Hi Reiner,

Just a “classic” suggestion :

1/ Did you try to optimize the Stoploss call/short on volatility (ATR…) and not % of close ?

And less classical, to lower the (max) drawdown (notably):

2/ To optimize the stoploss not on % of close but on a Trailing stop of the equity curve (smooth the equity curve in my experience) ?

Thanks for your work

Zilliq

Hi Zilliq,

Thanks for your suggestions for improvement.

1. I played around with a lot of thinks and also with ATR depending position management but nothing was really better then the simple percentuage stop/take profit mechanism.

2. I have observed that the trailing stop exit is a seldomly event. I invest a lot of effort but didn’t find something that was much better then Nicolas default trailing stop algo.

Your suggestions are valueable ideas and it would be helpful if you could provide me with some code examples.

Thanks, Reiner

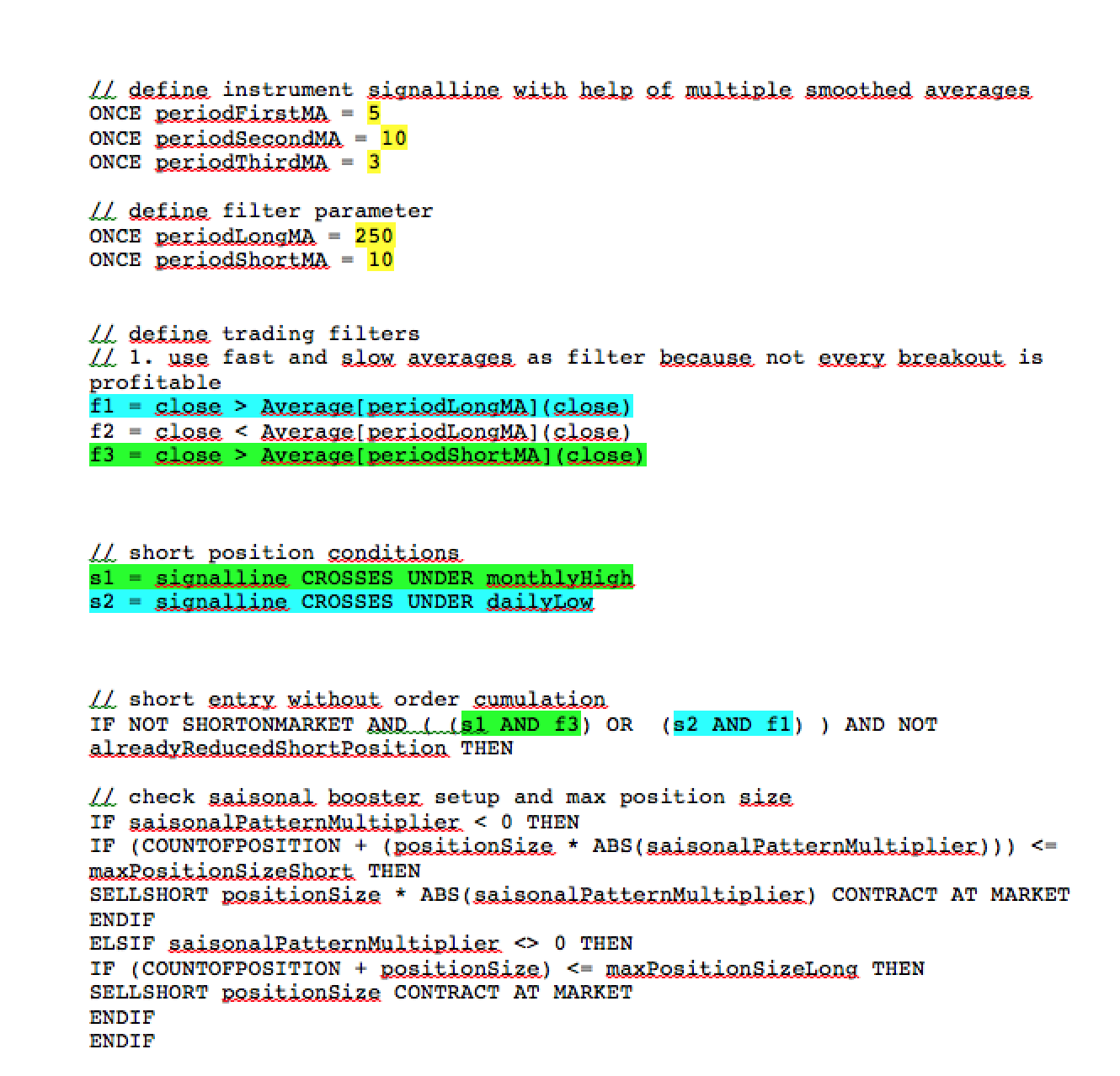

@Reiner,

I think I have found an error in the code on the short side for the 4H TS.

In line 7 below, the code must be: “IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeShort THEN”

However, in backtest it seems like it does not have that much impact on the performance.

In that case, it is consequently wrong in the 5 TS in this topics first post.

Don’t you agree?

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

Hi H_kan,

Yes, you have found an error. But this has no effect because the default max position size for long and short are equal (10).

Thanks for your feedback. I’ll change it in the next release.

Best, Reiner

Hi Reiner,

Thanks for your answers. Personnaly, I prefer the Van tharp approach to determine the position sizing, who depends on the stop loss notably. It’s more logical I find and a better control of the risk I think

I see your code, and I just want to be sure that it was what you wanted to do with this line

maxPositionSizeLong = max(10, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

Because, like this as you will see on my graph you always increase the risk you wanted

I put these lines on the codes to control on the graph

graph maxPositionSizeLong

graph abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize)

As you see with the risk you define (5.5 for DAX) it should take one or 2 position, but with this first line it take sometimes 6 positions ! If the Stoploss is touch, you burn your account …

Are you sure that it was what you wanted to do because like this the risk is very much higher than you wanted

Bye and thanks for your work

Zilliq

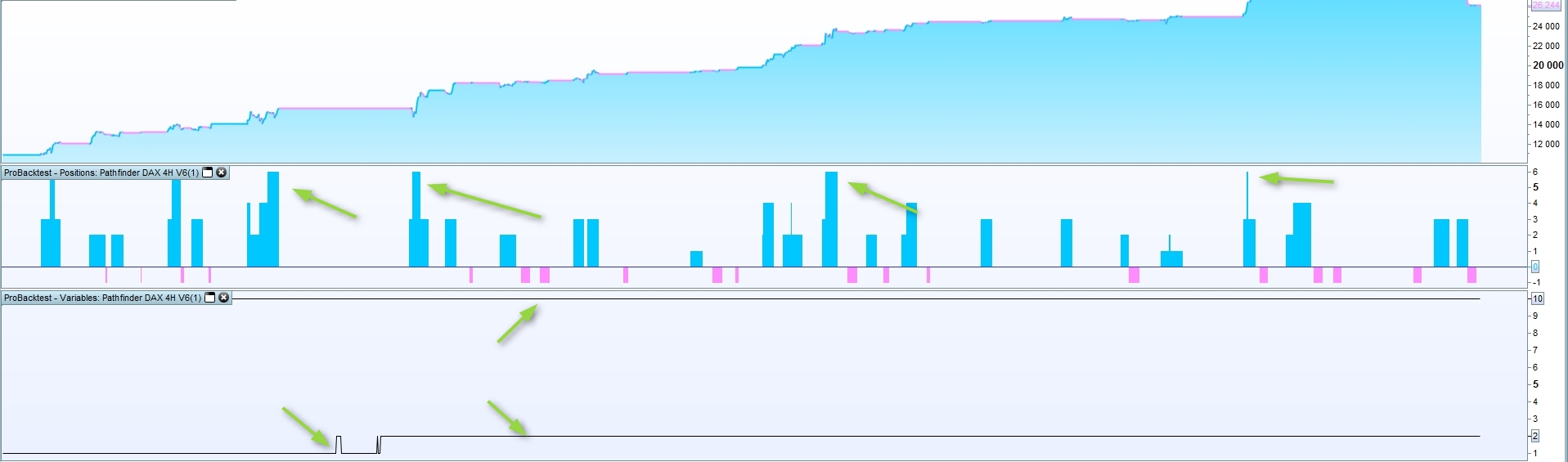

Hello!

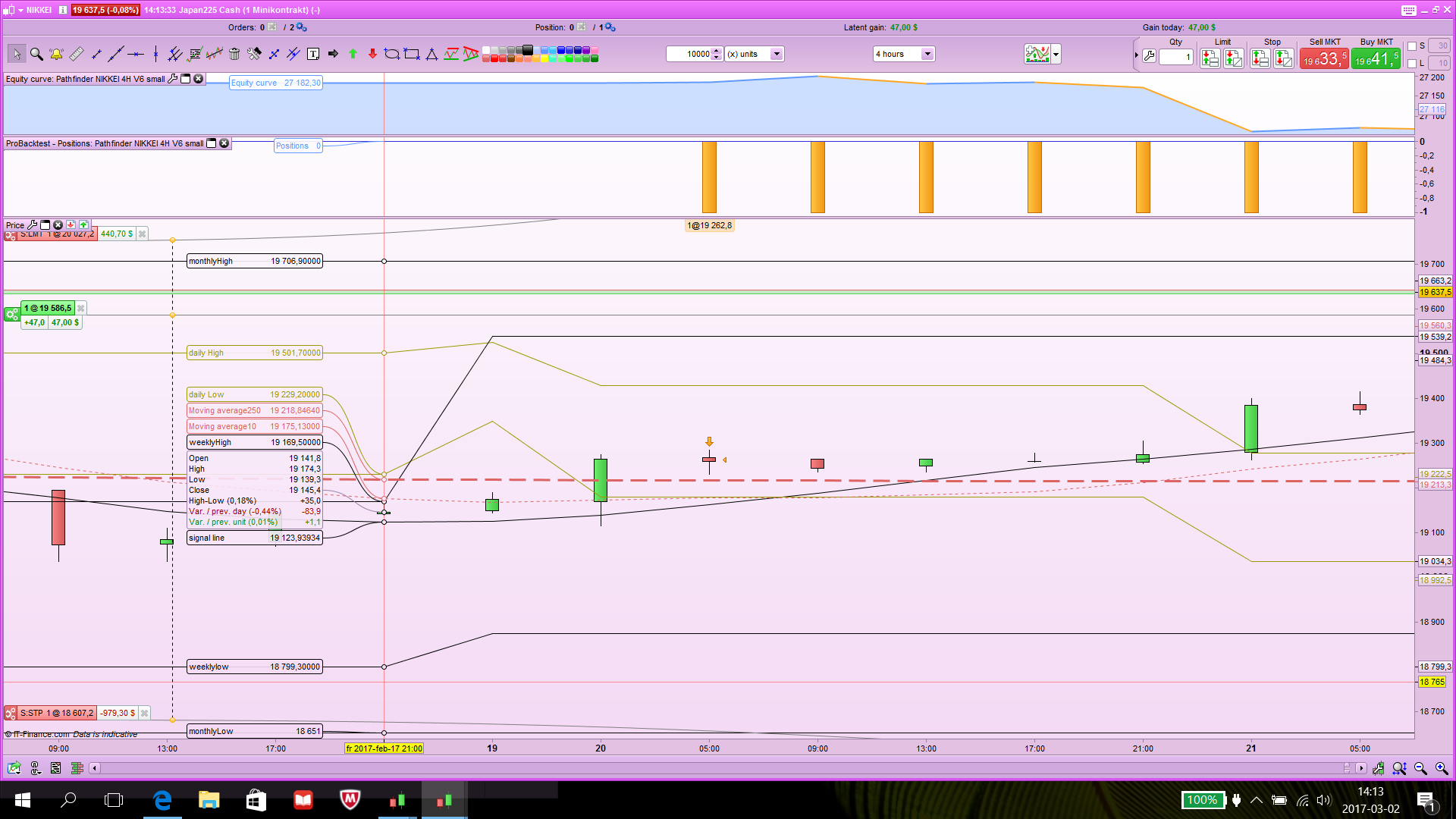

I was looking in to Pathfinder NIKKEI 4H V6 tonight to see if it was going to take any livepositition and noticed that all the short trades i looked at in backtest where taken randomly. have anyone else noticed that?

Thanks for good work and sharing Reiner!

Regards Henrik

@Henrik by randomly do you mean that it doesn’t jump out at you why there is a trade at that point?

My last trade on the Nikkei was 20 Feb entry and 21 Feb exit … is that what is shown in your screen shot (you dont show dates).

Cheers

Graham

Hi Reiner and other friends,

A quick calcul on DAX show

if stopLossLong = 5.5 % of the close

And the countof position is often 5 as we see on backtest

If the Stoploss of the 5 positions is touch, the system loose

0.055*5*close(+/-12000)=3300 euros

equal 3300/10000= 33 % risk not the 5 % define by the system at the beginning…

This is really what you wanted to do ?

Have a nice day

Zilliq

Hi!

Yes Grahal, I refer to trade 20 Feb entry and 21 Feb exit as an example. I cant see that the conditions has met for short position. I post new pictures for better overlook. Ive configured the pathfinder indicator with nikkis numbers so that is what you see in the pricechart. Chart pictures displays my backtest. Long orders seems ok! ive changed positionsize for this code but same things happen with the original bigsizecode. Have I missed something or what is wrong?

Cheers

Henrik

Hi Reiner,

Some other suggestions (may be you already think about them)

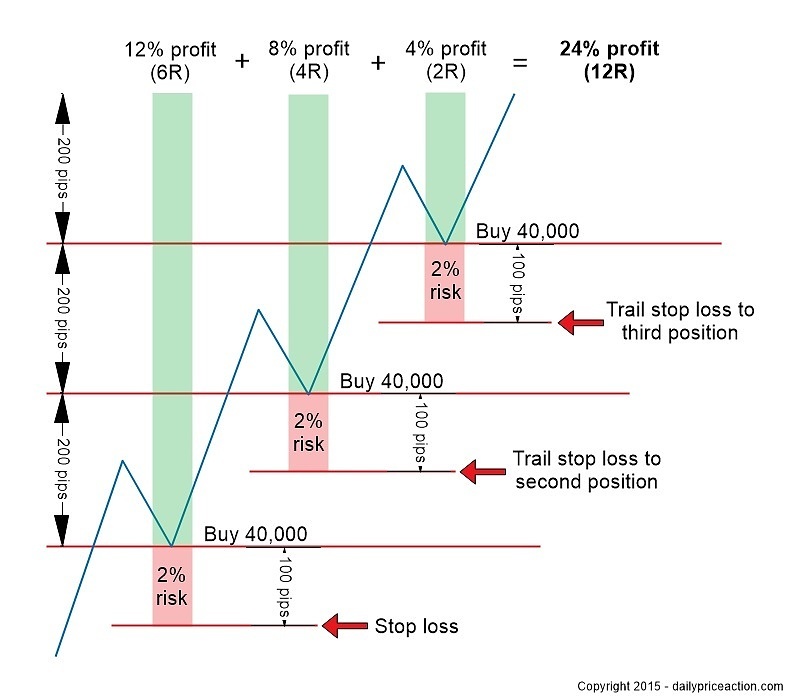

1/ Did you try to progressively sell positions on call (and buy on short). For example the system buy 5 successive positions in different times and it sell one position every 1ATr, x point, x % etc ..?

The purpose is that if reverse, you already win on some positions

For example you have a stop loss at x points, you buy progressively 2 positions : At 2*x points the system sell (for a call) one position and continue with one : If the index reverse you are flat

It’s a different point of vue than the breakeven. The problem with the breakeven is that often you have some retracements and you’re stop even if you’re right

2/ Did you try to pyramid ONLY if the trailing stop is higher than the previous position (for a call, inverse for a short)=an improvment of the breakeven of the last position. The purpose is to pyramid with more security and if you reverse it’s not a problem you’re flat or winner (cf picture below)

Bye

Zilliq

One other…

Add calculation fee (because sometimes Pathfinder stay many days on road)

According to Nicolas code

https://www.prorealcode.com/blog/learning/overnight-fees-calculation-proorder-strategies/

…

Bye

Grrr I can’t edit my last post ….

Other idea…

Did you try martingale code on Pathfinder : Buy one more position if you lose the previous one (but not more than the max position you can) ?

https://www.prorealcode.com/blog/practical-martingale-code-automated-trading/

….

Arno

ArnoParticipant

Average

Hi zilliq,

I asked exactly the same question this evening on Pathfinder swing TS forum 😉

Hi Reiner, We know that we have a statistical advantage to buy the market with Pathfinder swing TS entry. We known that a downward strategy averaging (inverted pyramid) is effective in this context of high probability of rise. When the p&n is negative following a Pathfinder swing TS entry, it would be interesting to take a second position at a lower price while respecting the pathfinder stops loss. I’m currently manually testing this idea. What do you think ? It is an alluring idea no ? I don’t know well coded and i would like to know if you have tested this idea or if it’s already integrated to Pathfinder swing TS ?

Hi Arno,

I think that to pyramid a position AFTER the trailing stop is higher than the close of the previous trade is a good thing (As everyone said and write)

1/ BUT I don’t know (but I think) it’s a better and safer solution instead of taking a position on every candle when the conditions are good (Solution 1). In this case, you cumulate quickly a lot of positions and cumulate the risk in case of reverse (Solution 2). It’s not what we recommend to pyramid. In the solution 1 you increase you profit may be lower, but safer, in the solution 2 quicker but with more risk

2/ BUT I think it’s a very risky solution to average the loosing positions. Because the risk is to go lower and lower

That’s just my opinion

Cheers

Hi Guys,

For different reasons I decided to finish all my public projects in this forum. Thanks a lot for your support especially to Nicolas. I’ve learned a lot in the last year. This forum is a great source of PRT know how and inspired me very much.

Good trades, Reiner