wp01

wp01Participant

Master

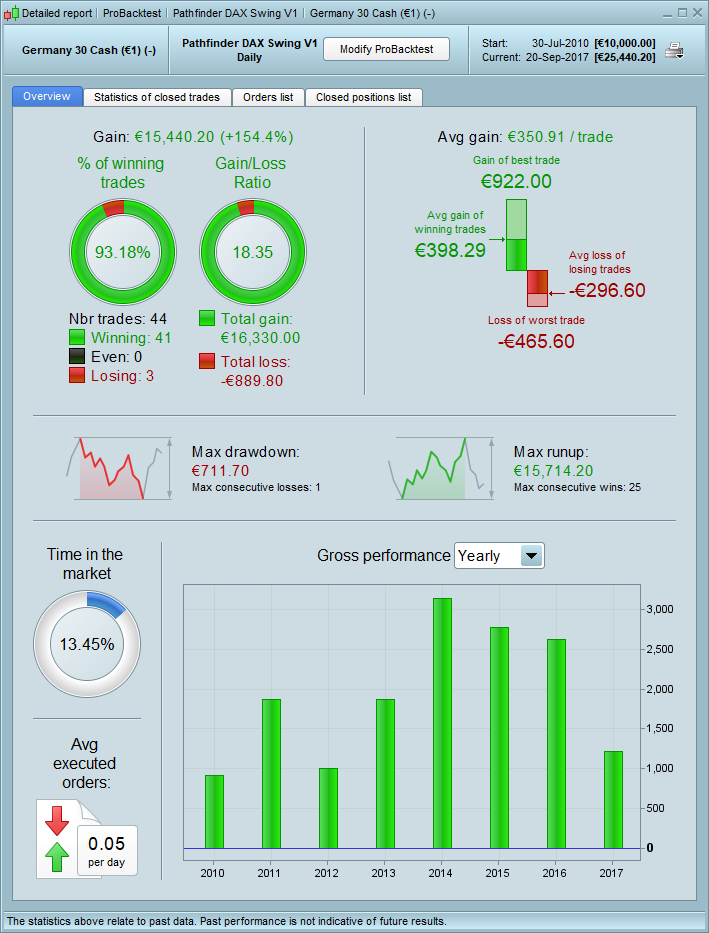

DAX swing V1 until october:

I think in this latest version from Reiner where you can add all variables in the month you have to make

two versions, one for long and one for short. In Oskar’s version i deleted the short periods from Aug1, Sep1 and Sep2. I also added October 1 and 2.

This is the tick by tick mode, which means with data from 2010 and on.

Maybe it is useful when it is finished with to lats two months we also try with walk forward.

@Patrick

In S v1.

I tried to implement the new features from S v1 to any v2, but too much has changed between the versions so a quick fix was not possible.

1 long and 1 short full year version is acceptable I think.

wp01Participant

Master

I think line 54 in S doesn’t belong there. From my rookie site of view it doesn’t make sense. If you look at the other periods it is build every time the same way.

If you leave it out the BT remains the same.

These versions changed too much for a quick fix. I noticed myself that one mistake doesn’t give any result at all.

I think the quickest way is to continue with the two weeks periods and add them later in the new swing version. After that we can use the swing as template.

Yes 2 versions is ok 🙂 So for the 30 or so different indices/commodities it would be 60ish running algos.

Dax looks very nice now with your version 🙂

wp01Participant

Master

Yes but 60 algo’s is not for every account. And they will not trade all at the same time. There are a lot of zero periods among them. We will see what it brings us.

You experience now that it is not easy to look at your negative positions every day. When the market is supporting you and it goes your way, it is really

nice. In february, april and july those were really good months. But it is a way of trading that has to suit you.

Wp01: Yep. But if you have the capital and want to do minimum effort you could just have them all running I suppose. I want just a few for each period so I’d still have to check every period which ones best to run.

This looks tempting indeed. Good work guys.

Or you could have all the 60 algos in the “not running section” and just follow Pfeilers RW-ratings and activate the ones you prefer each period.. 🙂 Of course it will take alot of work to do all the algos but after that nearly no effort to use them.

wp01Participant

Master

Yes that will also work. You can store there 150 algo’s.

Indeed a lot of work. And there are also several versions of each instrument. In almost all cases i just took 1 position, even if the roadmap said 2 or 3.

I prefer to take it slow and see how it develop. Others go all in. You see now how it goes with CAC, DAX, EU stocks. Nice BT but there has not been a moment

that they were in profit in the last two weeks. Hard to understand. Maybe over optimized. No idea what to do about that.

Since I am running all versions, plus some with my own alterations I see that either they don’t open at all or 1 of 3 open or they all open at about the same time, maybe a day or two difference. The difference comes when the algo is told to exit.

September is a low month for the markets.

wp01Participant

Master

Yes there is definitely a pattern in it. Most indices run in the same direction. It is not that when the U.S. is at it’s highest, that Europe is in a bearmarket. The rest of the world will

still follows the line of overseas. When the basic of the code is the same it is clear that positions will probably open more or less at the same time. That is probably also why there

were about three well performing periods this year. Most positions opened in the same direction and had the market in their back.

Regarding september i had already my doubts on forehand with the shorts. When everybody expects a downturn, it never happens. Most media tell a correction is overdue. it is probably

postponed to october when we are long 🙂

But nevertheless just a nice profit from PF DowJones 4H of € 774,00. And that is well timed at the moment after the surge of yesterday evenening.

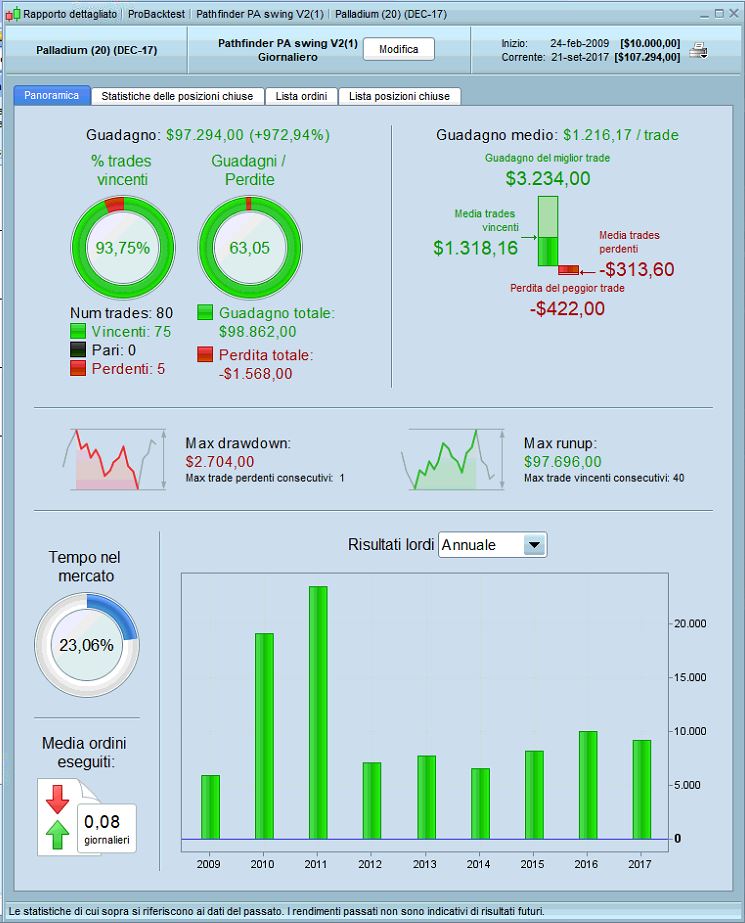

Hi all,

i have do some optimization of the last Reiner code for Palladium. I have do optimization for every 15 day of the year of the following variables :

periodFirstMA

periodSecondMA

periodThirdMA

maxCandlesWithProfit

maxCandlesWithoutProfit

The result it is great!

Let me know your opinions.

You guys here should really start making OOS-Tests with your algos! Look at the results here (and this is just an example of many) from Mat_CH. Does anybody here really believe this has anything to do with how the algorithm will perform in the future?

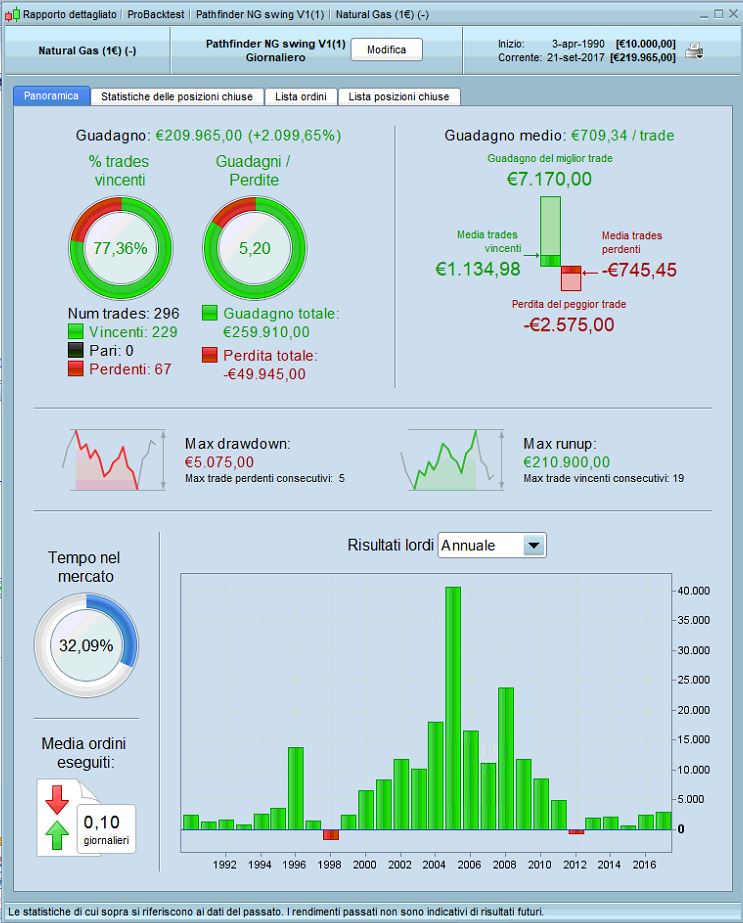

Hi all,

also an optimization of Natural Gas but only with the following three variable every 15 days:

periodFirstMA

periodSecondMA

periodThirdMA

Let me know your opinions

wp01Participant

Master

Hi Despair,

Maybe you are right. Nobody knows. Admitted the results are a bit lame lately.

You know it is work in progress and under construction. If i speak for myself i can surely say that the past 11 months were quite promissing.

It can not all be luck. I know we have to move on and bring it to the next level.

I assume with OOS-tests you mean walkforward test? I know you are busy on the forum but maybe you have some spare time

to help us further. It will be appreciated. Thanks in advance for your support.

Kind regards,