Cynthia Kase KRev Amounts

{kind=link}

The KRev indicator – aka the Reversal amount indicator tells you the amount of dollar/pound/euro risk you’re exposed to on a unit basis if your position hits Kase Dev Stop 3 (Please see PRC Library for an explanation of the Kase Dev Stops: https://www.prorealcode.com/prorealtime-indicators/kase-dev-stop/).

The correct application of this KRev indicator will easily let you decide what time frame you can trade on to meet your fixed currency risk limit, per unit exposure.

For a better explanation as to why this indicator is so useful, please watch the following Kase StatWare presentation at 22 mins 08 secs to 31 mins 04 secs: https://www.youtube.com/watch?v=cd2gK8179u8

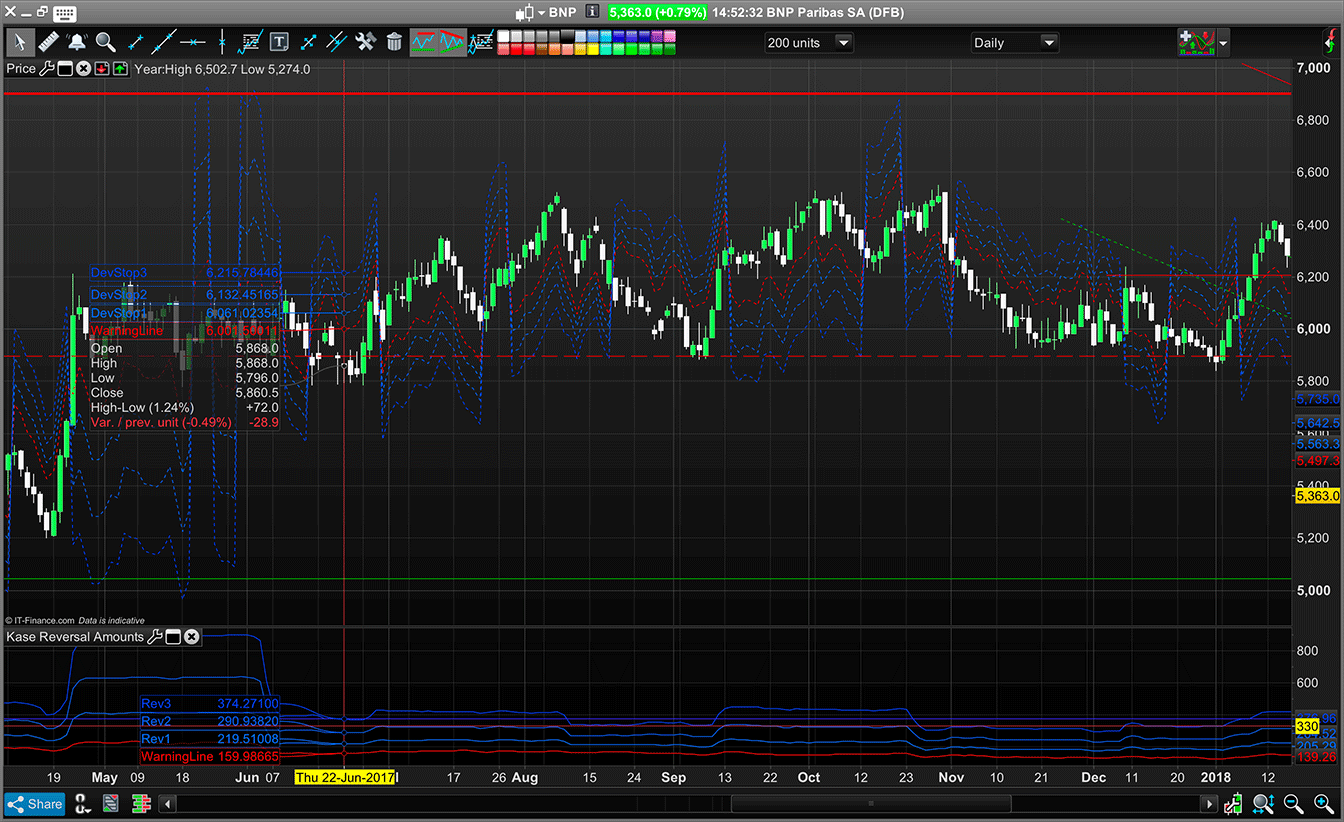

In the attached screen shot of BNP Bank the current price is €53.

The Euro risk is €3.74/share at Dev Stop 3.

Cynthia Kase: “The Dev Stop is the closest we can come to an ideal stop level in the real world. The indicator mathematics accounts for volatility (which is directly proportional to risk), and also for the variance of volatility (how much risk changes from bar to bar) and volatility skew (the propensity for volatility to spike higher from time to time). Specifically, the Dev Stop places exit points at 1, 2 and 3 standard deviations over the mean two bar true range, are corrected for skew. So we can take profit or cut losses at levels at which the probability of a trade remaining profitable is low, without taking more of a loss or cutting profits any sooner than necessary.”

Dev Stop 3 represents the “Get out of your position NOW!” statistically significant 3 standard deviation move against your trade with only a 0.1% chance of reversal. This is the point of no return to break even or profit – i.e. the highly improbable reversal that we as traders hope for when holding losses and which rarely happens.

It is calculated from a mathematically and statistically sound basis – 70 years worth of commodity/stocks and currency backtesting by Cynthia Kase and her team and includes an adjustment to account for price volatility skew in the market. This allows the data to reflect a normal distribution of ATR values and therefore confidence intervals and percentile probabilities – see the so-called 68–95–99.7 rule below. Skewness is a measure of the asymmetry of the probability distribution of a real-valued random variable about its mean. (Market price skew occurs because prices are not normally distributed and are bounded by zero – the price can never go below zero – but can potentially reach extreme values on the right hand side of the bell curve).

For a normal distribution bell curve, for example, a stop placed at the one standard deviation level has an 85% chance of being hit. Cynthia Kase designed the Dev Stop to withstand any 2 bar reversal so you’re not unnecessarily stopped out. Kase: “Our stops can be as the doorway that most (97.5 percent) of our two-bar reversals can pass through. Only the tallest sets of bars (candlesticks) will be blocked. (ie Allows position to remain open and only stop us out when prices hit extreme values ie. the remaining 2.5% of the price distribution).”

1 Std Devs = 68.2% of data falls within this range with a 84.1% chance of being hit — i.e. that a value will hit this probability percentile.

2 Std Devs = 95.4% of data falls within this range with a 97.7% chance of being hit.

3 Std Devs = 99.7% of data falls within this range with a 99.9% chance of being hit.

//pararemeters:

n = 30

//30 representing a statistically significant sample size

DTR = max(max(High - Low[2], abs(High - Close[2])),max(abs(Low - Close[2]),(abs(Low - Close[2]))))

price = typicalprice

avg = average[n](DTR)

st = std[n](DTR)

WarningLine = avg //30 Bar Ave, of 2 Bar Average True Range

KRev1 = avg + st

KRev2 = avg + 2.2*st //To account for volatility skew

KRev3 = avg + 3.6*st

RETURN Warningline coloured(255,0,0) as "WarningLine", KRev1 coloured(2, 118, 253) as “Rev1", KRev2 coloured(20, 100, 244) as “Rev2", KRev3 coloured(1, 71, 250) as “Rev3"The “hope and pray” approach to an open trading loss reversing (back to break even) is no longer required 😁

{kind=link}