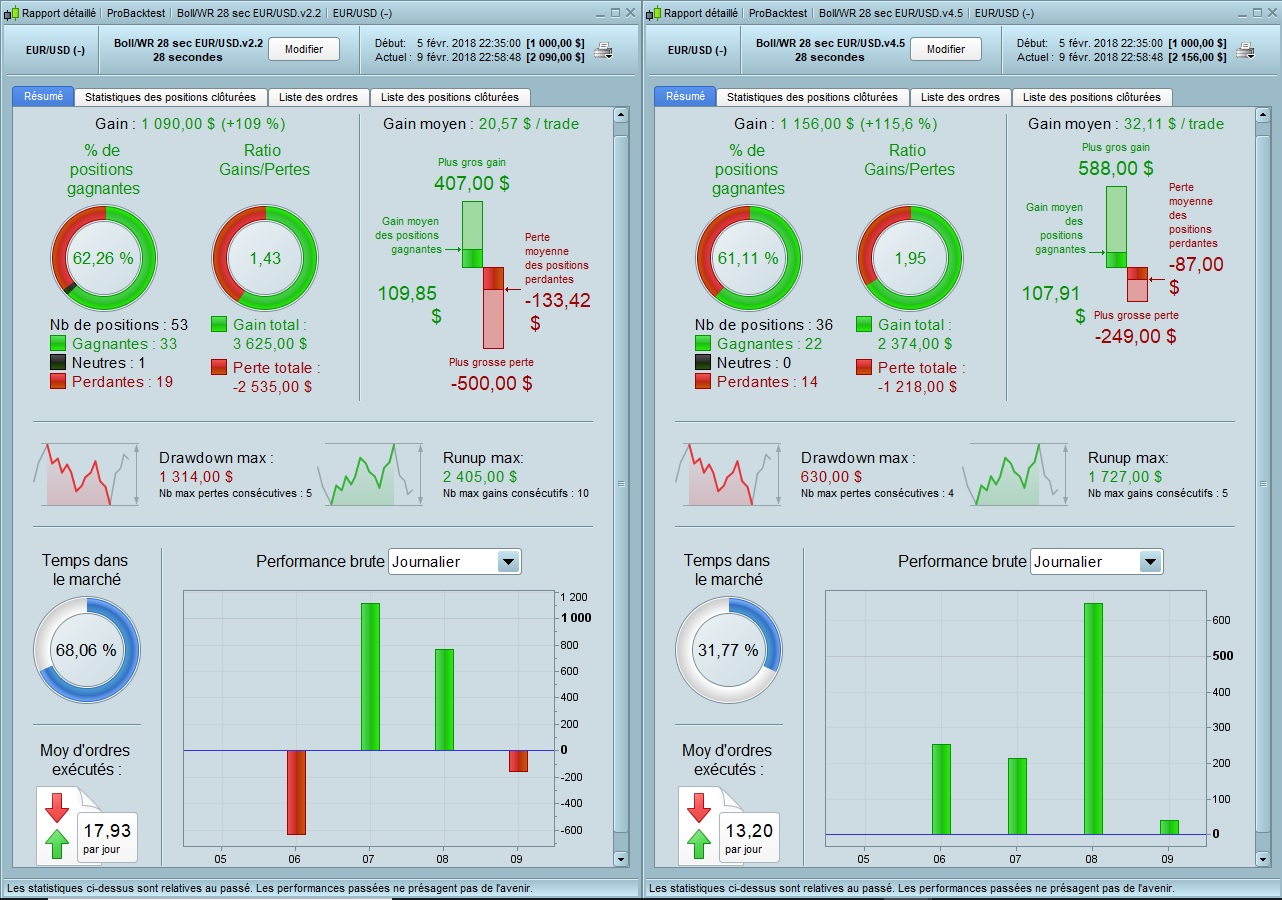

To be precise in the comparison with the results of Cyril 21, I just took the date of 05/02 at 22:35 as beginning of the comparison between V2.2 and V4.5. The gains are almost identical for a number of lower trades on the V4.5 and a drawdown favorable to the V4.5.

If we compare the results of Cyril 21 with my backtest over the same period, there is a noticeable difference in the results. Why that ??? Is there a difference between the EUR / USD and the EUR / USD Mini ??? the ratio goes from 10 to about 20.

Hi Guys

Loving this, Learning so much from you all, thank you.

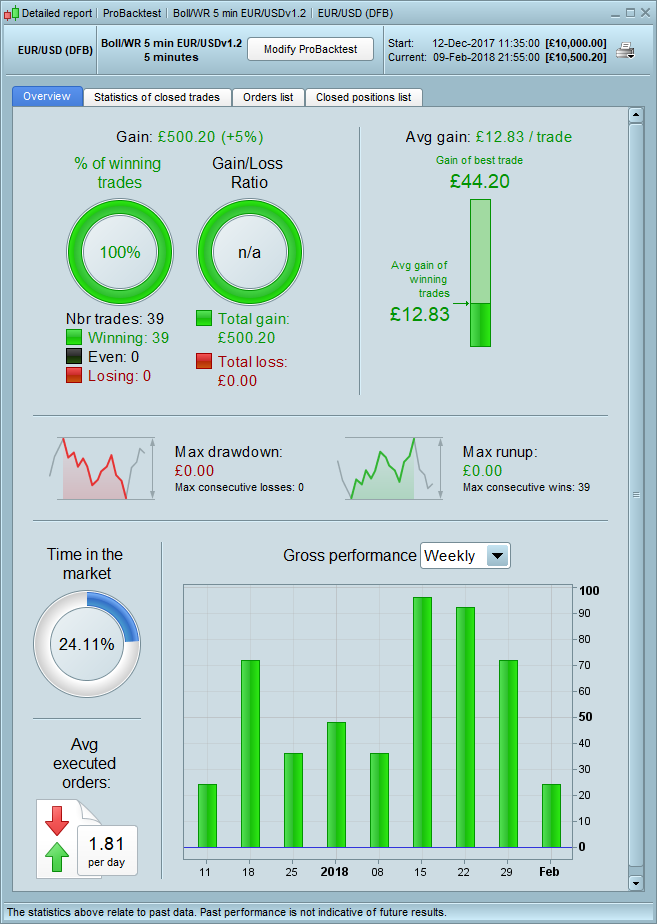

I have been working on v1.2 and made a few adjustments, there are far fewer trades but the trades seem to be better?

It only has a take profit though and no stops, is this too risky? yes i guess, but figures look good?

Can anyone help me put in SL/TS that will keep it as profitable or it just not possible?

Cheers

@Gertrade

I confirm the large difference between backtests on EUR/USD and on EUR/USD Mini. The backtest on EUR/USD Mini gets really closer to my live performance (on EUR/USD Mini too), but I don’t get exactly the same because of the variable spread. For the backtest I don’t set the spread to 0.6 ; after a few tests, the best spread seems to be between 0.8 and 1.1 (depends on the strategy and on the period).

Thanks for your V4.5. It gives good backtests (same as yours) ; so we’ll see next week !

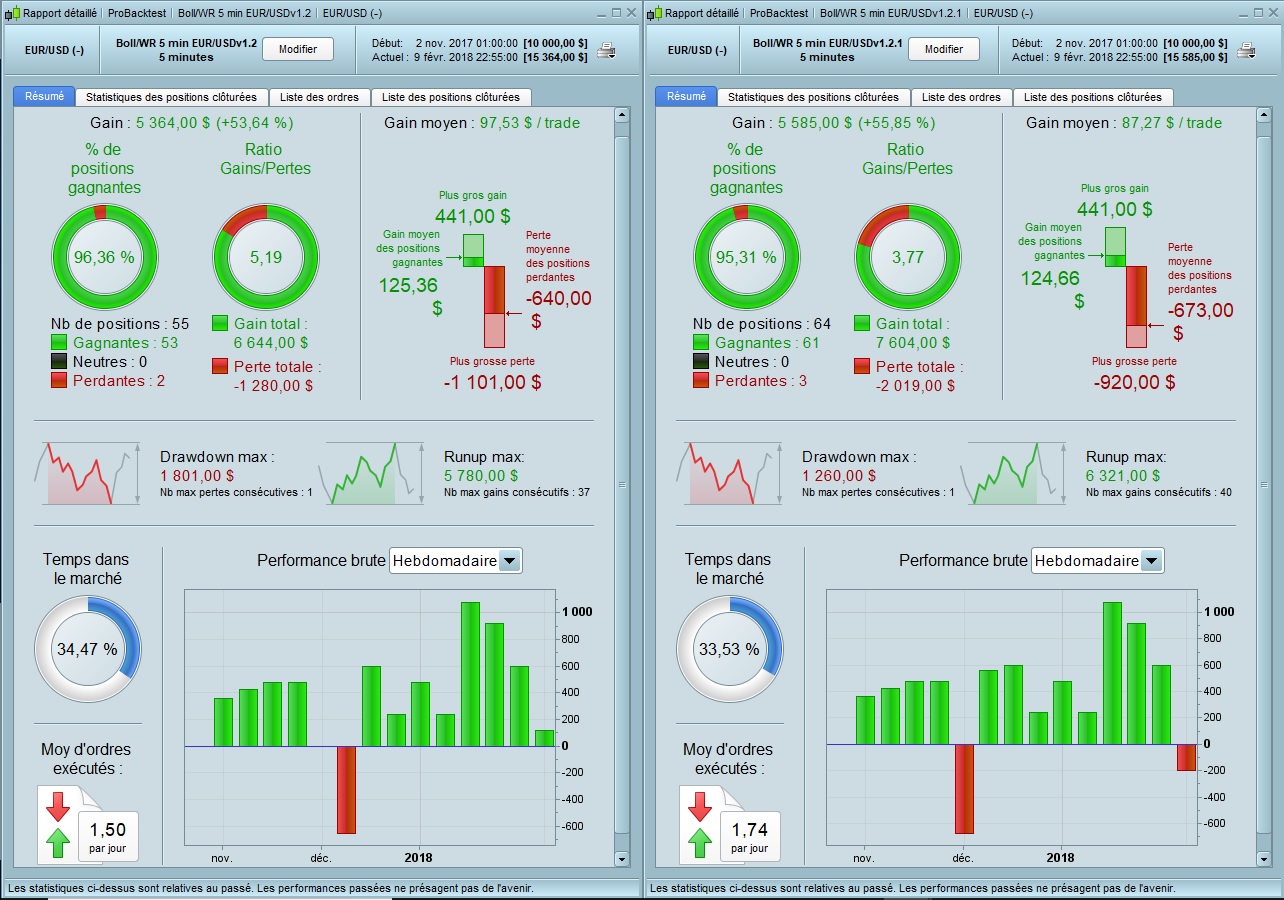

Hi jusmih1,

I have just included in your V1.2 version a Stop Loss without degrading the results or even improving them.

Congratulations to you for this V1.2 !!!

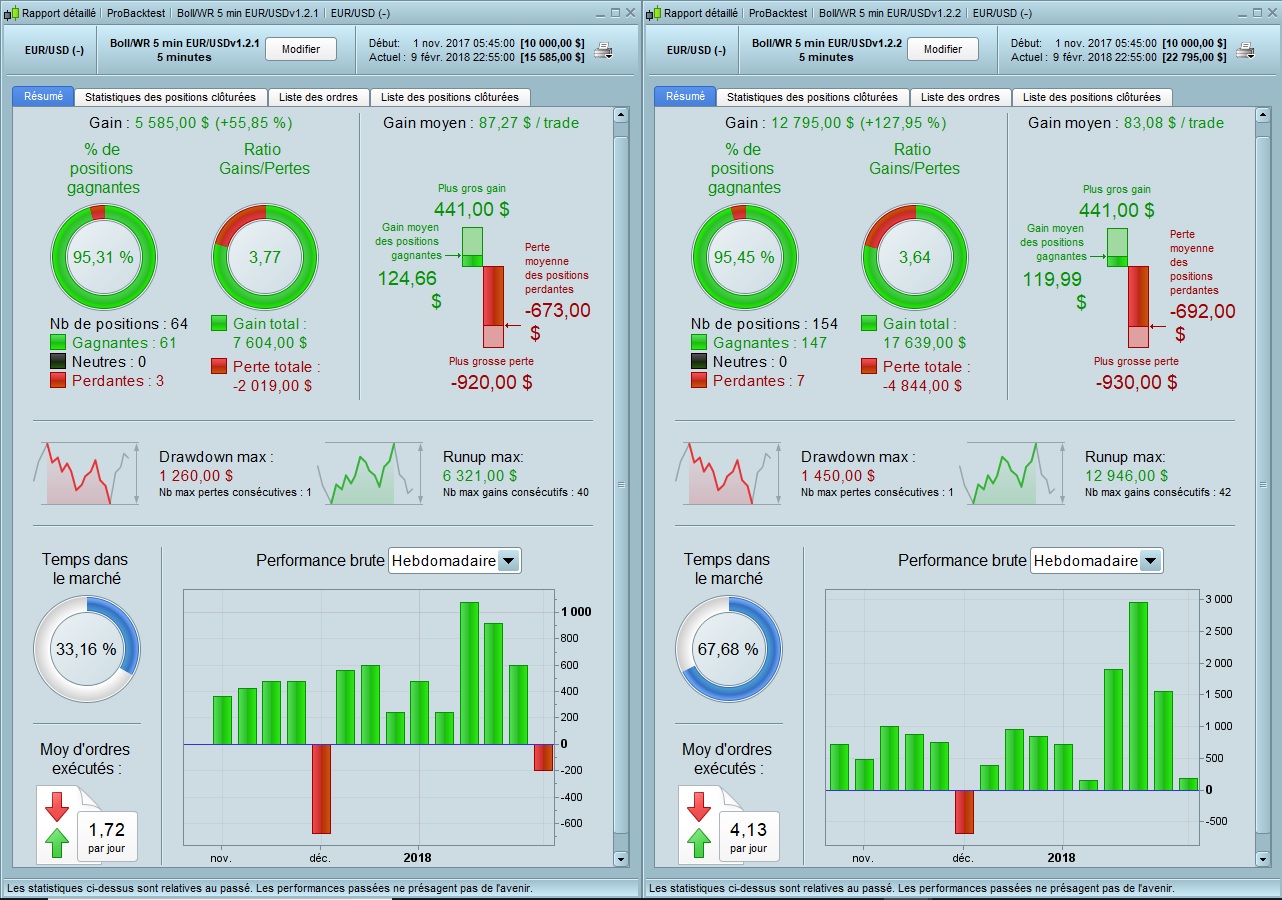

@ jusmih1,

I just optimized the V1.2, I very much improve the gain without degrading the results or even improve the curve of fairness which is smoother and oriented upwards throughout the length.

I kept the Stop Loss.

Good week and good work !!!

@ jusmih1,

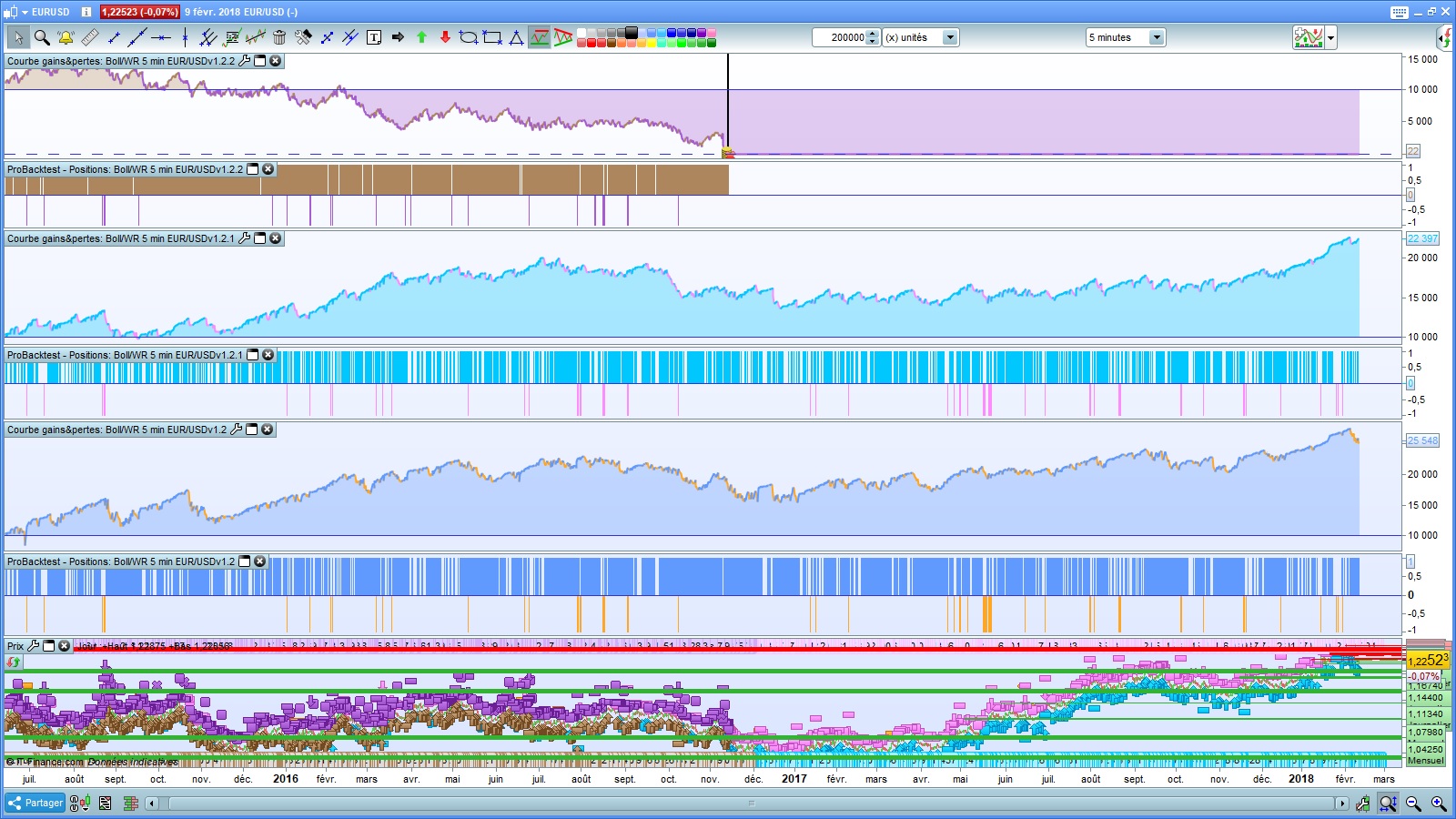

I have just compared the equity curves of versions V1.2, V1.2.1, V1.2.2 on 200,000 units.

V1.2 and V1.2.1 remain, while V1.2.2 collapses.

Conclusion: we must be wary of over-optimizing.