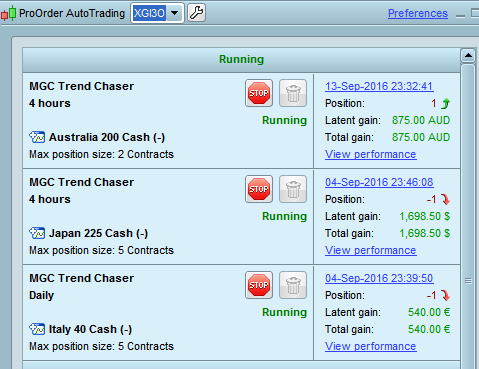

Trend Chaser 3.0 with Money Management

{kind=link}

Traders,

I have been working on the Trend Chaser concept for some time but always had a problem with false signals, large draw-downs, and sub-optimal stops. It had value in that it averages 50% wins on most instruments with most time-frames, so I felt it was worth persevering.

I am indebted to cfta’s idea for grid-step trading and Nicolas’ assistance and development of the code for a brilliant money-management system, as well a number of traders (and my close friend Free2Trade) for their encouragement and ideas. I have been able to find a solution to these problems through the incorporate the money management code with the Trend Chaser code.

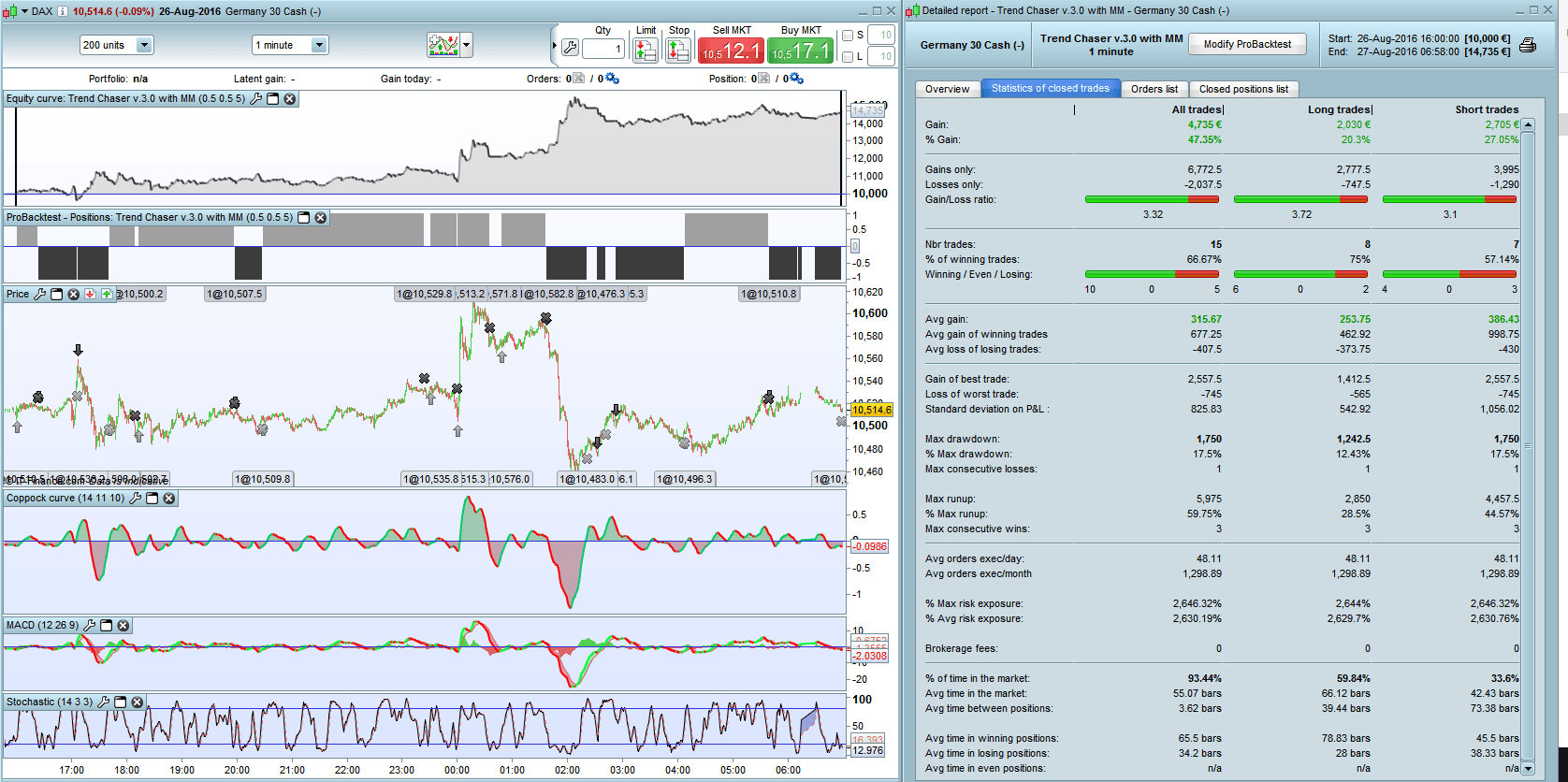

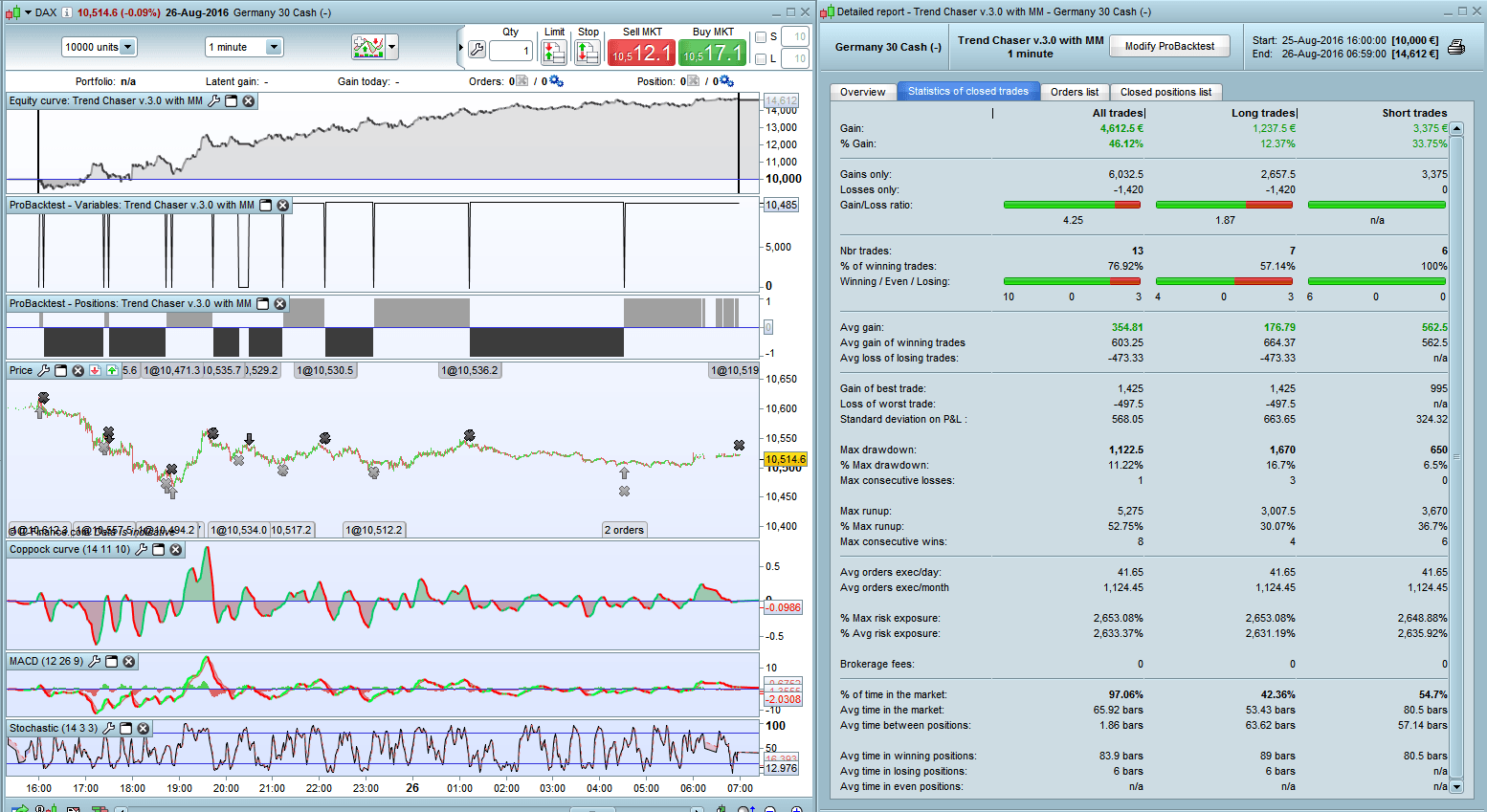

It is early days in the testing but so far the results have been spectacular. I have attached a spreadsheet of the test results I have run on major indices, with the optimisation of some of the money management parameters: standard deviation (line 73), risk/reward (line 11) and risk percent (line 9). Please note that the formula in the spreadsheet are:

- ME (mathematical expectancy) = % of winning trades x average gain of winning trades / average loss of losing trades – (1 – % of winning trades).

- IRR (internal rate of return or compounded return per annum) = 360 x (((end $ / start $) ^ (1 / (end date – start date)) – 1)).

- This is a way to compare trading systems with different time frames, starting accounts, outcomes, etc.

- I have rejected ME’s < 0.5, and % wins < 50%.

- The max. DD (max. draw down) is expressed in $’s but the percentage is the dollar amount divided by 100.

- I have noticed that the max draw-down figures given by PRT don’t seem to bear any relationship to the reality of the charts. Does anyone know how this is calculated?

I find that the sweet spot for the code is in the shorter time frames such as 5 and 1 minute charts. The last two tests of the DAX were spectacular as I ran them over only the opening hours for that market. The negatives were the draw-downs of 11% and 17% – worth the risk, Elsborgtrading????

I have attached the code for examination and critique, please. All comments and suggestions for improvement are most welcome.

/// Definition of code parameters

defparam preloadbars = 3000

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

COI= WEIGHTEDAVERAGE[14](ROC[11] +ROC[10])

MAC= MACDline[12,26,9]

STO = Stochastic[14,5]

once RRreached = 0

accountbalance = 10000 //account balance in money at strategy start

riskpercent = rp //whole account risk in percent%

amount = 1 //lot amount to open each trade

rr = rr //risk reward ratio (set to 0 disable this function)

//dynamic step grid

minSTEP = 5 //minimal step of the grid

maxSTEP = 20 //maximal step of the grid

ATRcurrentPeriod = 5 //recent volatility 'instant' period

ATRhistoPeriod = 100 //historical volatility period

ATR = averagetruerange[ATRcurrentPeriod]

histoATR= highest[ATRhistoPeriod](ATR)

resultMAX = MAX(minSTEP*pipsize,histoATR - ATR)

resultMIN = MIN(resultMAX,maxSTEP*pipsize)

gridstep = (resultMIN)

// Conditions to enter long positions

c1 = (COI > COI[1])

c2 = (MAC > MAC[1])

c3 = (STO > 20)

c4 = (STO < 40)

c5 = (STO > STO[1])

// Conditions to enter short positions

c11 = (COI< COI[1])

c12 = (MAC< MAC[1])

c13 = (STO < 80)

c14 = (STO > 60)

c15 = (STO < STO[1])

//first trade whatever condition

if NOT ONMARKET AND HIGHEST[5](c1)=1 AND HIGHEST[5](c2)=1 AND HIGHEST[5](c3)=1 AND HIGHEST[5](c4)=1 AND HIGHEST[5](c5)=1 then //close>close[1]

BUY amount LOT AT MARKET

endif

if NOT ONMARKET AND HIGHEST[5](c11)=1 AND HIGHEST[5](c12)=1 AND HIGHEST[5](c13)=1 AND HIGHEST[5](c14)=1 AND HIGHEST[5](c15)=1 then //close<close[1]

SELLSHORT amount LOT AT MARKET

endif

// case BUY - add orders on the same trend

if longonmarket and close-tradeprice(1)>=gridstep*pipsize then

BUY amount LOT AT MARKET

endif

// case SELL - add orders on the same trend

if shortonmarket and tradeprice(1)-close>=gridstep*pipsize then

SELLSHORT amount LOT AT MARKET

endif

//money management

liveaccountbalance = accountbalance+strategyprofit

moneyrisk = (liveaccountbalance*(riskpercent/100))

if onmarket then

onepointvaluebasket = pointvalue*countofposition

mindistancetoclose =(moneyrisk/onepointvaluebasket)*pipsize

endif

//floating profit

floatingprofit = (((close-positionprice)*pointvalue)*countofposition)/pipsize

//actual trade gains

MAfloatingprofit = average[20](floatingprofit)

BBfloatingprofit = MAfloatingprofit - std[20](MAfloatingprofit)*sd

//floating profit risk reward check

if rr>0 and floatingprofit>moneyrisk*rr then

RRreached=1

endif

//GRAPH floatingprofit as "float"

//GRAPH RRreached as "rr"

//GRAPH floatingprofit as "floating profit"

//GRAPH BBfloatingprofit as "BB Floating Profit"

//GRAPH positionprice-mindistancetoclose

//GRAPH moneyrisk

//GRAPH onepointvaluebasket

//GRAPH gridstep

//stoploss trigger when risk reward ratio is not met already

if onmarket and RRreached=0 then

SELL AT positionprice-mindistancetoclose STOP

EXITSHORT AT positionprice-mindistancetoclose STOP

endif

//stoploss trigger when risk reward ratio has been reached

if onmarket and RRreached=1 then

if floatingprofit crosses under BBfloatingprofit then

SELL AT MARKET

EXITSHORT AT MARKET

endif

endif

//resetting the risk reward reached variable

if not onmarket then

RRreached = 0

endif

{kind=link}

{kind=link}