if I can’t live with the % amount of drawdown!

Have you checked out the definition of Drawdown as calculated and shown by PRT?

I’ll try and find my Topic I raised ages ago on Drawdown … it can be misleading?

EDIT / PS

Here we are … have a read of this …

https://www.prorealcode.com/topic/drawdown-useful-or-misleading/

Bard

BardParticipant

Master

That’s very interesting to hear that there is a difference between the demo and live and that the stops are treated differently, thanks for the heads up Dynstrom. I will have to try it live. I wish PRT would make it easy for users to switch between demo and live and access indicators and systems for both accounts instead of having to go through IG’s platform and switch using “My IG.”

Trailing Stop Type 2 killed it stone dead

You may recall me saying above? To make sure I wasn’t mistaken … I did a comparison check today.

First I duplicated a System to make all else was equal.

Attached shows variable settings for Box size = 120, RenkoType = 3, TrailingStopType = 1 (also = 0!).

- Lower curve is with TrailingStopType = 2 … code deleted.

- Upper curve is with TrailingStopType = 2 … code included.

My conclusion is that values from TrailingStopType = 2 are being used in TrailingStopType = 1 (and even = o … which should be no TrailingStop!!??) ?

Please can somebody else do tests and post your findings or confirm my findings?

Paul

PaulParticipant

Master

yes it’s off! Fifi mentioned it somewhere and I was wrong in my assumption it worked correct.

If you using two trailingstops a fix would be to make every variable different or is the problem where the once command is. I’am 100% sure. That’s the reason I went back to only 1 trailing stop. No fuss.

BardParticipant

Master

Edit:

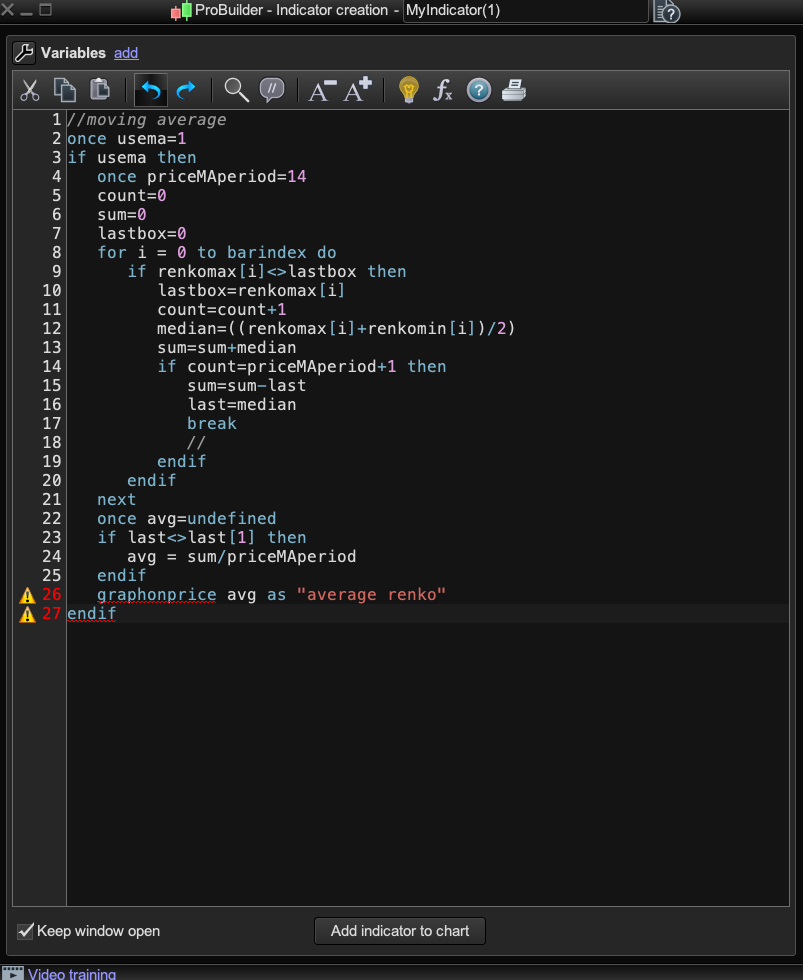

I got the original graphonprice working, thanks Paul. I also fixed it as a standalone indicator. Cheers.

//moving average

once usema=1

if usema then

once priceMAperiod=14

count=0

sum=0

lastbox=0

for i = 0 to barindex do

if renkomax[i]<>lastbox then

lastbox=renkomax[i]

count=count+1

median=((renkomax[i]+renkomin[i])/2)

sum=sum+median

if count=priceMAperiod+1 then

sum=sum-last

last=median

break

//

endif

endif

next

once avg=undefined

if last<>last[1] then

avg = sum/priceMAperiod

endif

endif

Return avg as "average renko"

BardParticipant

Master

When you wish there was a delete previous post button… 😀

This is the working Renko Moving Average Indicator:

//Renko moving average

Boxsize = 100

renkoMax = ROUND(close / boxSize) * boxSize

renkoMin = renkoMax - boxSize

once usema=1

if usema then

once priceMAperiod=10

count=0

sum=0

lastbox=0

for i = 0 to barindex do

if renkomax[i]<>lastbox then

lastbox=renkomax[i]

count=count+1

median=((renkomax[i]+renkomin[i])/2)

sum=sum+median

if count=priceMAperiod+1 then

sum=sum-last

last=median

break

//

endif

endif

next

once avg=undefined

if last<>last[1] then

avg = sum/priceMAperiod

endif

endif

Return avg coloured(255,255,0) style(line, 2) as "Renko Moving Average"

When you wish there was a delete previous post button

You can always delete all text and replace with text asking Mods to delete the blank post … if you realise within 5 minutes!? 🙂

When you wish there was a delete previous post button… 😀 This is the working Renko Moving Average Indicator:

Hi @Bard,

I applied this Renko Moving Average code to my renko code and got 100% wins with 4 trades, sl 75 and tp 175 on 1s timeframe. Not sure how it is intended to be used. I used close > avg on long positions and vice verca on short, is that how it is inteded to be used?

I used close > avg on long positions and vice verca on short, is that how it is inteded to be used?

Do you mean as an extra filter to a Renko System off this Topic?

Feel free to share the full code … we could do with something that works!? 🙂

Feel free to share the full code … we could do with something that works!? 🙂

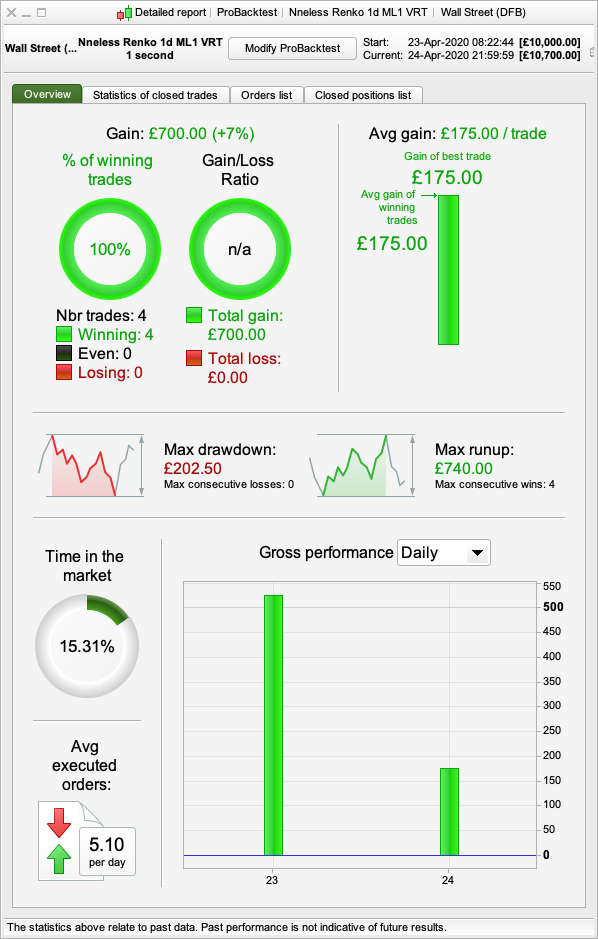

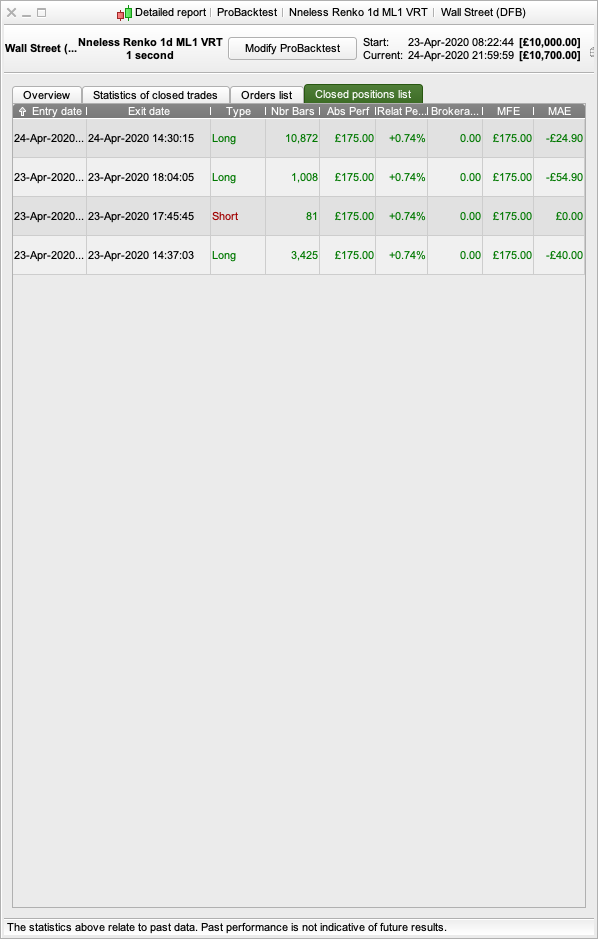

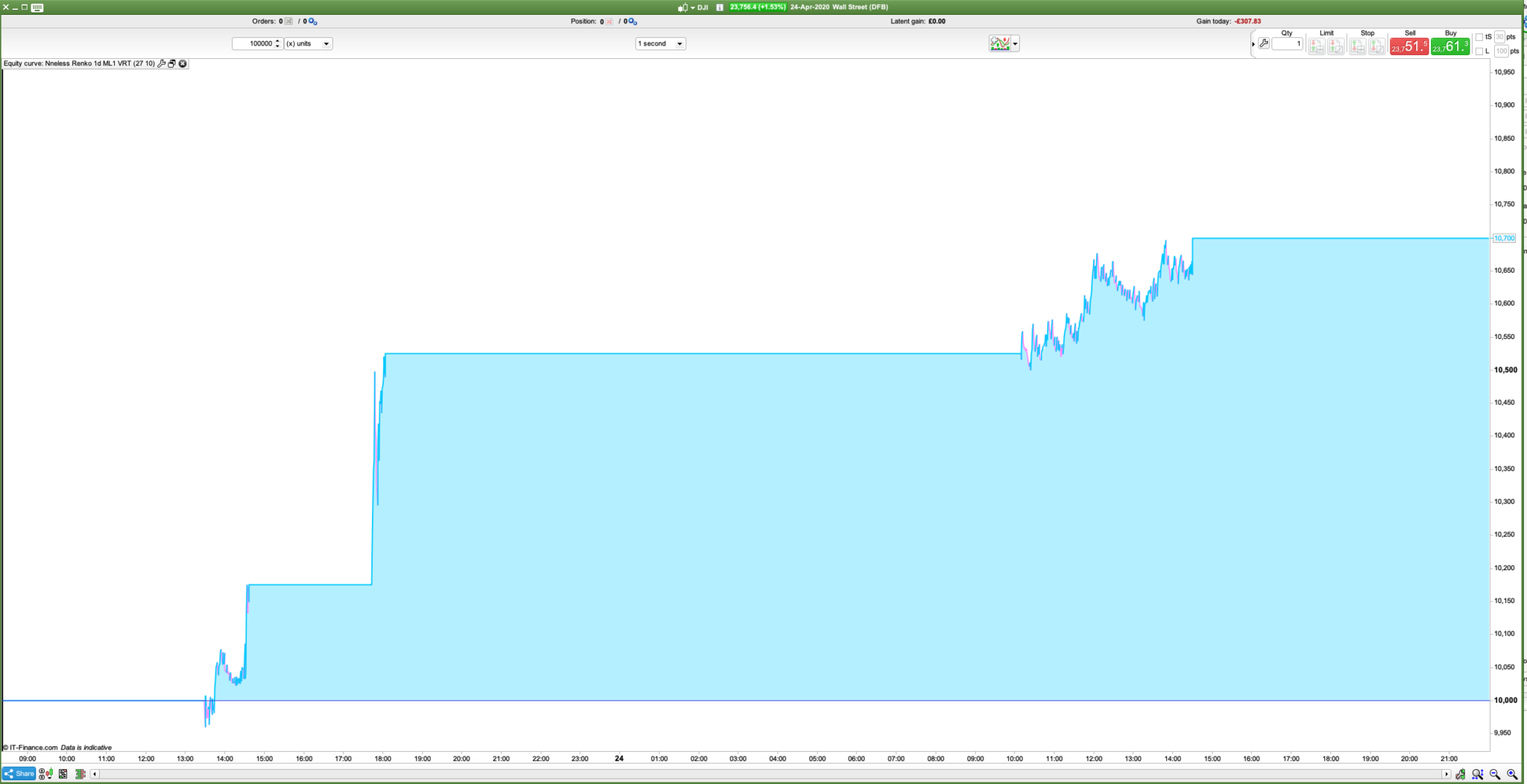

@GraHal – I don’t know if this works yet, but it looks promising from the backtest – 1s. I’m interested to see how it performs in demo/live with a higher ‘reps’ number, rather than using 2 I’m keen to see how it performs with 8 or more for the analysis of the optimum renko box size. From my observation, I can see that 50 boxsize did really well for a week, but now around 90 boxsize seems to be the right number. So from that analysis I think it doesn’t make sense to ‘optimise’ the renkobox size too often, but rather give it some time to figure out what is the correct setting for the current market movements. I might be wrong but let’s see how it performs next week.

Please note I have have run several renko strategies in backtest in demo that didn’t work out as well as it looked in the backtest. Work in progress!

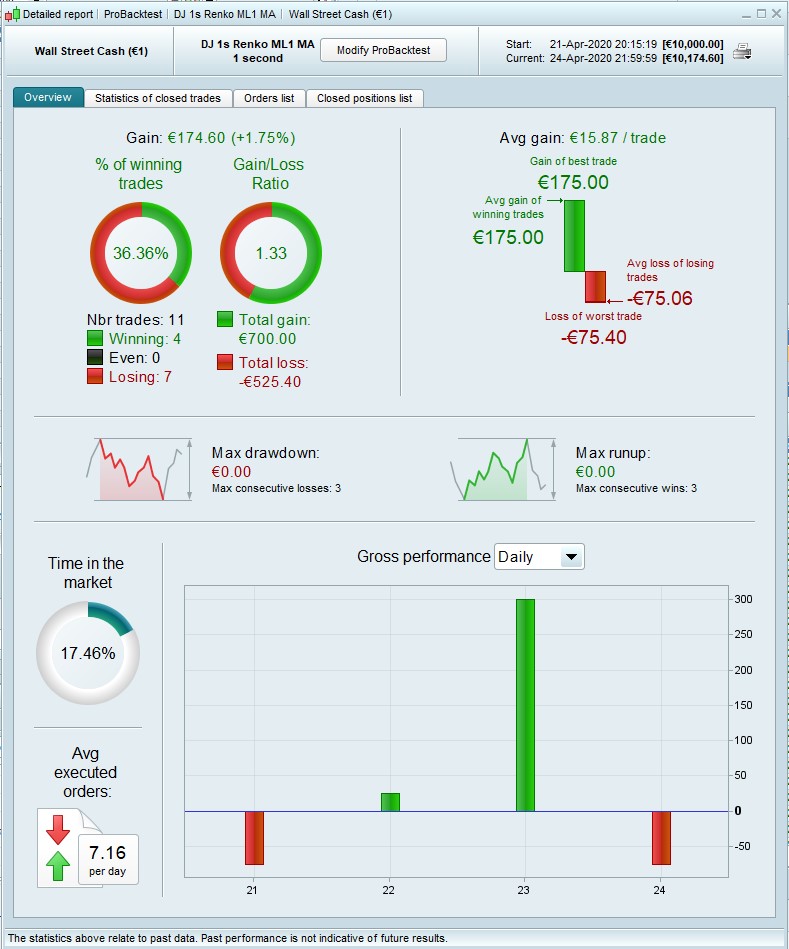

These are the backtest restulst. I don’t mind less trades per day on this timeframe, as long as the winrate is high. Let’s see how the ML algo works moving forward.I also wonder how the ML code interacts with fixed stoploss and targetprofit code rather than trailing stop and optimised sl. Maybe a fixed value helps in determining the right boxsize?

Hi @

eckaw, sadly I’m not getting anything like your results from that itf 🤔

What value are you using for pricemaperiod ?

@nonetheless

I used pricemaperiod = 10 and startingvalue=27

In the backtest the boxsize stayed at 27 as there are only 4 trades. Let’s see what the ML code does on the first optimasation. I will launch on Monday to test and will post the results here.

This is what I get, after stripping out the VRT component, which is redundant. Also removed (longonmarket or (not onmarket and tradeon)) and (shortonmarket or (not onmarket and tradeon)) from entry conditions, which belong to VRT.

Although tbh, even leaving all that in, I still couldn’t get anything like your numbers … strange.

I can see the date range is different. I. My backtest I can only access 100000 units in 1s, so 23rd + 24th. You must have 200000. I guess that’s why the results are different, startingvalue 27 was probably not working prior 23rd? I assume your boxsize would have changed from the startingvalue 27 after 8 trades?