Hello everybody !

I open this discussion file in order to share dans discuss about the strategy VECTORIAL DAX (M5) you can find here : https://www.prorealcode.com/prorealtime-trading-strategies/vectorial-dax-m5/

Best regards.

Hi Balmoral,

I like the approach you have chosen. Just a quick question. With instruments where pipsize =1 the code works fine, but I think as soon as this is not the case, things might not go as intended. In the code sample below for example only the MMA 15 steps back is multiplied by pipsize. For EUR/USD the pipsize can be 0.0001 and will therefore result in an angle that is always close to 90° (given that MMA is not multiplied) hence a buy condition.

ADJASUROPPO = (MMA–MMA[nbchandelierA]*pipsize) / nbChandelierA

If pipsize < 1 one might need to consider:

ADJASUROPPO = ((MMA–MMA[nbchandelierA])/pipsize) / nbChandelierA

Maybe I am missing something in my observation, so please review and I love to hear your feedback.

Paul

PaulParticipant

Master

Thanks for sharing!

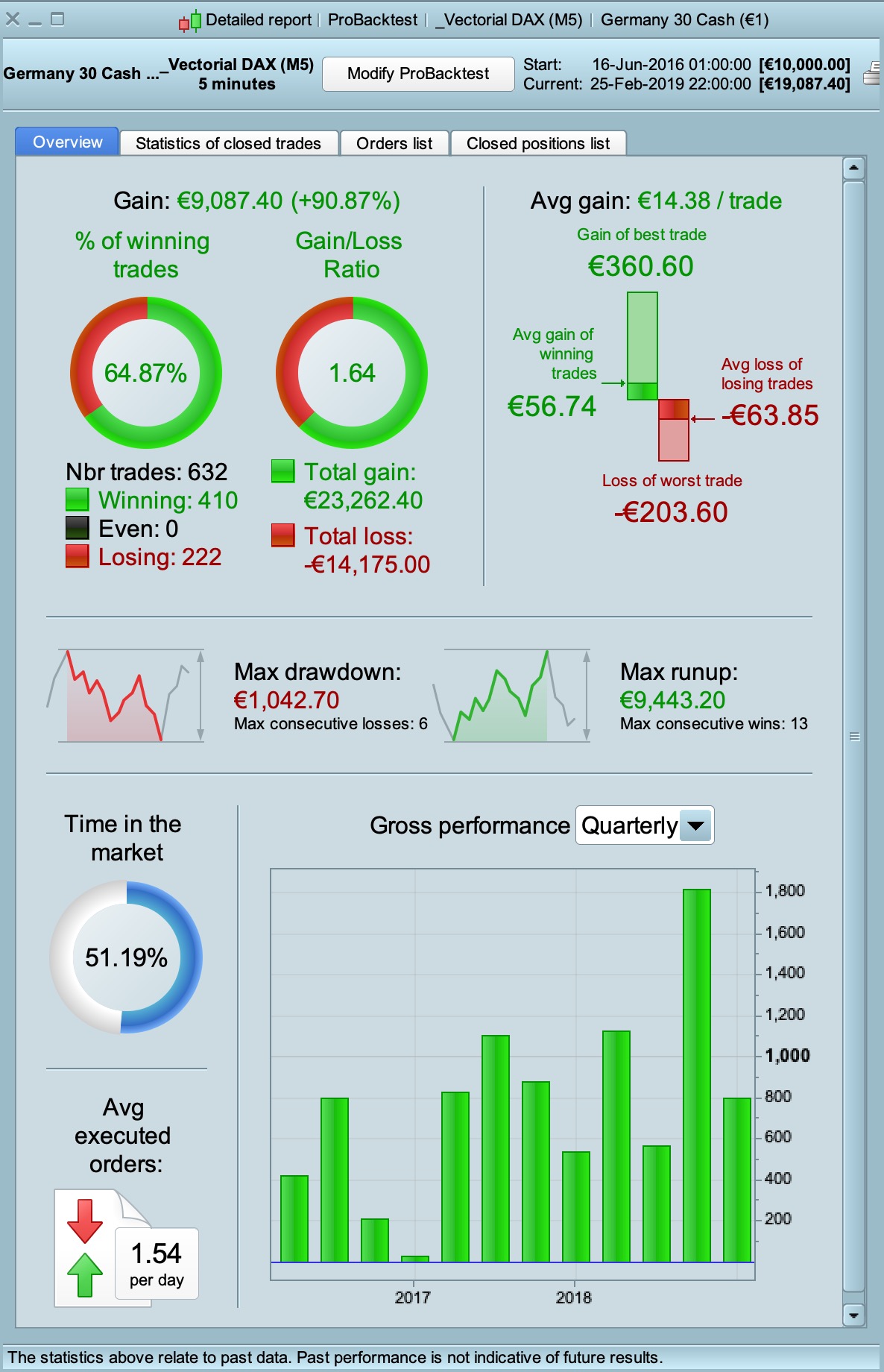

At first glance I thought it was over optimised but it’s a very impressive performance!

It needed a realistic stoploss. Testing shows 1 – 2% and I settled at 1.5% for 5 min TF

I disabled profit target but the change is little with or without.

Changed time, from 080000 to 180000 and set position size short 1 to match long 1.

Removed the barLong and barshort criteria to prevent zombie trades.

Adjusted the trailingstop reset criteria.

Changed the trailing stop and set long and short distance to same value 4.

The strange thing is the atrtrailingperiod doesn’t matter if it’s 14 or 25. Gonna check that some more.

Didn’t change your values for entry criteria.

The best thing is the results are still being good when using a stoploss!

Hi Balmoral,

I like the approach you have chosen. Just a quick question. With instruments where pipsize =1 the code works fine, but I think as soon as this is not the case, things might not go as intended. In the code sample below for example only the MMA 15 steps back is multiplied by pipsize. For EUR/USD the pipsize can be 0.0001 and will therefore result in an angle that is always close to 90° (given that MMA is not multiplied) hence a buy condition.

ADJASUROPPO = (MMA–MMA[nbchandelierA]*pipsize) / nbChandelierA

If pipsize < 1 one might need to consider:

ADJASUROPPO = ((MMA–MMA[nbchandelierA])/pipsize) / nbChandelierA

Maybe I am missing something in my observation, so please review and I love to hear your feedback.

Hi Nwesterhuijs !

Yes I am aware of this problem with Forex. But I use this strategy only on indices and not on forex because it is primarily a trend tracking strategy. The strategy is profitable over the long term thanks to a few very directional trades and an entry point adjusted to this trend and coupled with a trailing stop that allows to take maximum advantage of the trend.

On the forex the problem is that the price is rarely directional and tends to evolve in range and the strategy is not made for that.

But I think it is of course possible to adapt the calculation of the angle for the forex by searching a little …

If that can help you I have attached 2 indicator that correspond to the display of the angle (in degree) in form of histograms and the slope of the moving average (in radius) and its moving average. These are the indicators found in the code.

Moreover one can also adapt the code for the stock markets. Besides, that’s where I got the idea of the code when I studied the method of Stan Wenstein in timeframe Hebdo that I adapted to scalping 🙂

Good luck 🙂

Thanks for sharing!

At first glance I thought it was over optimised but it’s a very impressive performance!

It needed a realistic stoploss. Testing shows 1 – 2% and I settled at 1.5% for 5 min TF

I disabled profit target but the change is little with or without.

Changed time, from 080000 to 180000 and set position size short 1 to match long 1.

Removed the barLong and barshort criteria to prevent zombie trades.

Adjusted the trailingstop reset criteria.

Changed the trailing stop and set long and short distance to same value 4.

The strange thing is the atrtrailingperiod doesn’t matter if it’s 14 or 25. Gonna check that some more.

Didn’t change your values for entry criteria.

The best thing is the results are still being good when using a stoploss!

Thank you for these valuable tips Paul. I’ll will try with your parameters.

Another question I ask myself is whether the strategy can be profitable in real terms with slippage and overnights costs …

This is the version of the code with Paul’s parameters. And it is really improving the strategy. I have put %2 for the stop loss instead %1.5

Thanks a lot Paul !

I got a question regarding how u optimized it.

- You have access to 200K bars, how many did u optmize on?

- Is the code/idea original or copied and changed from interwebz/books?

- I think the code is simple enough (just looking angles on the MA’s) so im not that worried, but there are still a few MA variables and such.

Done walk forward? What was the results?

- How many variables have you optimized?

- Have u tried optimizing it for other markets/timeframes?

Hi everybody

Did you try on another index like DOJI? Could be a good test…

Tof

I got a question regarding how u optimized it.

- You have access to 200K bars, how many did u optmize on?

- Is the code/idea original or copied and changed from interwebz/books?

- I think the code is simple enough (just looking angles on the MA’s) so im not that worried, but there are still a few MA variables and such.

Done walk forward? What was the results?

- How many variables have you optimized?

- Have u tried optimizing it for other markets/timeframes?

1. on 200 K bars

2. Original idea after read the book of Stan Wenstein who trade with MM30 on timeframe HEBDO

3. No i don’t try walk forward

4. The 6 optimized variables who are = PeriodeA / nbChandelierA / ANGLE / lag / PeriodB / nbChandelierB

5. Yes it seems to work very well on DAX (H4) and quit well DJIA (M15 / M5) and on shares market by adapting the calculation of the MM angle

This is the code for CFD Wall Street Cash (M5)

@Balmora74

I think that you should consider sharing the original code but with the variables to be optimized included, so that everyone could make optimization and WF on many different instruments and share here their results. Thank you 😉

Will run a walk forward later today. Will share results.

Im gonna run the WF tonight, 25K combinations per run lol. Gonna take some hours. Will update on the results.