DOW Breakout 15Min

{kind=link}

Firstly, a big thank you to Nicolas for this great site and for originally introducing us to the CAC Breakout using the same code here.

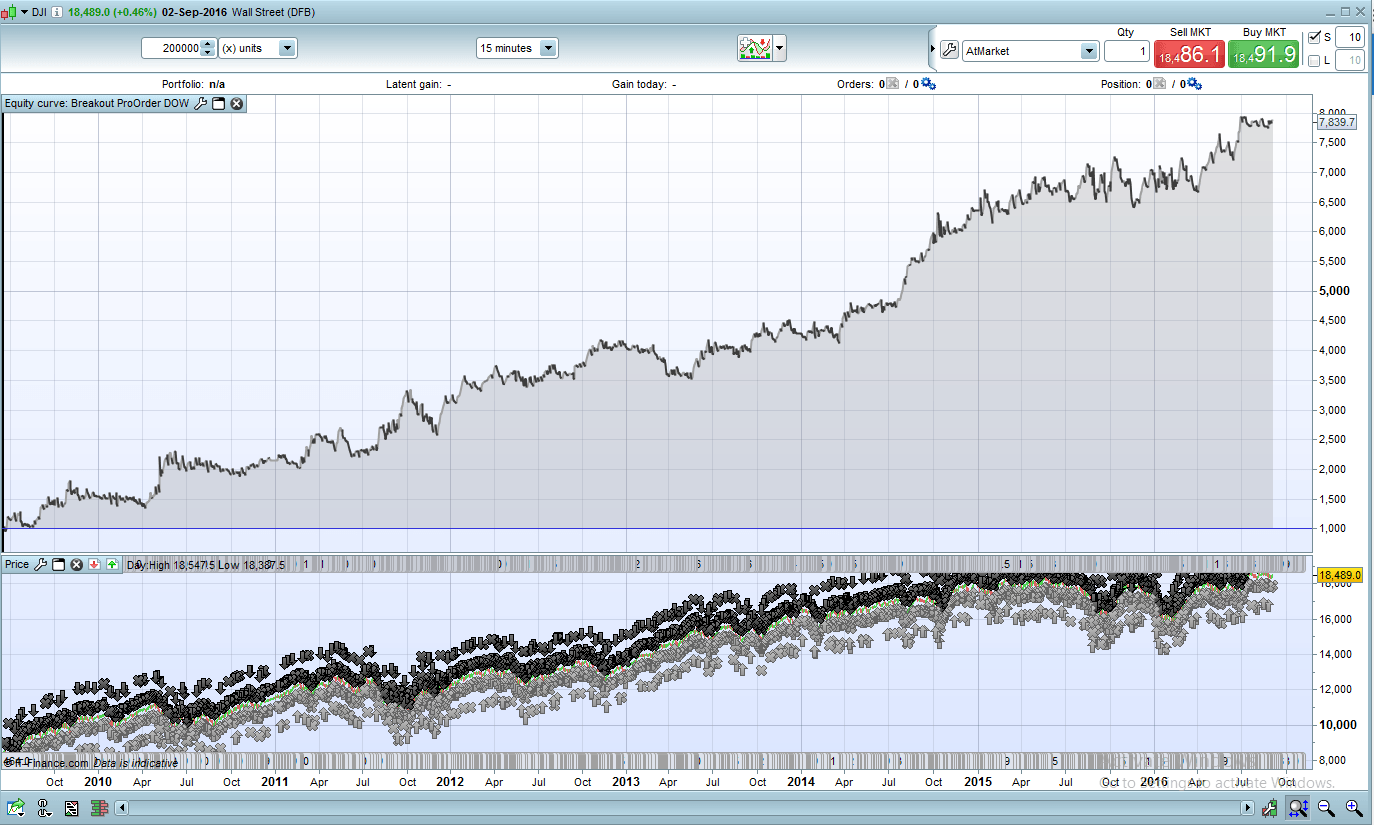

I set about testing this strategy on other markets due to the fact you can backtest 8 years of data with 200,000 units on the 15Min time-frame. The other massive plus is no fake profits and only 9, 0 bars in 1700 trades! 🙂

The DOW is slightly different to the CAC and DAX breakout. It did not like the first 30 min range but prefers the first hour range BUT we exclude the first 15min candle as you can see from the modifications to the code.

In this version I am using a fixed position size but you can activate the re-invest system if you are happy with that. It makes for an interesting ride!

I stuck to the rules of not over optimising/curve fitting by using an IN/OUT sample as documented here. This ran from Jun 2009 – May 2014.

The results above are £1 Per Point, £1000 Start and 1.8 Spread.

I am live trading this with real money with minimum stakes to test.

All times in the code are UK so please adjust to your timezone.

I have some more of these ported to other markets but need to spend a little more time getting them right before posting in the library. Expect them soon.

I have not had enough time to test different time frames. Maybe I will try that next if time allows.

Good luck and enjoy your trading.

// We do not store datas until the system starts.

// If it is the first day that the system is launched and if it is afternoon,

// it will be waiting until the next day for defining sell and buy orders

//UK TIME ZONE

DEFPARAM PreLoadBars = 0

// Position is closed at 20:30

DEFPARAM FlatAfter = 203000

// No new position will be initiated after the 19:45 candlestick.

LimitHour = 200000

// Market scan begin with the 15 minute candlestick that closed at 15:30

StartHour = 151500

// The 24th and 31th days of December will not be traded because market close before 7h45 PM

IF (Month = 5 AND Day = 1) OR (Month = 12 AND (Day = 24 OR Day = 25 OR Day = 26 OR Day = 30 OR Day = 31)) THEN

TradingDay = 0

ELSE

TradingDay = 1

ENDIF

// Variables that would be adapted to your preferences

if time = 144500 then

//PositionSize = max(1,1+ROUND((strategyprofit-1000)/1000)) //gain re-invest trade volume

PositionSize = 1 //constant trade volume over the time

endif

MaxAmplitude = 160

MinAmplitude = 20

OrderDistance = 4

PourcentageMin = 35

// Variable initilization once at system start

ONCE StartTradingDay = -1

// Variables that can change in intraday are initiliazed

// at first bar on each new day

IF (Time <= StartHour AND StartTradingDay <> 0) OR IntradayBarIndex = 0 THEN

BuyTreshold = 0

SellTreshold = 0

BuyPosition = 0

SellPosition = 0

StartTradingDay = 0

ELSIF Time >= StartHour AND StartTradingDay = 0 AND TradingDay = 1 THEN

// We store the first trading day bar index

DayStartIndex = IntradayBarIndex

StartTradingDay = 1

ELSIF StartTradingDay = 1 AND Time <= LimitHour THEN

// For each trading day, we define each 15 minutes

// the higher and lower price value of the instrument since StartHour

// until the buy and sell tresholds are not defined

IF BuyTreshold = 0 OR SellTreshold = 0 THEN

HighLevel = Highest[IntradayBarIndex - DayStartIndex + 2](High)

LowLevel = Lowest [IntradayBarIndex - DayStartIndex + 2](Low)

// Spread calculation between the higher and the

// lower value of the instrument since StartHour

DaySpread = HighLevel - LowLevel

// Minimal spread calculation allowed to consider a significant price breakout

// of the higher and lower value

MinSpread = DaySpread * PourcentageMin / 100

// Buy and sell tresholds for the actual if conditions are met

IF DaySpread <= MaxAmplitude THEN

IF SellTreshold = 0 AND (Close - LowLevel) >= MinSpread THEN

SellTreshold = LowLevel + OrderDistance

ENDIF

IF BuyTreshold = 0 AND (HighLevel - Close) >= MinSpread THEN

BuyTreshold = HighLevel - OrderDistance

ENDIF

ENDIF

ENDIF

// Creation of the buy and sell orders for the day

// if the conditions are met

IF SellTreshold > 0 AND BuyTreshold > 0 AND (BuyTreshold - SellTreshold) >= MinAmplitude THEN

IF BuyPosition = 0 THEN

IF LongOnMarket THEN

BuyPosition = 1

ELSE

BUY PositionSize CONTRACT AT BuyTreshold STOP

ENDIF

ENDIF

IF SellPosition = 0 THEN

IF ShortOnMarket THEN

SellPosition = 1

ELSE

SELLSHORT PositionSize CONTRACT AT SellTreshold STOP

ENDIF

ENDIF

ENDIF

ENDIF

// Conditions definitions to exit market when a buy or sell order is already launched

IF LongOnMarket AND ((Time <= LimitHour AND SellPosition = 1) OR Time > LimitHour) THEN

SELL AT SellTreshold STOP

ELSIF ShortOnMarket AND ((Time <= LimitHour AND BuyPosition = 1) OR Time > LimitHour) THEN

EXITSHORT AT BuyTreshold STOP

ENDIF

// Maximal risk definition of loss per position

// in case of bad evolution of the instrument price

SET STOP PLOSS MaxAmplitude

//SET TAGRGET PPROFIT //70 //160{kind=link}

{kind=link}

{kind=link}