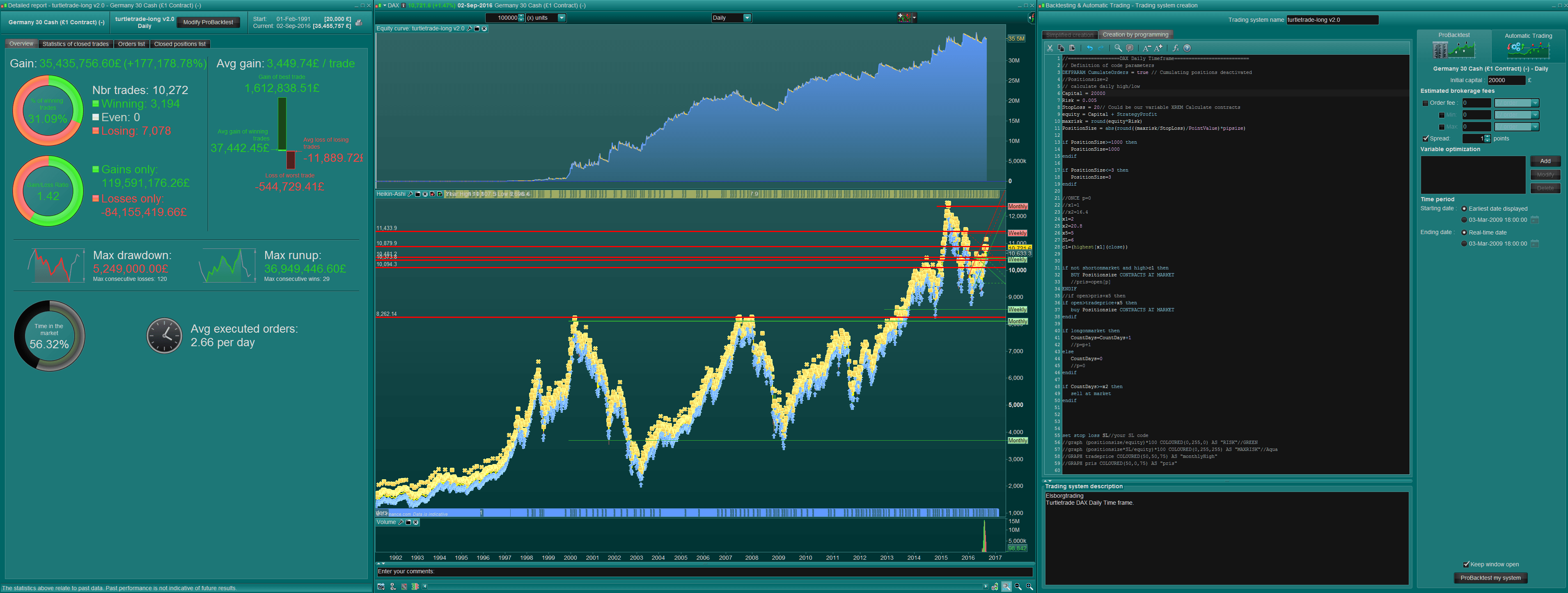

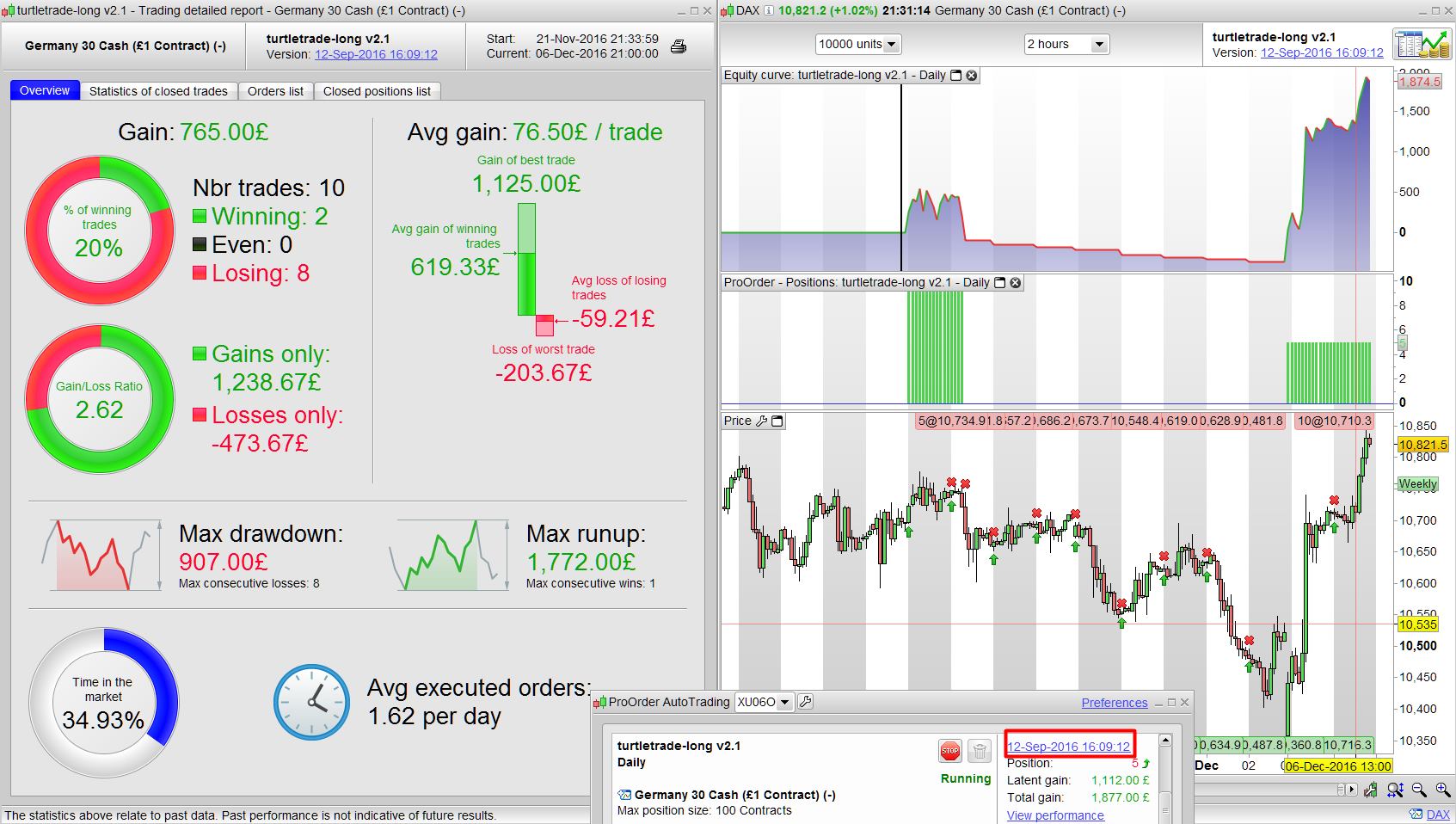

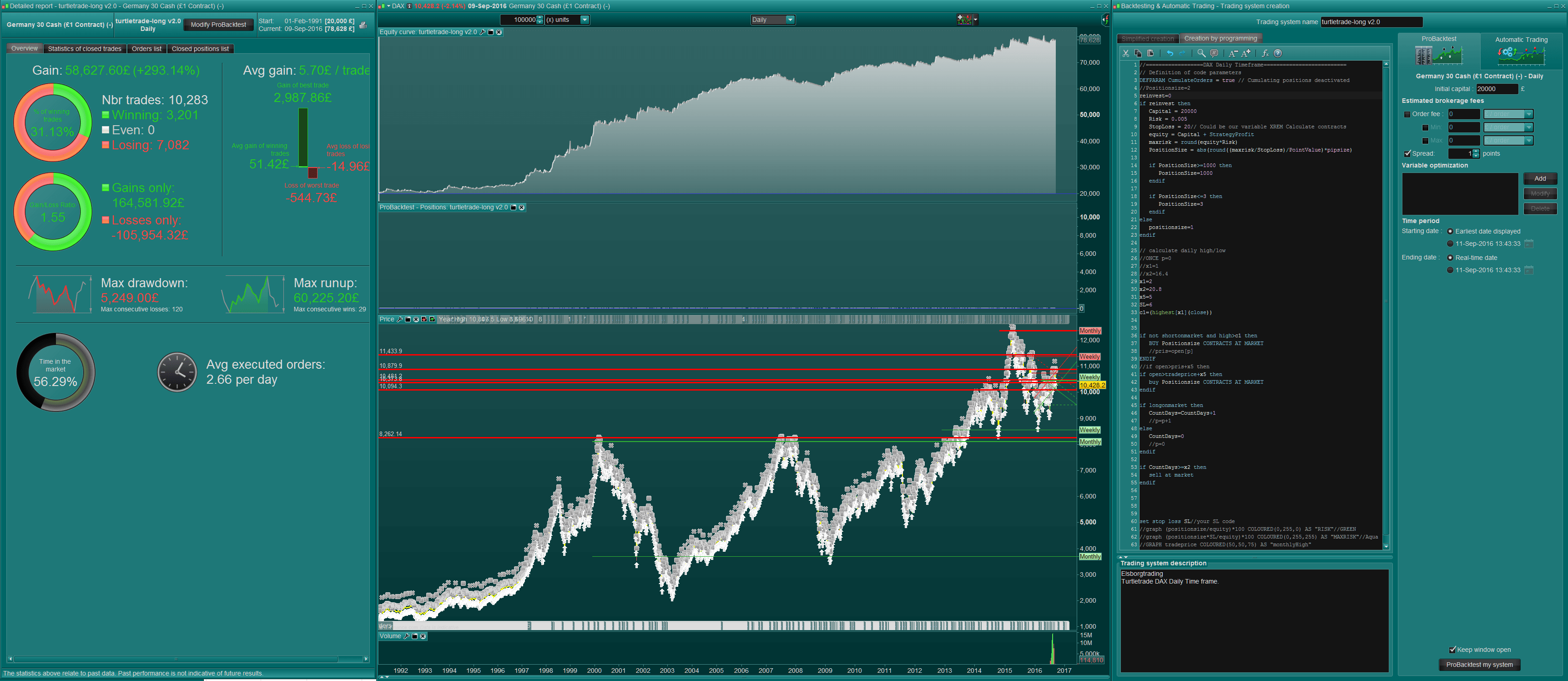

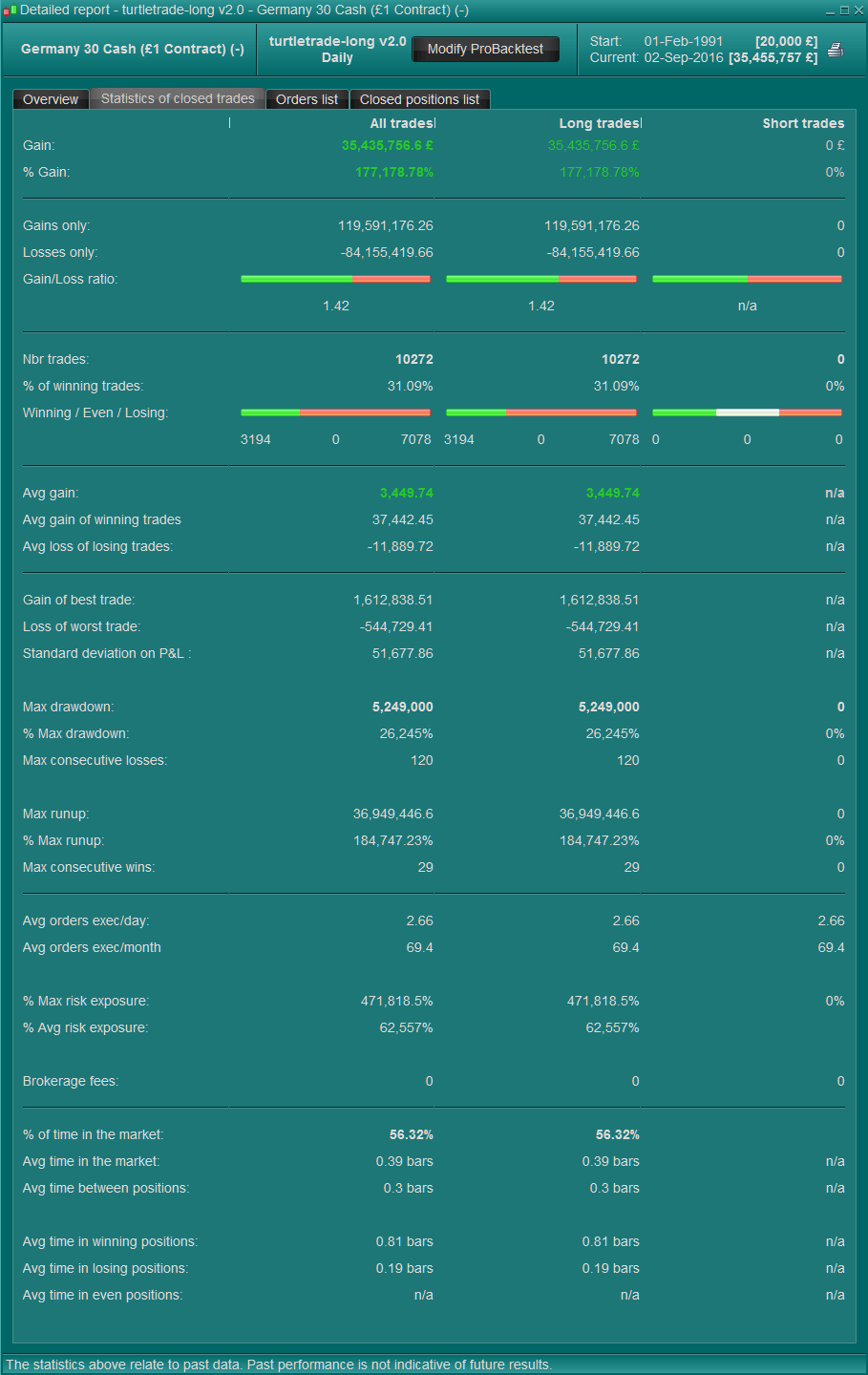

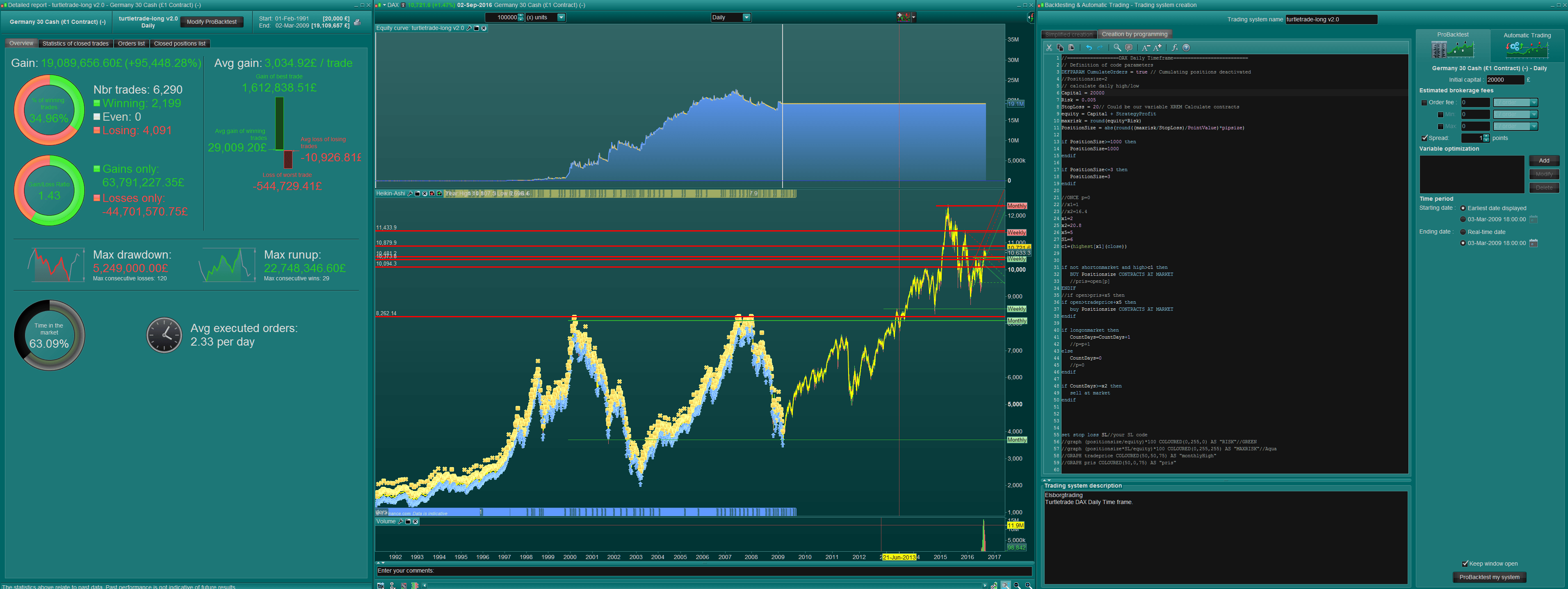

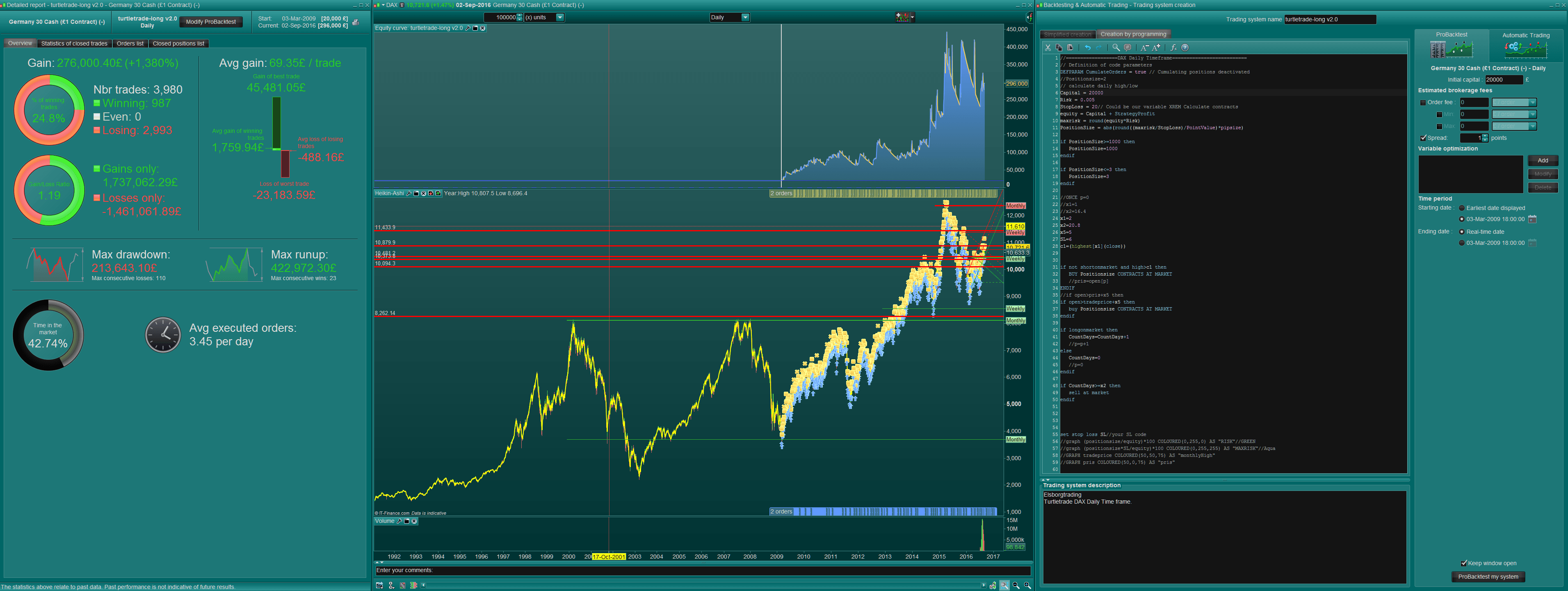

TurtleTrade DAX Daily timeframe

{kind=link}

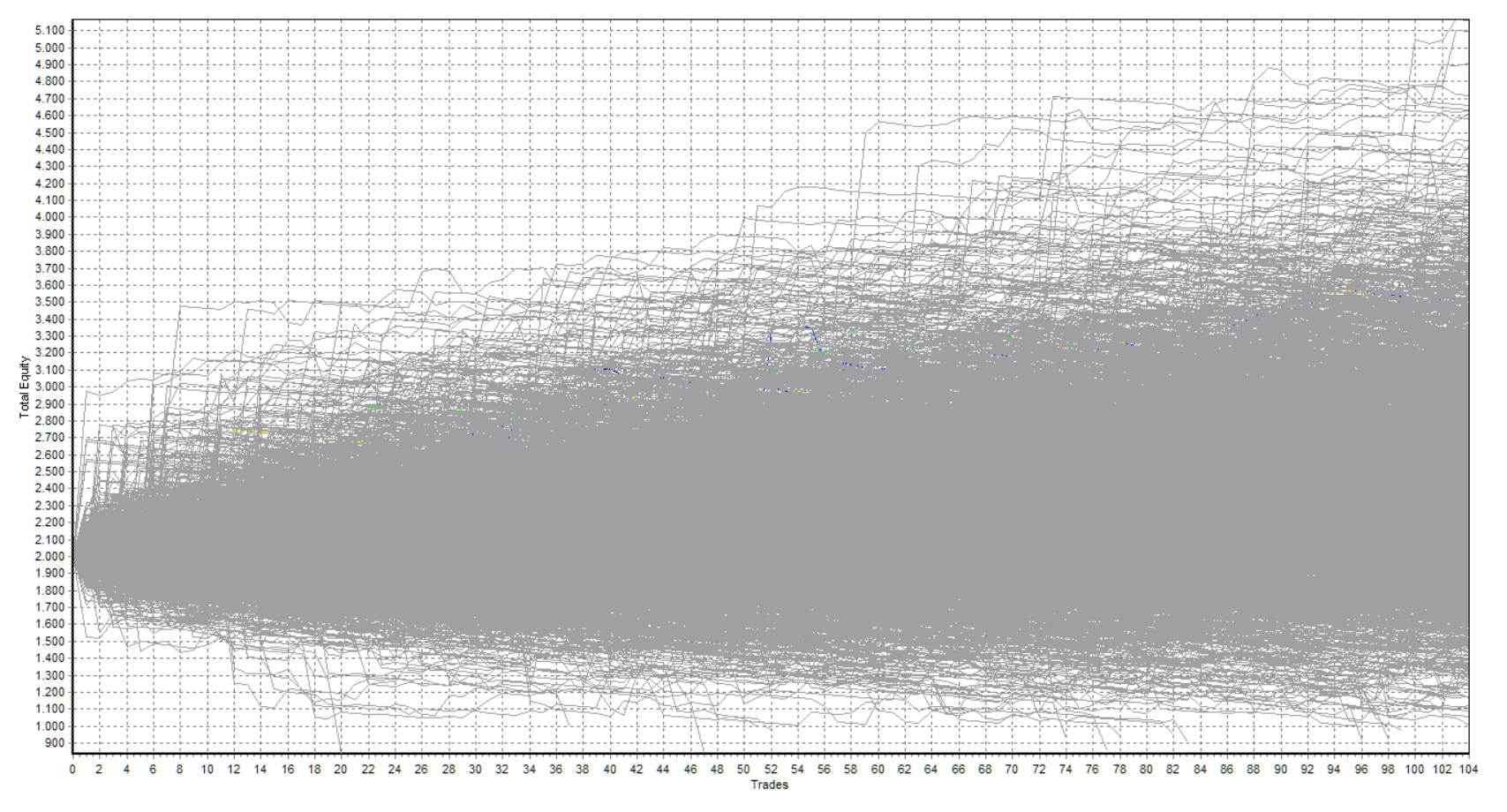

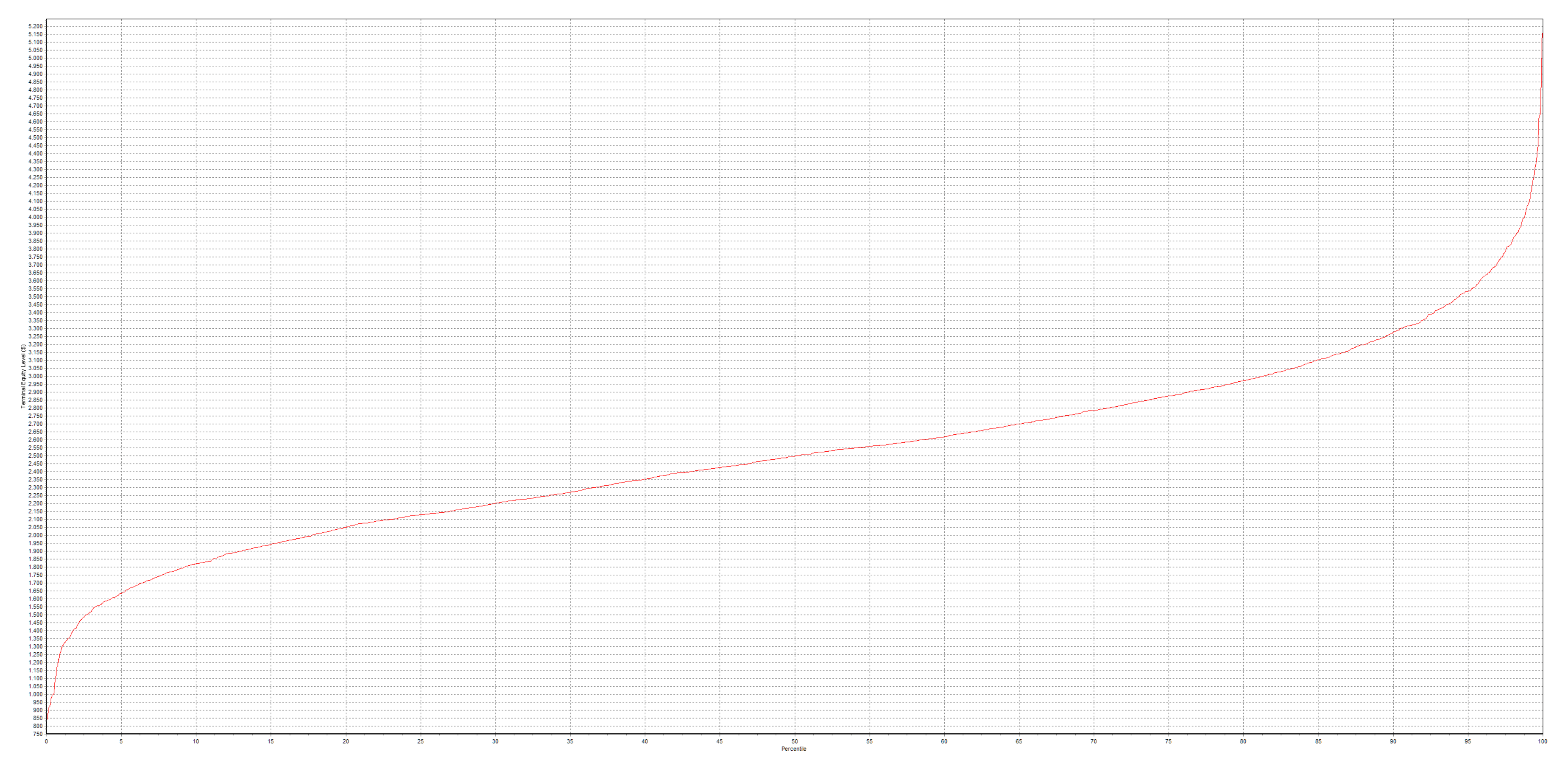

Here is a turtletrader code I have been playing around with. It not perfect as there are huge drawbacks, but it has even larger profits. It also need a decent amount of capital to begin with- a lot of patience and stomach ice.

There are many 0-bar trades but only on the stoploss. Profit bars is 5 so I think the trades are valid and not subjected to the zerobar trade issue so many have written about here.

It makes a trade on 2nd day breakout and adds a trade every day with a minimum SL- many get stopped out but some get going.

I also added some extra trades if there was a trend. I hope you like it. I didn’t clean up the code, so you would see some of the alternative things I have been optimizing.

Comments and improvement are as always welcome.

//==================DAX Daily Timeframe==========================

// Definition of code parameters

DEFPARAM CumulateOrders = true // Cumulating positions deactivated

//Positionsize=2

// calculate daily high/low

Capital = 20000

Risk = 0.005

StopLoss = 20// Could be our variable XREM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

if PositionSize>=1000 then

PositionSize=1000

endif

if PositionSize<=3 then

PositionSize=3

endif

//ONCE p=0

//x1=1

//x2=16.4

x1=2

x2=20.8

x5=5

SL=6

c1=(highest[x1](close))

if not shortonmarket and high>c1 then

BUY Positionsize CONTRACTS AT MARKET

//pris=open[p]

ENDIF

//if open>pris+x5 then

if open>tradeprice+x5 then

buy Positionsize CONTRACTS AT MARKET

endif

if longonmarket then

CountDays=CountDays+1

//p=p+1

else

CountDays=0

//p=0

endif

if CountDays>=x2 then

sell at market

endif

set stop loss SL//your SL code

//graph (positionsize/equity)*100 COLOURED(0,255,0) AS "RISK"//GREEN

//graph (positionsize*SL/equity)*100 COLOURED(0,255,255) AS "MAXRISK"//Aqua

//GRAPH tradeprice COLOURED(50,50,75) AS "monthlyHigh"

//GRAPH pris COLOURED(50,0,75) AS "pris"

Cheers Kasper

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}