Paul

PaulParticipant

Master

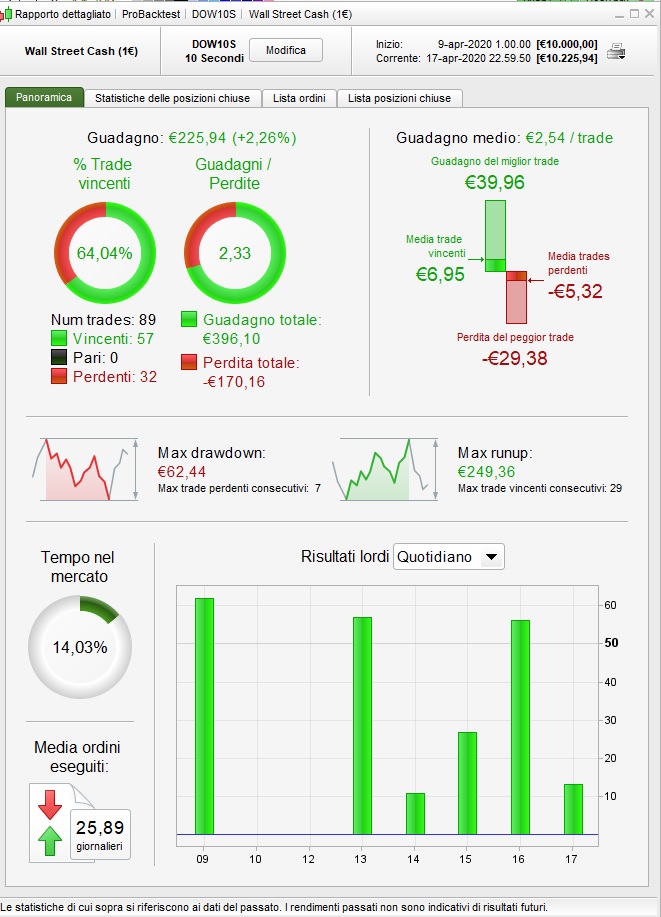

I loaded up you code and saw your results which were oke, but spotted also there wasn’t a stoploss in the code. If there was 0.5% stoploss the results in the backtest go down.

the maxloss 1 was meant that if the total loss of the day exceeds 1% there will no new trade made for that day. That means in your trading today if you have a position and it turns negative, you take the big loss and THEN no new position will be made.

So basically it looks you traded without stoploss, which I wonder how that is possible!

Thanks Paul for explanation. A better point of entry seems key to avoid being stopped out. Also I noticed that the trend often continued after the trailing stop cut the trade, so the trailing stop seems a bit too tight. But this migth not always be the case as I haven’t been watching the screen at all times when running the demo. As it stands I a 2% stop loss will be needed on a small account like my live account.

The same code in demo forward test shows different amount of losses, for example, £105.60, £104.50, 143.40, £255.40, £250.80. How come there are so different when there is no stop loss in this code? How / when does this code decide to pull out when the trade is going the wrong direction?

PaulParticipant

Master

say have a long entry & market goes down 0.60% and then goes up again +1%

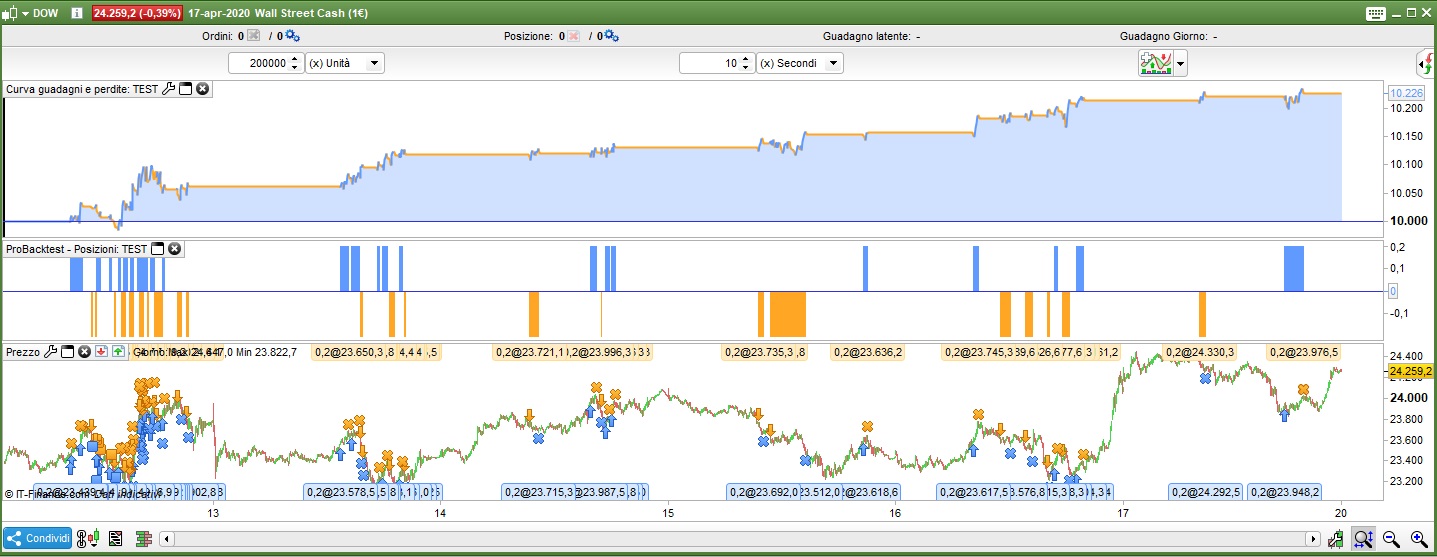

If trading without or with a big stoploss you have a win and never see the loss (look at the backtest report at the mae colum, where it shows how much the position was turned against you)

If you were exited on stoploss 0.5% you have a loss, but if quickly a new long signal appears you likely also have a new win.

(you don’t see or act on that new signal with a big stoplosss! That’s why good optimisation parameters are often “unreliable”)

So a code with a smaller stoploss (and/or ts/ pt ) creates more trades but spread takes quickly away profits on a small timeframe.

Trailingstop is a bit tricky. Too tight and you miss out on a bigger rally. Too big and the market has less range at that time, you could end up with loss instead of a (smaller) win.

Not easy to find a nice balance!

Well so, why not adding ML also to the stoploss? Tried on my yesterday’s test: half drawdown and much less trades

If trading without or with a big stoploss you have a win and never see the loss (look at the backtest report at the mae colum, where it shows how much the position was turned against you)

@Paul I look at MAE also and have been trying to bring this down with more precise entries. Now testing with MA Crossover and backtest results look really promising. It now works much better with stoploss..

I will forward test next week. I also divide the total of MAE with MFE to get an e-ratio, higher number is better. Anyone else doing this also when creating strategies?

https://www.dukascopy.com/fxcomm/fx-article-contest/?Measurement-Of-Potential-In-Trading=&action=read&id=1861&language=en

I also divide the total of MAE with MFE to get an e-ratio,

Sorry.. I was meant to say: total of MFE / total of MAE = e-ratio

Higher than 1 is good. I’m getting 3.5 at the moment.

Anyone else doing this also when creating strategies?

Not heard of anyone, but thanks for drawing our attention to it and the article!

I have in the past used MFE / MAE as a quick way to determine range for TP and SL in the optimiser.

I will be taking a closer look now, but as usual any analysis will have to be done off Platform …. which I find a pain / annoyance! If the columns on the Backtest Detailed Report showed totals then calculating the total e-ratio would be a simple 2 second calculator job!? What do you do … drag and drop results into excel??

I wonder if @Vonasi has heard of this … he may even be tempted do one of his big analysis jobs that will prove / disprove the theory??

From the charts in the article, one can see that the total e-ratio could be a useful yardstick to a System’s predictability and stress free trades (as if!? 🙂 )??

I’m going to do an e-ratio right now!! 🙂

EDIT / PS

It was only about 30 seconds anyway and that included opening google sheets!

Total e-ratio = – 1.73 … minus would be ignored.

Here we go again, an immediate annoyance … we can’t see MFE and MAE on the Detailed Report of a System under Forward Test! So we won’t be able to check backtest e-ratio against forward test e-ratio!

And of course we can only copy and paste 1000 rows!

I just tried scrolling down to where the 1000 rows ended and copying from thereon to the end, but no go … still only get the 1st 1000 rows no matter what! I’d have to backtest from and to specified dates to get around the 1000 row limit for copying to excel??

My System had 1251 trades! E-ratio for the most recent 1000 trades is 1.36 … guess that is good enough, don’t need all the trades as e-ratio is only a broad brush test anyway.

Now I’ll try and find a System that has been performing badly on Forward Test, then backtest it to get MFE and MAE and see what the e-ratio is!? 🙂

And of course we can only copy and paste 1000 rows!

@Grahal – yes this is super annoying. I don’t know if there is a workaround to that issue? I use excel in order to do analysis outside of Prorealtime – not ideal but it works. Would be great to be able to export more rows. Will this be possible in PRT11 perhaps?

PaulParticipant

Master

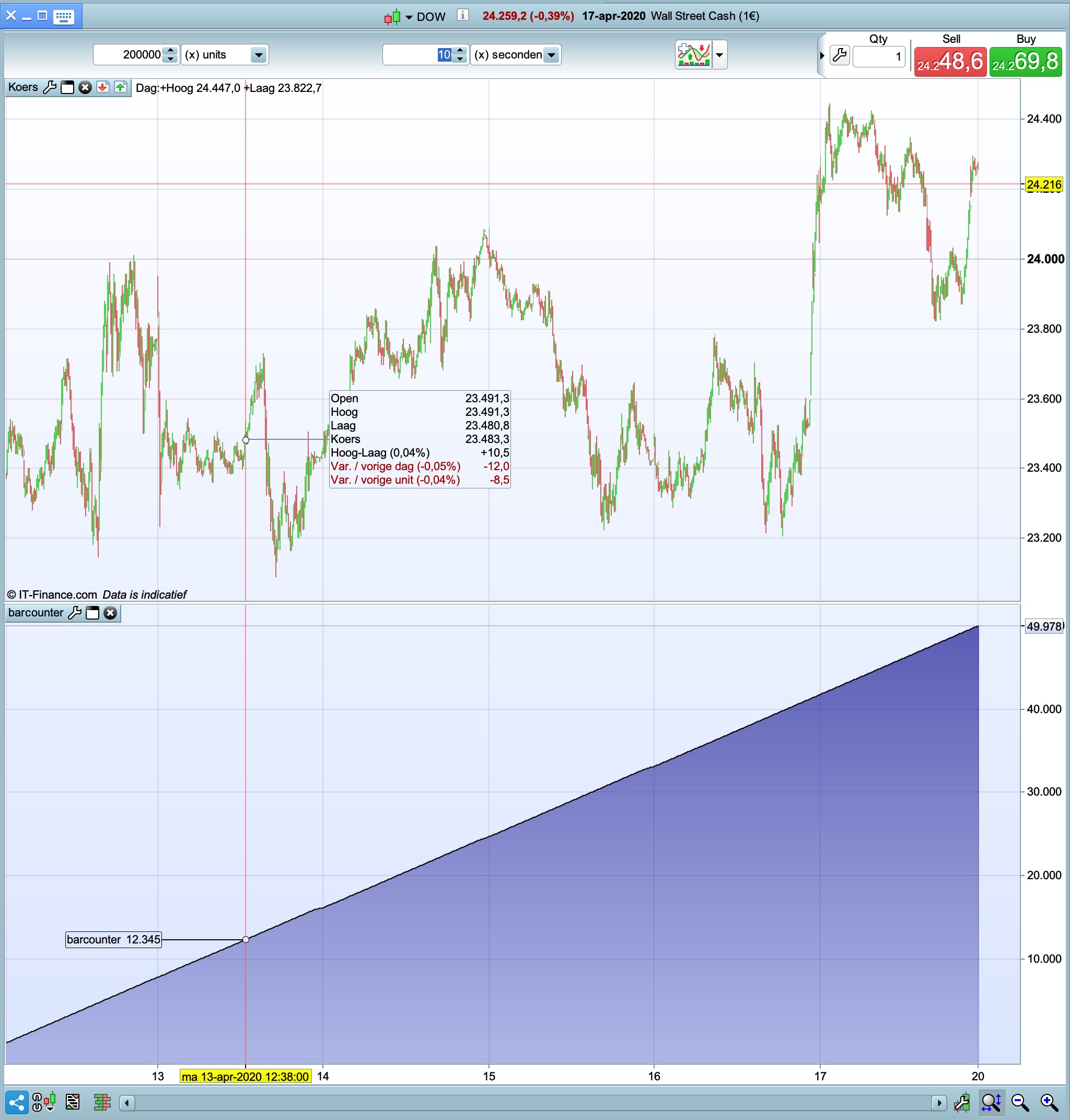

is 10 seconds the way to go or go faster & have more bars ?

barcounter 10s vs 2s vs 1s

edit 1s again, chart was zoomed in a bit.

Interresting Paul. I’m using 1s now too and trying to figure out if I have overoptimised or if it will work in real life. Will try on Monday and will let you know.

Regarding trailing stop, would it be possible at all to start 2 positions (as separate orders) and activate one with trailing stop 2 (fast) and let the second run with trialling stop 1 (slow)? If that’s possible, maybe that’s worth exploring?

As far as I understand one can not partially close a position started off from the same level, but if one order is filled 1-2seconds after the first one maybe that can be done?

is 10 seconds the way to go

Forgive the daft question … what is this about?

Just say look back 2 pages etc if there’s been a discussion re number of bars?? 🙂

PaulParticipant

Master

Yeah, thats why I posted, although a bit late 🙂 Just sharing pics with the exact number of bars & days. I was mostly committed to 10s. Let’s see how it rolls on 2s tf.

but if one order is filled 1-2seconds after the first one maybe that can be done?

No … all open trades will be / must be closed at same time.

It’s daft really as on manual trades I can open 5 trades separately and then close 5 separately.