Heiken Ashi TMS/TDI strategy

{kind=link}

Hi guys.

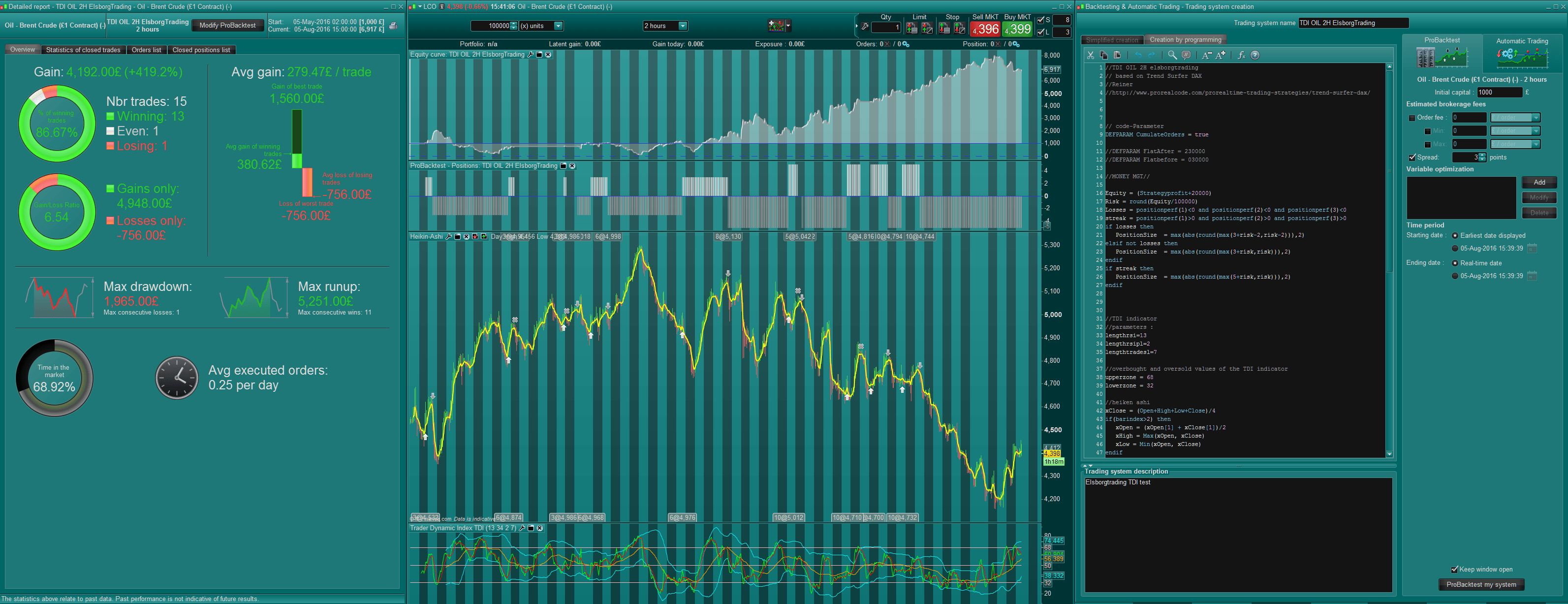

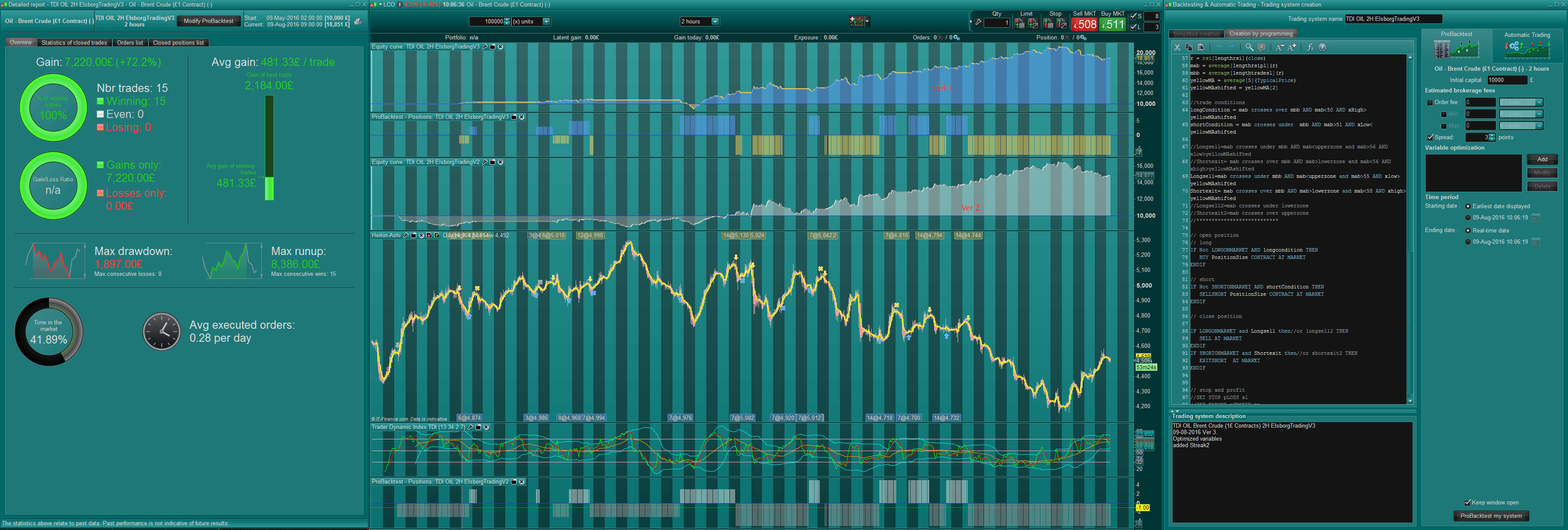

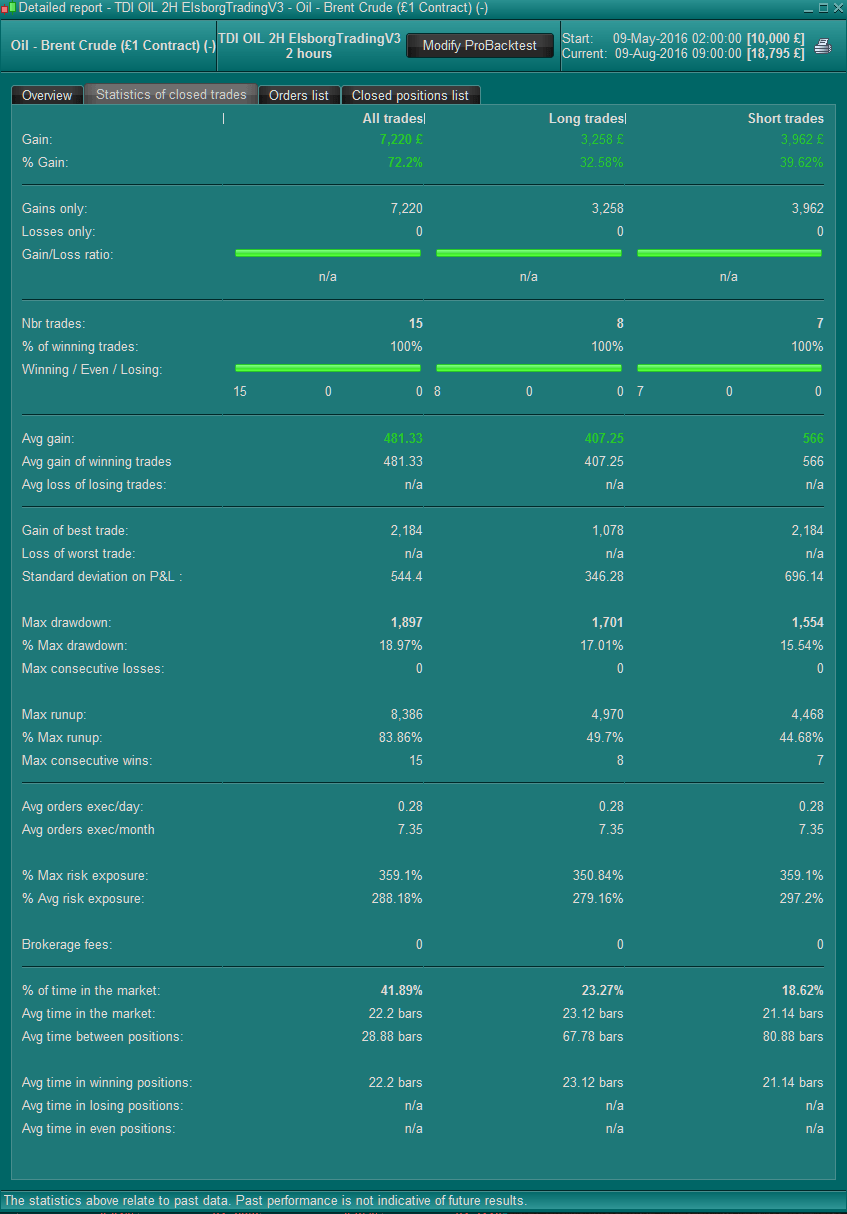

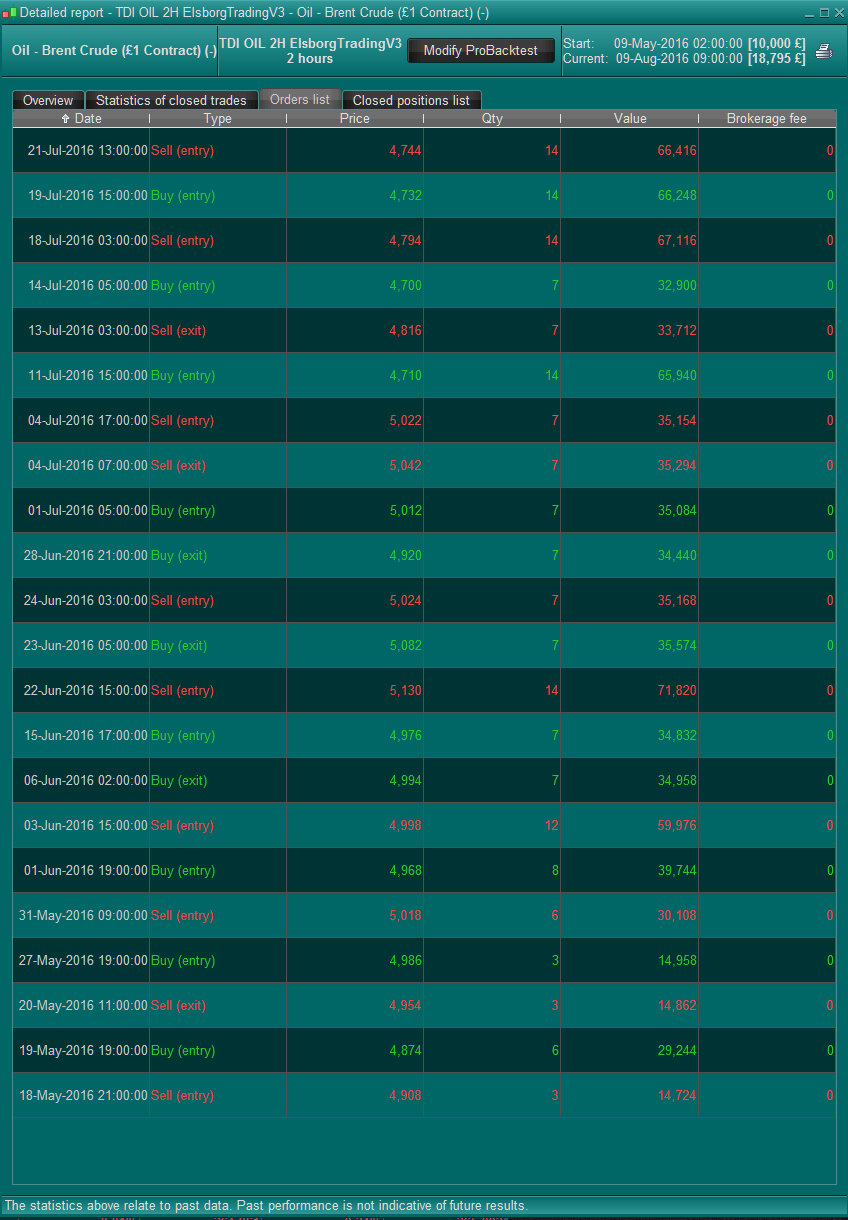

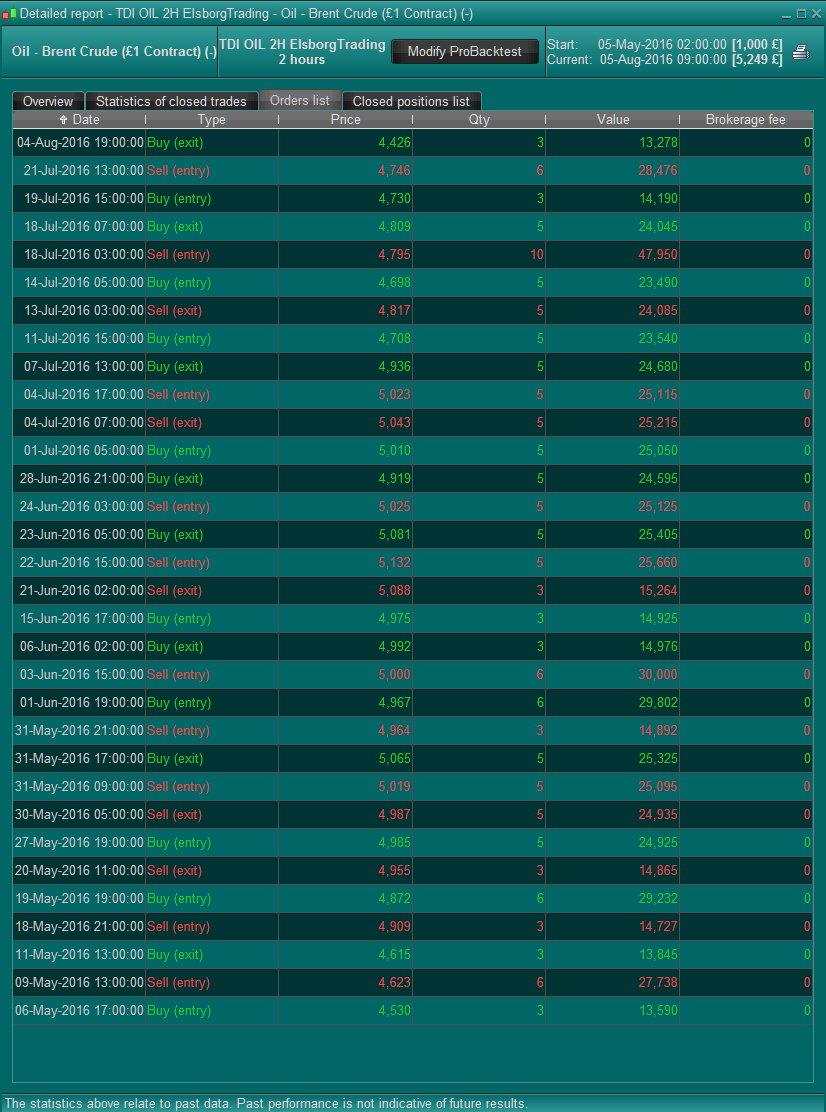

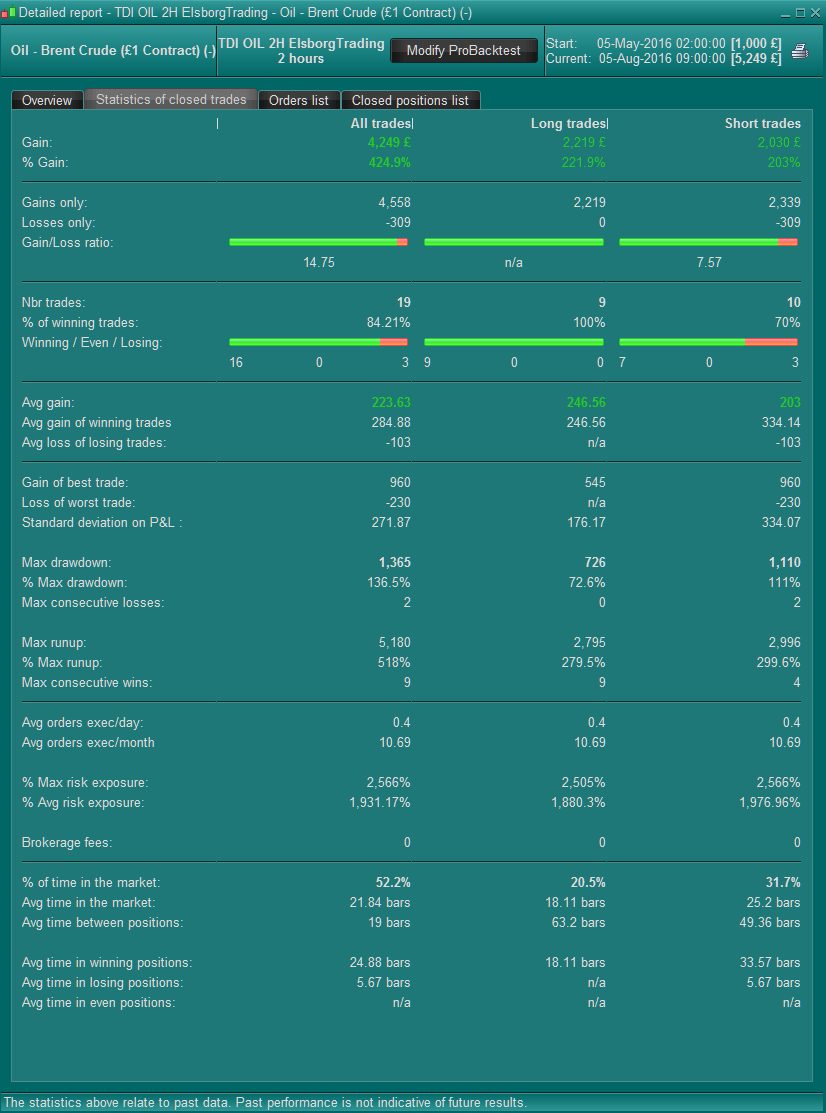

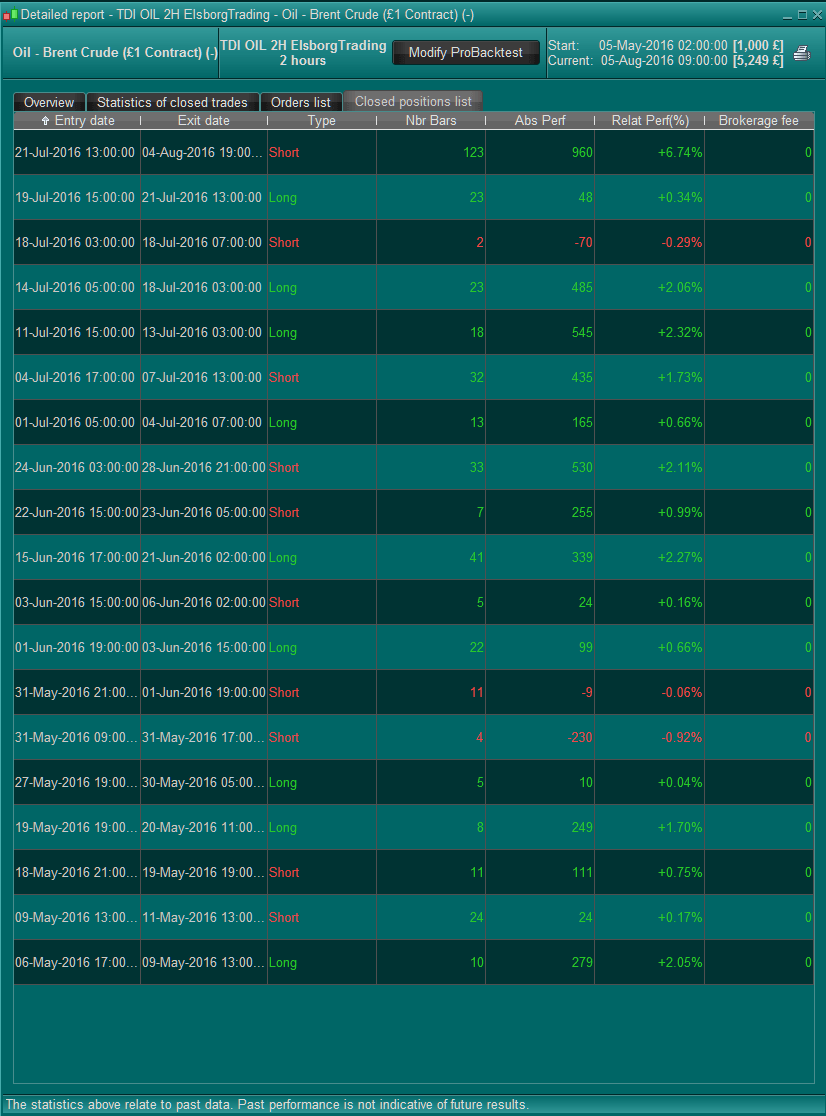

My first contribution to the strategy site. It’s based on several codes from the site, but mainly the TDI and TMS from both Nicolas and Reiner. I changed the strategy a bit so it fits the Oil- Brent Crude. It seems like that every strategy that I test need to be “adjusted” to the particular instrument. Does anyone do the same, or do you strictly keep the rule? Anyway the code has no zero bar profit nor does it have SL or TP coded, in fact it has only 15 trades over 3 month. It sure could be more “perfect” as there are some entries that could be more profitable. Unfortunately I can only backtest it 3 month. Apparently IG only hold 3 month of data for Crude Oil. It’s tested with a 3 point spread. Anyway here it is, please comment 🙂

Cheers

Kasper

//TDI OIL 2H elsborgtrading

// based on Trend Surfer DAX-Reiner/Nicolas-TMS

//http://www.prorealcode.com/prorealtime-trading-strategies/trend-surfer-dax/

//http://www.prorealcode.com/topic/trading-made-simple-tms-system/

//http://www.forexmt4.com/_MT4_Systems/Traders%20Dynamics/TDI_1.pdf

// code-Parameter

DEFPARAM CumulateOrders = true

//DEFPARAM FlatAfter = 230000

//DEFPARAM Flatbefore = 030000

//MONEY MGT//

Equity = (Strategyprofit+20000)

Risk = round(Equity/100000)

Losses = positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0

streak = positionperf(1)>0 and positionperf(2)>0 and positionperf(3)>0

if losses then

PositionSize = max(abs(round(max(3+risk-2,risk-2))),2)

elsif not losses then

PositionSize = max(abs(round(max(3+risk,risk))),2)

endif

if streak then

PositionSize = max(abs(round(max(5+risk,risk))),2)

endif

//TDI indicator

//parameters :

lengthrsi=13

lengthrsipl=2

lengthtradesl=7

//overbought and oversold values of the TDI indicator

upperzone = 68

lowerzone = 32

//heiken ashi

xClose = (Open+High+Low+Close)/4

if(barindex>2) then

xOpen = (xOpen[1] + xClose[1])/2

xHigh = Max(xOpen, xClose)

xLow = Min(xOpen, xClose)

endif

//indicators

r = rsi[lengthrsi](close)

mab = average[lengthrsipl](r)

mbb = average[lengthtradesl](r)

yellowMA = average[5](TypicalPrice)

yellowMAshifted = yellowMA[2]

//trade conditions

longCondition = mab crosses over mbb AND mab<50 AND xHigh>yellowMAshifted

shortCondition = mab crosses under mbb AND mab>50 AND xLow<yellowMAshifted

Longsell=mab crosses under mbb AND mab<upperzone and mab>50 AND xlow>yellowMAshifted

Shortexit= mab crosses over mbb AND mab>lowerzone and mab<50 AND xhigh>yellowMAshifted

//***************************

// open position

// long

IF Not LONGONMARKET AND longcondition THEN

BUY PositionSize CONTRACT AT MARKET

ENDIF

// short

IF Not SHORTONMARKET AND shortCondition THEN

SELLSHORT PositionSize CONTRACT AT MARKET

ENDIF

// close position

//Longsell

IF LONGONMARKET and Longsell THEN

SELL AT MARKET

ENDIF

//Shortexit

IF SHORTONMARKET and Shortexit THEN

EXITSHORT AT MARKET

ENDIF

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}