Hello,

Using Dax PathFinder V6B2 this morning I had a Long signal at 9:00

Long 3 contracts@11467,2

Can anybody confirm?

Regards

Massimo

@Massimo

I am running v6 and Pathfinder went long with 2 contracts at 9 am 2 days ago at 11447.7 and then again 2 contracts 9 am today at 11467.4.

Regards, David

Hi guys,

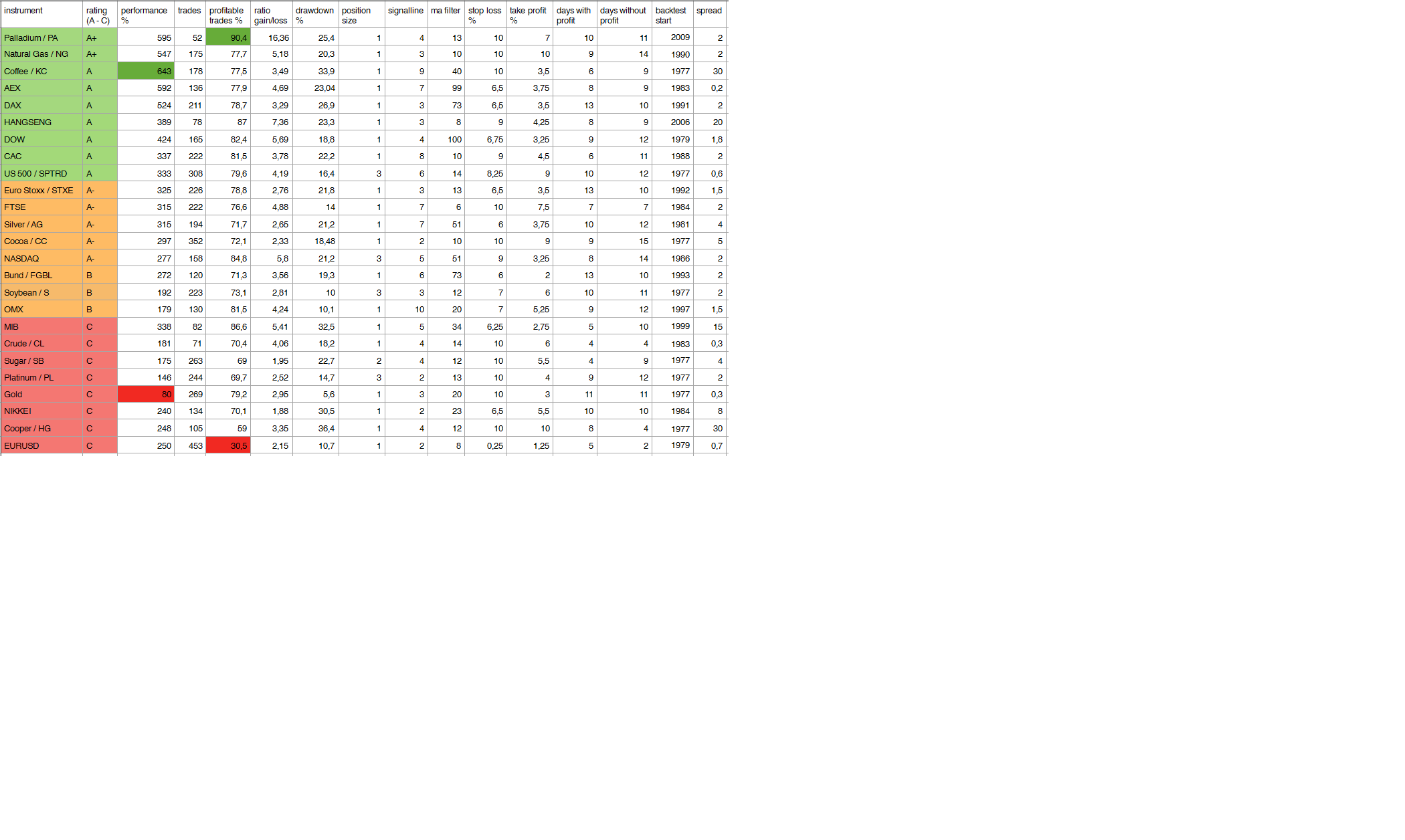

I want to give you an update about Pathfinder Trading System.

I have tested 25 instruments with the Pathfinder daily version V2 to find out which are the best suitable underlyings. Requirements for every backtest were that the number of profitable trades are over 70% and that the drawdown wasn’t highter than 25%. I have rated all backtests, the best ones with A+, A or A-, the good ones with a B and the worst ones with a C. The rating is a mixture of how easy was it to find a “smooth equity curve” and the real numbers of the backtest results especiallity the performance (not quite fair because of different history), number of prof. trades and the drawdown.

Pathfinder daily could work as a signal generator for swing trading of instruments that works well (A+, A, A-) with the breakout algorithm. For instance using a demo account and set up a mail trigger and follow with futures, cfd’s or ETF’s.

Another approach could be to develop a portfolio strategy with the aim to reduce the risk and trading instruments from different asset classes that are not related (e.g. DAX, coffee, palladium). Next, I will check the other timeframes (4H, 1H, 1D) for the best instruments.

The journy isn’t over and it remains exciting what will be the result of this little algorithmic trading project. Also in 2017 I will publish everything related to Pathfinder TS, everyone can use it for free and at their own risk but I promise nothing.

MCAAHNY, Reiner

code palladium ? where is . thanks

ALE

ALEModerator

Master

Hello Reiner,

Thank you very much for your great work!

Hi Reiner,

I have been following the discussions for a while now more as a passive observant trying to learn. I would like to thank you for sharing so much useful information in this forum.

Frohe Weihnachten und guten Rutsch,

Asura

Hi guys,

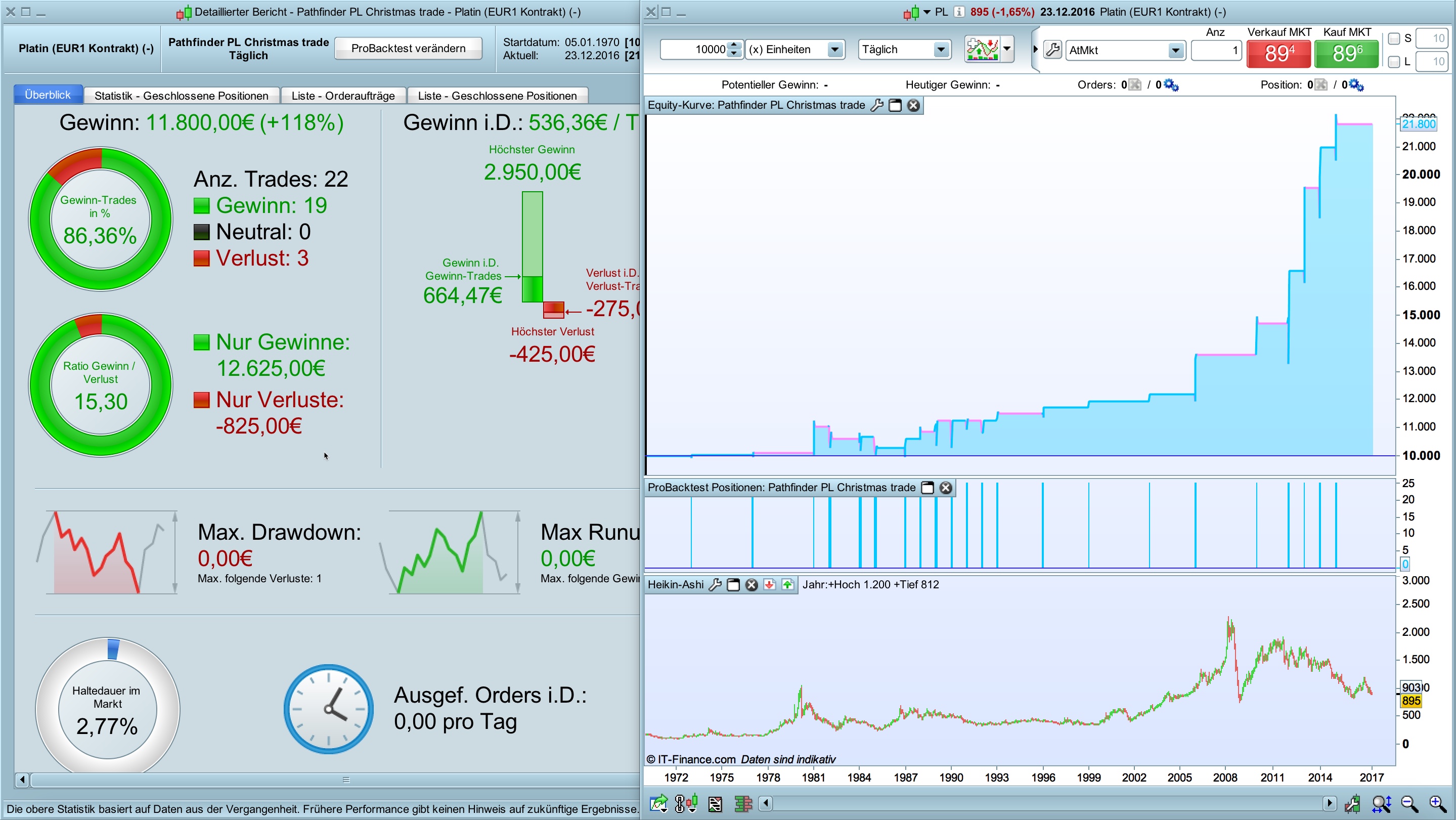

Platinum PL has a very well known saisonal pattern around Christmas. This swing trade is called “Christmas present” because of the very high success probability. Buy around Christmas and Sell in mid/end February works very well over the last years. I have adjusted Pathfinder PL daily for that scenario because I have seen that the trade trigger isn’t yet active for this year.

Please adjust the position size to your account size if you want to trade this setup. The attached code is for an 10k Euro account and trade 25 PL minis.

Best, Reiner

Alco

AlcoParticipant

Senior

Hi guys!

Do you think to trade with dow, DAX and ftse 4h (last versions) in one 10k account is enough? Or do someone know a better portfolio with the system with the knowledge we know at this moment.

Regards,

Alco

Salve Miguel,

as requested, here the Pathfinder PA daily V2.

Saluti, Reiner

Great work Reiner!

I have basicly two questions:

- Which parameters to change for a daily algo to test new instruments? I read on first page what to change in original version for 4h algos.

- Which parameters to adjust and which script to base it on? DAX 4h v6? Newer versions are a bit different than original.

Edit:

Just did a versioncompare of DAX daily v2 with PA daily v2.

Difference is following lines:

periodThirdMA

periodLongMa

stopLossLong

takeProfitLong

maxCandlesLongWithProfit

maxCandlesLongWithoutProfit

currentDayOfTheMonth

and seasonal adjustments

I think several people here can test different combinations making the time to find good versions shorter and helping eachover.

Hi hakke,

Take the Pathfinder PA daily as a template.

You can adopt Pathfinder daily very easy to other instruments. Set 3. to 6, 4. to 3, 5. and 6. to 10 and optimize 1. and 2. in below ranges with the aim to find a first positive equity curve. Start with 1 for all saisonal adjustments. If you have a positive result start again and check all variables focus on drawdown and profitable trades. If you find a positive result set all saisonal adjustment to 0 and optimize all saisonal multiplier (0 -3) start with January. Keep an eye on drawdown and profitable trades. With a little practice you are finished in 30 minutes.

1. periodThirdMA (between 1 -10)

2. periodLongMA (check values beetween 10 -100)

3. stopLossLong (5-10)

4. takeProfitLong (between 3-10)

5. maxCandlesLongWithProfit (5 – 15)

6. maxCandlesLongWithoutProfit (5 – 15)

7. saisonal adjustments

All Pathfinder backtests have to fullfill the two quality requirements: profitable trades > 70% and drawdawn not higher 25%. Try to avoid curve fitting e.g to less trades or a too short data history. Reduce position size if your drawdown is to high. Start with the mini version of an instrument.

Best, Reiner

Hi Reiner,

trying to increase positions on 4H I tried to add a new long condition

l5 = signalline CROSSES OVER weeklyLow

This condition add 23 new long positions with 82% of winning trades with a drawdown of 2700€.

Maybe can be useful to someone.

CKW

CKWParticipant

Veteran

Hi Reiner,

I am running live demo of H4v6 based on replied #17981. My system stopped last week due to “insufficient pre-load bar”. What could be the possible issue?

Time Zone CET, No custom Trading Hour in Platform option.

br,

CKW

CKWParticipant

Veteran

Sorry, Reiner.

I re-send with complete question.

Hi Reiner,

I am running live demo of H4v6 based on Post: post-17981

My system stopped last week due to “insufficient pre-load bar”. What could be the possible issue?

Time Zone CET, No custom Trading Hour in Platform option.

Minor Code changes on following:

- Change positionSize from 1 to 5

- Remove “l1” from buy condition

br, CKW

Hello Rainer and really big thx to this code and I appreciate your work.

Also great job of the community I really appreciate the work and ideas here in the community.

Has somebody tested the code in the 5 minutes timeframe ?

Regards