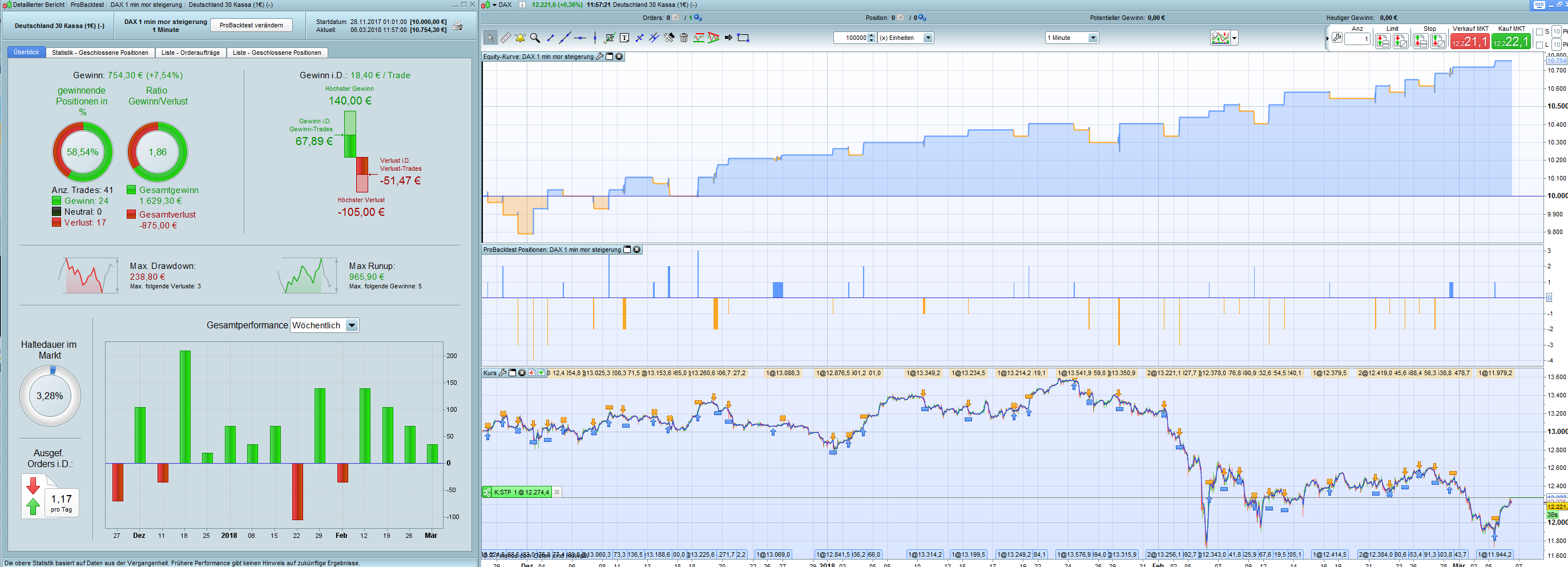

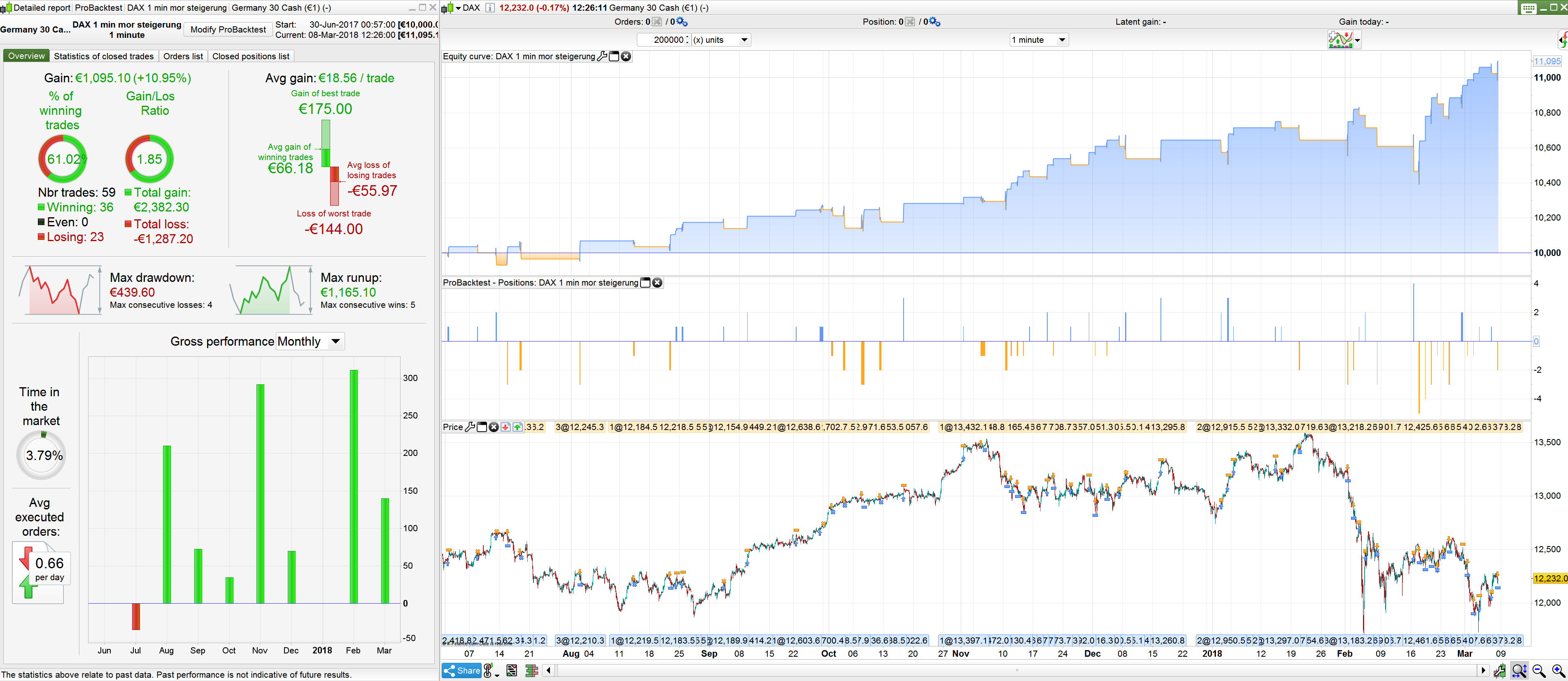

DAX 30 - Morning range breakout with order size increase

March 8, 2018, 1:33 PM

Strategies

18 Comments

{kind=link}

This automatic trading robot use the morning range from 7 o’clock to 9 o’clock of the Dax 30 on a 1 minute timeframe basis. If the price breaks the range up or down, a trade with fixed StopLoss and TakeProfit is set.

This strategy is another version of the famous Open Range Breakout methodology applied on DAX.

DEFPARAM FLATBEFORE=090100

// Festlegen der Code-Parameter

DEFPARAM CumulateOrders = false // Kumulieren von Positionen deaktiviert

// einmalige werte

once size = 1

once profi = 20

once in = 1

once korrek = 1

sl = 35

// Verhindert das Trading an bestimmten Wochentagen

daysForbiddenEntry = OpenDayOfWeek = 6 OR OpenDayOfWeek = 0

noEntryAfterTime = 100000

timeEnterAfter = time < noEntryAfterTime

// einen trade nur

IF (CurrentTime = 010000) then

onetrade = 0

ENDIF

// Bedingungen zum Einstieg in Long-Positionen

IF (CurrentTime = 085900) then

high7 = HIGHEST[120](high)

low7 = LOWEST[120](low)

ENDIF

IF (close > high7) AND (CurrentTime >= 090100) then

onetrade = 1

ENDIF

IF (CurrentTime >= 090100) AND not daysForbiddenEntry AND (onetrade = 0) AND timeEnterAfter THEN

BUY size CONTRACT AT high7 STOP

ENDIF

IF (LONGONMARKET = 1) then

onetrade = 1

in = 1

korrek = 0

//l1 = POSITIONPRICE + 0.0008

l2 = POSITIONPRICE - sl

//sell at l1 LIMIT

sell at l2 stop

ENDIF

// Bedingungen zum Einstieg in Short-Positionen

IF close < low7 AND (CurrentTime >= 090100) then

onetrade = 1

ENDIF

IF (CurrentTime >= 090100) AND not daysForbiddenEntry AND (onetrade = 0) AND timeEnterAfter THEN

SELLSHORT size CONTRACT AT low7 STOP

ENDIF

IF (SHORTONMARKET = 1) then

onetrade = 1

in = 1

korrek = 0

//s1 = POSITIONPRICE - 0.0008

s2 = POSITIONPRICE + sl

//EXITSHORT at s1 LIMIT

EXITSHORT at s2 STOP

ENDIF

// korrektur

IF (LONGONMARKET < 1) AND (SHORTONMARKET < 1) then

in = 0

ENDIF

IF in = 0 and korrek = 0 then

d1 = POSITIONPERF(1) > 0

d2 = POSITIONPERF(1) < 0

IF d1 and size > 1 then

size = size - 1

korrek = 1

ELSIF d2 then

size = size + 1

korrek = 1

ENDIF

ENDIF

// Stops und Targets

SET STOP pLOSS 60

SET TARGET pPROFIT sl

// Performance

IF STRATEGYPROFIT > profi then

size = 1

profi = profi + 20

ENDIF

Download

{kind=link}

Filename:

DAX-open-range-breakout-automated-trading-strategy.png

Downloads:

454

Download

Filename:

DAX-1-min-mor-steigerung.itf

Downloads:

803

Average

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...