Hello everyone,

I found this strategy called ” Winning Pips System” (you can see it just by searching “winning pips system” on Google).

The strategy seemed profitable and I wanted to test it.

Disappointment :

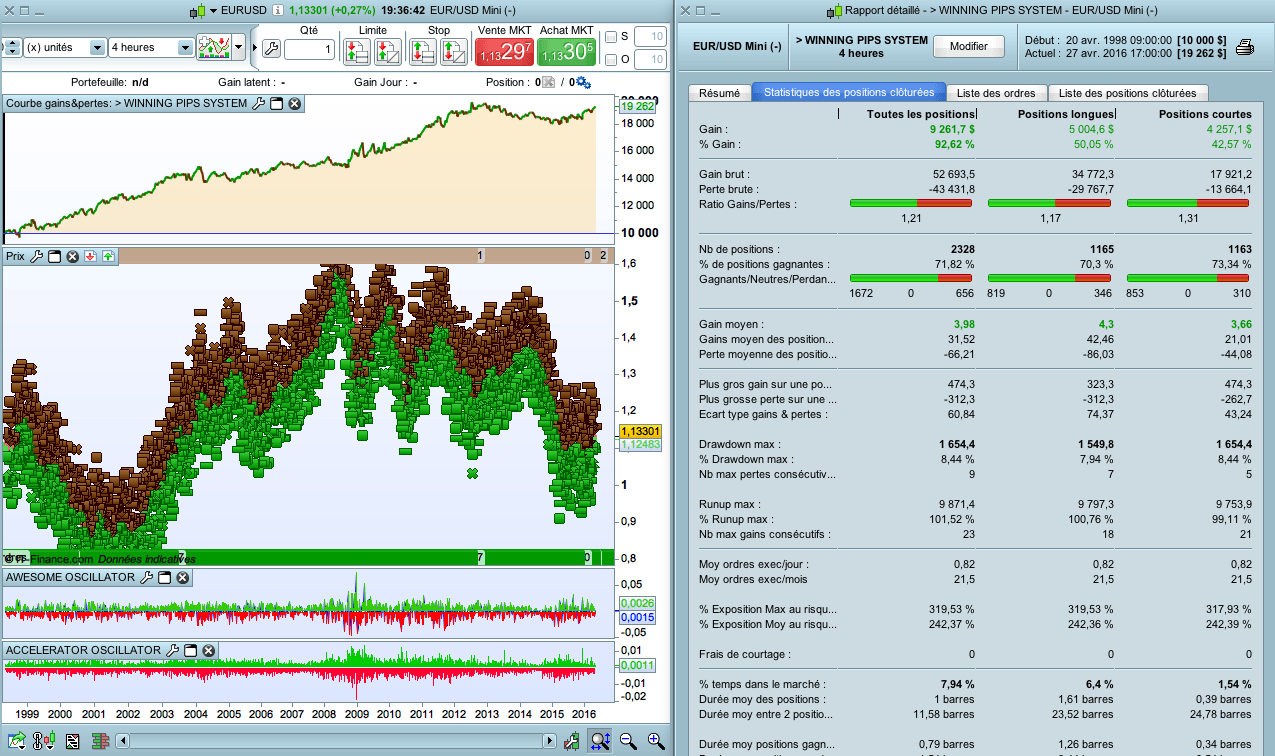

– It loses below the H4 timeframe, because of the spread (if there was no spread, it would be winning in H1)

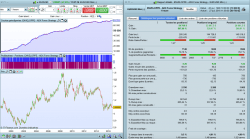

– To be a winner, the take profit must be 2 times more little than the stop loss. However, even with a 1.5 point spread on EUR/USD (see backtest ), the strategy is profitable.

No doubt it is improvable .

It’s your turn !

|

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 |

DEFPARAM CumulateOrders = False // TAILLE DES POSITIONS N = 2 // DEFINITION DES INDICATEURS AO = Average[5](medianprice) - Average[34](medianprice) AC = AO - Average[5](AO) PSAR = SAR[0.02,0.02,0.2] // 1 SEUL TRADE par changement de SAR IF close crosses over PSAR THEN phase = 1 ELSIF close crosses under PSAR THEN phase = -1 ENDIF // ACHAT ca1 = AO > AO[1] ca2 = AC > AC[1] ca3 = close > PSAR IF ca1 AND ca2 AND ca3 and phase = 1 THEN buy N shares at market amplitude = close - low phase = 0 ENDIF // VENTE cv1 = AO < AO[1] cv2 = AC < AC[1] cv3 = close < PSAR IF cv1 AND cv2 AND cv3 and phase = -1 THEN sellshort N shares at market amplitude = close - low phase = 0 ENDIF // Stop Loss and Take Profit SET STOP LOSS amplitude SET TARGET PROFIT amplitude*0.5 // Stop loss au SAR sell at PSAR STOP exitshort at PSAR STOP |

Share this

No information on this site is investment advice or a solicitation to buy or sell any financial instrument. Past performance is not indicative of future results. Trading may expose you to risk of loss greater than your deposits and is only suitable for experienced investors who have sufficient financial means to bear such risk.

ProRealTime ITF files and other attachments :

Find other exclusive trading pro-tools on ![]()

PRC is also on YouTube, subscribe to our channel for exclusive content and tutorials

Hi Doctrading!

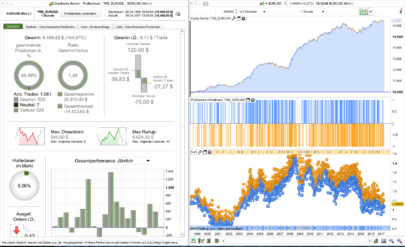

I did a backtest and a little change from amplitude*0.5 to amplitude*1.7 (Profit) with this results: :O

http://www.prorealcode.com/wp-content/uploads/2015/07/USD-Wining-pips-.png

Hello. Results are better with amplitude * 0.5Less drawdown, best profit factor on my test.But BEWARE ! You are using the test on EUR/USD, I am using it on EUR/USD MINI-CONTRACT.So you’re not just using n = 2, but n = 20. The drawdown is inacceptable (more than the initial capital).

Don’t forget also to set the SPREAD.

Best Regards,

Hi,

I have oprimized on EURUSD MINI starting from January 2016.

Best result with low drawdown:

TF 3H

AO = Average[10](medianprice) – Average[32](medianprice)AC = AO – Average[10](AO)

TF 4H

AO = Average[5](medianprice) – Average[32](medianprice)AC = AO – Average[5](AO)

I think to start these strategy in real account…what do you think ?

Tanks

Emanuele

….i have optimized with 1.5 spread….

Hello.It’s not much better, I think.

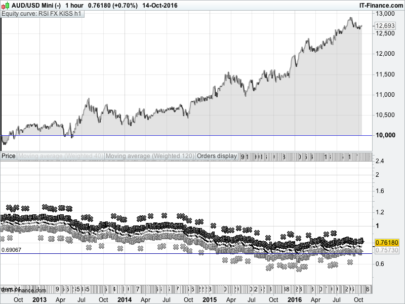

Although this strategy is interesting, I don’t find it profitable. My own codes (daily timeframe) make > 25% each year, this one make less than 6% each year…

I think that the “End of Day USD/JPY” that I did post before is more profitable.

Bonjour à tous,

Je suis, en général, assez effaré de voir cette course au meilleur backtest, à croire qu’il n’y a pas de traders ! Car le gros problème des backtests, c’est leur fiabilité. Il suffit de décortiquer les ordres “tests” pour s’apercevoir que beaucoup de positions données gagnantes sont en fait …perdantes. Le target profit, s’il est atteint dans le timeframe, considère le trade gagnant, même si le stop loss est atteint avant. On peut donc aller vers beaucoup de désillusions, même avec de bons backtests. Donc avant de se lancer : testez les tests !

Bonjour,

Tu as raison, il faut faire attention à la fiabilité de certains backtests. Le problème du SL et du TP sur la même bougie est bien connu sur ProRealTime, une prochaine version devrait corriger ce problème. Ceux qui comme nous codent régulièrement connaissent bien le problème, nous savons rester critiques devant un backtest “trop parfait”.

Je vérifie que ce problème n’existe pas sur les backtests que je publie, et avant de me lancer en réel je teste mes stratégies.Après tout, ça fait maintenant 3 ans que j’utilise deux stratégies qui avaient été backtestées sur PRT par mes soins, je m’y suis fiée à la lettre, et ça fait 3 ans que je gagne, je ne vois pas pourquoi je changerais… (stratégies en graphes Daily, jamais d’entrée et sortie sur la même bougie, une seule position à la fois, donc aucun problème pour le backtest). Je pense que > 80% des traders à domicile / amateurs ne peuvent pas en dire autant.

Belle journée à tous

Hi DocTrading,

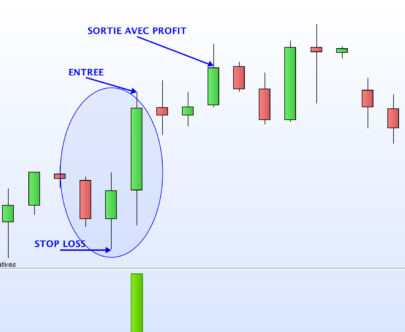

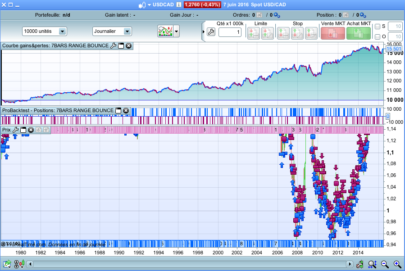

I’ve backtested your strategy and I notice that 75% of position have been closed in 0 bar.

Have y0u tested this strategy in real account? The profits are the same of the backtest?

Thank you so much

Hello,

No, I don’t use this strategy on real account, because my own strategies (that you can see on my website) in real account are FAR better, and not on forex but on indexes / stocks.

But I post some codes here, because I’m still looking to making a good forex strategy, so I test different ones.

Best regards,

Marc