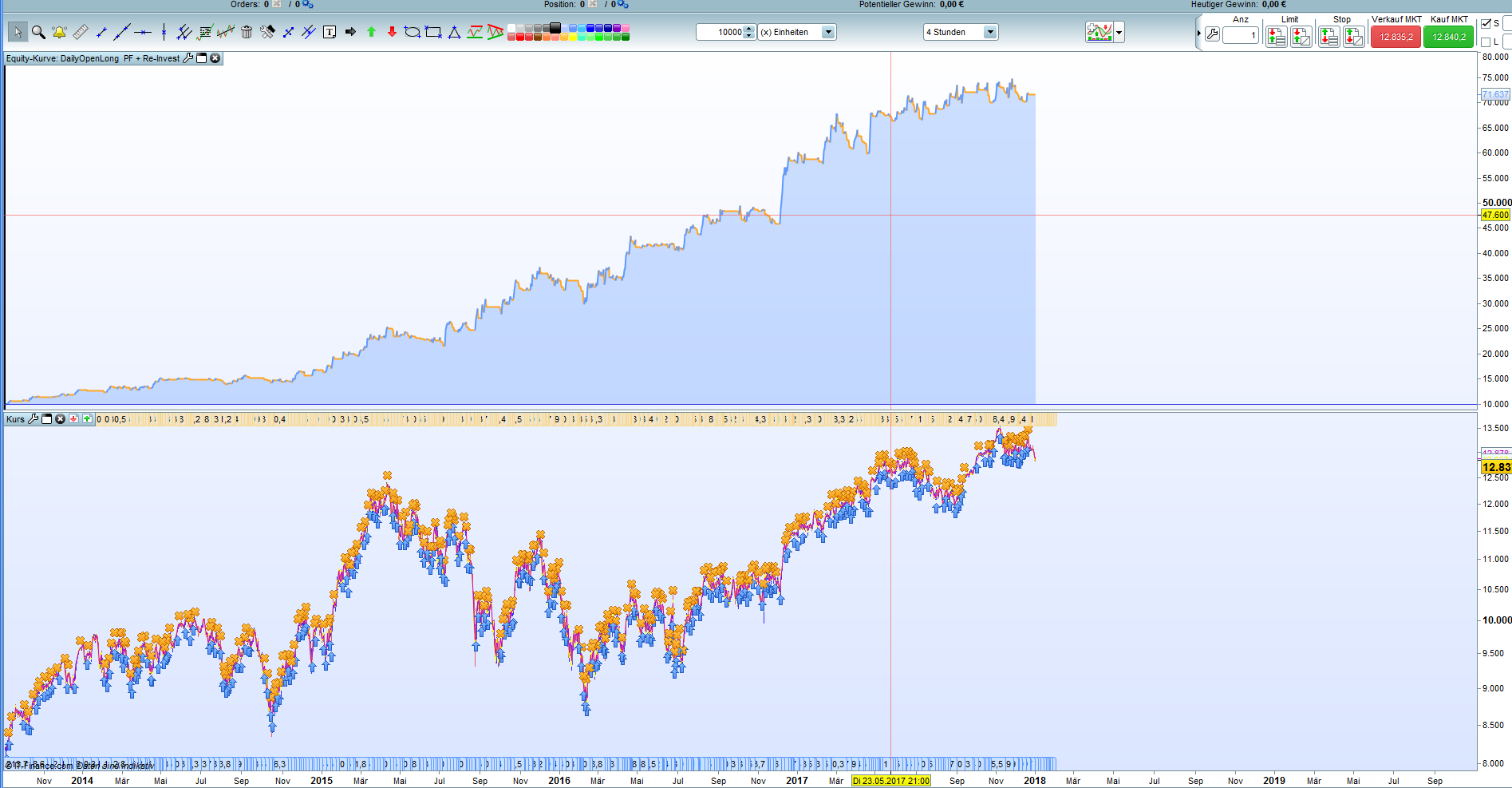

Dax Daily Open Long - timeframe 4 hours

January 3, 2018, 2:05 PM

Strategies

19 Comments

{kind=link}

A simple code with differently weighted averages and a stop by repulse.

Supplemented by the seasonal pattern multiplier and a re-invest strategy.

If necessary, the latter can also be omitted, but it still remains a gain that achieves a higher performance than the Dax itself.

Time conditions should be adapted to your timezone. Timeframe = H4.

You can also do without the fixed TP and SL. The insurance can stay.

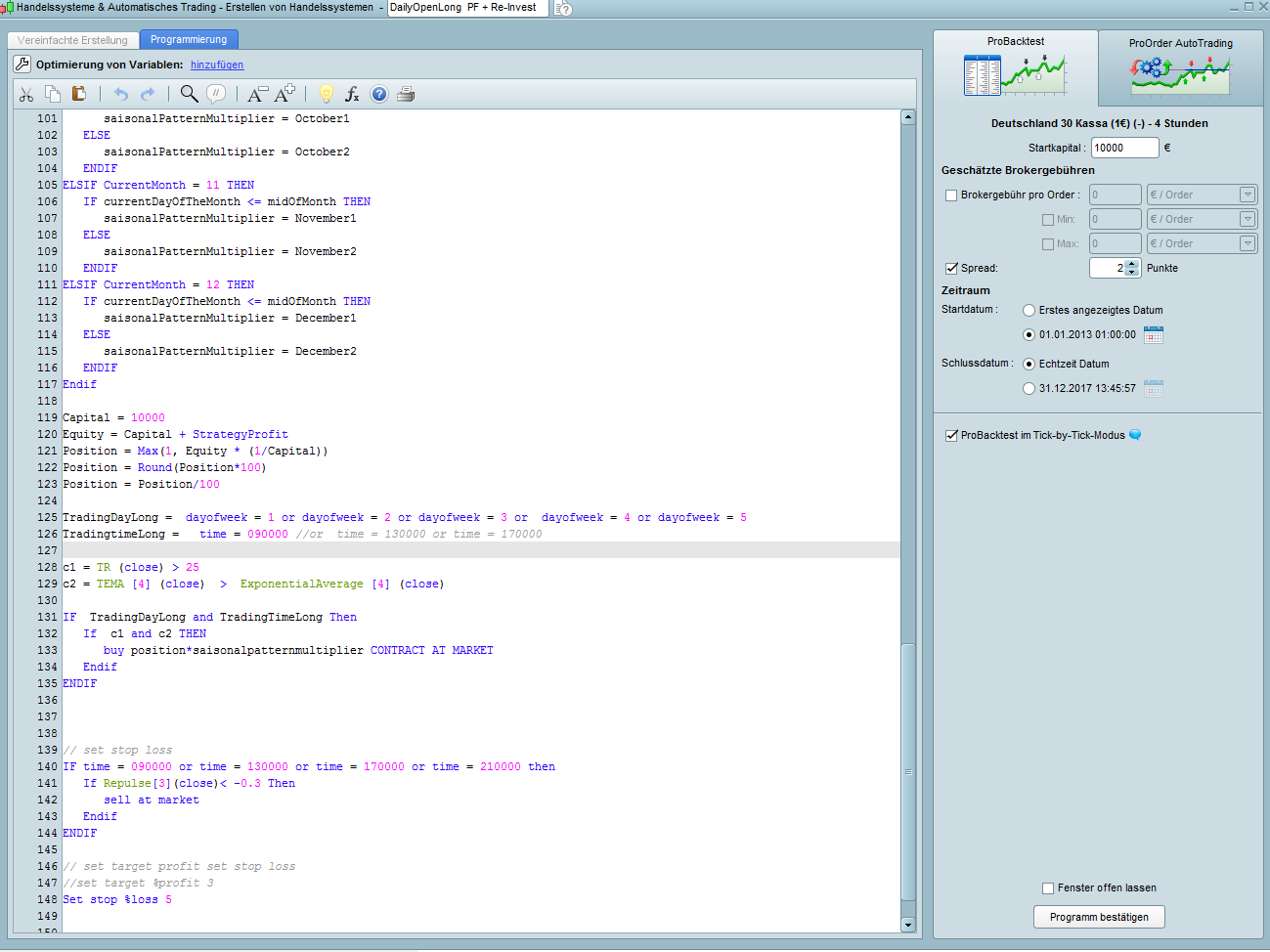

// MainCode : DailyOpenLong

// Dax 1 Euro

// TimeFrame4H

// created by JohnScher

// with SainsonalPatternMultiplier from Pathfinder-Systems

// with Re-Invest-Strategie

//..............................................................

// Start

//..............................................................

defparam cumulateorders = false

// saisonal pattern muliplier

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 0 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 3 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 1 //0 risk(1)

ONCE June1 = 1 //1 ok 2

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 0 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = Day

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

Endif

// end sainsonal pattern multiplier

// code re-invest

Capital = 10000

Equity = Capital + StrategyProfit

Position = Max(1, Equity * (1/Capital))

Position = Round(Position*100)

Position = Position/100

// start maincode

TradingDayLong = dayofweek = 1 or dayofweek = 2 or dayofweek = 3 or dayofweek = 4 or dayofweek = 5

TradingtimeLong = time = 080000 //or time = 130000 or time = 170000

c1 = TR (close) > 25

c2 = TEMA [4] (close) > ExponentialAverage [4] (close)

IF TradingDayLong and TradingTimeLong Then

If c1 and c2 THEN

buy position*saisonalpatternmultiplier CONTRACT AT MARKET

Endif

ENDIF

// set stop loss

IF time = 080000 or time = 120000 or time = 160000 or time = 200000 then

If Repulse[3](close)< -0.3 Then

sell at market

Endif

ENDIF

// set target profit set stop loss

//set target %profit 3

Set stop %loss 5

// end maincode

kind regards

Download

Filename:

DAX-Daily-Open-Long.itf

Downloads:

489

Download

{kind=link}

Filename:

DailyOpenLong-11-1.png

Downloads:

219

Download

{kind=link}

Filename:

dailyopenlong-15147247008pc4l.png

Downloads:

178

Veteran

As an architect of digital worlds, my own description remains a mystery. Think of me as an undeclared variable, existing somewhere in the code.

Author’s Profile

Loading...