Kase Peak Oscillator

April 30, 2016, 10:28 AM

Indicators

9 Comments

{kind=link}

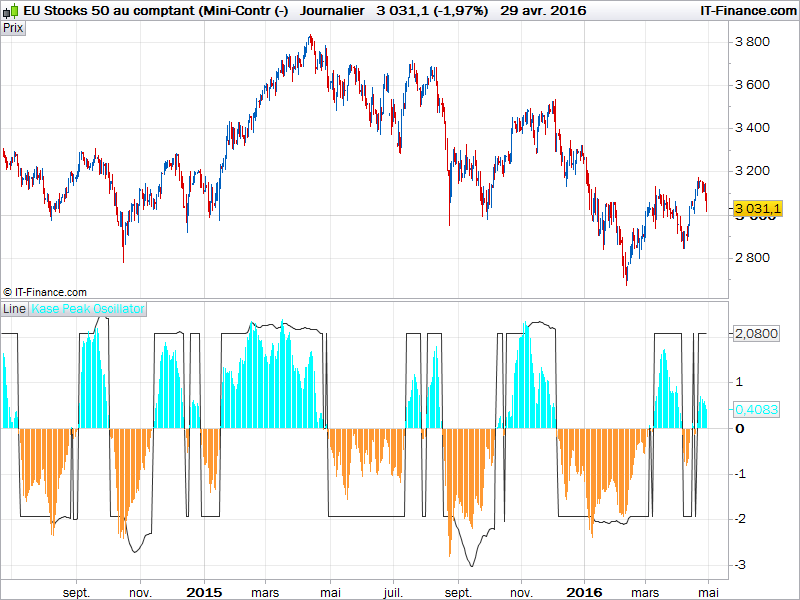

The Kase Peak Oscillator is made of statistical observation of prices over the last KPeriod. It automatically adapt its cycle to any timeframe or instrument by using a percentile rank of what happen now in comparison of the whole distribution of past values.

The KPeriod would be adapted to trade horizons.

KPeriod = 30

sq = sqrt(KPeriod)

rge = averagetruerange[KPeriod]

RWHL = ((High-Low[KPeriod])-(High[KPeriod]-Low)) / (rge*sq)

Pk = weightedaverage[3](RWHL)

mnn = average[KPeriod](Pk)

dSum=0

for i = 0 to KPeriod do

dSUM = dSUM+(Pk[i]-mnn)*(Pk[i]-mnn)

next

sd = sqrt(dSUM/KPeriod)

v1 = MAX(2.08,mnn+(1.33*sd))

v2 = MIN(-1.92,mnn-(1.33*sd))

if (pK[1]>=0 and pK>0) then

Line = v1

elsif (pK[1]<=0 and pK<0) then

Line = v2

else

Line = 0

endif

RETURN Line as "Line", pK as "Kase Peak Oscillator"

Download

Filename:

Kase-Peak-Oscillator.itf

Downloads:

106

Master

I created ProRealCode because I believe in the power of shared knowledge. I spend my time coding new tools and helping members solve complex problems.

If you are stuck on a code or need a fresh perspective on a strategy, I am always willing to help. Welcome to the community!

Author’s Profile

Loading...