Hi guys,

this topic is for all discussions related to the Pathfinder trading system strategies. The system based on four components that work perfectly together.

- signalline – instrument trend line based on two smoothed averages (Wilder and Time Series)

- breakout levels – previous daily, weekly and monthly high/lows in combination with fast and slow averages as filters because not every breakout is profitable

- saisonal behavior – position size will be boost with a multiplier for each month depending on the historical seasonal behavior

- smart money and position management – grid orders, maximal position size monitoring, superordinate stop loss/take profit, trailing stop and maximum holding periods are used mechanisms

The Pathfinder breakout logic works well for many instruments with 24 hour quotes such as DAX, DOW, FTSE, Hang Seng, NIKKEI in 4 hours timeframe. All versions are optimized for an 10k Euro account.

Pathfinder strategies offer a statistical advantage but are of course not a holy grail and there is no guarantee to make money with it. The systems are optimized for historical data and historical gains are not a guarantee to be successful in the future. I strictly recommend to adjust the position sizes to your personal account size and try first in demo mode. The results in life trading will differ from the backtest results. I also recommend to start in life trading with a small account size. Anyone can use the programs for free and at their own risk.

Pathfinder is my private and fully transparent algorithmic trading project exclusively implemented for ProRealTime 10.3. The status is experimental and I don’t trade all the systems presented here. I would also like to thank all members who have helped to improve the system with their contributions.

Please find below the last released Pathfinder trading system versions for suitable instruments.

Dropbox Link: https://www.dropbox.com/sh/xyymvk6gscxbfbe/AABaOs9_ZExILA18HxKW9kdqa

Best, Reiner

04.02.2018 Updated dropbox with new algos V7-FEB-2018 with automatic scaling for ASX, DAX, DOW, FTSE, GOLD, HS, NIKKEI, SAF and STXE (#post-61450)

08.01.2017 Checkout the results from 2017 (#post-56978) || introducing new PF algo category DAX-1H-V8 (#post-57005) || new algos in dropbox DAX-V7-2018 (#post-57521), DOW-V7-2018 (#post-57524) and HS-V7-2018 (#post-57528)

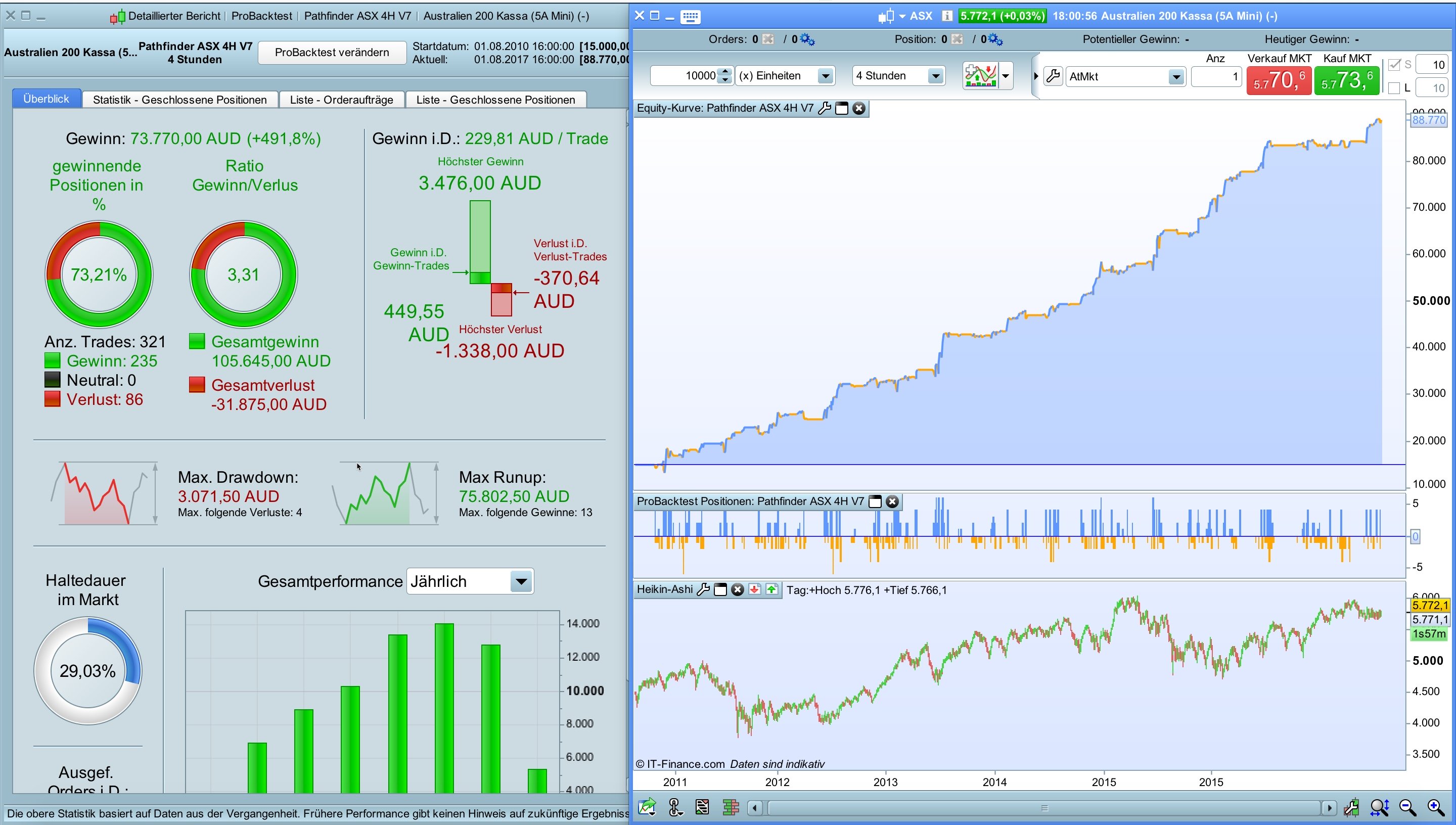

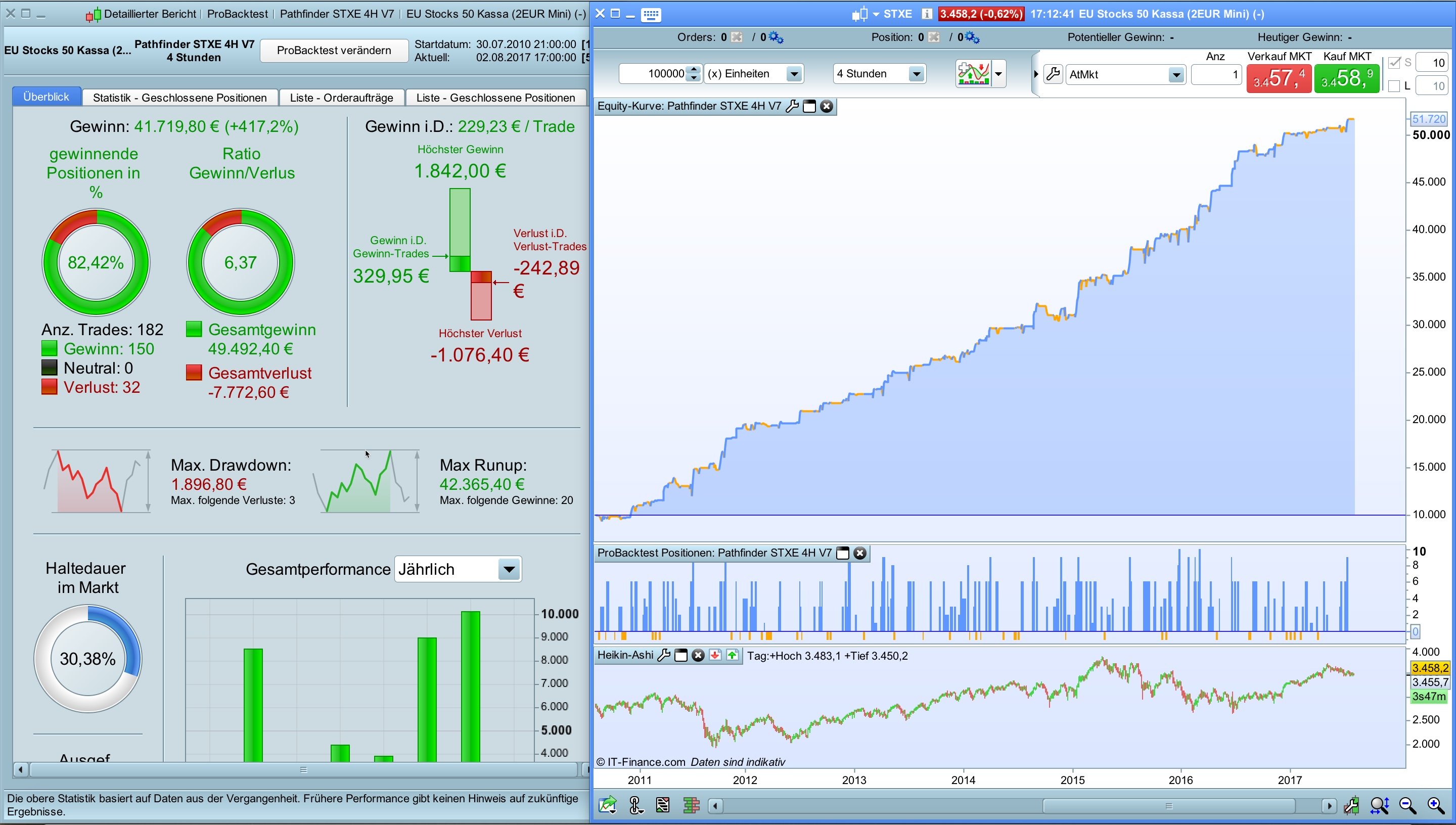

02.08.2017 Updated dropbox with new algos FTSE-V7 and Nikkei-V7 (#post-42223), ASX-V7 (#post-42249) and STXE-V7 (#post-42332)

31.07.2017 Updated dropbox with new algos DAX-V7-2, DOW-V7-2 and HS-V7-2 (#post-41811)

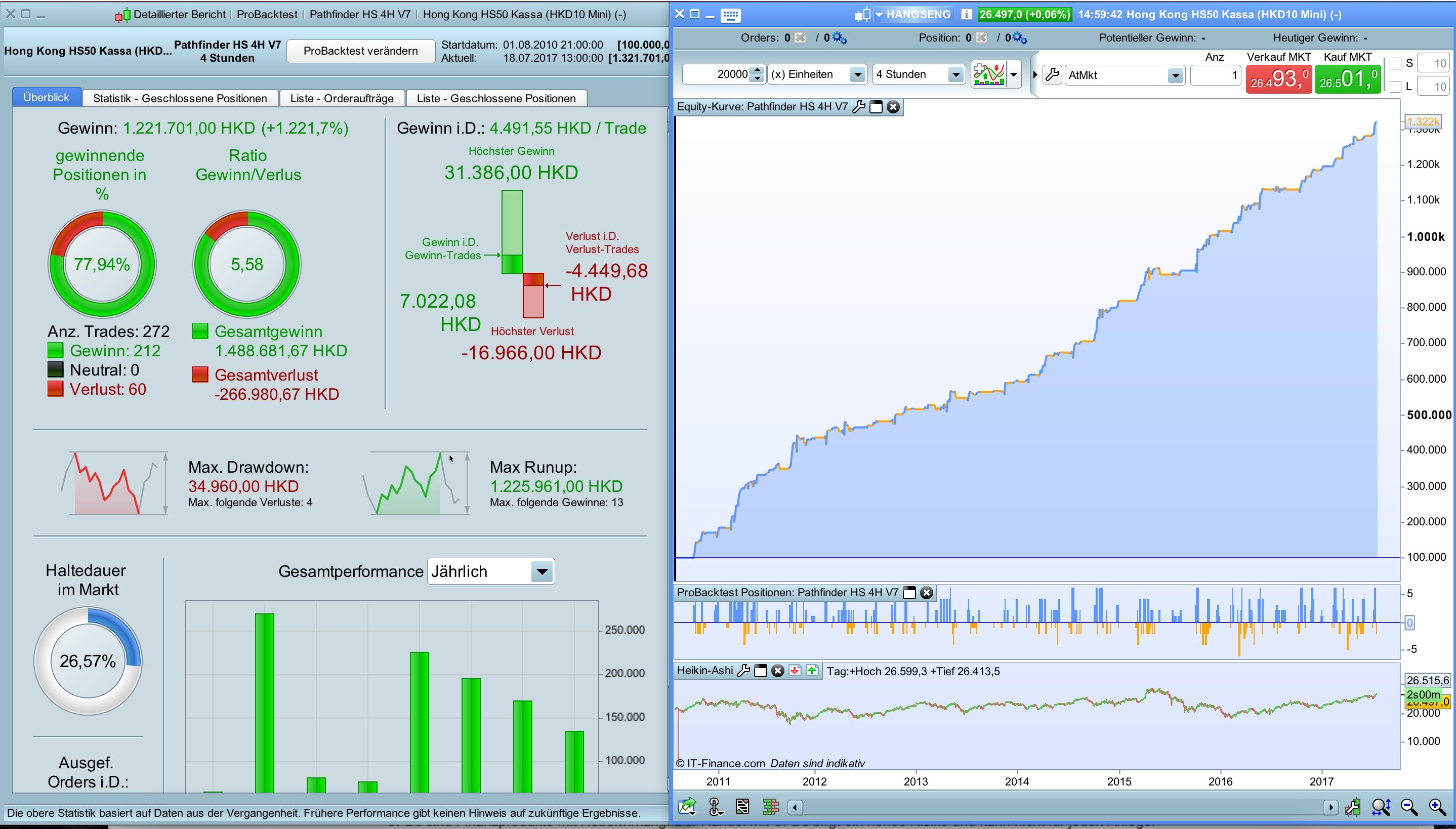

18.07.2017 Release V7 containing error fixes, improvements and new features for DAX-V7 (#post-40798) and DOW-V7 (#post-40880)

Hi Reiner, Great work on the code. Can I ask what variables you have been optimising in your backtests? I’d like to run this live but I wanted to run some IN/OUT testing first.

Hi Cosmic1, here are the optimized variables that are important for your test. Also check these variables if you want to adjust Pathfinder to other instruments.

ONCE periodThirdMA = 3 // this variable define the "heartbeat" of every instrument and have to be adjusted, possible values are 3, 4, 5, 6, 7

// filter parameter

ONCE periodLongMA = 250 // the settings of the filter periods are also important for the profit factor, 200, 250, 300 are good values

ONCE periodShortMA = 50 // 10, 40 or 50 are good settings

// money and position management parameter - these parameters are important for the risk and performance

ONCE stoppLoss = 5 // in % the system would works without a stopp loss, it's more in the sense of a disaster exit

ONCE takeProfitLong = 2 // in %

ONCE takeProfitShort = 1.75 // in %

ONCE maxCandlesLongWithProfit = 18 // take long profit latest after 18 candles - 15 with a higher take profit is my new favorite in the next version

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 12 candles - 13 is a good value for every instrument

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles - 30 or 40 are good values

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles - 25 is my favorite for all instruments

Reiner

it may be useful to avoid returning the same day (or candle) to me makes no sense out of the trade and return immediately after. it would be appropriate to wait a day. what do you think ?

Miguel, I saw it, Pathfinder re-entered in the DAX on the same day – from today’s perspective that’s probably not a good trade. I will try to test it.

Thanks Reiner, I presumed that was the case. That is a lot of variables so will have to cut it up in to chunks and run many tests. Will try it over the weekend and let you know what I find.

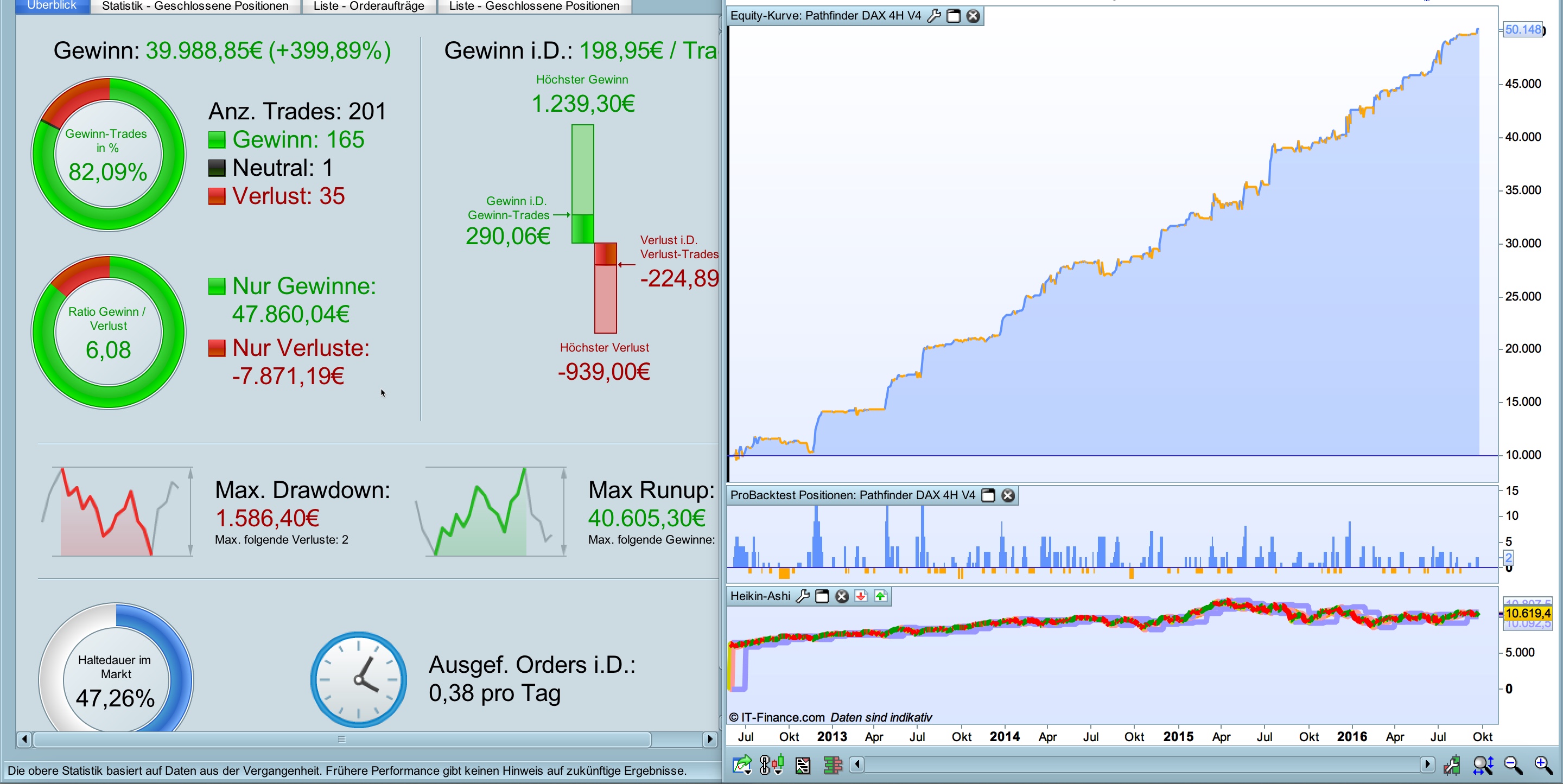

I have created a new version. Pathfinder V4 is now more applicable to other indices such as DOW or FTSE. Here are the changes:

- reorganize the code a little bit to make things clearer

- introduce maximal position size for long and short trades to avoid an excessive risk

- separation of the stop loss for long and short trades

- introduce monthly saisonal pattern management

- adjust signal and filter logic for other indices such as FTSE or DOW

- modify some trading parameter

changes in detail for the DAX:

- new: maxPositionSizeLong

- new: maxPositionSizeShort

- new: stoppLossShort

- change: periodLongMA = 300 // 250

- change: stopLossLong = 5 // 5.5

- change: takeProfitLong = 2.75 // 2

- change: maxCandlesWithProfit = 15 // 18

- rename: c1, c2, c3 in f1, f2, f3

- remove: c4 filter

- remove: monthlyLow for short trades

Here is the code for the DAX (backtest result is attached):

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 4

// Instrument: DAX mini 4H, 8-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 80000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 3

// define filter parameter

ONCE periodLongMA = 300

ONCE periodShortMA = 50

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 10

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 3.5 // in %

ONCE takeProfitLong = 2.75 // in %

ONCE takeProfitShort = 1.75 // in %

ONCE maxCandlesLongWithProfit = 15 // take long profit latest after 15 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 30 // limit long loss latest after 30 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade

ONCE January = 2

ONCE February = 2

ONCE March = 2

ONCE April = 3

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = -1

ONCE September = -2

ONCE October = 1

ONCE November = 3

ONCE December = 3

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry

IF ( l1 OR l4 OR l2 OR (l3 AND f2) ) THEN // cumulate orders for long trades

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) THEN // no cumulation for short trades

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Will take some time to look at this over the weekend but looks very impressive. I finished running some IN/OUT opp just now on V3 Jan 2009 – March 2014 and results were very similar on the forward test, infact slightly better so this gives very good confidence. 🙂

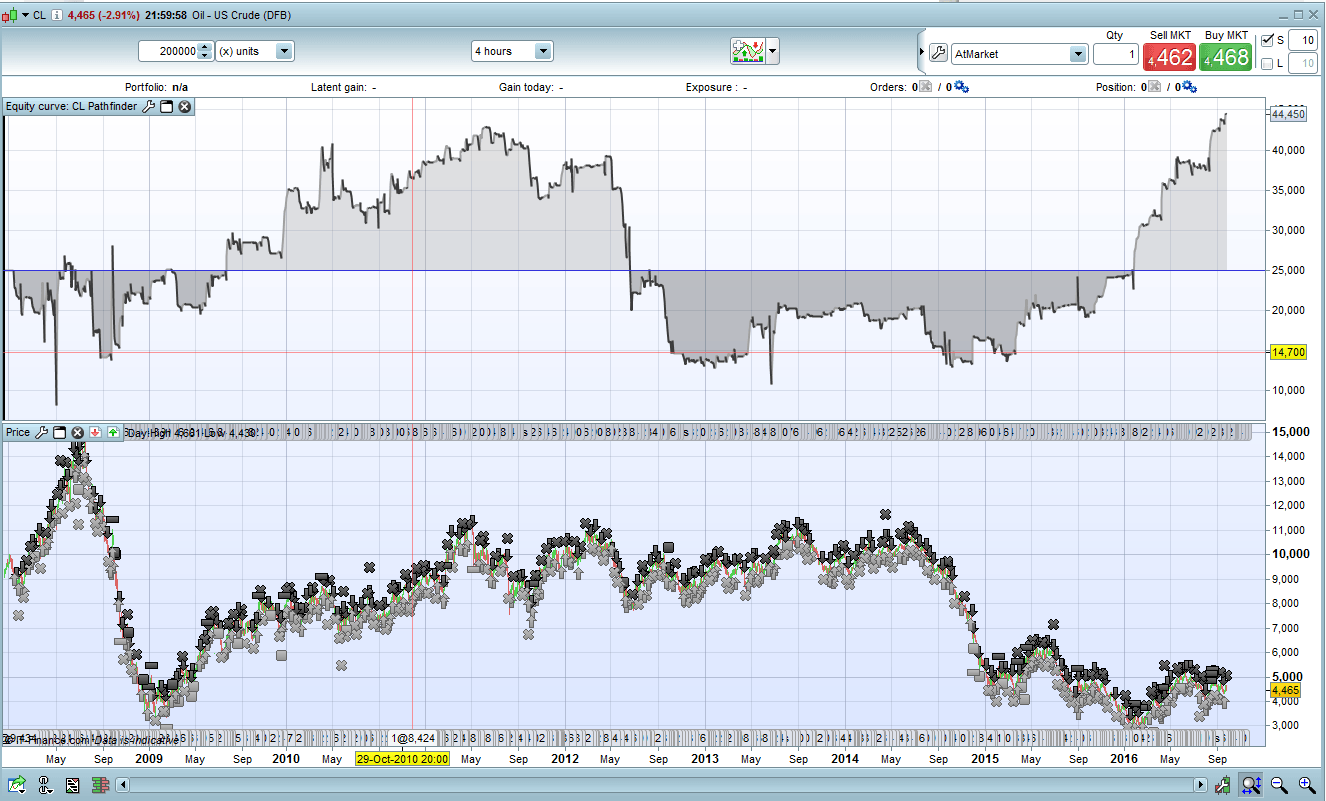

The consideration of seasonal patterns have improved my trading results significantly. Especially for commodities they are very helpful. On the webpage http://www.equityclock.com you will find excellent information about this topic. I have created a first Pathfinder version for crude oil based on the historic backtest results of saisonal patterns http://charts.equityclock.com/crude-oil-futures-cl-seasonal-chart. Unfortunately IG PRT has only a very limited data history and maybe someone with longer history is able to check the reliability of the results.

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 1

// Instrument: CL mini 4H, 7-23 CET, 3 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 70000

ONCE endTime = 230000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 4

// define filter parameter

ONCE periodLongMA = 100

ONCE periodShortMA = 10

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 15

ONCE stopLossLong = 10 // in %

ONCE stopLossShort = 5 // in %

ONCE takeProfitLong = 8 // in %

ONCE takeProfitShort = 10 // in %

ONCE maxCandlesLongWithProfit = 20 // take long profit latest after 20 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 40 // limit long loss latest after 40 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

// define saisonal position multiplier >0 - long / <0 - short / 0 no trade (www.equityclock.com)

ONCE January = 5

ONCE February = -5

ONCE March = 5

ONCE April = 5

ONCE May = 5

ONCE June = 5

ONCE July = 5

ONCE August = 5

ONCE September = 5

ONCE October = -5

ONCE November = -5

ONCE December = 3

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

weeklyLow = Lowest[BarIndex - lastWeekBarIndex](dailyLow)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER weeklyHigh

s3 = signalline CROSSES UNDER weeklyLow

s4 = signalline CROSSES UNDER dailyHigh

s5 = signalline CROSSES UNDER dailyLow

// long entry

IF ( l1 OR l4 OR l2 OR (l3 AND f2) ) THEN // cumulate orders for long trades

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) OR (s3 AND f2) OR (s4 AND f1) OR (s5 AND f1) ) THEN // no cumulation for short trades

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

End part matches yours at least… Choppy ride. I will take a look at the weekend further.

Thanks Cosmic1, long trades are good, short trades are bad, next step is to sort out the weak short conditions, I asume that weekly high/low and daily high are not realy working with oil

perfect. Also this version will look. do you think it’s OK to Wallstreet and FTSE 100? after oil might be useful for a gold system. I hope that your great work is rewarded.

Grazie.

miguel

Miguel, FTSE and DOW is almost ready for V4, I will release it soon. Gold and silver are on my agenda as well. This weekend is sunny weather here in Frankfurt and my family have requested some outdoor activities, so my time is limited on this weekend 🙂

y’re the best. I Will send you My tradizional christmas sweets of puglia. . promised. good wekend.

Miguel

I adapted Pathfinder V4 on FTSE and DOW. Due every index has it’s own “heartbeat” minor adjustments were necessary. Please be aware that this is an optimized view to historic data. Please check the position size and the related drawdown and adjust it to your own risk.

Pathfinder FTSE V4

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 4

// Instrument: FTSE mini 4H, 9-22 CET, 2 points spread, account size 10.000 Euro

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 90000

ONCE endTime = 220000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 7

// define filter parameter

ONCE periodLongMA = 200

ONCE periodShortMA = 10

// define position and money management parameter

ONCE positionSize = 1

ONCE maxPositionSizeLong = 15

ONCE maxPositionSizeShort = 10

ONCE stopLossLong = 5.25 // in %

ONCE stopLossShort = 2.5 // in %

ONCE takeProfitLong = 3 // in %

ONCE takeProfitShort = 2 // in %

ONCE maxCandlesLongWithProfit = 25 // take long profit latest after 25 candles

ONCE maxCandlesShortWithProfit = 13 // take short profit latest after 13 candles

ONCE maxCandlesLongWithoutProfit = 40 // limit long loss latest after 40 candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after 25 candles

// define saisonal position multiplier >0 - long / <0 - short

ONCE January = 3

ONCE February = 3

ONCE March = 3

ONCE April = 2

ONCE May = 2

ONCE June = 2

ONCE July = 3

ONCE August = 2

ONCE September = -3

ONCE October = 2

ONCE November = 3

ONCE December = 3

// calculate daily high/low

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// filter criteria because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// saisonal pattern

IF CurrentMonth = 1 THEN

saisonalPatternMultiplier = January

ELSIF CurrentMonth = 2 THEN

saisonalPatternMultiplier = February

ELSIF CurrentMonth = 3 THEN

saisonalPatternMultiplier = March

ELSIF CurrentMonth = 4 THEN

saisonalPatternMultiplier = April

ELSIF CurrentMonth = 5 THEN

saisonalPatternMultiplier = May

ELSIF CurrentMonth = 6 THEN

saisonalPatternMultiplier = June

ELSIF CurrentMonth = 7 THEN

saisonalPatternMultiplier = July

ELSIF CurrentMonth = 8 THEN

saisonalPatternMultiplier = August

ELSIF CurrentMonth = 9 THEN

saisonalPatternMultiplier = September

ELSIF CurrentMonth = 10 THEN

saisonalPatternMultiplier = October

ELSIF CurrentMonth = 11 THEN

saisonalPatternMultiplier = November

ELSIF CurrentMonth = 12 THEN

saisonalPatternMultiplier = December

ENDIF

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry

IF ( l1 OR l4 OR l2 OR (l3 AND f2) ) THEN // cumulate orders for long trades

IF saisonalPatternMultiplier > 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) THEN // no cumulation for short trades

IF saisonalPatternMultiplier < 0 THEN // check saisonal booster setup and max position size

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

m1 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND (BarIndex - TradeIndex) >= maxCandlesShortWithoutProfit

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF