Hi Guy’s

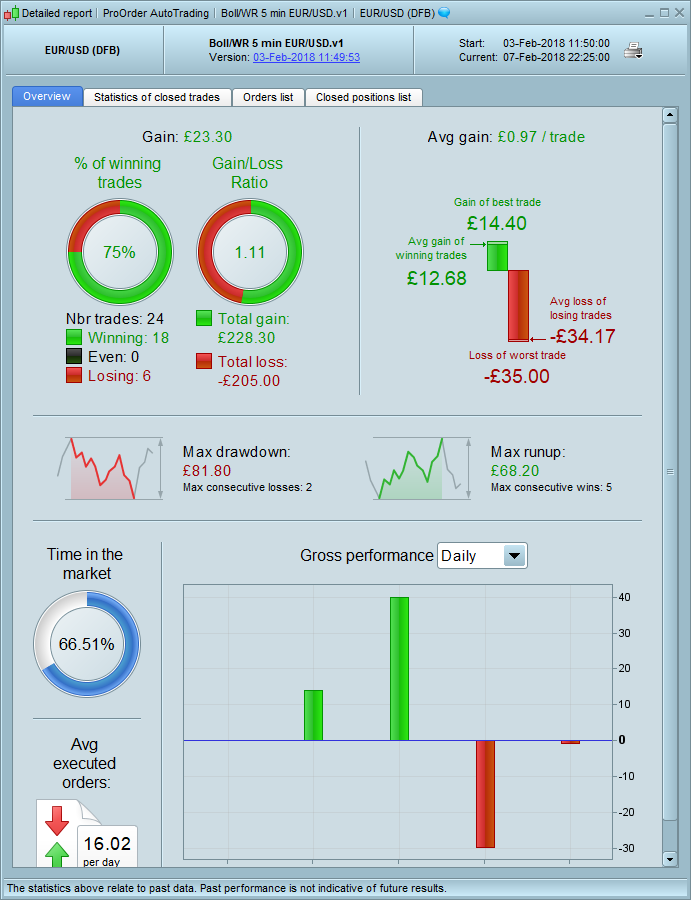

I have been running my original Version (v1) all this week live, and alothough its nothing startling, its still in profit for the week. see atached.

I would say the win ratio is acceptable but the gain/loss is not great.

I do think that keeping it simple, is the key to this strategy, and it may have lost its way a little with the various diffrent versions over the last few days.

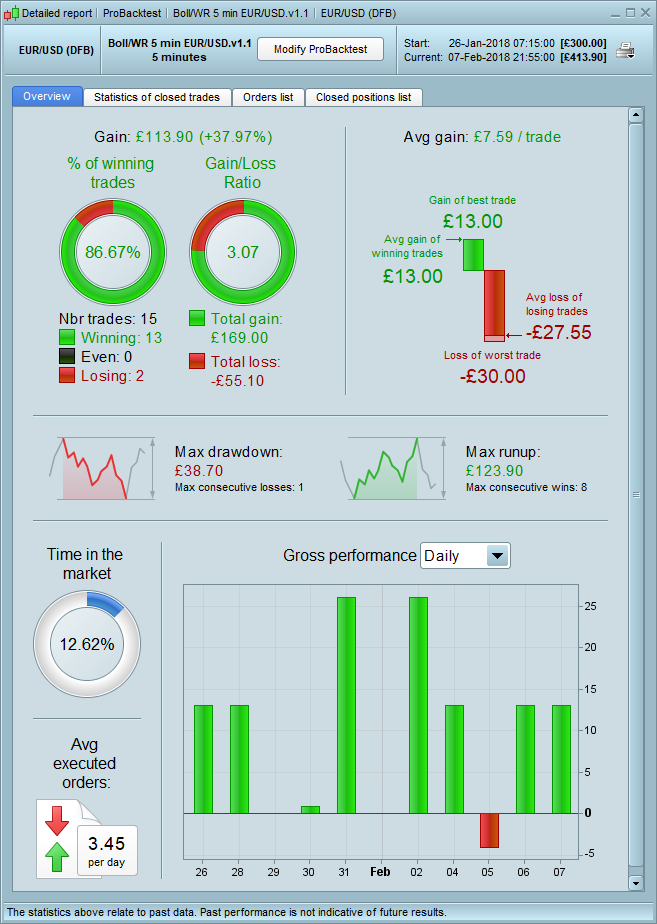

I have reviewed V1 again and added a directional movement indicator to it to remove alot of the big losses caused by sharp movements up or down in the price, it

has improved the stats considerably

I have it running live as of tonight so will keep you posted on how it goes.

Bravo Jusmih1!

I enjoyed your post with a novelty on your Strat to integrate the ADX.

This improves the results.

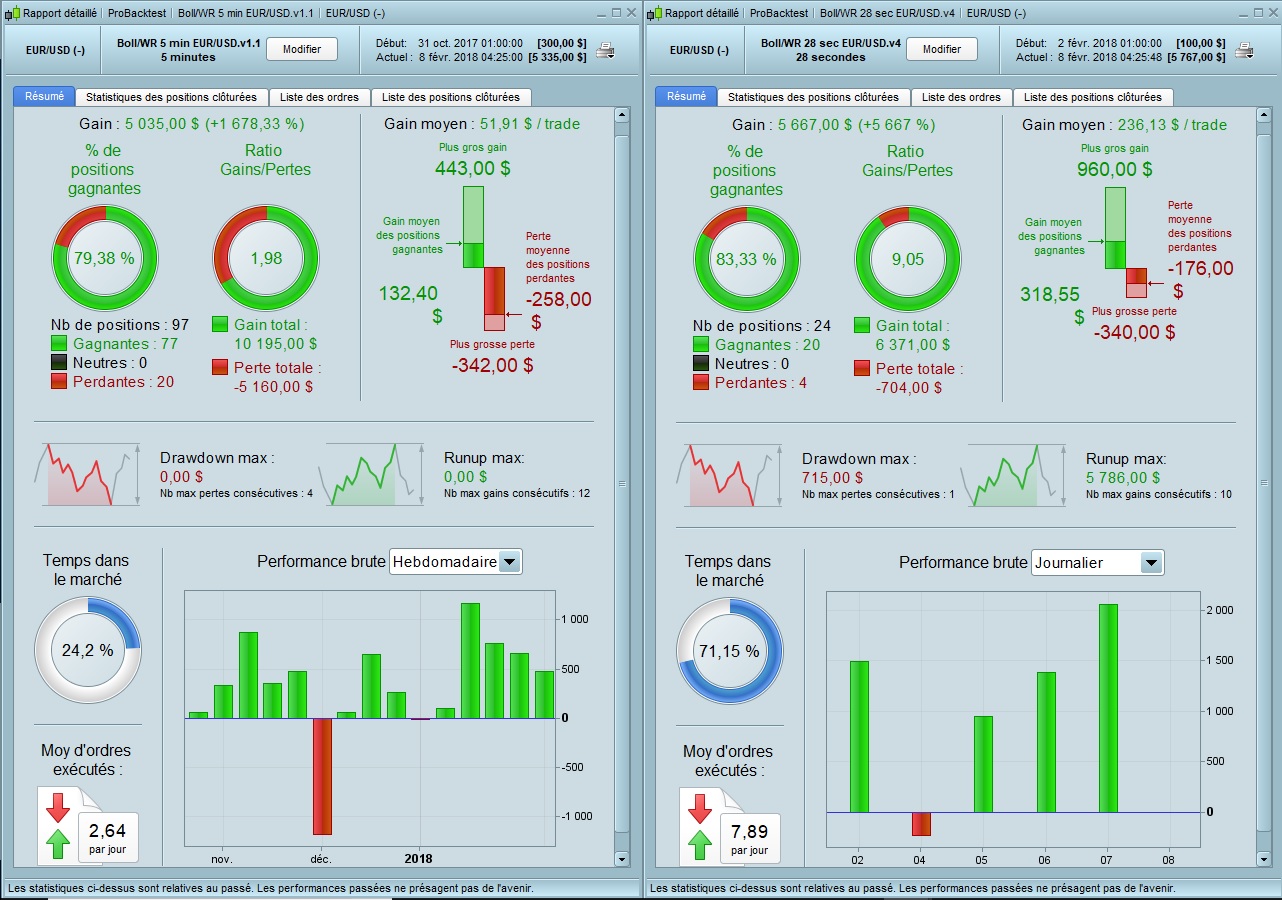

So I had the idea to integrate the ADX in V2.2, which worked well, but had problems of Drawdown important. So I studied a new version, the V4, which integrates the ADX in V2.2. The results are excellent, the curve of equity better, the Gain too, the Drawdown too, the Ratio Gain / Loss too, with a much smaller number of trades.

Below the comparison charts V1.1 / V4, V2.2 / V4, Backtest V4

and the new V4 version.

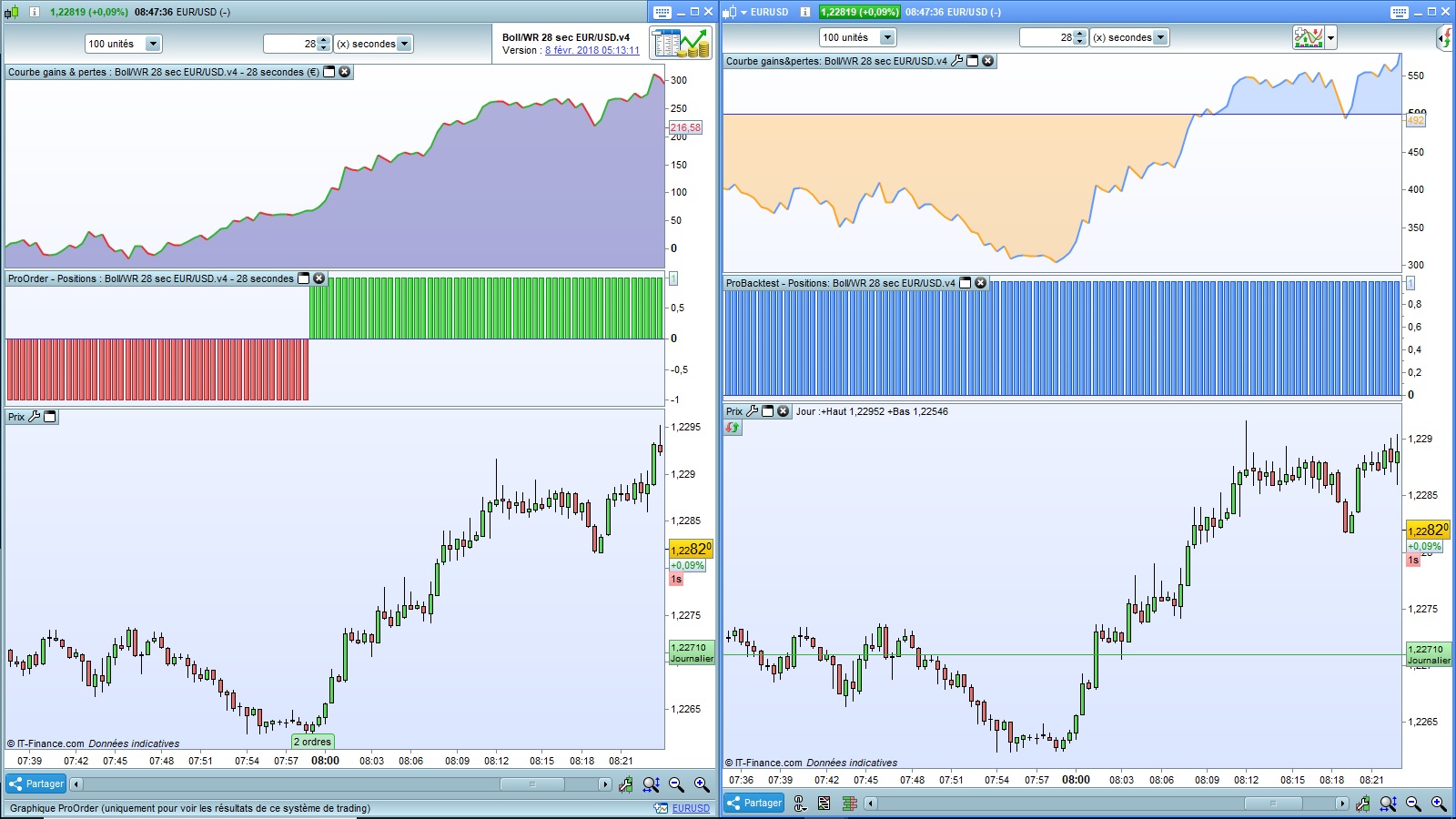

I put into service this morning the v4. I noticed a malfunction between the Backtest and the Live ProOrder.

Between 7:00 and 8:00, the Backtest was positioned at 1 while the ProOrder live was at -1.

It is disconcerting !!! Who to believe? Backtest or Live ProOrder.

It was favorable to me on the ProOrder gain, but what can we think of live ProOrder, if we put real money?

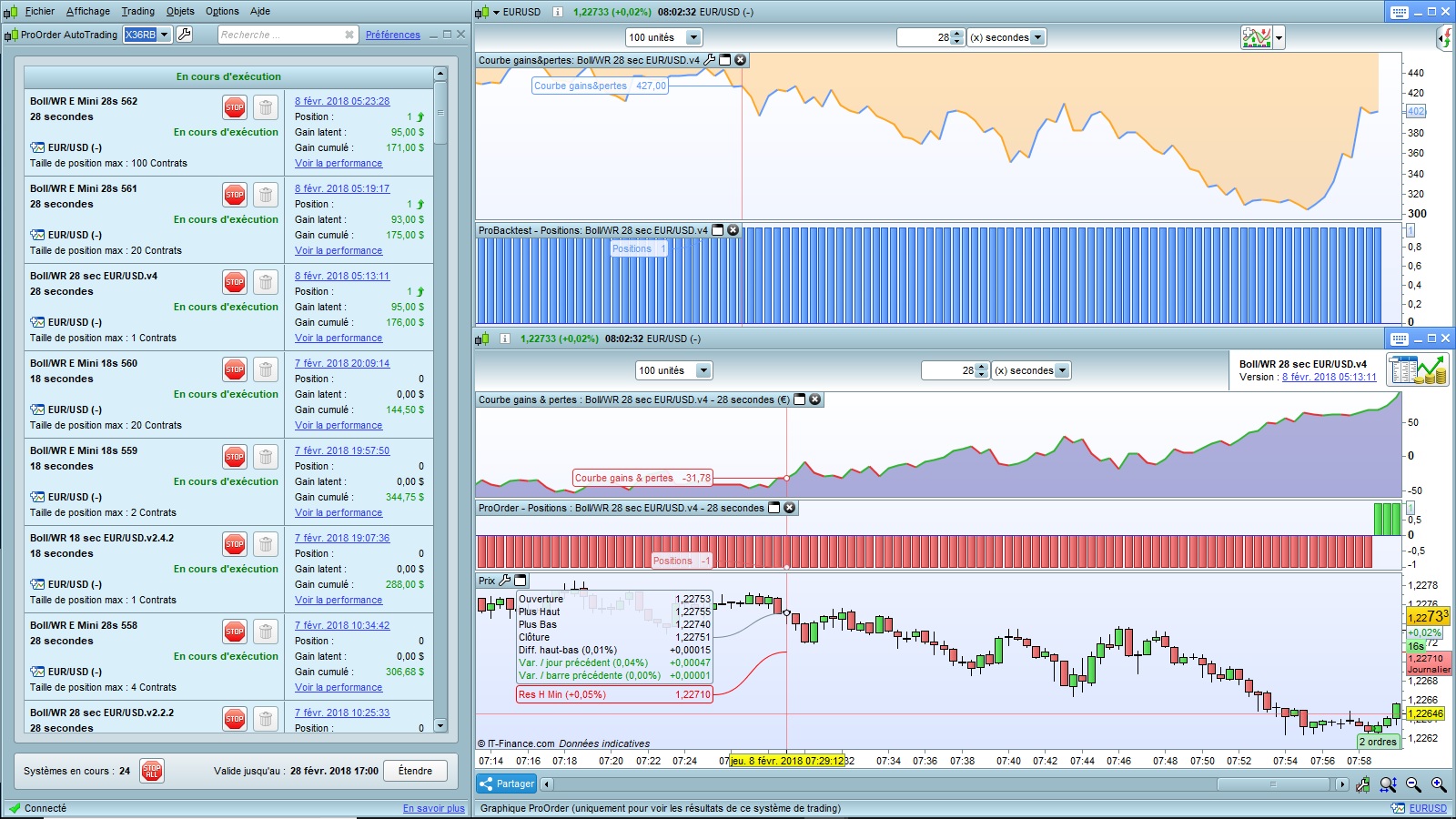

Below is the Backtest / Live ProOrder Comparison Chart.

I just made a more explicit comparison.

On the left, the ProOrder Live. Right, the Backtest.

below the comparison of the graphs.

I did an exercise yesterday on a 28 Sec version … I ran backtest and noted the time where a particular short was entered. Then I changed the spread – by 1 point – and noted a new / different time (within several minutes to previous time) where a particular short was entered!

Then I changed the spread – by 2 points – and a Long trade (no short trade at all!) was entered within 10 mins or so of times above! I should have made screen shots sorry.

As we know the spread on the EUR/USD flash widens from 0.6 to 2.5 or so in milliseconds then collapses back to 0.6 again. So as my investigations show, it’s not surprising we get variations between a fixed spread backtest and a variable spread Live trade??

Try it yourself and report back please??

Cheers

GraHal

@ Grahal,

I actually noticed a shift only on the time of the exits when one modifies the spread (0.6,1,2, etc …)

You can try to play with ‘defparam preloadbars=0’. In this particular kind of timeframe (construct from 1 second), if the history does not start at the exact same time, some discrepancies may exist.. Not sure it could fix the differences, but I think you should try! 🙂

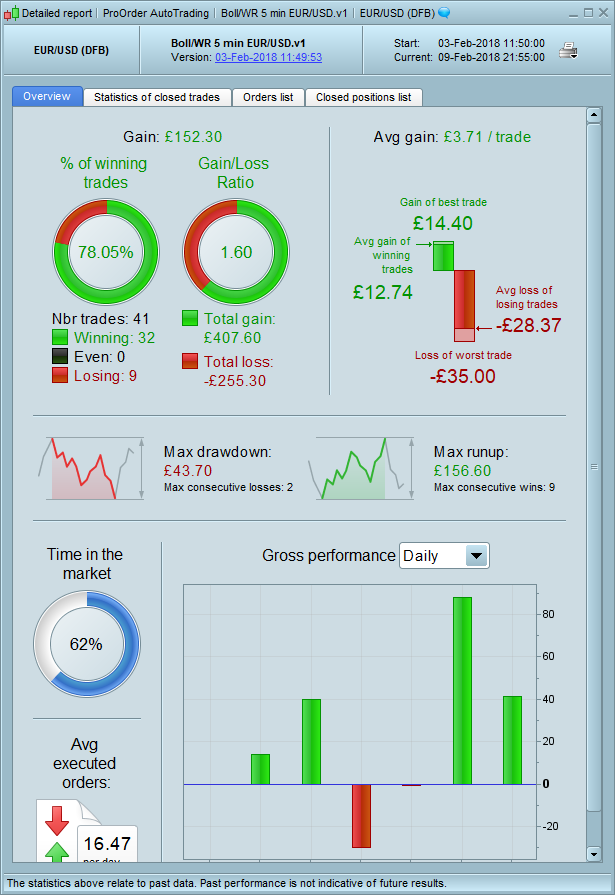

Up to now I am well impressed with Jusmih1 v1.1 (5 min TF) … it is one of the few Strats in my experience that makes an entry at a logical point and is in profit within seconds!

Still early days as not many trades yet, but it’s making money. Although if price rise slows / stalls just under the 13 points TP (which it often seems to) I’ve been exiting manually. I’ll check out what effect a TP of 11 or 12 has on results.

@ grahal,

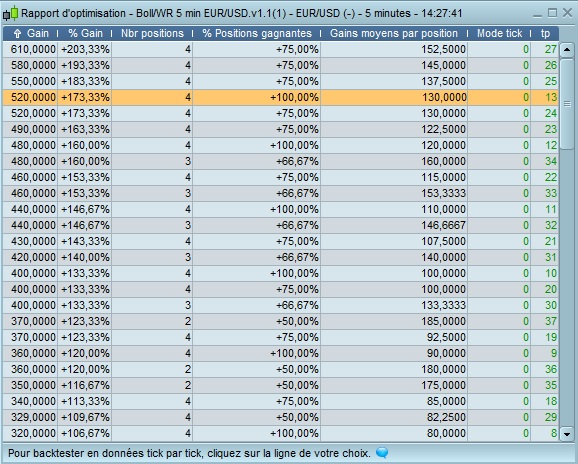

This version V1.1 is very attractive, its results surprising, the code is very simple, and for me an excellent source of inspiration.

below the optimization report of the take profit variable for V1.1

Hi All,

I have been running the original V1 since Sunday night and wanted to give you an update of the Live performance over the week. Got to say i am quite impressed!

i have also ran v1.1 for a couple of days which i will post separately.

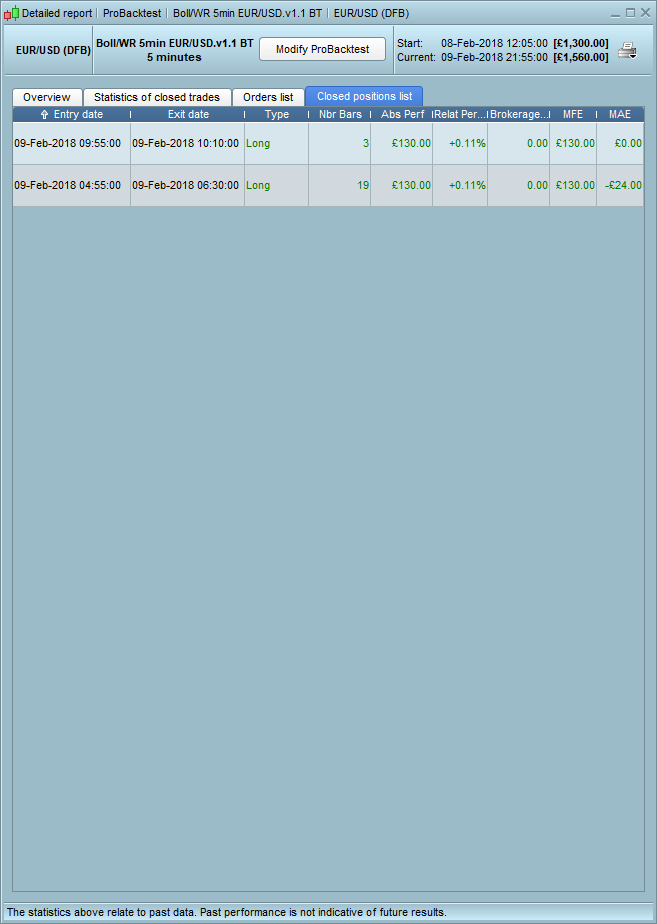

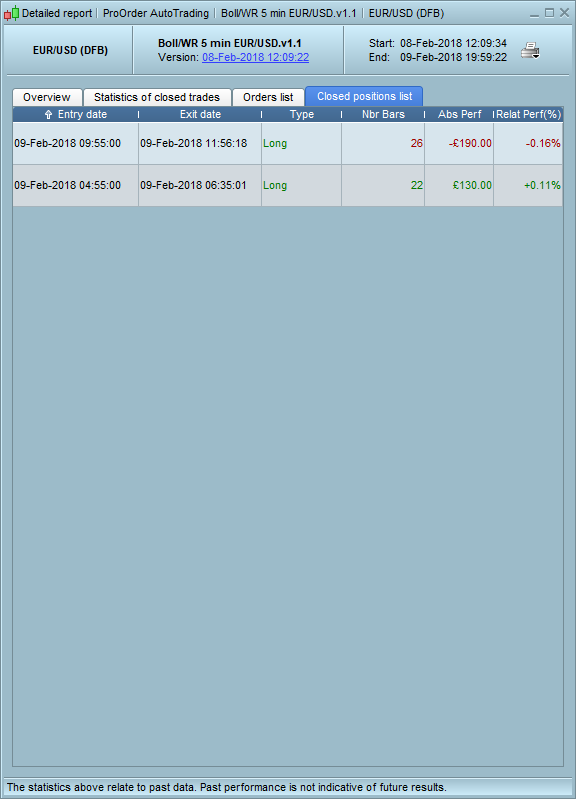

Hi Again, Only tested v.1.1 from the 8th till close on the 9th so not much to report however i did have a loss on the live results, but when tested on the Backtest it didnt show as a loss?

The Entery points were both the same on Live and backtest but the exit times were completly diffrent resulting in a painful loss.

Any thoughts why this would be?

Just noticed that the spread had changed from 0.6 to 1.5 which has resulted in the loss but surely mid morning the spread should be consistant at 0.6?

AVT

AVTParticipant

Senior

I had a look into the code of BollWR-28-sec-EURUSD.v4.itf

Would someone please explain to me how these 4 conditions can work? We have 1st LongEntry and 1st LongExit – so far so good – but right afterwards 2nd LongEntry and 2nd LongExit (same for Short side). So in case of a long Entry either the 1st or the 2nd LongEntry condition could be discovered to become true and we would buy, same for exit: if one of the two LongExit are met, we would be out. But why do we not code IF 1st LongEntry OR 2nd LongEntry THEN buy (this would be at least how I guess what happens at execution)?

Thanks for clarification.

Hi AVT,

It is true that I could have used an OR between 1st LongEntry and 2nd LongEntry, same for the outputs, but I did not want to break the structure of the Strat which seemed to me simple to understand and write. In any case, with an OU, we would have obtained the same result, it is TRUE.

I’m waiting a few days next week to give you an orientation on what strategies are profitable on ProOrder.

I started a last one that has 3 inputs and 3 outputs on the same structure as the V4 (it is the V4.5), it behaves like a scalper, this 3rd entry and 3rd exit gives us precision. I have also integrated in this version of the code that allows when the profit limit is reached to suspend future trades. It is based on an observation that we do not be all day to launch trades, if we want to be profitable and reduce Drawdowns. I tested it last night on ProOrder, it’s promising.

Thank you for your feedback.

AVTParticipant

Senior

Ok, I thought I missed something important in understanding. I was just a bit shocked to find such a lot of conditions in a single strategy marked 28 sec 😳