Repulse and DPO - 4H OnlyLong-Strategy on Dax

May 6, 2018, 5:42 PM

Strategies

20 Comments

{kind=link}

Hello

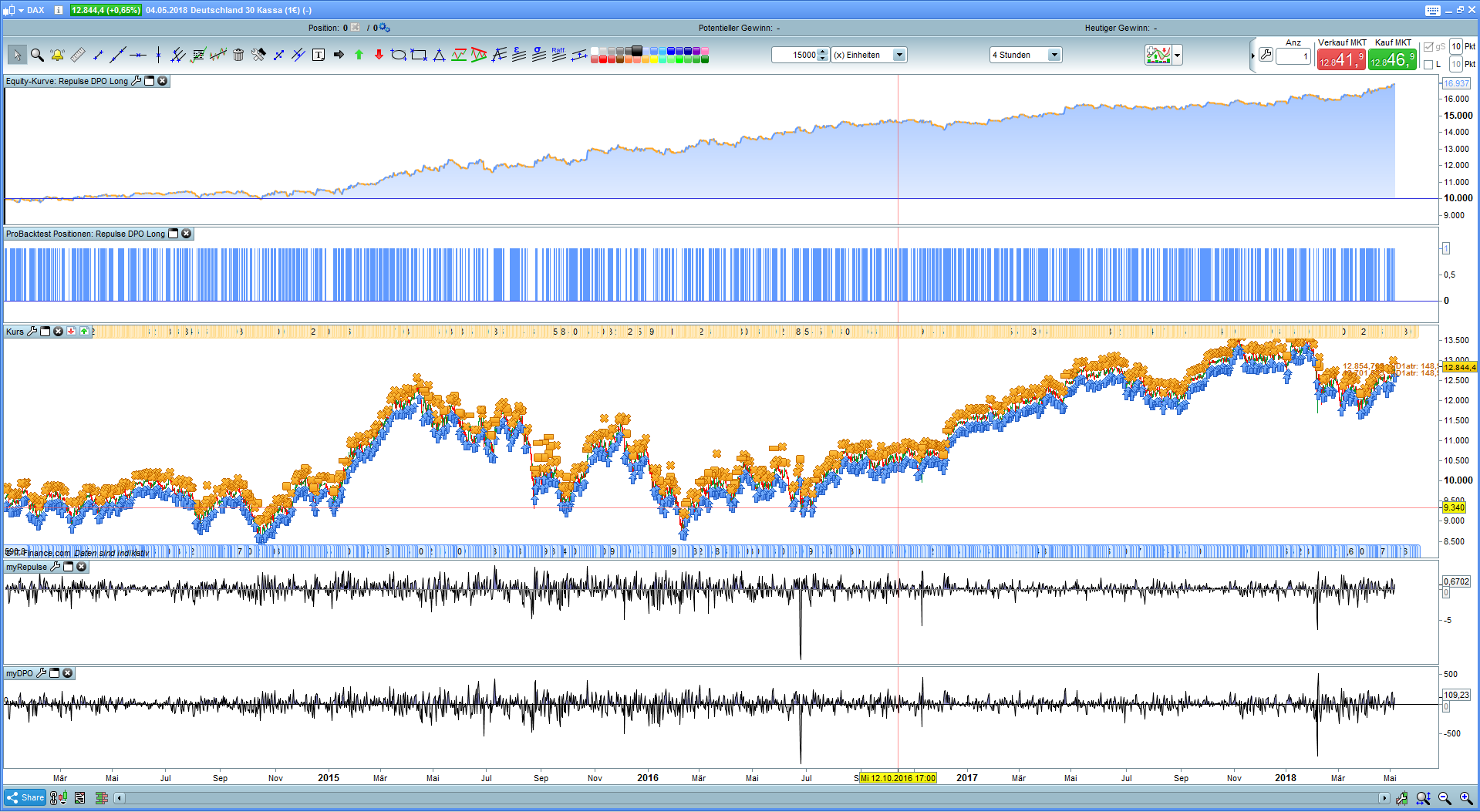

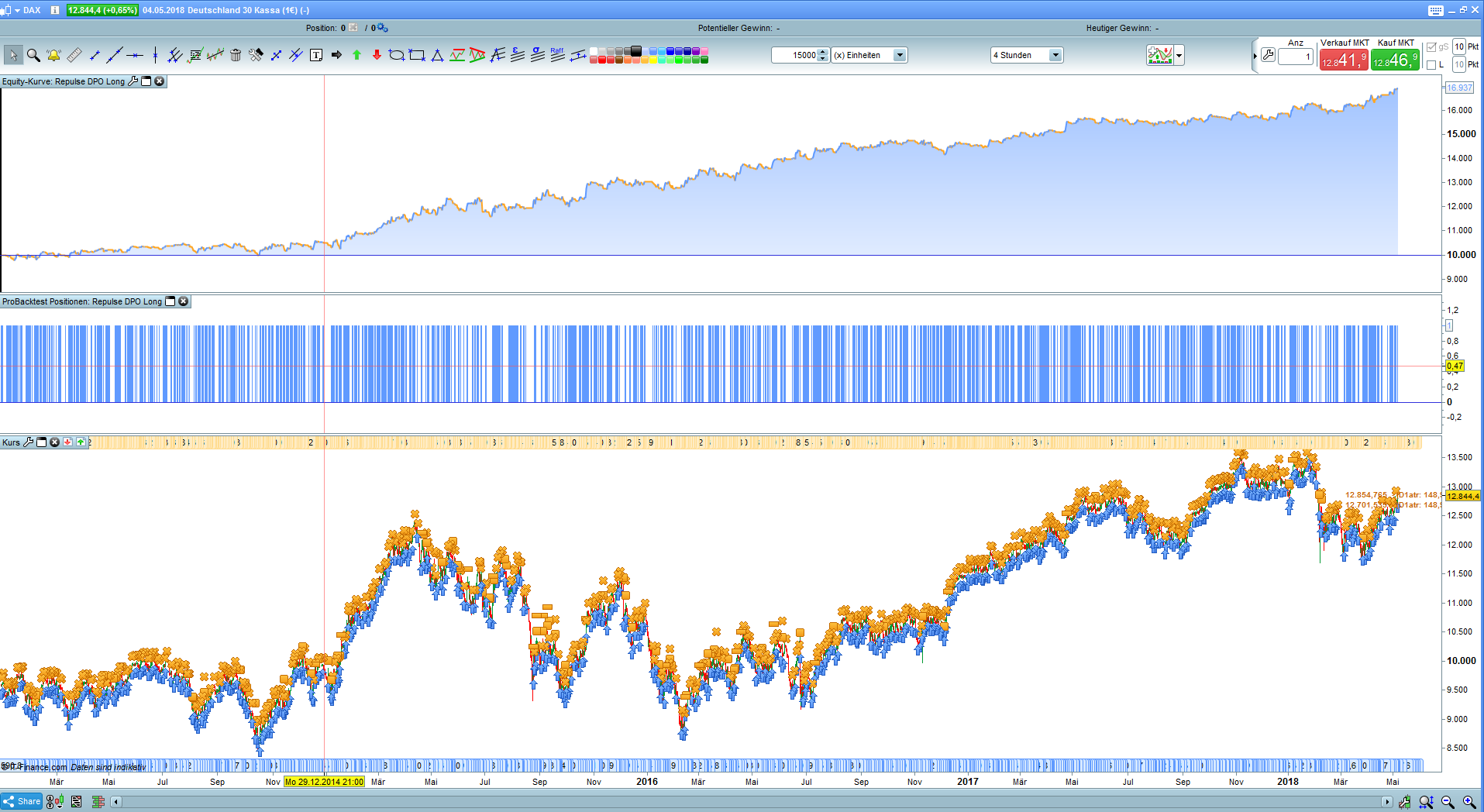

This is a small OnlyLongstrategy with quite acceptable results.

The Detrended Price Oscillator and the power of the candles with the Repulse Indicator are used.

If both > 0.1 we buy a position, if one of the two indicators Short < 0.1 we sold. Buying and selling is quite convenient at the usual times in the Dax at 09.00 / 13.00 / 17.00 and 21.00 hours (utc+2 “Berlin-time”). Who likes can protect the losses and profits in percent and not only via the indicators.

Like all trend-following systems, it has weaknesses in sudden trend changes and range phases, but this strategy still achieves a better result than the Dax itself.

kind regards

JohnScher

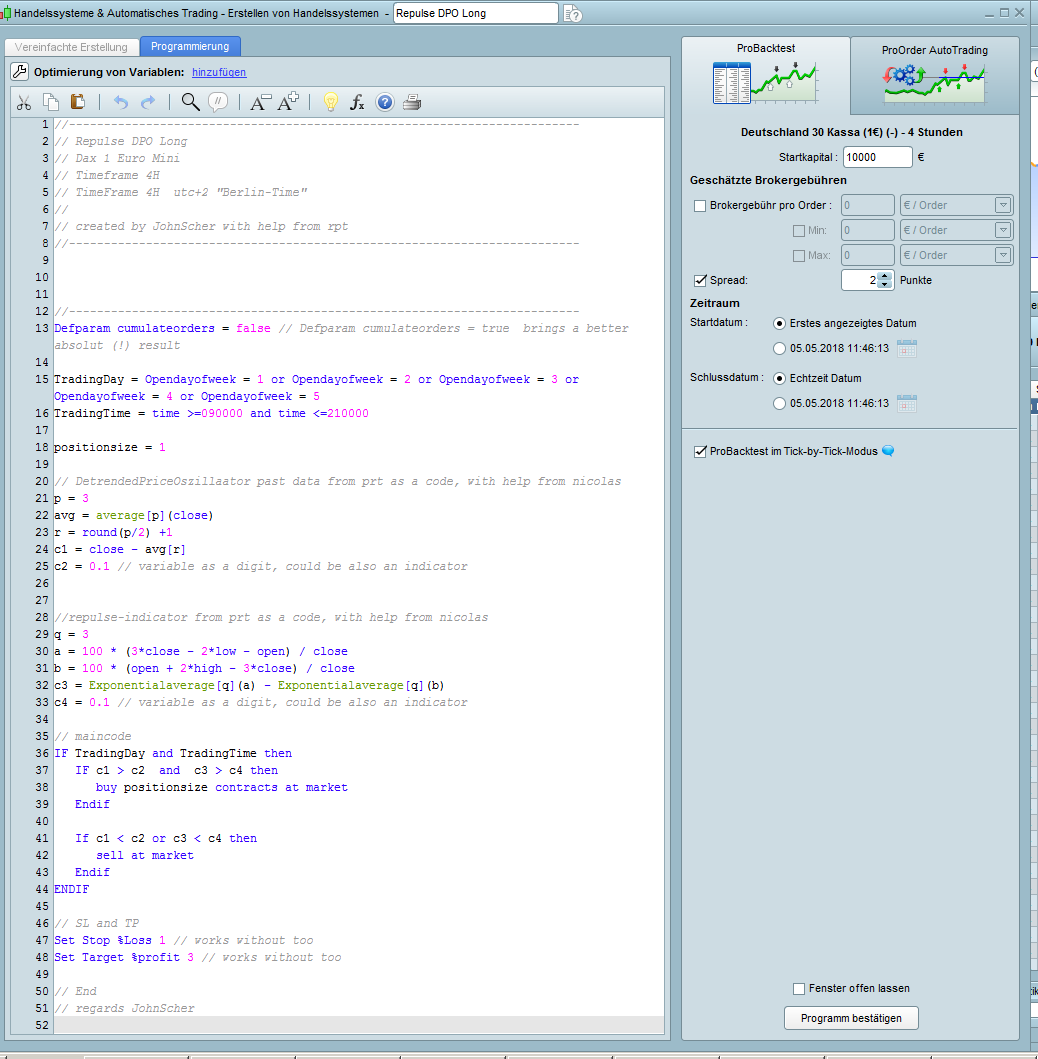

//-------------------------------------------------------------------------

// Repulse DPO Long

// Dax 1 Euro Mini

// Timeframe 4H

// TimeFrame 4H utc+2 "Berlin-Time"

//

// created by JohnScher with help from rpt

//-------------------------------------------------------------------------

//-------------------------------------------------------------------------

Defparam cumulateorders = false // Defparam cumulateorders = true brings a better absolut (!) result

TradingDay = Opendayofweek = 1 or Opendayofweek = 2 or Opendayofweek = 3 or Opendayofweek = 4 or Opendayofweek = 5

TradingTime = time >=090000 and time <=210000

positionsize = 1

// DetrendedPriceOszillaator past data from prt as a code, with help from nicolas

p = 3

avg = average[p](close)

r = round(p/2) +1

c1 = close - avg[r]

c2 = 0.1 // variable as a digit, could be also an indicator

//repulse-indicator from prt as a code, with help from nicolas

q = 3

a = 100 * (3*close - 2*low - open) / close

b = 100 * (open + 2*high - 3*close) / close

c3 = Exponentialaverage[q](a) - Exponentialaverage[q](b)

c4 = 0.1 // variable as a digit, could be also an indicator

// maincode

IF TradingDay and TradingTime then

If c1 > c2 and c3 > c4 then

buy positionsize contracts at market

Endif

If c1 < c2 or c3 < c4 then

sell at market

Endif

ENDIF

// SL and TP

Set Stop %Loss 1 // works without too

Set Target %profit 3 // works without too

// End

// regards JohnScher

Download

Filename:

RepulseDPO-DAX-Long-Only.itf

Downloads:

535

Download

{kind=link}

Filename:

Screenshot_5.png

Downloads:

153

Download

{kind=link}

Filename:

Screenshot_4.png

Downloads:

400

Download

{kind=link}

Filename:

Screenshot_3.png

Downloads:

158

Veteran

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...