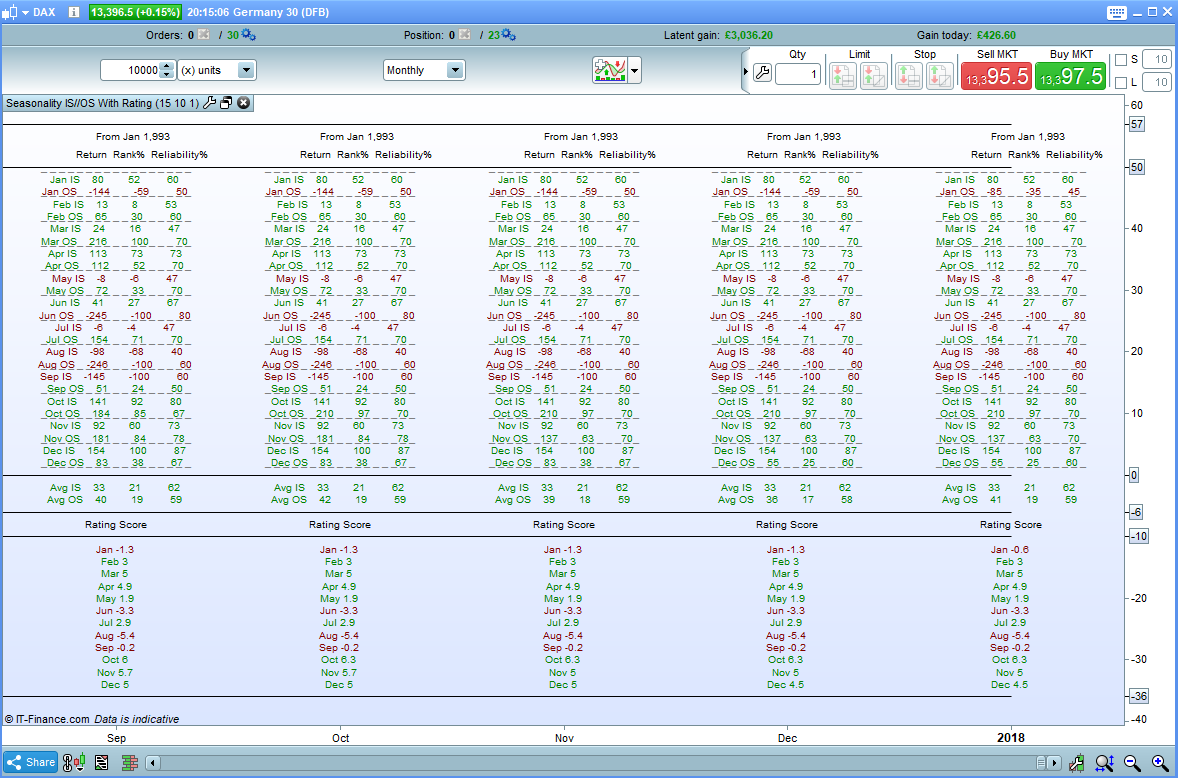

Seasonality Analysis with In Sample and Out of Sample and Monthly Rating

{kind=link}

This is a further development of my Seasonality Analysis Indicator that analyses historical data month by month to test for the seasonality of any market.

Apply only on Monthly charts.

In this version you can select a period to be tested as in sample and a period to be tested as out of sample. Comparison of the two allows more accurate analysis of the results.

You can set any number of years for each sample period but be aware that short data samples will not include much data. For example there are only five of each month in a five year sample.

You must set the current month before each test. 1 = Jan and 12 = Dec.

If you set fifteen years for the in sample and ten years for the out of sample then the analysis will start twenty five years back from today. The in sample will be tested on the first fifteen years and and the out of sample on the last ten.

The results you are interested in are the last ones under the current months candle and I suggest making the indicator window full size to make it easier to read.

The result categories are as follows:

Return: The average pips return in that month over the period tested. If you had opened a long bet at the beginning of that month and closed it at the end of that month every year then this is how much you would have gained or lost on average each month.

Rank%: The best performing monthly average return and the worst performing monthly average return are ranked at 100% and -100%. All months in between are given a ranking% relative to these. This is useful if you want to alter position sizing in a strategy month by month based on seasonality. You might want to place position size of 100% of your maximum bet size in months rated at 100% and only 33% in months rated 33% for example.

Reliability%: The number of up months and number of down months are totalled up and a reliability percentage calculated. For example if you test over 10 years and have ten tests of January and January’s results favour long positions then if 7 of those months see a gain and 3 a loss then the reliability is 70%. You may wish to only go long in months with a Reliability% of over 70% for example. This reliability% helps you decide the probability of future results matching historical results.

Rating Score: The in sample and out of sample Rank% and Reliability% are combined and converted into this score. Twice as much weight is given to the more recent out of sample data. A very low score indicates a very good month to enter short trades and a very high score a very good month to enter long trades. The rating can also be used to decide on position size and preferred trade direction for trades month by month. This rating system is unproven and will obviously vary depending on the length of sample periods chosen – so use at your discretion.

If this indicator is used alongside my other two indicators Seasonality Analysis and Seasonality Analysis Graph then any trader should be easily be able to make good decisions on when is a good time to trade long or short and whether to increase or decrease position size month by month for any market where sufficient data is available.

I advise downloading and importing the .itf file to ensure that you get full functionality.

//Seasonality Analysis In Sample and Out of Sample with Rating

//Created by Vonasi

//In Sample calculations

StartMonthIn = ThisMonth

StartYearIn = CurrentYear - (InSampleYears + OutofSampleYears)

YearInEnd = CurrentYear - OutOfSampleYears

IF OpenYear >= StartYearIn and OpenYear < YearInEnd THEN

YearFlag = 1

ELSE

YearFlag = 0

ENDIF

IF OpenMonth = StartMonthIn and OPenYear = StartYearIn THEN

MonthFlag = 1

ENDIF

IF YearFlag = 1 and MonthFlag = 1 THEN

IF OpenMonth = 1 THEN

JanTotal = JanTotal + (close - open)

JanCount = JanCount + 1

IF close > open THEN

JanUp = JanUp + 1

ENDIF

ENDIF

IF OpenMonth = 2 THEN

FebTotal = FebTotal + (close - open)

FebCount = FebCount + 1

IF close > open THEN

FebUp = FebUp + 1

ENDIF

ENDIF

IF OpenMonth = 3 THEN

MarTotal = MarTotal + (close - open)

MarCount = MarCount + 1

IF close > open THEN

MarUp = MarUp + 1

ENDIF

ENDIF

IF OpenMonth = 4 THEN

AprTotal = AprTotal + (close - open)

AprCount = AprCount + 1

IF close > open THEN

AprUp = AprUp + 1

ENDIF

ENDIF

IF OpenMonth = 5 THEN

MayTotal = MayTotal + (close - open)

MayCount = MayCount + 1

IF close > open THEN

MayUp = MayUp + 1

ENDIF

ENDIF

IF OpenMonth = 6 THEN

JunTotal = JunTotal + (close - open)

JunCount = JunCount + 1

IF close > open THEN

JunUp = JunUp + 1

ENDIF

ENDIF

IF OpenMonth = 7 THEN

JulTotal = JulTotal + (close - open)

JulCount = JulCount + 1

IF close > open THEN

JulUp = JulUp + 1

ENDIF

ENDIF

IF OpenMonth = 8 THEN

AugTotal = AugTotal + (close - open)

AugCount = AugCount + 1

IF close > open THEN

AugUp = AugUp + 1

ENDIF

ENDIF

IF OpenMonth = 9 THEN

SepTotal = SepTotal + (close - open)

SepCount = SepCount + 1

IF close > open THEN

SepUp = SepUp + 1

ENDIF

ENDIF

IF OpenMonth = 10 THEN

OctTotal = OctTotal + (close - open)

OctCount = OctCount + 1

IF close > open THEN

OctUp = OctUp + 1

ENDIF

ENDIF

IF OpenMonth = 11 THEN

NovTotal = NovTotal + (close - open)

NovCount = NovCount + 1

IF close > open THEN

NovUp = NovUp + 1

ENDIF

ENDIF

IF OpenMonth = 12 THEN

DecTotal = DecTotal + (close - open)

DecCount = DecCount + 1

IF close > open THEN

DecUp = DecUp + 1

ENDIF

ENDIF

ENDIF

Jan = Round(JanTotal/JanCount)

Feb = Round(FebTotal/FebCount)

Mar = Round(MarTotal/MarCount)

Apr = Round(AprTotal/AprCount)

May = Round(MayTotal/MayCount)

Jun = Round(JunTotal/JunCount)

Jul = Round(JulTotal/JulCount)

Aug = Round(AugTotal/AugCount)

Sep = Round(SepTotal/SepCount)

Oct = Round(OctTotal/OctCount)

Nov = Round(NovTotal/NovCount)

Dec = Round(DecTotal/DecCount)

IF Jan > 0 THEN

JanR = 0

JanG = 128

JanRel = Round((JanUp/JanCount)*100)

JanRelScore = JanRel

ELSE

JanR = 128

JanG = 0

JanRel = Round(((JanCount - JanUp)/JanCount)*100)

JanRelScore = (0 - JanRel)

ENDIF

IF Feb > 0 THEN

FebR = 0

FebG = 128

FebRel = Round((FebUp/FebCount)*100)

FebRelScore = FebRel

ELSE

FebR = 128

FebG = 0

FebRel = Round(((FebCount - FebUp)/FebCount)*100)

FebRelScore = (0 - FebRel)

ENDIF

IF Mar > 0 THEN

MarR = 0

MarG = 128

MarRel = Round((MarUp/MarCount)*100)

MarRelScore = MarRel

ELSE

MarR = 128

MarG = 0

MarRel = Round(((MarCount - MarUp)/MarCount)*100)

MarRelScore = (0 - MarRel)

ENDIF

IF Apr > 0 THEN

AprR = 0

AprG = 128

AprRel = Round((AprUp/AprCount)*100)

AprRelScore = AprRel

ELSE

AprR = 128

AprG = 0

AprRel = Round(((AprCount - AprUp)/AprCount)*100)

AprRelScore = (0 - AprRel)

ENDIF

IF May > 0 THEN

MayR = 0

MayG = 128

MayRel = Round((MayUp/MayCount)*100)

MayRelScore = MayRel

ELSE

MayR = 128

MayG = 0

MayRel = Round(((MayCount - MayUp)/MayCount)*100)

MayRelScore = (0 - MayRel)

ENDIF

IF Jun > 0 THEN

JunR = 0

JunG = 128

JunRel = Round((JunUp/JunCount)*100)

JunRelScore = JunRel

ELSE

JunR = 128

JunG = 0

JunRel = Round(((JunCount - JunUp)/JunCount)*100)

JunRelScore = (0 - JunRel)

ENDIF

IF Jul > 0 THEN

JulR = 0

JulG = 128

JulRel = Round((JulUp/JulCount)*100)

JulRelScore = JulRel

ELSE

JulR = 128

JulG = 0

JulRel = Round(((JulCount - JulUp)/JulCount)*100)

JulRelScore = (0 - JulRel)

ENDIF

IF Aug > 0 THEN

AugR = 0

AugG = 128

AugRel = Round((AugUp/AugCount)*100)

AugRelScore = AugRel

ELSE

AugR = 128

AugG = 0

AugRel = Round(((AugCount - AugUp)/AugCount)*100)

AugRelScore = (0 - AugRel)

ENDIF

IF Sep > 0 THEN

SepR = 0

SepG = 128

SepRel = Round((SepUp/SepCount)*100)

SepRelScore = SepRel

ELSE

SepR = 128

SepG = 0

SepRel = Round(((SepCount - SepUp)/SepCount)*100)

SepRelScore = (0 - SepRel)

ENDIF

IF Oct > 0 THEN

OctR = 0

OctG = 128

OctRel = Round((OctUp/OctCount)*100)

OctRelScore = OctRel

ELSE

OctR = 128

OctG = 0

OctRel = Round(((OctCount - OctUp)/OctCount)*100)

OctRelScore = (0 - OctRel)

ENDIF

IF Nov > 0 THEN

NovR = 0

NovG = 128

NovRel = Round((NovUp/NovCount)*100)

NovRelScore = NovRel

ELSE

NovR = 128

NovG = 0

NovRel = Round(((NovCount - NovUp)/NovCount)*100)

NovRelScore = (0 - NovRel)

ENDIF

IF Dec > 0 THEN

DecR = 0

DecG = 128

DecRel = Round((DecUp/DecCount)*100)

DecRelScore = DecRel

ELSE

DecR = 128

DecG = 0

DecRel = Round(((DecCount - DecUp)/DecCount)*100)

DecRelScore = (0 - DecRel)

ENDIF

Avg = Round((Jan + Feb + Mar + Apr + May + Jun + Jul + Aug + Sep + Oct + Nov + Dec)/12)

AvgCount = (JanCount + FebCount + MarCount + AprCount + MayCount + JunCount + JulCount + AugCount + SepCount + OctCount + NovCount + DecCount)

AvgUp = (JanUp + FebUp + MarUp + AprUp + MayUp + JunUp + JulUp + AugUp + SepUp + OctUp + NovUp + DecUp)

IF Avg > 0 THEN

AvgR = 0

AvgG = 128

AvgRel = Round((AvgUp/AvgCount)*100)

ELSE

AvgR = 128

AvgG = 0

AvgRel = Round(((AvgCount - AvgUp)/AvgCount)*100)

ENDIF

Bottom = Min(Dec,Min(Nov,Min(Oct,Min(Sep,Min(Aug,Min(Jul,Min(Jun,Min(May,Min(Apr,Min(Mar,MIN(Feb,Jan)))))))))))

Top = Max(Dec,Max(Nov,Max(Oct,Max(Sep,Max(Aug,Max(Jul,Max(Jun,Max(May,Max(Apr,Max(Mar,Max(Feb,Jan)))))))))))

IF Jan > 0 THEN

JanPerc = Round((Jan/Top)*100)

ELSE

JanPerc = 0 - Round((ABS(Jan)/ABS(Bottom))*100)

ENDIF

IF Feb > 0 THEN

FebPerc = Round((Feb/Top)*100)

ELSE

FebPerc = 0 - Round((ABS(Feb)/ABS(Bottom))*100)

ENDIF

IF Mar > 0 THEN

MarPerc = Round((Mar/Top)*100)

ELSE

MarPerc = 0 - Round((ABS(Mar)/ABS(Bottom))*100)

ENDIF

IF Apr > 0 THEN

AprPerc = Round((Apr/Top)*100)

ELSE

AprPerc = 0 - Round((ABS(Apr)/ABS(Bottom))*100)

ENDIF

IF May > 0 THEN

MayPerc = Round((May/Top)*100)

ELSE

MayPerc = 0 - Round((ABS(May)/ABS(Bottom))*100)

ENDIF

IF Jun > 0 THEN

JunPerc = Round((Jun/Top)*100)

ELSE

JunPerc = 0 - Round((ABS(Jun)/ABS(Bottom))*100)

ENDIF

IF Jul > 0 THEN

JulPerc = Round((Jul/Top)*100)

ELSE

JulPerc = 0 - Round((ABS(Jul)/ABS(Bottom))*100)

ENDIF

IF Aug > 0 THEN

AugPerc = Round((Aug/Top)*100)

ELSE

AugPerc = 0 - Round((ABS(Aug)/ABS(Bottom))*100)

ENDIF

IF Sep > 0 THEN

SepPerc = Round((Sep/Top)*100)

ELSE

SepPerc = 0 - Round((ABS(Sep)/ABS(Bottom))*100)

ENDIF

IF Oct > 0 THEN

OctPerc = Round((Oct/Top)*100)

ELSE

OctPerc = 0 - Round((ABS(Oct)/ABS(Bottom))*100)

ENDIF

IF Nov > 0 THEN

NovPerc = Round((Nov/Top)*100)

ELSE

NovPerc = 0 - Round((ABS(Nov)/ABS(Bottom))*100)

ENDIF

IF Dec > 0 THEN

DecPerc = Round((Dec/Top)*100)

ELSE

DecPerc = 0 - Round((ABS(Dec)/ABS(Bottom))*100)

ENDIF

IF Avg > 0 THEN

AvgPerc = Round((Avg/Top)*100)

ELSE

AvgPerc = 0 - Round((ABS(Avg)/ABS(Bottom))*100)

ENDIF

//Out of Sample Calculations

StartMonthOut = ThisMonth

StartYearOut = CurrentYear - OutOfSampleYears

IF OpenYear = StartYearOut and OpenMonth = StartMonthOut THEN

OutFlag = 1

ENDIF

IF OutFlag = 1 THEN

IF OpenMonth = 1 THEN

JanOutTotal = JanOutTotal + (close - open)

JanOutCount = JanOutCount + 1

IF close > open THEN

JanOutUp = JanOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 2 THEN

FebOutTotal = FebOutTotal + (close - open)

FebOutCount = FebOutCount + 1

IF close > open THEN

FebOutUp = FebOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 3 THEN

MarOutTotal = MarOutTotal + (close - open)

MarOutCount = MarOutCount + 1

IF close > open THEN

MarOutUp = MarOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 4 THEN

AprOutTotal = AprOutTotal + (close - open)

AprOutCount = AprOutCount + 1

IF close > open THEN

AprOutUp = AprOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 5 THEN

MayOutTotal = MayOutTotal + (close - open)

MayOutCount = MayOutCount + 1

IF close > open THEN

MayOutUp = MayOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 6 THEN

JunOutTotal = JunOutTotal + (close - open)

JunOutCount = JunOutCount + 1

IF close > open THEN

JunOutUp = JunOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 7 THEN

JulOutTotal = JulOutTotal + (close - open)

JulOutCount = JulOutCount + 1

IF close > open THEN

JulOutUp = JulOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 8 THEN

AugOutTotal = AugOutTotal + (close - open)

AugOutCount = AugOutCount + 1

IF close > open THEN

AugOutUp = AugOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 9 THEN

SepOutTotal = SepOutTotal + (close - open)

SepOutCount = SepOutCount + 1

IF close > open THEN

SepOutUp = SepOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 10 THEN

OctOutTotal = OctOutTotal + (close - open)

OctOutCount = OctOutCount + 1

IF close > open THEN

OctOutUp = OctOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 11 THEN

NovOutTotal = NovOutTotal + (close - open)

NovOutCount = NovOutCount + 1

IF close > open THEN

NovOutUp = NovOutUp + 1

ENDIF

ENDIF

IF OpenMonth = 12 THEN

DecOutTotal = DecOutTotal + (close - open)

DecOutCount = DecOutCount + 1

IF close > open THEN

DecOutUp = DecOutUp + 1

ENDIF

ENDIF

ENDIF

JanOut = Round(JanOutTotal/JanOutCount)

FebOut = Round(FebOutTotal/FebOutCount)

MarOut = Round(MarOutTotal/MarOutCount)

AprOut = Round(AprOutTotal/AprOutCount)

MayOut = Round(MayOutTotal/MayOutCount)

JunOut = Round(JunOutTotal/JunOutCount)

JulOut = Round(JulOutTotal/JulOutCount)

AugOut = Round(AugOutTotal/AugOutCount)

SepOut = Round(SepOutTotal/SepOutCount)

OctOut = Round(OctOutTotal/OctOutCount)

NovOut = Round(NovOutTotal/NovOutCount)

DecOut = Round(DecOutTotal/DecOutCount)

IF JanOut > 0 THEN

JanOutR = 0

JanOutG = 128

JanOutRel = Round((JanOutUp/JanOutCount)*100)

JanOutRelScore = JanOutRel

ELSE

JanOutR = 128

JanOutG = 0

JanOutRel = Round(((JanOutCount - JanOutUp)/JanOutCount)*100)

JanOutRelScore = (0 - JanOutRel)

ENDIF

IF FebOut > 0 THEN

FebOutR = 0

FebOutG = 128

FebOutRel = Round((FebOutUp/FebOutCount)*100)

FebOutRelScore = FebOutRel

ELSE

FebOutR = 128

FebOutG = 0

FebOutRel = Round(((FebOutCount - FebOutUp)/FebOutCount)*100)

FebOutRelScore = (0 - FebOutRel)

ENDIF

IF MarOut > 0 THEN

MarOutR = 0

MarOutG = 128

MarOutRel = Round((MarOutUp/MarOutCount)*100)

MarOutRelScore = MarOutRel

ELSE

MarOutR = 128

MarOutG = 0

MarOutRel = Round(((MarOutCount - MarOutUp)/MarOutCount)*100)

MarOutRelScore = (0 - MarOutRel)

ENDIF

IF AprOut > 0 THEN

AprOutR = 0

AprOutG = 128

AprOutRel = Round((AprOutUp/AprOutCount)*100)

AprOutRelScore = AprOutRel

ELSE

AprOutR = 128

AprOutG = 0

AprOutRel = Round(((AprOutCount - AprOutUp)/AprOutCount)*100)

AprOutRelScore = (0 - AprOutRel)

ENDIF

IF MayOut > 0 THEN

MayOutR = 0

MayOutG = 128

MayOutRel = Round((MayOutUp/MayOutCount)*100)

MayOutRelScore = MayOutRel

ELSE

MayOutR = 128

MayOutG = 0

MayOutRel = Round(((MayOutCount - MayOutUp)/MayOutCount)*100)

MayOutRelScore = (0 - MayOutRel)

ENDIF

IF JunOut > 0 THEN

JunOutR = 0

JunOutG = 128

JunOutRel = Round((JunOutUp/JunOutCount)*100)

JunOutRelScore = JunOutRel

ELSE

JunOutR = 128

JunOutG = 0

JunOutRel = Round(((JunOutCount - JunOutUp)/JunOutCount)*100)

JunOutRelScore = (0 - JunOutRel)

ENDIF

IF JulOut > 0 THEN

JulOutR = 0

JulOutG = 128

JulOutRel = Round((JulOutUp/JulOutCount)*100)

JulOutRelScore = JulOutRel

ELSE

JulOutR = 128

JulOutG = 0

JulOutRel = Round(((JulOutCount - JulOutUp)/JulOutCount)*100)

JulOutRelScore = (0 - JulOutRel)

ENDIF

IF AugOut > 0 THEN

AugOutR = 0

AugOutG = 128

AugOutRel = Round((AugOutUp/AugOutCount)*100)

AugOutRelScore = AugOutRel

ELSE

AugOutR = 128

AugOutG = 0

AugOutRel = Round(((AugOutCount - AugOutUp)/AugOutCount)*100)

AugOutRelScore = (0 - AugOutRel)

ENDIF

IF SepOut > 0 THEN

SepOutR = 0

SepOutG = 128

SepOutRel = Round((SepOutUp/SepOutCount)*100)

SepOutRelScore = SepOutRel

ELSE

SepOutR = 128

SepOutG = 0

SepOutRel = Round(((SepOutCount - SepOutUp)/SepOutCount)*100)

SepOutRelScore = (0 - SepOutRel)

ENDIF

IF OctOut > 0 THEN

OctOutR = 0

OctOutG = 128

OctOutRel = Round((OctOutUp/OctOutCount)*100)

OctOutRelScore = OctOutRel

ELSE

OctOutR = 128

OctOutG = 0

OctOutRel = Round(((OctOutCount - OctOutUp)/OctOutCount)*100)

OctOutRelScore = (0 - OctOutRel)

ENDIF

IF NovOut > 0 THEN

NovOutR = 0

NovOutG = 128

NovOutRel = Round((NovOutUp/NovOutCount)*100)

NovOutRelScore = NovOutRel

ELSE

NovOutR = 128

NovOutG = 0

NovOutRel = Round(((NovOutCount - NovOutUp)/NovOutCount)*100)

NovOutRelScore = (0 - NovOutRel)

ENDIF

IF DecOut > 0 THEN

DecOutR = 0

DecOutG = 128

DecOutRel = Round((DecOutUp/DecOutCount)*100)

DecOutRelScore = DecOutRel

ELSE

DecOutR = 128

DecOutG = 0

DecOutRel = Round(((DecOutCount - DecOutUp)/DecOutCount)*100)

DecOutRelScore = (0 - DecOutRel)

ENDIF

AvgOut = Round((JanOut + FebOut + MarOut + AprOut + MayOut + JunOut + JulOut + AugOut + SepOut + OctOut + NovOut + DecOut)/12)

AvgOutCount = (JanOutCount + FebOutCount + MarOutCount + AprOutCount + MayOutCount + JunOutCount + JulOutCount + AugOutCount + SepOutCount + OctOutCount + NovOutCount + DecOutCount)

AvgOutUp = (JanOutUp + FebOutUp + MarOutUp + AprOutUp + MayOutUp + JunOutUp + JulOutUp + AugOutUp + SepOutUp + OctOutUp + NovOutUp + DecOutUp)

IF AvgOut > 0 THEN

AvgOutR = 0

AvgOutG = 128

AvgOutRel = Round((AvgOutUp/AvgOutCount)*100)

ELSE

AvgOutR = 128

AvgOutG = 0

AvgOutRel = Round(((AvgOutCount - AvgOutUp)/AvgOutCount)*100)

ENDIF

BottomOut = Min(DecOut,Min(NovOut,Min(OctOut,Min(SepOut,Min(AugOut,Min(JulOut,Min(JunOut,Min(MayOut,Min(AprOut,Min(MarOut,MIN(FebOut,JanOut)))))))))))

TopOut = Max(DecOut,Max(NovOut,Max(OctOut,Max(SepOut,Max(AugOut,Max(JulOut,Max(JunOut,Max(MayOut,Max(AprOut,Max(MarOut,Max(FebOut,JanOut)))))))))))

IF JanOut > 0 THEN

JanOutPerc = Round((JanOut/TopOut)*100)

ELSE

JanOutPerc = 0 - Round((ABS(JanOut)/ABS(BottomOut))*100)

ENDIF

IF FebOut > 0 THEN

FebOutPerc = Round((FebOut/TopOut)*100)

ELSE

FebOutPerc = 0 - Round((ABS(FebOut)/ABS(BottomOut))*100)

ENDIF

IF MarOut > 0 THEN

MarOutPerc = Round((MarOut/TopOut)*100)

ELSE

MarOutPerc = 0 - Round((ABS(MarOut)/ABS(BottomOut))*100)

ENDIF

IF AprOut > 0 THEN

AprOutPerc = Round((AprOut/TopOut)*100)

ELSE

AprOutPerc = 0 - Round((ABS(AprOut)/ABS(BottomOut))*100)

ENDIF

IF MayOut > 0 THEN

MayOutPerc = Round((MayOut/TopOut)*100)

ELSE

MayOutPerc = 0 - Round((ABS(MayOut)/ABS(BottomOut))*100)

ENDIF

IF JunOut > 0 THEN

JunOutPerc = Round((JunOut/TopOut)*100)

ELSE

JunOutPerc = 0 - Round((ABS(JunOut)/ABS(BottomOut))*100)

ENDIF

IF JulOut > 0 THEN

JulOutPerc = Round((JulOut/TopOut)*100)

ELSE

JulOutPerc = 0 - Round((ABS(JulOut)/ABS(BottomOut))*100)

ENDIF

IF AugOut > 0 THEN

AugOutPerc = Round((AugOut/TopOut)*100)

ELSE

AugOutPerc = 0 - Round((ABS(AugOut)/ABS(BottomOut))*100)

ENDIF

IF SepOut > 0 THEN

SepOutPerc = Round((SepOut/TopOut)*100)

ELSE

SepOutPerc = 0 - Round((ABS(SepOut)/ABS(BottomOut))*100)

ENDIF

IF OctOut > 0 THEN

OctOutPerc = Round((OctOut/TopOut)*100)

ELSE

OctOutPerc = 0 - Round((ABS(OctOut)/ABS(BottomOut))*100)

ENDIF

IF NovOut > 0 THEN

NovOutPerc = Round((NovOut/TopOut)*100)

ELSE

NovOutPerc = 0 - Round((ABS(NovOut)/ABS(BottomOut))*100)

ENDIF

IF DecOut > 0 THEN

DecOutPerc = Round((DecOut/TopOut)*100)

ELSE

DecOutPerc = 0 - Round((ABS(DecOut)/ABS(BottomOut))*100)

ENDIF

IF AvgOut > 0 THEN

AvgOutPerc = Round((AvgOut/TopOut)*100)

ELSE

AvgOutPerc = 0 - Round((ABS(AvgOut)/ABS(BottomOut))*100)

ENDIF

//Rating Calculations

JanScore = Round((((((JanPerc/2) + JanOutPerc)/2) + (((JanRelScore/2) + JanOutRelScore)/2))/20)*10)/10

FebScore = Round((((((FebPerc/2) + FebOutPerc)/2) + (((FebRelScore/2) + FebOutRelScore)/2))/20)*10)/10

MarScore = Round((((((MarPerc/2) + MarOutPerc)/2) + (((MarRelScore/2) + MarOutRelScore)/2))/20)*10)/10

AprScore = Round((((((AprPerc/2) + AprOutPerc)/2) + (((AprRelScore/2) + AprOutRelScore)/2))/20)*10)/10

MayScore = Round((((((MayPerc/2) + MayOutPerc)/2) + (((MayRelScore/2) + MayOutRelScore)/2))/20)*10)/10

JunScore = Round((((((JunPerc/2) + JunOutPerc)/2) + (((JunRelScore/2) + JunOutRelScore)/2))/20)*10)/10

JulScore = Round((((((JulPerc/2) + JulOutPerc)/2) + (((JulRelScore/2) + JulOutRelScore)/2))/20)*10)/10

AugScore = Round((((((AugPerc/2) + AugOutPerc)/2) + (((AugRelScore/2) + AugOutRelScore)/2))/20)*10)/10

SepScore = Round((((((SepPerc/2) + SepOutPerc)/2) + (((SepRelScore/2) + SepOutRelScore)/2))/20)*10)/10

OctScore = Round((((((OctPerc/2) + OctOutPerc)/2) + (((OctRelScore/2) + OctOutRelScore)/2))/20)*10)/10

NovScore = Round((((((NovPerc/2) + NovOutPerc)/2) + (((NovRelScore/2) + NovOutRelScore)/2))/20)*10)/10

DecScore = Round((((((DecPerc/2) + DecOutPerc)/2) + (((DecRelScore/2) + DecOutRelScore)/2))/20)*10)/10

IF JanScore > 0 THEN

JanScoreR = 0

JanScoreG = 128

ELSE

JanScoreR = 128

JanScoreG = 0

ENDIF

IF FebScore > 0 THEN

FebScoreR = 0

FebScoreG = 128

ELSE

FebScoreR = 128

FebScoreG = 0

ENDIF

IF MarScore > 0 THEN

MarScoreR = 0

MarScoreG = 128

ELSE

MarScoreR = 128

MarScoreG = 0

ENDIF

IF AprScore > 0 THEN

AprScoreR = 0

AprScoreG = 128

ELSE

AprScoreR = 128

AprScoreG = 0

ENDIF

IF MayScore > 0 THEN

MayScoreR = 0

MayScoreG = 128

ELSE

MayScoreR = 128

MayScoreG = 0

ENDIF

IF JunScore > 0 THEN

JunScoreR = 0

JunScoreG = 128

ELSE

JunScoreR = 128

JunScoreG = 0

ENDIF

IF JulScore > 0 THEN

JulScoreR = 0

JulScoreG = 128

ELSE

JulScoreR = 128

JulScoreG = 0

ENDIF

IF AugScore > 0 THEN

AugScoreR = 0

AugScoreG = 128

ELSE

AugScoreR = 128

AugScoreG = 0

ENDIF

IF SepScore > 0 THEN

SepScoreR = 0

SepScoreG = 128

ELSE

SepScoreR = 128

SepScoreG = 0

ENDIF

IF OctScore > 0 THEN

OctScoreR = 0

OctScoreG = 128

ELSE

OctScoreR = 128

OctScoreG = 0

ENDIF

IF NovScore > 0 THEN

NovScoreR = 0

NovScoreG = 128

ELSE

NovScoreR = 128

NovScoreG = 0

ENDIF

IF DecScore > 0 THEN

DecScoreR = 0

DecScoreG = 128

ELSE

DecScoreR = 128

DecScoreG = 0

ENDIF

//Text

IF StartMonthIn = 1 THEN

DrawText(" From Jan #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 2 THEN

DrawText(" From Feb #StartYearIn#" ,barindex,15.5,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 3 THEN

DrawText(" From Mar #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 4 THEN

DrawText(" From Apr #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 5 THEN

DrawText(" From May #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 6 THEN

DrawText(" From Jun #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 7 THEN

DrawText(" From Jul #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 8 THEN

DrawText(" From Aug #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 9 THEN

DrawText(" From Sep #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 10 THEN

DrawText(" From Oct #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 11 THEN

DrawText(" From Nov #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

IF StartMonthIn = 12 THEN

DrawText(" From Dec #StartYearIn#",barindex,55,SansSerif,Standard,10)coloured(0,0,0)

ENDIF

DrawText(" Return Rank% Reliability%",barindex,52,SansSerif,Standard,10)coloured(0,0,0)

DrawText("Jan IS #Jan# #JanPerc# #JanRel#",barindex,48,SansSerif,Standard,10)coloured(JanR,JanG,0)

DrawText("Feb IS #Feb# #FebPerc# #FebRel#",barindex,44,SansSerif,Standard,10)coloured(FebR,FebG,0)

DrawText("Mar IS #Mar# #MarPerc# #MarRel#",barindex,40,SansSerif,Standard,10)coloured(MarR,MarG,0)

DrawText("Apr IS #Apr# #AprPerc# #AprRel#",barindex,36,SansSerif,Standard,10)coloured(AprR,AprG,0)

DrawText("May IS #May# #MayPerc# #MayRel#",barindex,32,SansSerif,Standard,10)coloured(MayR,MayG,0)

DrawText("Jun IS #Jun# #JunPerc# #JunRel#",barindex,28,SansSerif,Standard,10)coloured(JunR,JunG,0)

DrawText("Jul IS #Jul# #JulPerc# #JulRel#",barindex,24,SansSerif,Standard,10)coloured(JulR,JulG,0)

DrawText("Aug IS #Aug# #AugPerc# #AugRel#",barindex,20,SansSerif,Standard,10)coloured(AugR,AugG,0)

DrawText("Sep IS #Sep# #SepPerc# #SepRel#",barindex,16,SansSerif,Standard,10)coloured(SepR,SepG,0)

DrawText("Oct IS #Oct# #OctPerc# #OctRel#",barindex,12,SansSerif,Standard,10)coloured(OctR,OctG,0)

DrawText("Nov IS #Nov# #NovPerc# #NovRel#",barindex,8,SansSerif,Standard,10)coloured(NovR,NovG,0)

DrawText("Dec IS #Dec# #DecPerc# #DecRel#",barindex,4,SansSerif,Standard,10)coloured(DecR,DecG,0)

DrawText("Avg IS #Avg# #AvgPerc# #AvgRel#",barindex,-2,SansSerif,Standard,10)coloured(AvgR,AvgG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,50,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Jan OS #JanOut# #JanOutPerc# #JanOutRel#",barindex,46,SansSerif,Standard,10)coloured(JanOutR,JanOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,46,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Feb OS #FebOut# #FebOutPerc# #FebOutRel#",barindex,42,SansSerif,Standard,10)coloured(FebOutR,FebOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,42,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Mar OS #MarOut# #MarOutPerc# #MarOutRel#",barindex,38,SansSerif,Standard,10)coloured(MarOutR,MarOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,38,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Apr OS #AprOut# #AprOutPerc# #AprOutRel#",barindex,34,SansSerif,Standard,10)coloured(AprOutR,AprOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,34,SansSerif,Standard,10)coloured(128,128,128)

DrawText("May OS #MayOut# #MayOutPerc# #MayOutRel#",barindex,30,SansSerif,Standard,10)coloured(MayOutR,MayOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,30,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Jun OS #JunOut# #JunOutPerc# #JunOutRel#",barindex,26,SansSerif,Standard,10)coloured(JunOutR,JunOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,26,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Jul OS #JulOut# #JulOutPerc# #JulOutRel#",barindex,22,SansSerif,Standard,10)coloured(JulOutR,JulOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,22,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Aug OS #AugOut# #AugOutPerc# #AugOutRel#",barindex,18,SansSerif,Standard,10)coloured(AugOutR,AugOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,18,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Sep OS #SepOut# #SepOutPerc# #SepOutRel#",barindex,14,SansSerif,Standard,10)coloured(SepOutR,SepOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,14,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Oct OS #OctOut# #OctOutPerc# #OctOutRel#",barindex,10,SansSerif,Standard,10)coloured(OctOutR,OctOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,10,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Nov OS #NovOut# #NovOutPerc# #NovOutRel#",barindex,6,SansSerif,Standard,10)coloured(NovOutR,NovOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,6,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Dec OS #DecOut# #DecOutPerc# #DecOutRel#",barindex,2,SansSerif,Standard,10)coloured(DecOutR,DecOutG,0)

DrawText("_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _",barindex,2,SansSerif,Standard,10)coloured(128,128,128)

DrawText("Avg OS #AvgOut# #AvgOutPerc# #AvgOutRel#",barindex,-4,SansSerif,Standard,10)coloured(AvgOutR,AvgOutG,0)

DrawText("Rating Score",barindex,-8,SansSerif,Standard,10)coloured(0,0,0)

DrawText("Jan #JanScore#",barindex,-12,SansSerif,Standard,10)coloured(JanScoreR,JanScoreG,0)

DrawText("Feb #FebScore#",barindex,-14,SansSerif,Standard,10)coloured(FebScoreR,FebScoreG,0)

DrawText("Mar #MarScore#",barindex,-16,SansSerif,Standard,10)coloured(MarScoreR,MarScoreG,0)

DrawText("Apr #AprScore#",barindex,-18,SansSerif,Standard,10)coloured(AprScoreR,AprScoreG,0)

DrawText("May #MayScore#",barindex,-20,SansSerif,Standard,10)coloured(MayScoreR,MayScoreG,0)

DrawText("Jun #JunScore#",barindex,-22,SansSerif,Standard,10)coloured(JunScoreR,JunScoreG,0)

DrawText("Jul #JulScore#",barindex,-24,SansSerif,Standard,10)coloured(JulScoreR,JulScoreG,0)

DrawText("Aug #AugScore#",barindex,-26,SansSerif,Standard,10)coloured(AugScoreR,AugScoreG,0)

DrawText("Sep #SepScore#",barindex,-28,SansSerif,Standard,10)coloured(SepScoreR,SepScoreG,0)

DrawText("Oct #OctScore#",barindex,-30,SansSerif,Standard,10)coloured(OctScoreR,OctScoreG,0)

DrawText("Nov #NovScore#",barindex,-32,SansSerif,Standard,10)coloured(NovScoreR,NovScoreG,0)

DrawText("Dec #DecScore#",barindex,-34,SansSerif,Standard,10)coloured(DecScoreR,DecScoreG,0)

Hi = 57

Mid = 50

Mid2 = 0

Lo = -6

Lo1 = -10

Lo2 = -36

Return Hi as "Line1", Mid as "Line2", Mid2 as "Line3", Lo as "Line4", Lo1 as "Line5", Lo2 as "Line6"