Hi guys,

here is an update of the Pathfinder swing template. Based on the last long and short version the new template V3 is now better suitable for yearly usage. New features are:

- the usage of a signal line for each period is now possible

- introduce default parameter with the possibility to override these for each time period

- save maximum candle settings in the case of period change

- check monthly statistics (e.g. return and profitable trades) with the variable onlyTheseMonths (optimize the line with x = 1 – 12; onlyTheseMonths = CurrentMonth >= x AND CurrentMonth <= x)

- the variable tradeInPeriod determines wether to trade in a period or not

- close all positions if trade trigger runs against saisonality (variable closeOnlyMode – helpful if robot is only valid for one time period)

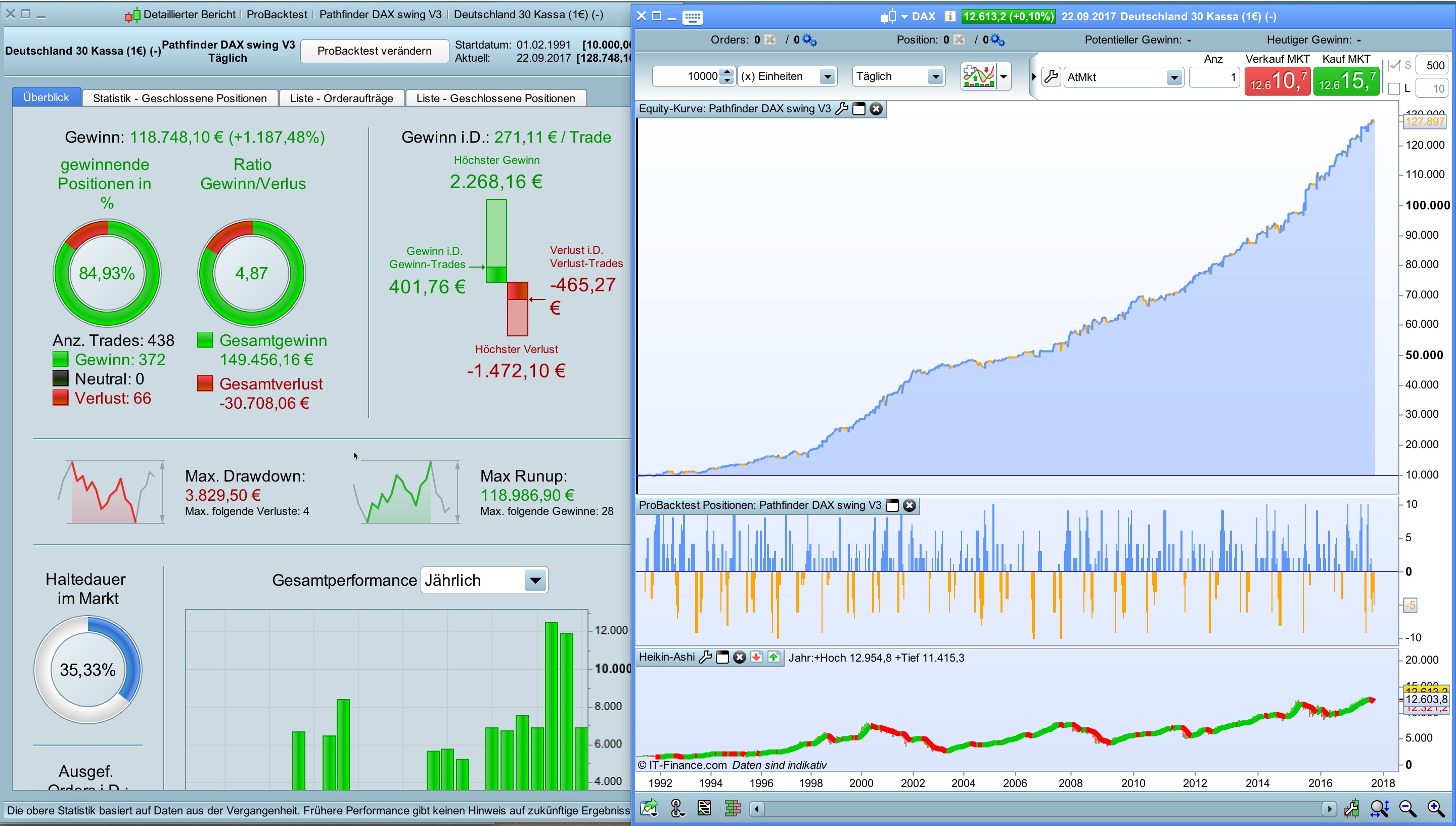

Please find attached a sample for the DAX.

Best, Reiner

Hi Patrick,

Hope you are well. Unfortunately I can not answer every question immediately and it’s not my intention to ignore someone here!

What should I say 🙂 ? I studied financial mathematics and have a talent for numbers and statistic but I never said that I’m an expert for trading systems. Unfortunately this site wasn’t available when I started with PRT so I have been published some reliable trading ideas to make life easier for the guys who just started here. Don’t expect to much from me and my algos – the main ideas of Pathfinder TS are very simple (breakout, trend follower, seasonality) and nothing I personally invented.

The swing algos based on daily data and the problem is the small data history this leads to unrealistic (curve fitted) backtests. Nobody expects results with a probability of 80-100%!

What is interesting that this it still works so well! According to my experience it works best from November to April. I played around with Walk Forward optimizing and seasonality and for me it delivers no better results.

Best, Reiner

wp01

wp01Participant

Master

Hi Reiner,

Thank you for your reply. I think that i’m not only talking for myself that we all appreciate what you have contributed to this forum.

I’ve never doubted your intensions but since we are all followers here i think that it is a good thing you pointed out how you are thinking about

the walkforward in combination with Pathfinder swing TS. I hope you understand it could be a bit frustrating when it seems that we are all running fantasy backtests here for months

which are useless. I also had my doubts from time to time about these backtests because you probably also noticed that everyone creates different results for the same period.

It is actually never in line with each other, so i’m wondering which one is the best? Which one can be used for the yearly codes?

From time to time it is nice to have some backup so that we know where we stand.

Thanks again.

Best regards,

Patrick

Hi Rainer,

You reply that there wasn’t the OOS feature when you created pathfinder. I’m not talking of WFA (what I agree is hard to do with such a seasonal strategy). A simple OOS test does not require any special feature from PRT. The whole story is just to optimize and test on two different datasets.

Testing on the optimized dataset like you do is IMO not saying much about how the algorithm might perform in the future. And I say it again, I don’t doubt that pathfinder is a good system. You seem to have ran it for some time live and this is of course the ultimate OOS-Test. The only thing I say and I stick to it, the curve fitted backtests in this thread don’t say anything about the quality of the algo and I think it is a pity that there are no tests shown that really show that pathfinder is as good as one is inclined to think after seeing this incredible backtests.

I personally would not dare to set an algo live based on this results. Of course if you have ran it for some time on demo and this was profitable then one might dare to try but based on this tests – no. But this is my personal opinion and others might of course have a different opinion.

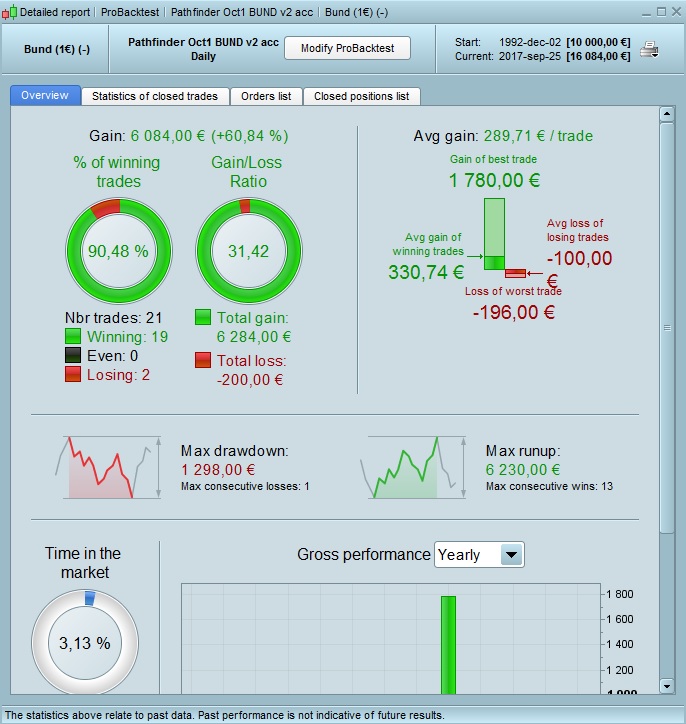

BUND and DAX with accumulation based on Oskar’s versions.

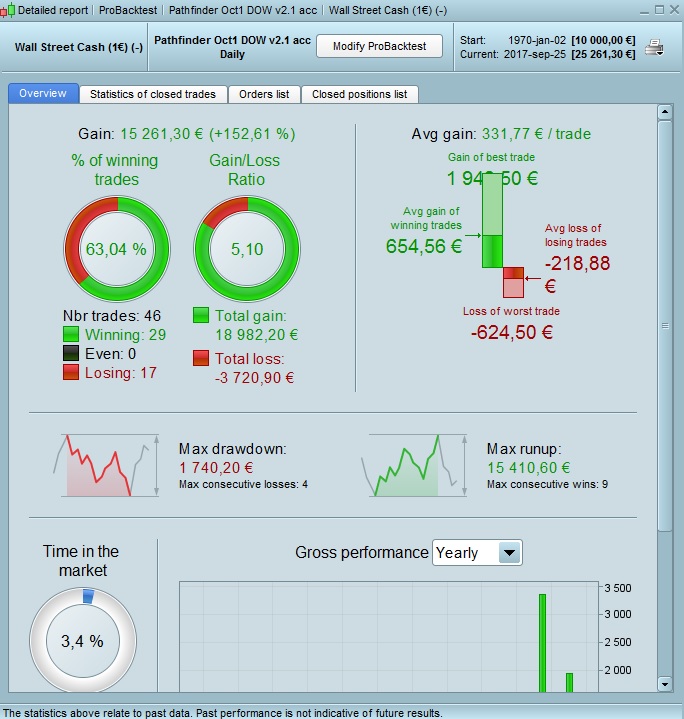

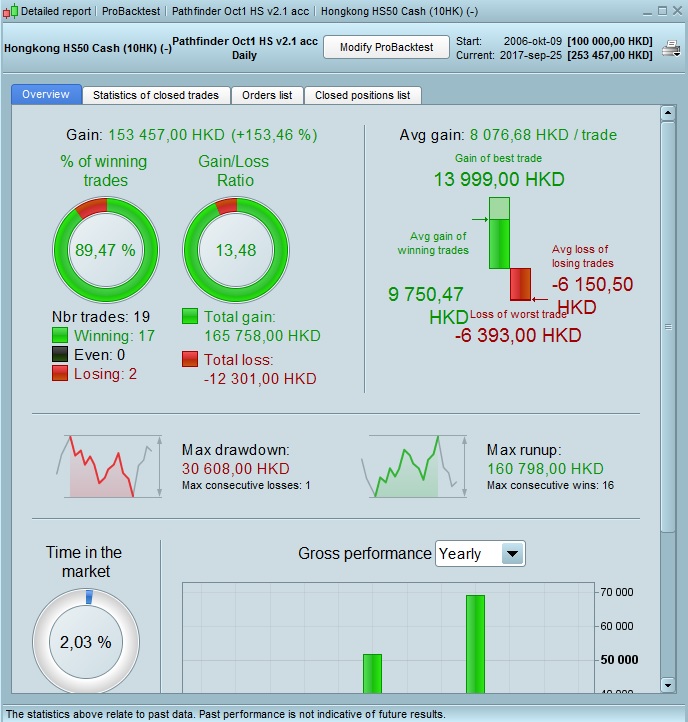

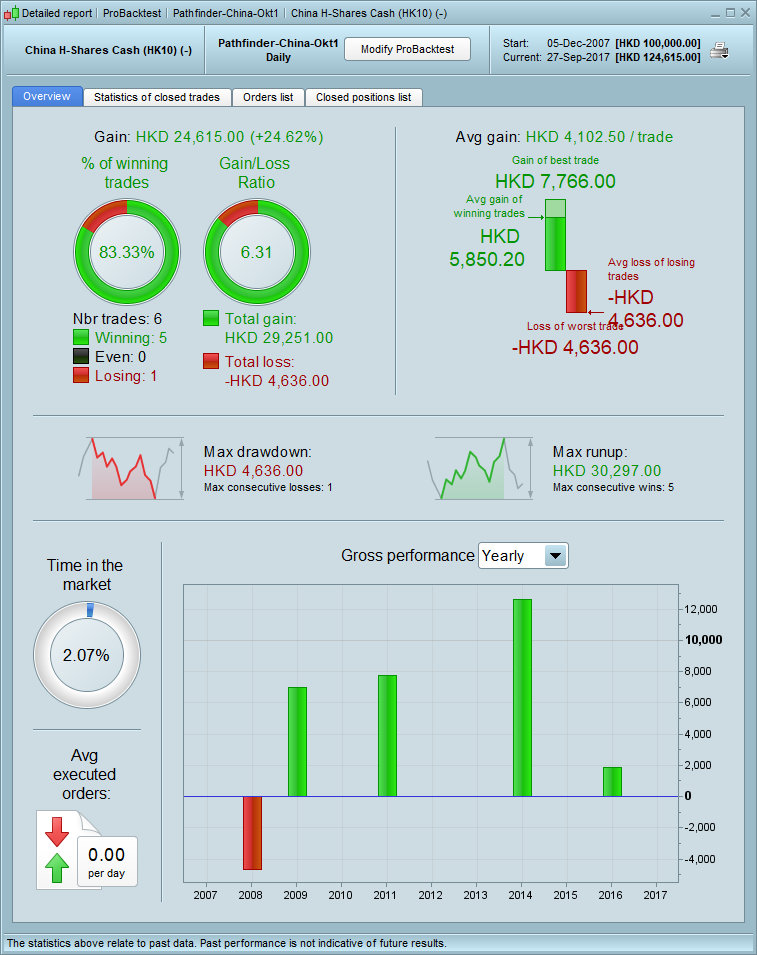

DOW and HS with accumulation based on Oskar’s versions.

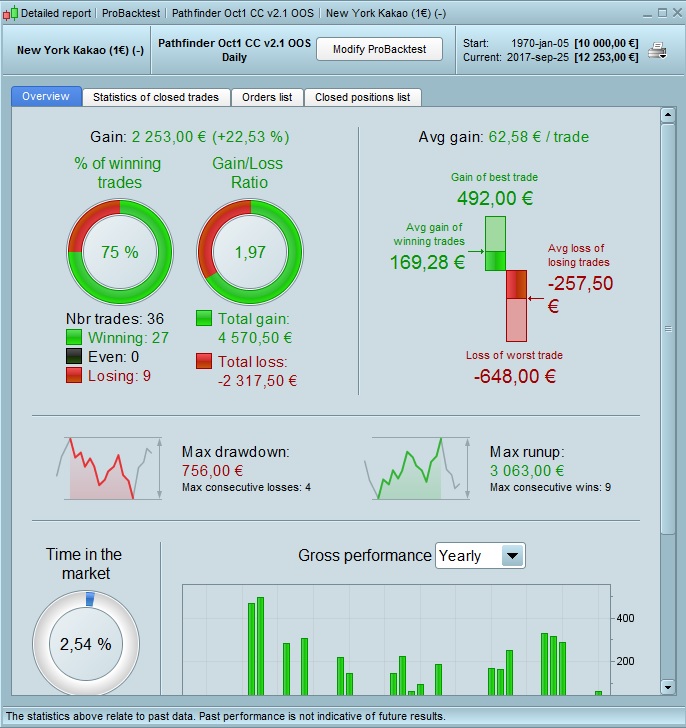

CC optimised 1970-2000 and LB optimised 2005-2013 with accumulation.

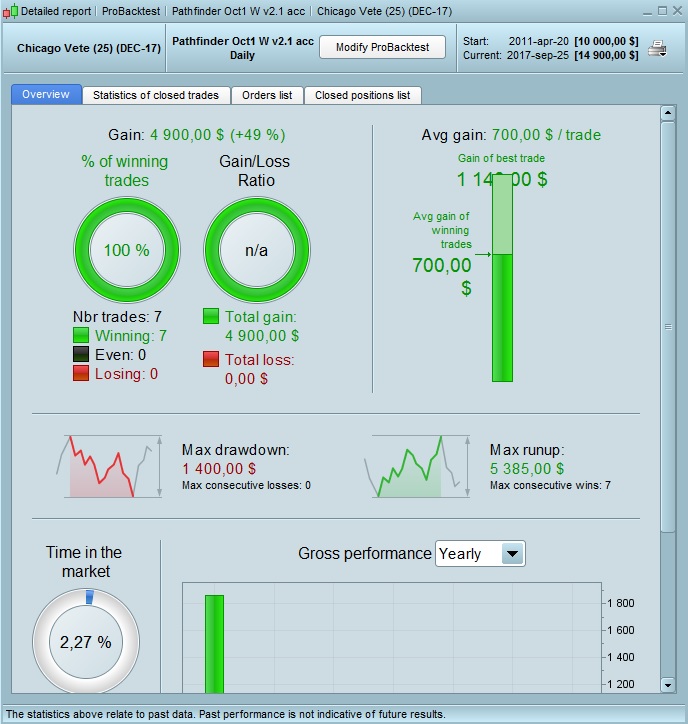

And W with accumulation. Tried OOS, but got the same result. Probably since the testing period is so limited.

wp01Participant

Master

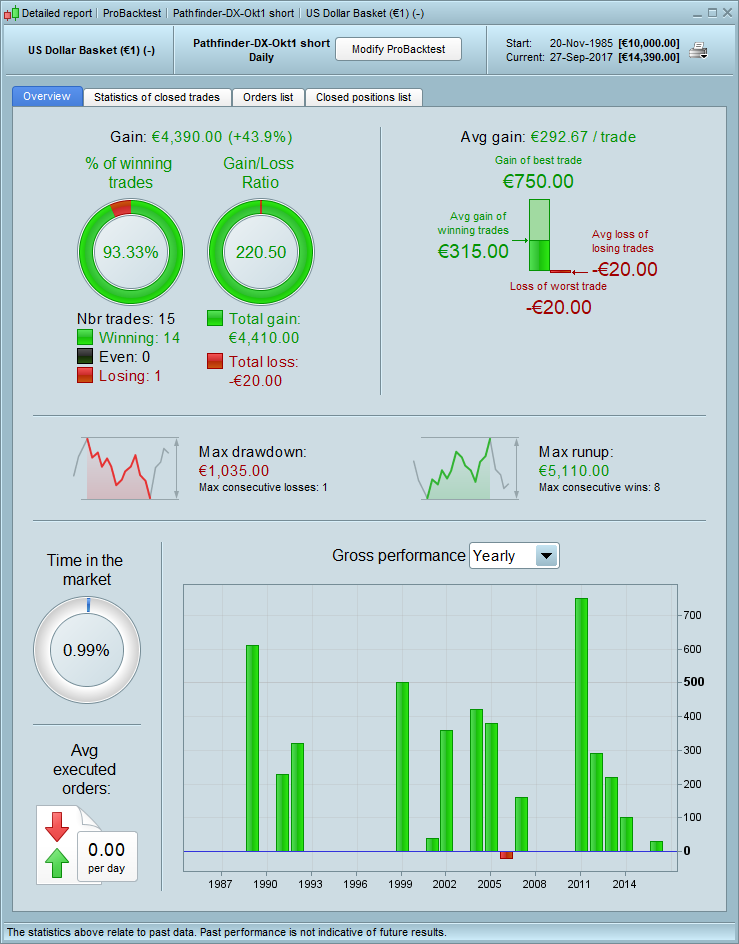

US Dollar Basket Okt1 short:

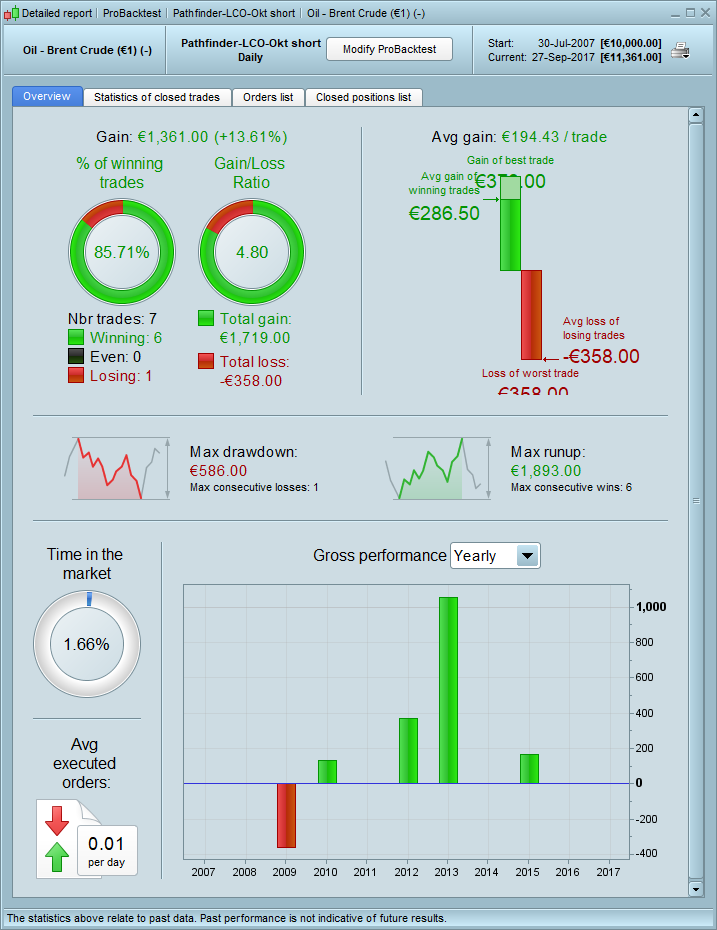

Brent Crude Okt1 short:

wp01Participant

Master

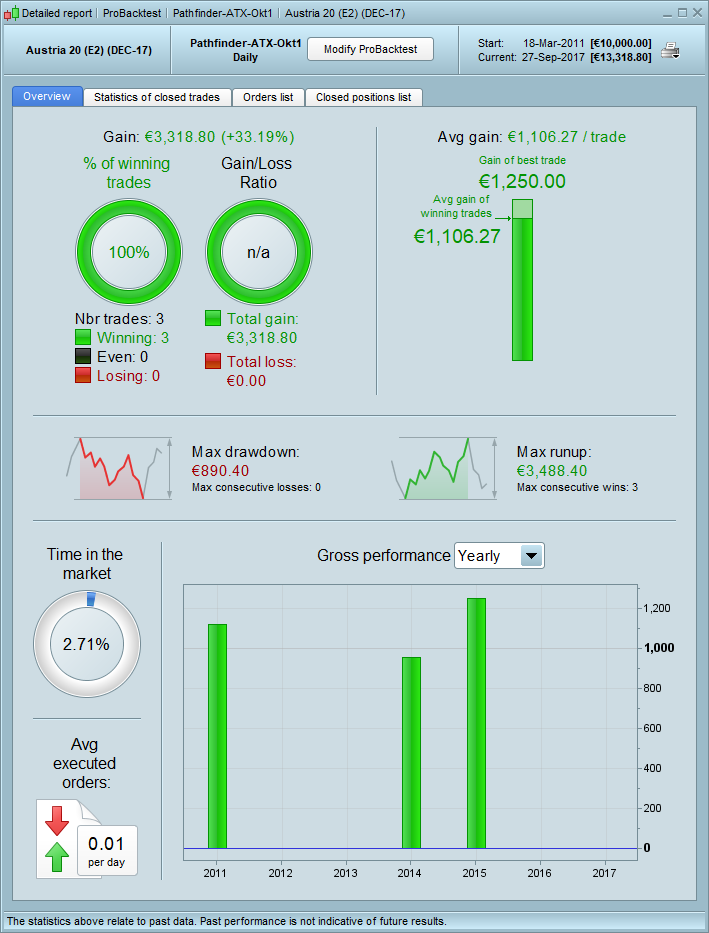

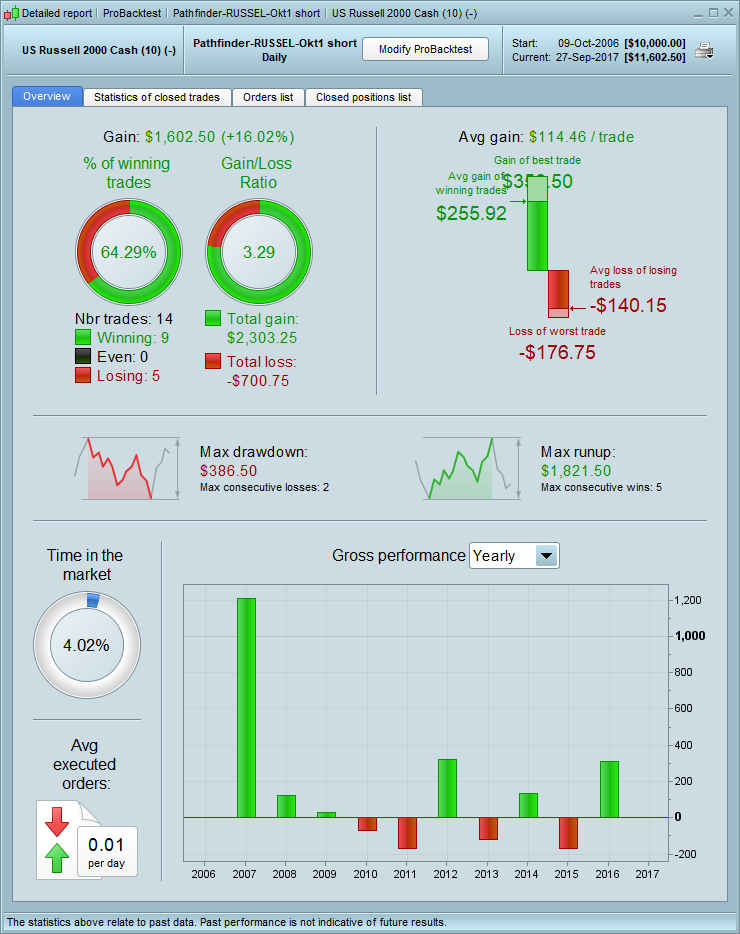

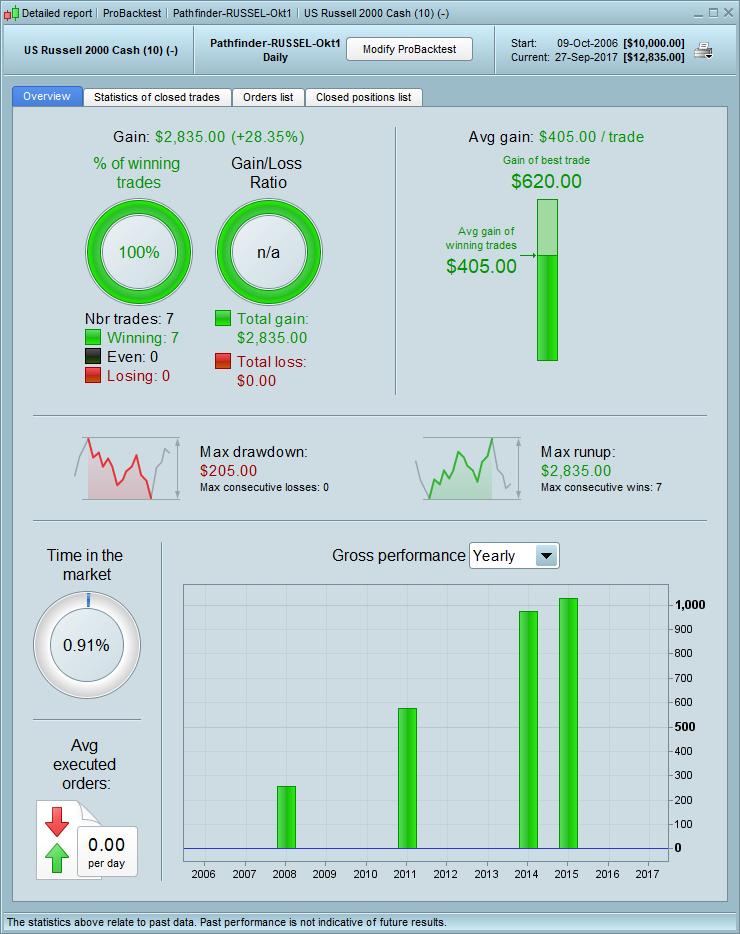

Russel 2000 Okt1 long and short. Both with accumulation:

wp01Participant

Master

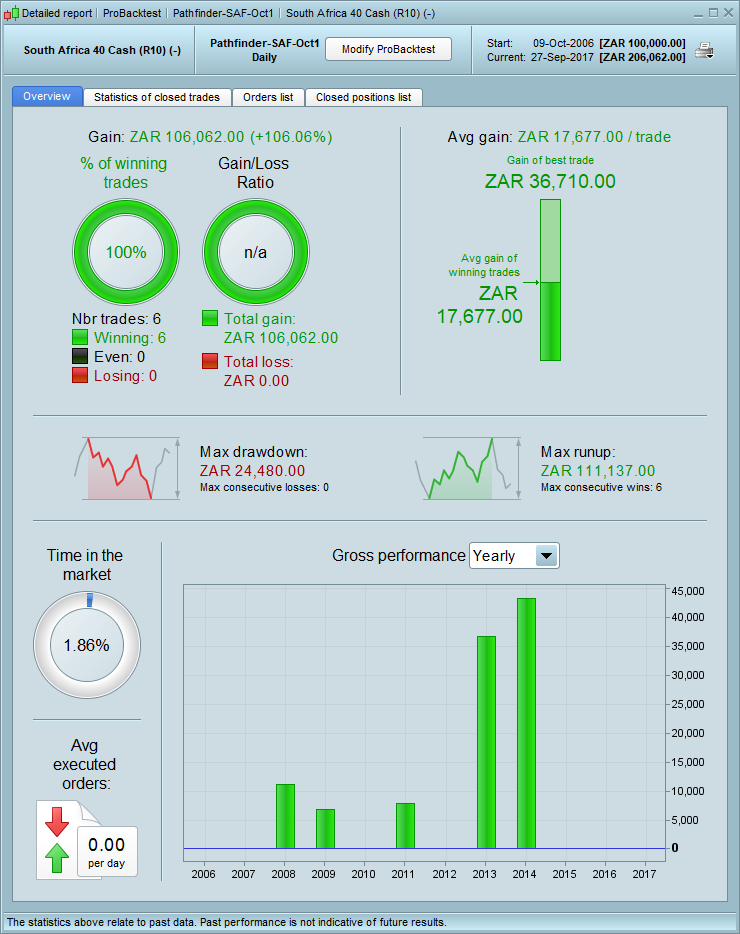

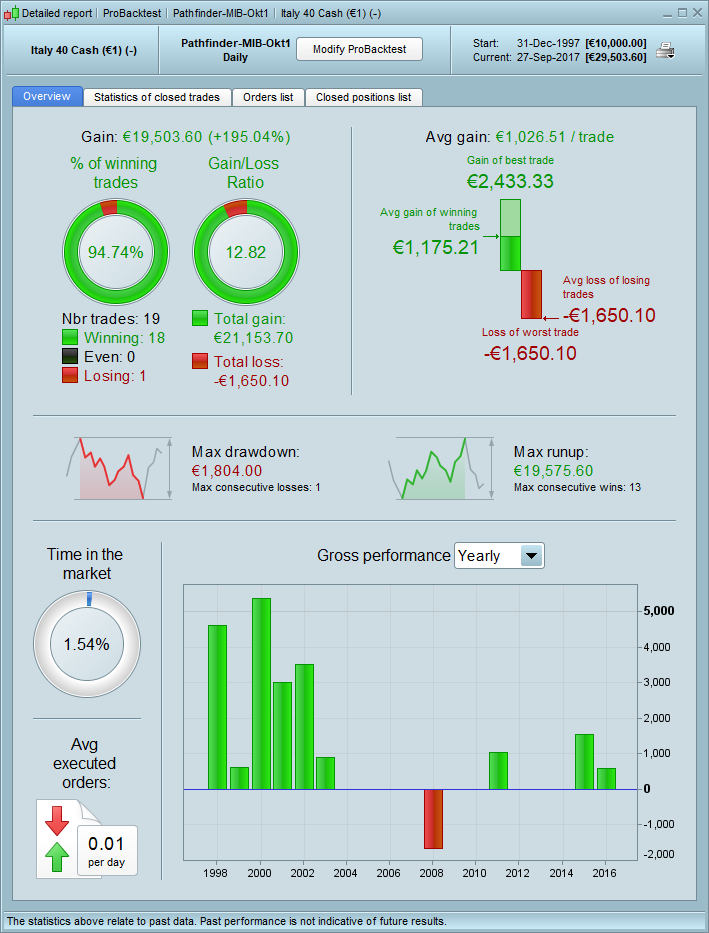

MIB Okt1 :

Short no results, long a higher DD.

Not sure if I’ll start any new ones for October. Many positions up already and they are not going well…