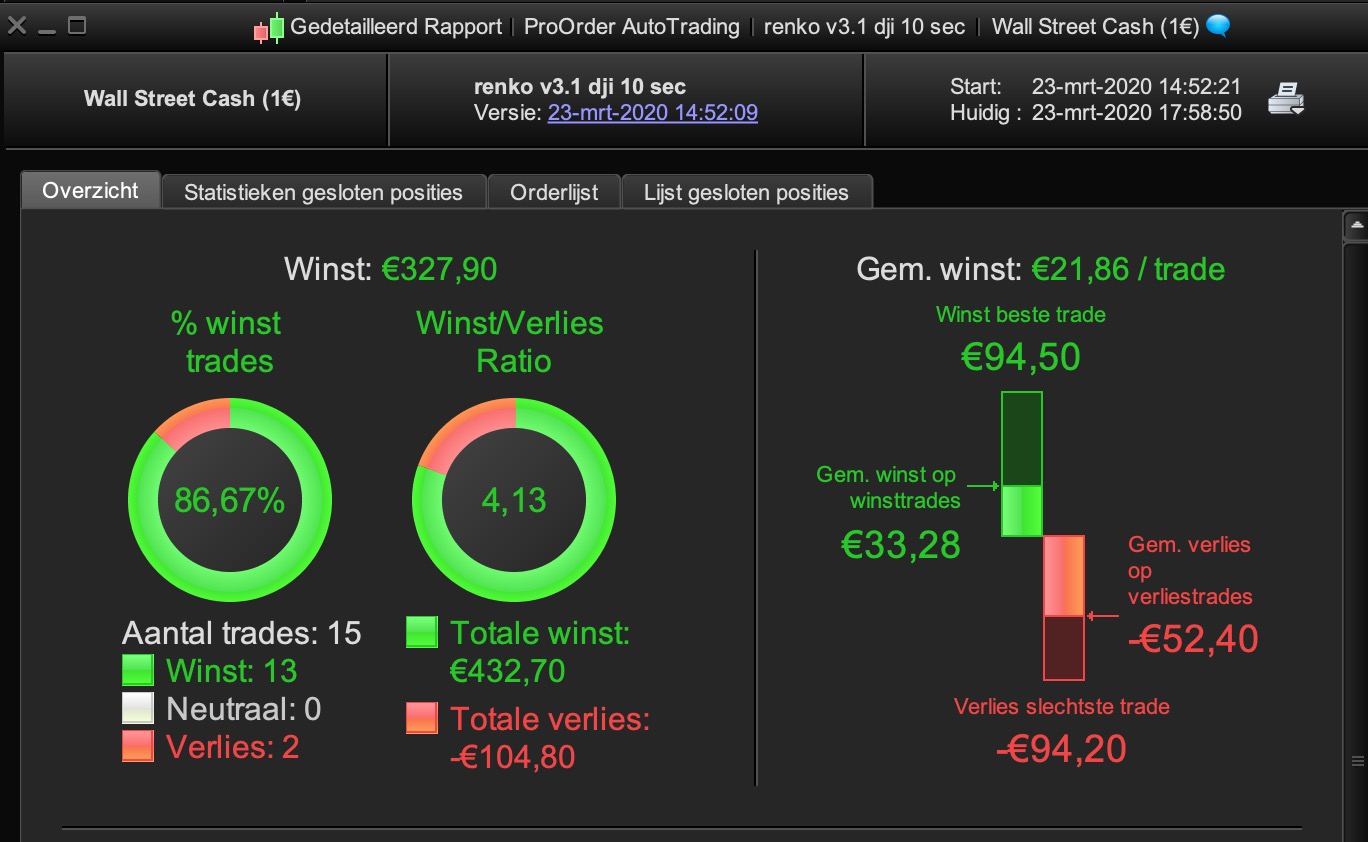

The backtest looks amazing! And I also love the 10 sec shift, it reduces the number of trades and that’s good.

The problem is still that we can’t test it on live demo, spreads only go up and up…

For the forex yes, it couldn’t be suitable because there are no “fixed spreads” like Wall Street, but having a look on some pairs, I noticed that in the 8-22 range the EURUSD is pretty solid between 0.6 and 1.2, so I think it’s the only pair where could be worth develope the strategy in the future without having to worry about spread changes.

As always, thanks for your contribution Paul 🙂

Paul

PaulParticipant

Master

no itf, only a pic to compare backengine to live demo.

the big loss of 0.5% was unfortunate, right at the top before going down.

backtest will normally be much better then demo (no spread i.e. for the exit, and live demo will be better then real.)

What do you mean by spread for the exit?

PaulParticipant

Master

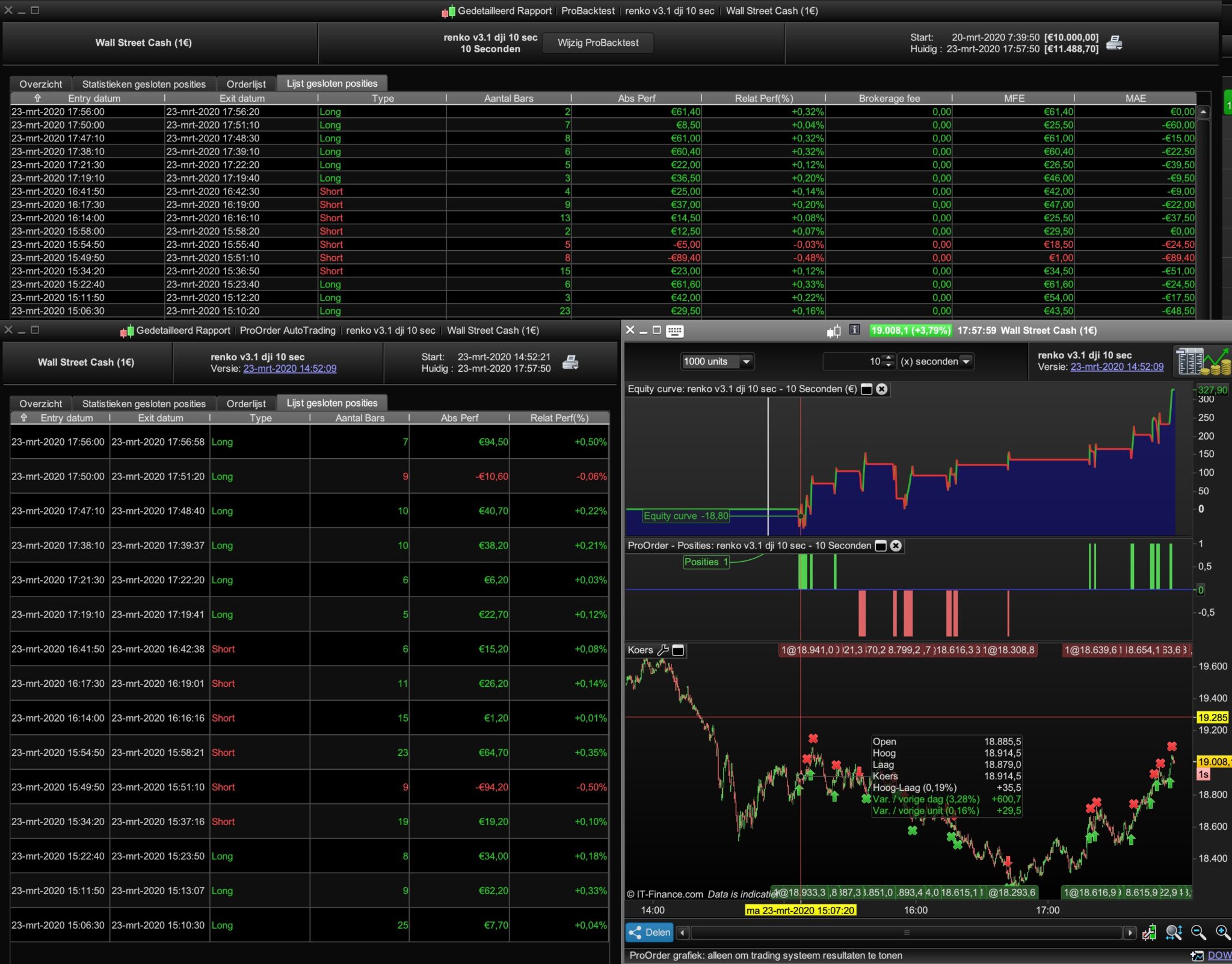

example old scenario, a profit target at 50 points. stoploss 50 points

long in the back-tester (spread at 2.8) at 19000 and goes to 19051 and goes down again. Backtest result 50 points gain.

in demo/live however, the price paid is 19003. It never reaches the 50 points gain and you go out with 50 points loss.

In my thinking, the backtest is better to be optimised on the entryprice(=orderprice with spread/slippage) I’ve set and calculated from that point for the stoploss/pt/ts. Preferably a worse price than in reality. In my backtest I never see that trade as a win, but as a loss. So that means, if I have a good backtest, it’s more likely to hold up in live trading. Does that make sense?

As result of my approach and the spread set in the backengine to 0, it does include spread/slippage (set in the code) in the orderprice and is used to calculate the exits, but not used when the exit actually happens in the backtest (because spread is set to 0)

Anyway, I don’t know, it’s just a different approach.

Sorry Paul, but putting 2.8 spread in the backtest, does not mean that he virtually consider that the position is paid at 19003 like in “real life”? If not so what is the utility of the spread box that we fill in the backtest?

PaulParticipant

Master

Bear with me, I’am poor with explaining 🙂 Not easy to put into words. Maybe wrong too!

The spreadbox is too resemble as close as possible the price paid as in live trading. But the big downside is that it ignores time and spread differences & slippage. It falls short. In live/demo you are much likely to pay more which effects everything.

Normally, if spread in the backtestengine is set to 0, you see the paid price is the open of the bar for the market order.

In above backtest long scenario, (spread 2.8, which adds +1.4 to the open price)

if criteria is reached and bought at the next bar (open=18998.6) you see in the backtest a paid price of 19000 & profit target is reached.

In demo if criteria is reached and bought at the next bar (open=18998.6) and you get 19003 as fill, no profit target is reached and get out on stoploss.

Difficult to put pro’s & cons to words. Nothing is ideal. It’s comparing what’s most comfortable/reliable.

The price you get from IG influences everything. It’s better to use your own terms.

Ok now it’s more clear, thanks for your patience 🙂

Well, to know what is the best approach, just need the normal spreads again to be able to analyze the demo performances I guess.

PaulParticipant

Master

yes much better for everyone!

Anybody got any 1 sec or 5 sec or 10 second strategies!!! hahah

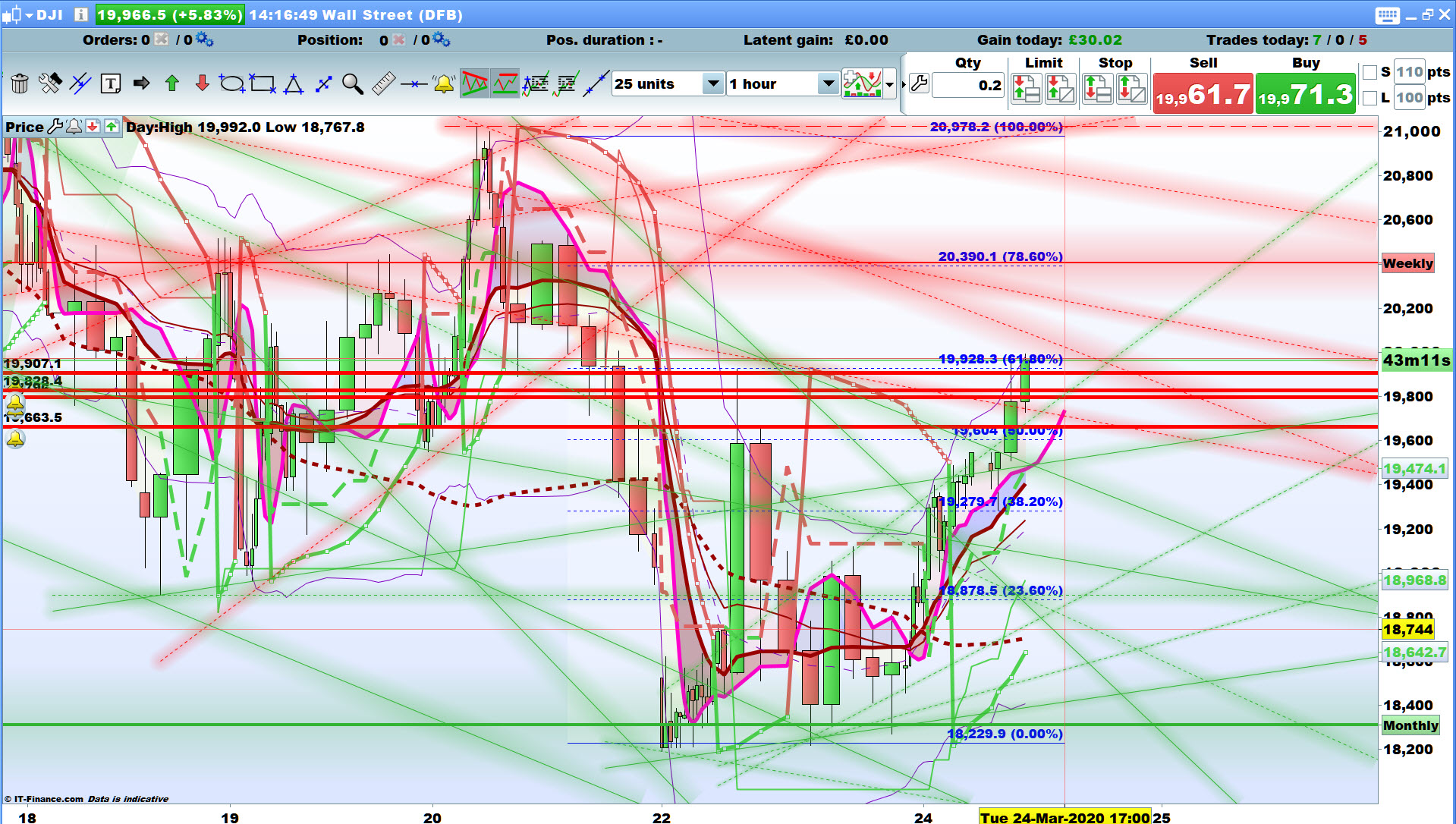

The market is always ahead of events so judging by rejection several times of monthly support at 18330 on the DJI we may have reached a bottom (IMHO) … unless there is some new disaster of course?

I have even started up my Live PRT Platform (after 2 years it being disabled) and I have been trading the 5 sec TF manually … seems a bit more predictable / sensible as each day passes?

But you know what it’s like … glued to the screen for an hour or two, then go and make a coffee and miss a big fat volume rich candle breaking a new level etc.

Sooo may as well Auto-Trade enter , watch closely and exit manually if necessary … so any strategy does not have to be a finished / perfect System! 🙂

PaulParticipant

Master

wow that chart would drive me NUTS 🙂

The trailingstop is so fast it would be hard to to beat it manually!

My experience btw is that the stoploss, using 0.5% is too big sometimes. But making it smaller doesn’t work either.

When short/long I determine the high/low for the last 12 bars on 10 second frame.

Exit is on stop.

By introducing manual closing, emotions are introduced into trading.

IMHO, emotions damage trading in an incredible way, so for this time I don’t agree with you.

An automatic system must be fully automatic, and if you want to put something manual in it, must not be the exit from positions, which is highly influenced from emotions.

Hello Paul is the V3 version file available. i m still losing with the V2 file…best regards.

Hello Paul,

Did you run your version all the week in live ?

How are the results ?

For the first time in a while DOW spread is now 5.6. Slowly coming back to normal levels…almost time to shine guys? 🙂