Short on rising markets - 4H OnlyShort-Strategy on Dax

May 14, 2018, 6:49 AM

Strategies

9 Comments

{kind=link}

Hello.

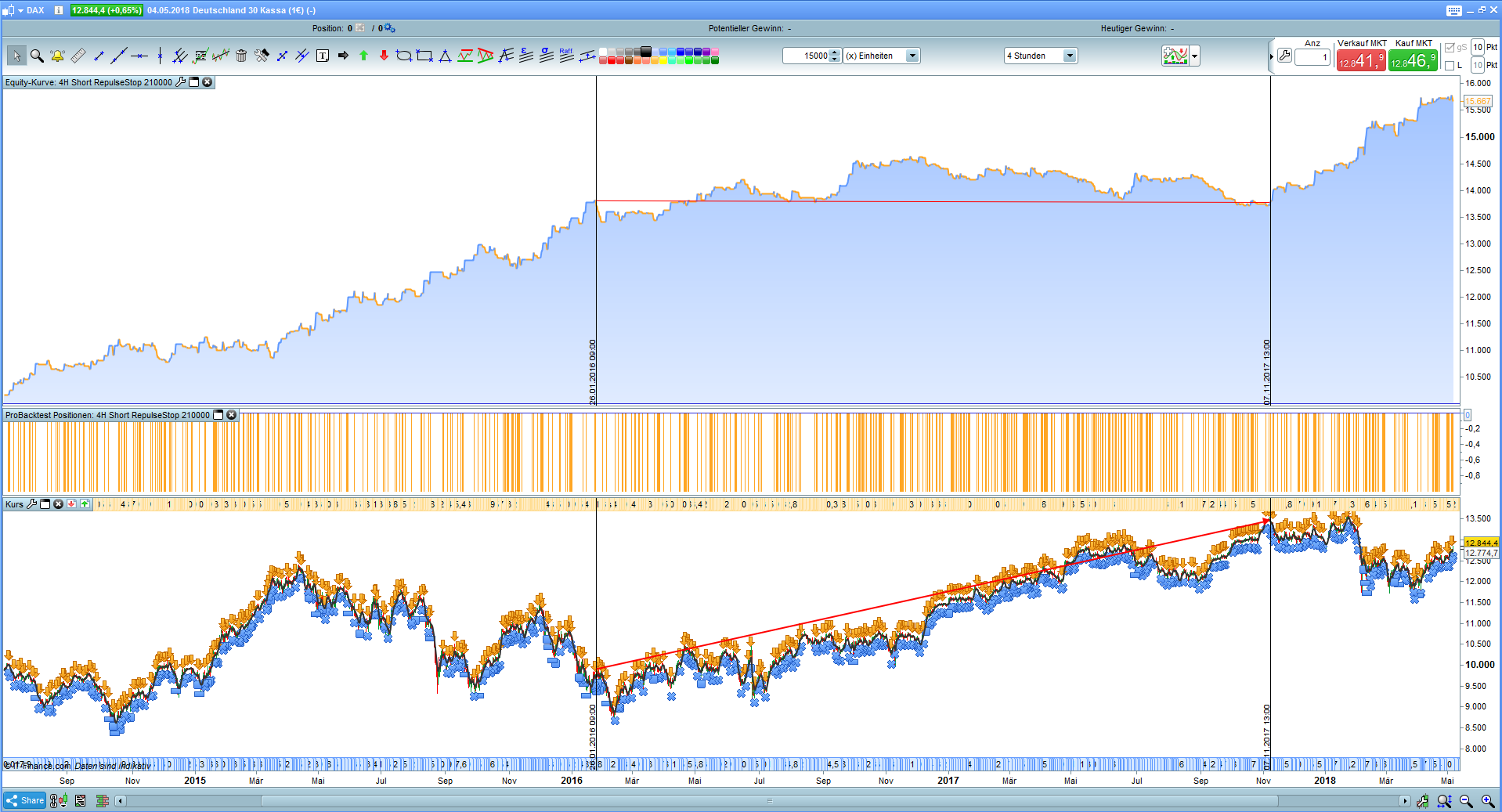

For this little OnlyShort-Strategy here in the Dax, we use the power of candles in the form of the Repulse indicator and provide the strategy with two three small filters.

Protected by the repulse stop and in percent, profits are generated when prices fall, while in the rising market with this OnlyShort-Strategy there are no significant losses.

We start the positions at 09.00 / 13.00 / if necessary 17.00 o’clock in timeframe 4H and in the time zone utc+2 (“Berlin-Time”). The position is closed for a peaceful sleep at 21.00 o´clock.

That’s all.

Until then

JohnScher

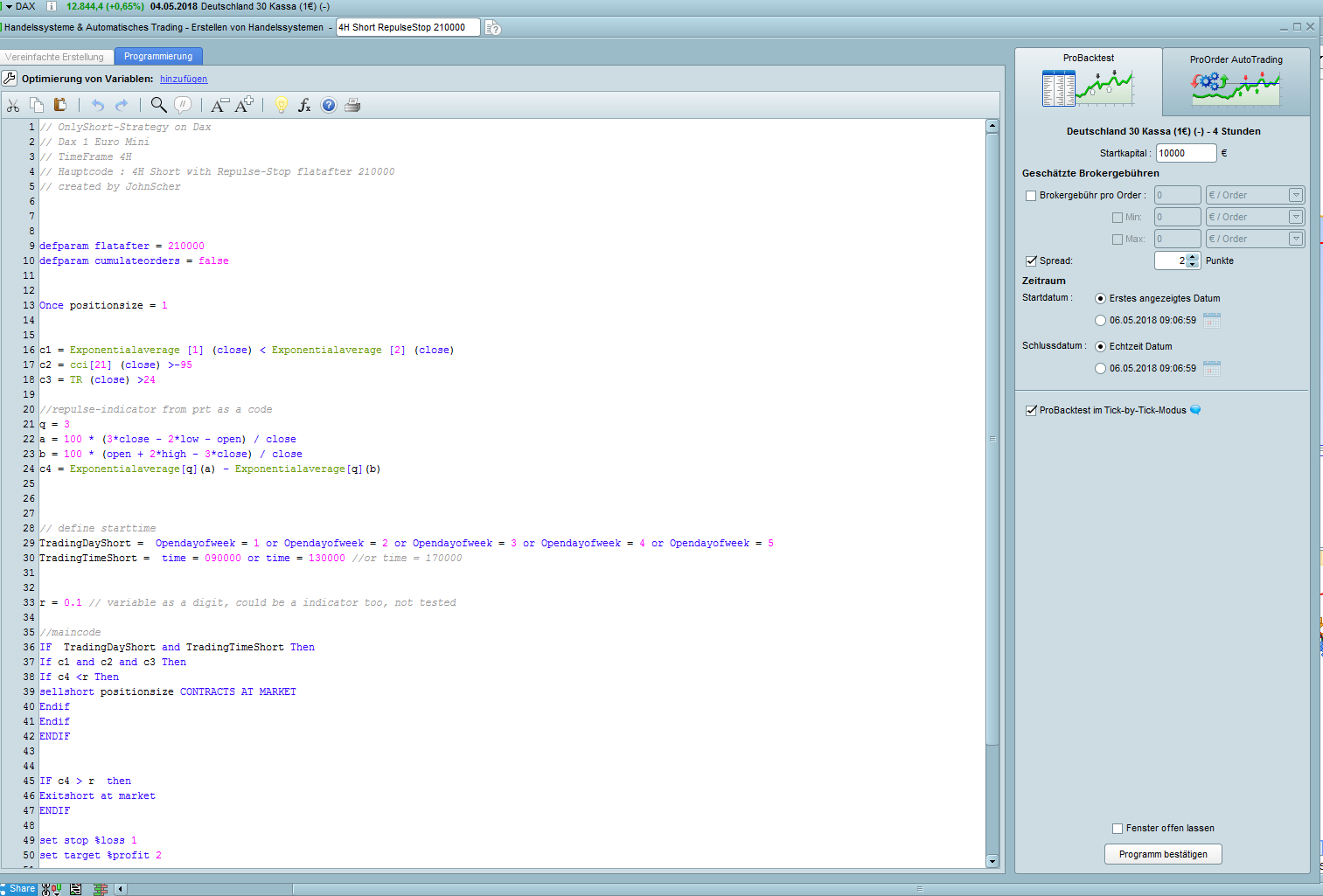

// OnlyShort-Strategy on Dax

// Dax 1 Euro Mini

// TimeFrame 4H

// Hauptcode : 4H Short with Repulse-Stop flatafter 210000

// created by JohnScher

defparam flatafter = 210000

defparam cumulateorders = false

Once positionsize = 1

c1 = Exponentialaverage [1] (close) < Exponentialaverage [2] (close)

c2 = cci[21] (close) >-95

c3 = TR (close) >24

//repulse-indicator from prt as a code

q = 3

a = 100 * (3*close - 2*low - open) / close

b = 100 * (open + 2*high - 3*close) / close

c4 = Exponentialaverage[q](a) - Exponentialaverage[q](b)

// define starttime

TradingDayShort = Opendayofweek = 1 or Opendayofweek = 2 or Opendayofweek = 3 or Opendayofweek = 4 or Opendayofweek = 5

TradingTimeShort = time = 090000 or time = 130000 //or time = 170000

r = 0.1 // variable as a digit, could be a indicator too, not tested

//maincode

IF TradingDayShort and TradingTimeShort Then

If c1 and c2 and c3 Then

If c4 <r Then

sellshort positionsize CONTRACTS AT MARKET

Endif

Endif

ENDIF

IF c4 > r then

Exitshort at market

ENDIF

set stop %loss 1

set target %profit 2

// not tested

// on other major indizes

// with Saisonalpatternmultipler from Pathfinder-Systems

// with some Re-invest-Stategies

// until then

// JohnScher

Download

Filename:

Short-on-rising-markets-DAX-4H.itf

Downloads:

340

Download

{kind=link}

Filename:

Screenshot_4-1.png

Downloads:

76

Download

{kind=link}

Filename:

Screenshot_3-1.png

Downloads:

183

Veteran

I usually let my code do the talking, which explains why my bio is as empty as a newly created file. Bio to be initialized...

Author’s Profile

Loading...