Hi @Reiner,

I’m from Singapore and I’ve updated my country in my profile.

The default timezone in my IG ProRealTime platform is local time, i.e. UTC +08:00.

By just adjusting the startTime and endTime variables, wouldn’t the daily Highs and Lows be affected in some occurrence?

Second, will chart running into/from weekend (Saturday local time in my instance) affect this system?

Last, will daylight savings be a consideration as well?

Thank you.

wp01

wp01Participant

Master

@Choo Jen-Sin.

The quickest way to get all your answers is to approach it the other way around.

Reiner always post a detailed report of the results. So you first adjust the date from the backtest to the date in your system. Does it have the exact same profitfactor your done.

If not, you try to change the timesettings one by one as you described. After every change you check again the profitfactor as posted. If it is not the same, you go to the next setting.

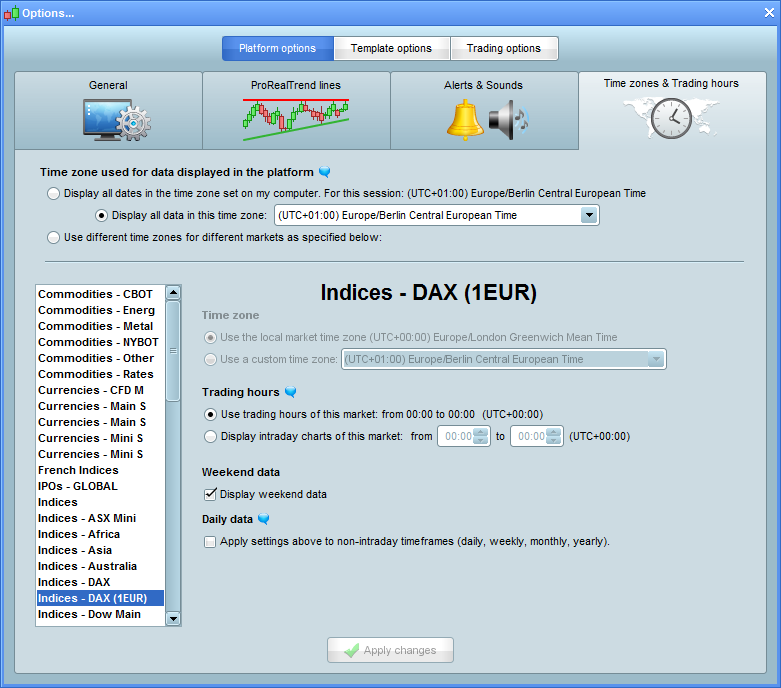

The settings in my system are UTC+1 and there is no daylight savings till march 25th. 2017. Attached a picture. Weekend data display is also marked as you see but that is standard and not changed at all.

Regards,

Patrick

I see this similar to what cosmic said. there are about 250 Trades. If you seperate the “seasonality” in 48 pieces, it is almost as if you rate/rank every single trade 😉 of course there are some weeks with more positive trades and some weeks with more negative trades, but I am not sure if this is a significant behaviour that will continue in the future 😉 But maybe I am wrong. Maybe it useful to seperate between the days of a weekend as a second booster.

Good work reiner. I think the mass of people that are interessted in your system is the best proof that you do some really nice work here! There are some way worse systems out there, that are only available for payment.

mfg

flo

Alco

AlcoParticipant

Senior

You see mainly big movements and higher volatility at the end of the month (last week) and the biginning of the next month (first week). That’s why I thought its maybe better to seperate it in four.

Hi Choo Jen-Sin,

From UTC+1 to UTC+8, you just need to add 7 hours to the time.

ONCE startTime = 160000 //Spore time

ONCE endTime = 004000 //Spore time

You also need to change AND to OR in the time

statement.

//IF Time >= startTime AND Time <= endTime THEN //original

IF Time >= startTime OR Time <= endTime THEN //modified to Spore time

Come daylight saving adjustment, you need to update the startime and endtime accordingly.

Hi Alco,

as promised, here is the adjusted version of Pathfinder DAX 4H V6 with the feature to separate month into four parts. I have the impression that the result delivers a curve fitted equity. In addition 48 variables makes the code a little bit confusing.

Every idea is worth making a test but I believe that two parts for a month should be the limit. Thanks again for sharing.

best, Reiner

Hi Kasper,

Sorry that I have confused you with my release management :-). Usually I start with e.g. V7 Beta 1, V7 Beta 2 and the clean code will then V7. Documentation is realy something that is valueable but also time consuming. I’ll try to make it better.

Thanks for sharing your idea. The motivation reinforcing only the long side was the backtest results. Please have a look to the numbers of the last version V6. Pathfinder generated 586% of the overall 631% return on the long side. Long signals have a higher quality and are more reliable. Pathfinder H4 has now around 300 lines of code and in my opinon the system complexity has reached a limit regarding the saisonal multiplier calculation.

Again thanks for your idea.

best, Reiner

AlcoParticipant

Senior

Thanks Reiner for taking your time to rewriting the v6 code.

Do you mean with curve fitted equity, that you try to adapt the system more and more to get better results from the historical data and does not benefit for the future or even worse?

AlcoParticipant

Senior

Ok guys, I did some tests with the version split in four.

I started with the following settings in the seasonal multiplier:

All months

WEEK 1 | 3

WEEK 2 | 0

WEEK 3 | 0

WEEK 4 | 0

So if you only traded the first week the result: €21000

WEEK 1 | 0

WEEK 2 | 3

WEEK 3 | 0

WEEK 4 | 0

result: €25800

WEEK 1 | 0

WEEK 2 | 0

WEEK 3 | 3

WEEK 4 | 0

Result: €32000

WEEK 1 | 0

WEEK 2 | 0

WEEK 3 | 0

WEEK 4 | 3

result: €17000

These tests are from 9dec 2012-9dec 2016

From this we may conclude in these 4 years, week 3 gave us the most gain.

So I tested again with the following settings for each month

WEEK 1 | 2

WEEK 2 | 3

WEEK 3 | 4

WEEK 4 | 1

Result: €67825 profit

€2939,10 drawdown

Next and last test I did the opposite

WEEK 1 | 3

WEEK 2 | 2

WEEK 3 | 1

WEEK 4 | 4

Result: €55990 profit

€3356,80 drawdown

I know 4 years of backtests give us not enough info, but if we look back at these tests, even in the worst settings it makes money. The drawdown goes higher ofcourse if I put the settings in the worst possible senario. But it probably change in the future so..

Maybe I’m totaly wrong with this approach.

Regards,

Alco

Pere

PereParticipant

Veteran

Hi Reiner.

Perhaps Alco is right, but my impression is also that seasonality would be too complex.

On the other side, I also backtested the versions V6 and V6B2, and surprisingly V6B2 is in the last 4 years slightly more successful than V6, year by year. I don’t know if I’m doing the tests like you, but these are my results. Are you really sure that splitting the monthly seasonality by 2 can give better results than only with 12 months?

PereParticipant

Veteran

However, I also backtested versión V6 month/4, and it gives slightly better results tan V6 and V6B2. That means that V6 could be the less succesful of these three versions. Draw down of V6 month/4 is also the lower ones. Is that right or am I wrong?

Hi Petrus,

I am agree with Reiner that the v6 month/4 is based on very few positions (the year is divided into 52, and you raise almost each winning past position, almost one by one, and avoid the bad ones) so it is not statistically signifiant, and if you adapt this way the past positions, you automatically get better results in the backtest, but live trading in the future might be worse. So I believe more in the V6.

Aloysius

AlcoParticipant

Senior

@ Aloysius,

You are right about ”getting better results” if you adapt the system more and more based on historical data. But in my last test I had still good performance in the most horrible setup. And I did just a simple math.. also with a multiplier set at 4! in the worst week. So in my opinion, if you like to run this system live it looks like it is still profitable if the future is different then the last 4 years. But you probably get higher drawdowns. Please correct me if i’m wrong.

Alco

Mark

MarkParticipant

Senior

Reiner, Petrus, Alco

Regarding seasonal multiplier…

Did you say that generally week 1 and week 4 gives better results? So would it be possible to keep the seasonal multiplier split into 2 but rather than week 1&2, week 3&4 could it not be split up as week 2&3 and week 4&1 and so on…?

Mark

Hi Reiner, and thanks for clearing that up. 🙂

I did some more testing on the money management side. Say that One wanted to go live with a 100000 Euro account. I change the code for this:

ONCE positionSize = 1

Capital = 100000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

maxPositionSizeLong = MAX(150, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(150, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

But It never traded over 15 position- until changed positionsize=10

It this attentional to adjust positionsize manual?

Cheers Kasper