I suppose the idea with V3 is to have the same code all year, but it’s bugged and uses previous candles, ThirdMA and so on… I tried to comment out the previous periods but it seems the code changes when I change ThirdMA for other periods than the current one…

I’ll just use Davids v3-mod version from now on, but I suppose it’s the same as V2. I don’t think original V3 should be used.

I have managed to combine 2-3 periods in v3 for several instruments with a bit of compromise. You can’t expect the exact same results because of previously mentioned bugs, but in some cases the results are pretty close. I will upload them once some of them has run live and matches the backtests.

Hi guys, all respect to you guys who keep this thread going with new markets to use for pathfinder 🙂

Im wondering, for you people who optimize it for short term markets and post the systems here: Do you run with these live in the markets you optimize them for?

I dont mind optimizing and walk forward testing different markets here, but are you actually running them? How long do they tend to last? do backtest results keep at it until the runtime is over? Is it over when the contracts expire (nov.. dec… etc) or is it only valid for 1-4 weeks`?

Any info would be nice, if you guys keep optimizing and running them live and make money, i would be happy to join you in the optimizing part så its less work and more fun for all! 🙂

Hello @jebus89 yes, I run almost all of them live. They last between 1 to 3 weeks. Though my Oct1 W has been running since Oct 4th, but that is because of accumulation.

Hi @dajvop, Thanks for the reply! Have they all been performing as backtest would have them to? How many trades pr optmized market (on avg) would you say that you get?

Its so cool to read that your actually run them live, have any of them proven to be a failure or has every optmized system given profits?

Im definitly going to start optimizing it with you guys in the future now. this is cool 🙂

I haven’t checked them all versus the backtest, there are too many, though those I have checked are correct.

That depends on the market situation. Since end of August we have been slightly out of sync compared to the seasonal behaviour.

My statistics:

August: 101 systems live on 35 instruments, 64 ran, 47 with profit

September: 73 systems live on 31 instruments, 38 ran, 15 with profit

October: 107 systems live on 39 instruments, 46 ran, 32 with profit (1 still open, but I think that will close with a loss)

How can you have more than 100 systems live? I thought the maximum for PRT premium is 100. Just curious, never been up in so many strats.

wp01

wp01Participant

Master

He probably took a second account as he mentioned a while ago….

It is actually all the systems for that month, so maybe 40 the first half and 60 the other half.

Hey Guys

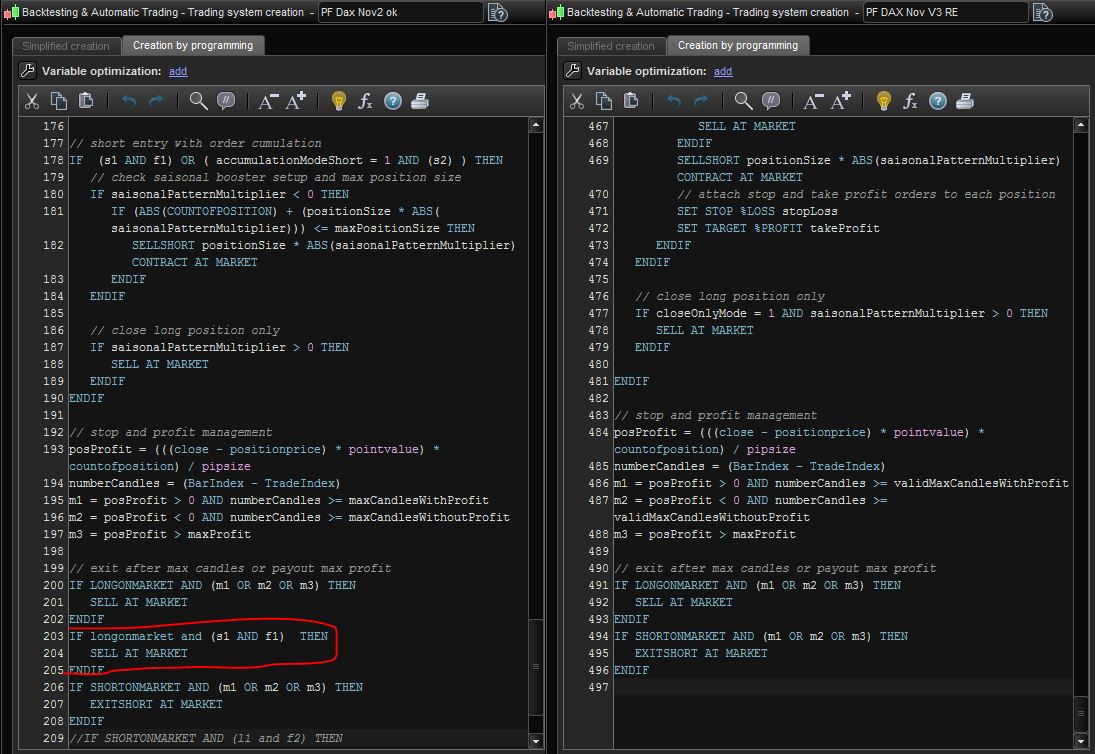

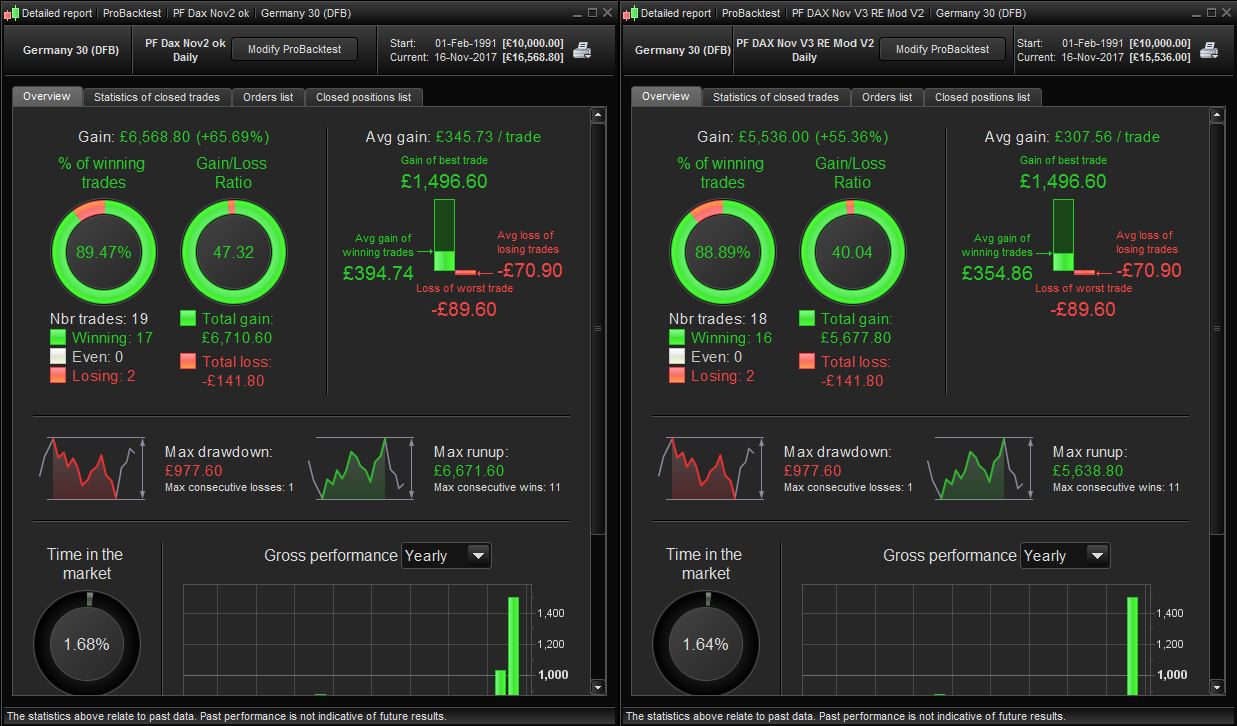

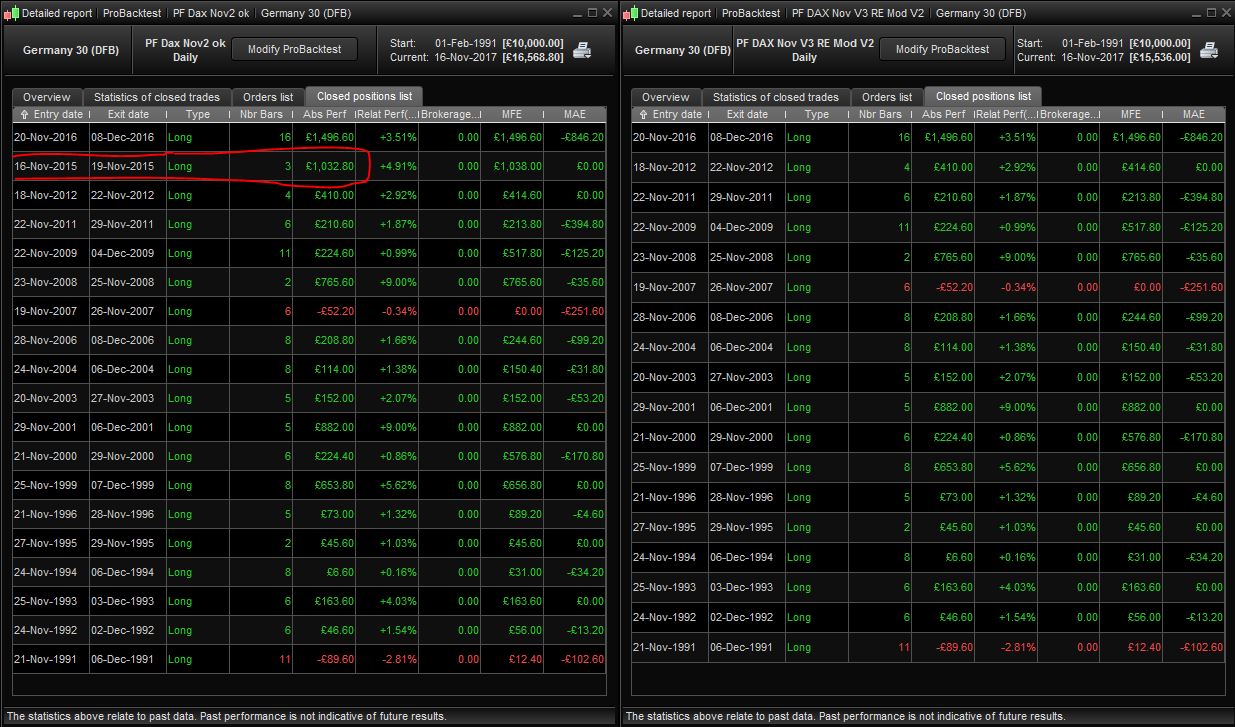

I could not leave it alone. It was bothering me why V3 and V2 are getting different results.

I think I found the main reason. As you can see in the screenshots, one condition to sell a long order is missing in the V3. These condition was included in V2.

I compared my Dax algo for Nov2.

If you compare then the trades from the original V2 and the new modified V3 (incl. this condition) its almost the same.

V2 just took one more trade which is unfortunately quite significant with a profit of 1000.

But all the other trades are the same.

Unfortunately I don’t know why Reiner omitted this condition.

I did the same with my Dow algo and there its the same result. All trades identical but V2 took 2 more trades in this case.

I dont know how you think about it but I would prefer rather the V3 including this condition as the results are very close to our V2.

This would mean we dont have to optimize all algos from Jan to October again. Would save us a lot of time.

Let me know what you think.

Here also the algos in case you want to check by yourself.

Reiners original V3 (latest update)

Reiners V3 including the V2 condition

Reiners V2

Well done! I will add the line to my v3’s and see if there is any difference.

Strange though that a missing sell command triggers a trade in 2015.