A new one: Oats with accumulation run on the Oats O 25 Dec-17 instrument.

Hi team,

I have one question related to the last DAX V3 that sent Rainer. I want to try to work on another one (CAC for example) in order to have a full year, but i don’t know how to make the optimization..there are many differents parameters now..or is my understanding wrong??

Have a nice week-end!

Hello!

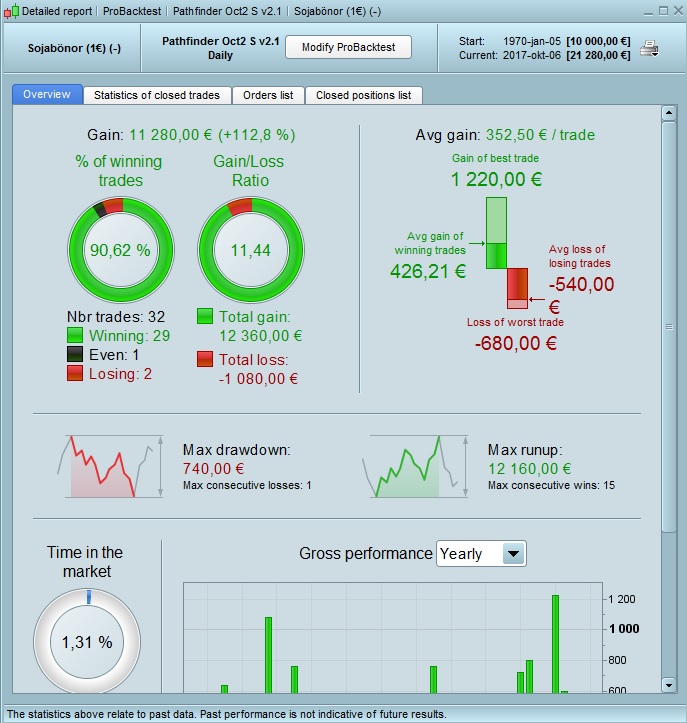

how many time needs pathfineder to start to work?

I’ve 7 daily Ts placed on different markets the 9th of september. They are all sleeping! It’s a normal situation?

Best regards. Cpt Nemo

@CapitanNemo: Which ones are you running? They can only take position for the time period they are optimized for. For example, currently only the algos defined for Oct1 can run, which works 1-15 october. If you want a system to be able to take position all the time you can try the normal Pathfinder systems.

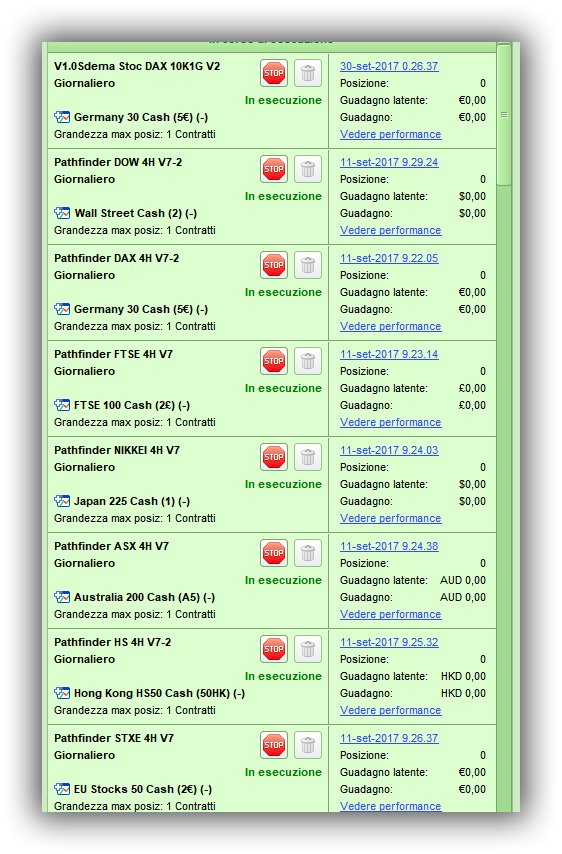

I’m using the 7.2 release. One for each market. See the .jpg. Wath have I to do for put the correct parameters in each Pathfinder TS? Where can I find instructions? Thanks. Cpt Nemo

I think you have to increase the number of maximum contracts. You have all set to 1. I think pathfinder orders more than 1 contract.

CapitanNemo: Like Despair says, it could be to many contracts and the orders get declined. You can see this in “order list” in PRT.

You can change the amount of contracts in the code if you want max 1 contract, scroll down to months and change them to 1.

wp01

wp01Participant

Master

@dajvop,

You applied the Platina on the $50 future. Not sure if you were intend to do that, but there is also a $10 future.

And, isn’t it a better idea to focus on the new V3 version? Just an idea no offence of course.

Kind regards,

wp01: Reiner wrote that V3 is good for yearly usage. Is it also better for swings? Haven’t tried it.

wp01Participant

Master

@ozz87,

It has a couple of new features such as a new signal line and also the posiblity to optimize per month.

If you continue with the V2 version you have to do it again later on when you use the V3 version.

V3 version? I don’t know it. Where is the code?

All TS 7.2 that I’m using, still sleeping, are in original settlement and in Paper Trade.

What have I to do? Must I set the month = 1? How and where??

The codes that dajvop (thanks dajvop!) sended to me are ok or they need some better setting?

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 – long / <0 – short / 0 no trade)

ONCE January1 = 0 //0 ok 1

ONCE January2 = 2 //2 chance

ONCE February1 = 1 //1 ok

ONCE February2 = 0 //0 ok

ONCE March1 = 2 //0 risk(2)

ONCE March2 = 3 //2 chance

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 0 //3 ok

ONCE May2 = 0 //0 ok

ONCE June1 = 3 //0 risk(3)

ONCE June2 = 1 //0 risk(2)

ONCE July1 = 3 //1 chance

ONCE July2 = 0 //1 ok

ONCE August1 = 0 // ok

ONCE August2 = 0 // ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 3 //0 risk(3)

ONCE October1 = 0 //0 ok

ONCE October2 = 3 //3 ok

ONCE November1 = 1 //0 chance

ONCE November2 = 3 //3 ok

ONCE December1 = 1 //3 ok

ONCE December2 = 2 //2 ok

// dynamic position sizing based on weekly performance

ONCE profitLastWeek = 0

IF DayOfWeek <> DayOfWeek[1] and DayOfWeek = 1 THEN

IF StrategyProfit > profitLastWeek + 1 THEN

positionSize = min(trendMultiplier, positionSize + 1) // increase risk

ELSE

positionSize = max(1, positionSize – 1) // decrease risk

ENDIF

profitLastWeek = strategyProfit

ENDIF

thanks boys!