Larry-Connor converted to DAX M1

July 18, 2023, 12:12 PM

Strategies

19 Comments

{kind=link}

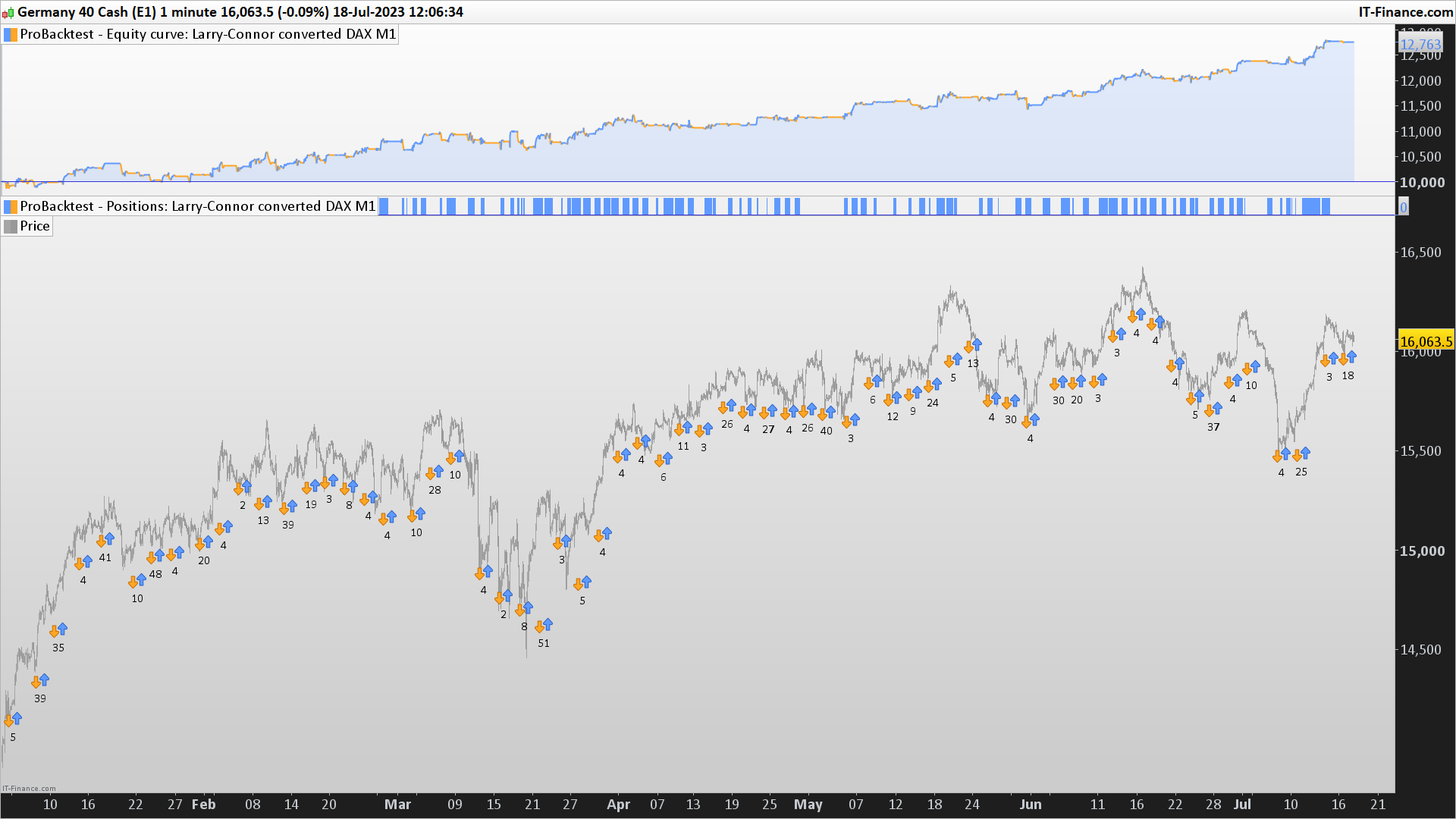

Runs on the 1 minute timeframe on DAX40. It’s traditionally run on the daily timeframe but I found out it works exceptionally on the 1 minute timeframe.

The rules of the 3-day high/low method/strategy converted to the 1 minute timeframe looks like this:

-

The latest bar close must be higher than the 200bars moving average.

-

The latest bar close must be lower than the 5-bars moving average.

-

Two bars ago both the high and low were lower than the bar before.

-

The high and low of the previous bar must be lower than the bar before that.

-

The high and low must be lower than the previous bar.

-

If conditions 1-5 are true, then buy.

-

Exit at the bar close when prive is above above the 5-bar moving average.

The code

////////////////////////////////////////////////////////////////////////

// _____ _____ _ _ //

// | __ \ | __ \ | | /\ | | //

// | |__) | __ ___ | |__) |___ __ _| | / \ | | __ _ ___ ___ //

// | ___/ '__/ _ \| _ // _ \/ _` | | / /\ \ | |/ _` |/ _ \/ __| //

// | | | | | (_) | | \ \ __/ (_| | |/ ____ \| | (_| | (_) \__ \ //

// |_| |_| \___/|_| \_\___|\__,_|_/_/ \_\_|\__, |\___/|___/ //

// __/ | //

// The highest rated developer on Trustpilot |___/ //

// ProRealAlgos.com //

////////////////////////////////////////////////////////////////////////

DefParam CumulateOrders=False

noEntryBeforeTime = 080000

noEntryAfterTime = 1715000

C1=Close>Average[200](Close)

C2=Close<Average[5](Close)

C3A=High[2]<High[3]

C3B=Low[2]<Low[3]

C4A=High[1]<High[2]

C4B=Low[1]<Low[2]

C5A=High<High[1]

C5B=Low<Low[1]

If C1 and C2 and C3A and C3B and C4A and C4B and C5A and C5B then

Buy 1 contract at Market

SET STOP %LOSS 1.4

EndIf

If Close>Average[5](Close) and (dlow(0) < dlow(1) xor dhigh(0) < dhigh(1)) then

Sell at Market

EndIf

if dlow(0) > dlow(1) and dhigh(0) < dhigh(1) then

sell at market

endif

Download

Filename:

Larry-Connor-converted-DAX-M1.itf

Downloads:

313

Download

{kind=link}

Filename:

Larry-Connor-converted-to-DAX-M1.png

Downloads:

127

Junior

Developing algos and indicators for ProRealTime

Go to ProRealAlgos.com

Author’s Profile

Loading...