EURUSD Mini overnight trading strategy 3 minutes TF

December 21, 2016, 7:01 PM

Strategies

13 Comments

{kind=link}

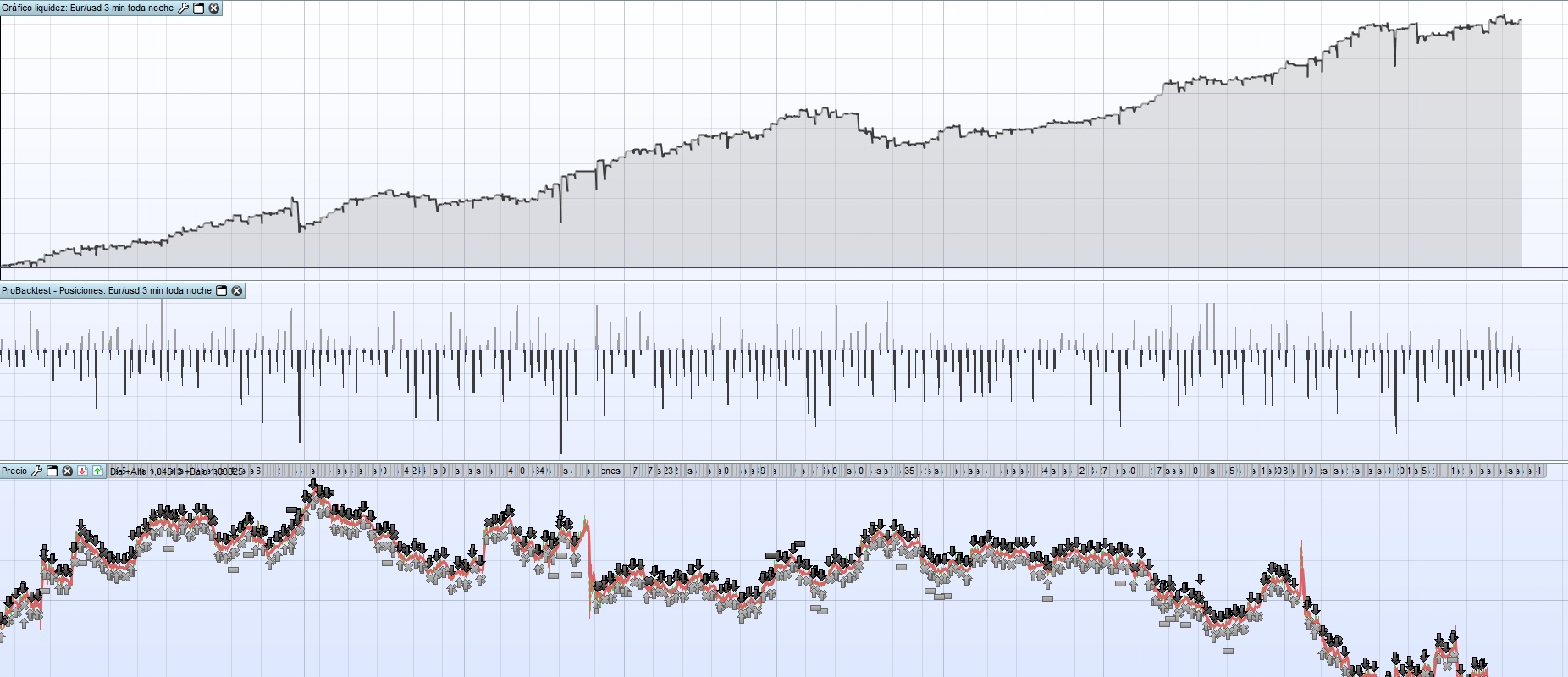

Good afternoon,

This strategy is designed for the Eur / Usd mini 1 € with a 3-minute timeframe and a spread of 0.6 pips. It only works in the evenings. Let’s see what you think and if anyone is encouraged to improve it. 😉 I have already put it with real money for a month and the backtest corresponds to what the robot does in real.

Buenas tardes,

Esta estrategia esta diseñada para el Eur/Usd mini 1€ con un timeframe de 3 minutos y un spread de 0,6 pips. Exclusivamente funciona por las noches. A ver que os parece y si alguno se anima a mejorarlo. 😉 Ya lo tengo puesto con dinero real desde hace un mes y el backtest se corresponde a lo que hace el robot en real.

DEFPARAM CumulateOrders = true // Acumulación de posiciones desactivada

DEFPARAM FlatAfter = 080300

// No se abren nuevas posiciones después de la vela que se cierra a las 5:15 p.m.

HoraEntradaLimite = 070000

// El análisis de mercado empieza en la vela de 15 minutos que cierra a las 9:30 a.m.

HoraInicio = 010000

IF ((Month = 6 AND (Day = 23 or day=24))or (month=11 and day=9)) THEN

DiaTrading = 0

ELSE

DiaTrading = 1

ENDIf

capital= 3000 + strategyprofit

posicion= capital/3000

if posicion>1then

posicion=1

endif

if posicion<1then

posicion=1

endif

if Time >= HoraInicio and time < HoraEntradaLimite and diatrading=1 then

// Condiciones para entrada de posiciones largas

indicator1 = ExponentialAverage[35](close)-2*std[5](close)

c1 = (close < indicator1[1])

indicator2 = RSI[11](close)

c2 = (indicator2 < 30)

IF c1 AND c2 THEN

buy posicion CONTRACT AT MARKET

ENDIF

// Condiciones de entrada de posiciones cortas

indicator3 = ExponentialAverage[35](close)+2*std[10](close)

c3 = (close > indicator3[1])

indicator4 = RSI[5](close)

c4 = (indicator4 > 70)

IF c3 AND c4 THEN

sellshort posicion CONTRACT AT MARKET

ENDIF

atr = AverageTrueRange[49](close)

stopus = atr*300000

TP = atr*80000

SET STOP pLOSS stopus

SET TARGET pPROFIT TP

endif

Download

Filename:

EURUSD-3min-overnight-trading.itf

Downloads:

559

Senior

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...