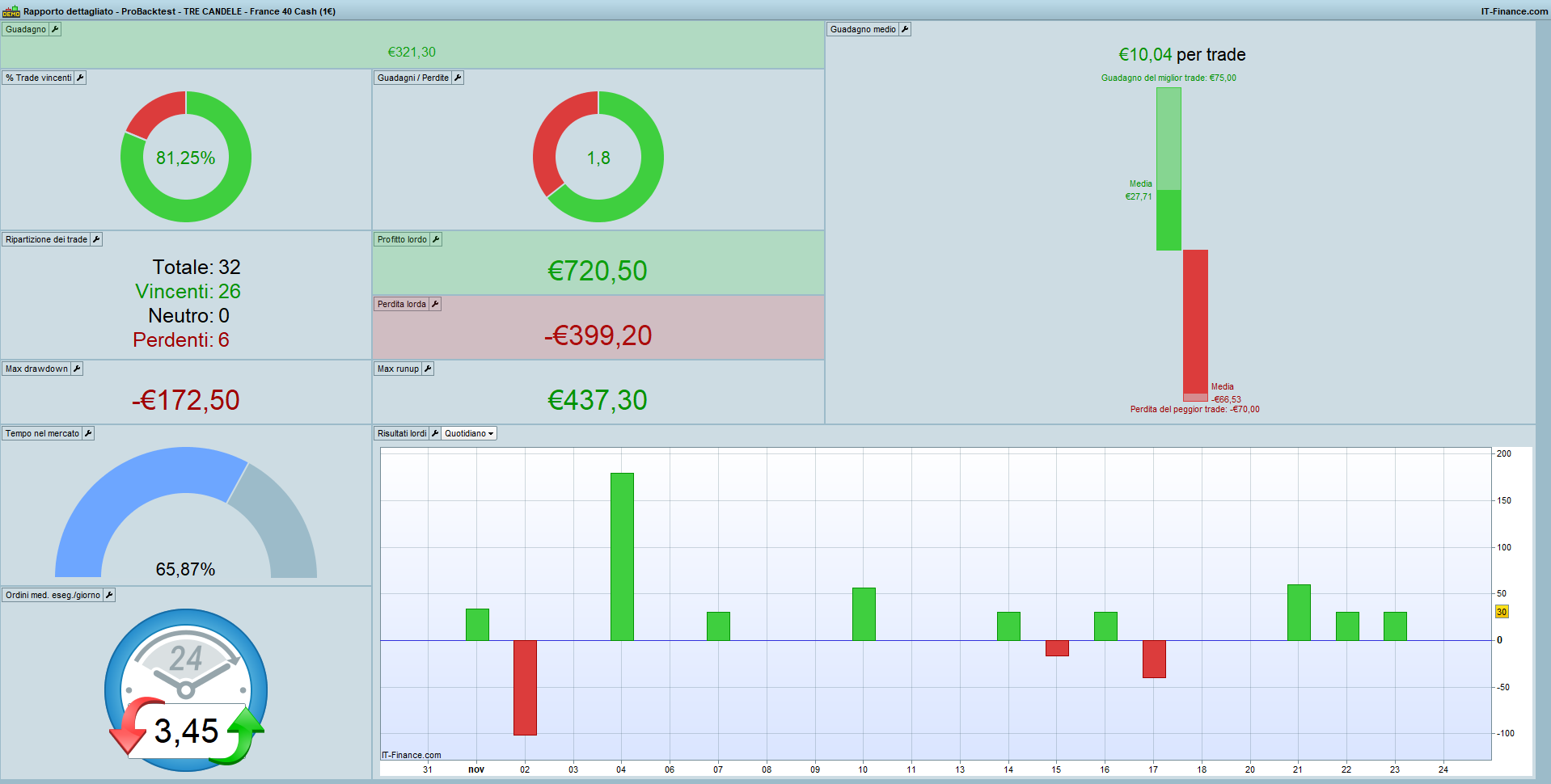

Strategy 3 CANDLES with CAC40

November 29, 2022, 1:03 PM

Strategies

22 Comments

{kind=link}

I would like to share a simple meanreverting system that is based on the analysis of the last 3 candles.

A long range of the last 3 candles of at least 10 pips is considered, and for the short side a move of at least 25 pips.

Preferred indices France 40, Ftse 100 and Dax.

Timeframe 1 minute.Target 75 pips, Stop 70 pips and breakeven update every 30 pips.

Suggestions would be welcome.

DEFPARAM CumulateOrders = False

timeEnterBefore = time >= 083000

timeEnterAfter = time <= 213000

UNO = (open[2] - close) > 10*pipsize

IF timeEnterAfter AND timeEnterBefore AND (open[2]>close[1]) AND (close[1]>close) AND UNO THEN

BUY 1 CONTRACT AT MARKET

ENDIF

DUE = (close - open[2]) > 25*pipsize

IF timeEnterAfter AND timeEnterBefore AND (open[2]<close[1]) AND (close[1]<close) AND DUE THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

SET TARGET pPROFIT 75

SET STOP pLOSS 70

//startBreakeven = 5 //30 pips in gain to activate the breakeven function

//PointsToKeep = 10 //5 pips to keep in profit above/below entry price when the breakeven is activated

//

// test if the price have moved favourably of "startBreakeven" points already

//

// --- LONG side

SCA = 30

IF LONGONMARKET AND (close - tradeprice(1)) >= (SCA* pipsize) THEN

breakevenLevel = tradeprice(1) + (SCA* pipsize) //calculate the breakevenLevel

//place the new stop orders on market at breakevenLevel

IF breakevenLevel > 0 THEN

SELL AT breakevenLevel STOP

ENDIF

ENDIF

// --- SHORT side

IF SHORTONMARKET AND (tradeprice(1) - close) >= (SCA* pipsize) THEN

breakevenLevel = tradeprice(1) + (SCA* pipsize) //calculate the breakevenLevel

//place the new stop orders on market at breakevenLevel

IF breakevenLevel > 0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

ENDIF

Download

Filename:

Strategy3-CANDLES-with-CAC40.itf

Downloads:

359

Senior

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...