Here is my version, with a different angle (WF).

Improvments and suggestions are welcome!

// ROBOT VECTORIAL DAX V.3

// M5

// SPREAD 1.5

// by BALMORA 74 - FEBRUARY 2019 /// winnie version 10/04/12019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//VARIABLES

CtimeA = time >= 080000 and time <= 180000

CtimeB = time >= 080000 and time <= 180000

ONCE BarLong = 950 //EXIT ZOMBIE TRADE LONG

ONCE BarShort = 650 //EXIT ZOMBIE TRADE SHORT

MoneyManagement = 2

//MoneyManagement = Set to 0 for level stakes. Set to 1 for increasing stake size as profits increase and decreasing stake size as profits decrease. Set to 2 for increasing stake size as profits increase with stake size never being decreased.

RiskManagement = 1

//RiskManagement = 0 = risk management off and 1 = risk management on. I do not recommend using this it can blow up your account very easily!

Capital = 10000

MinBetSize = 1

//MinBetSize = The minimum bet size allowed for the instrument.

RiskLevel = 10

//RiskLevel =A factor that changes how fast position size increases as profit increases. Only relevant if Risk Management is turned on.

Equity = Capital + StrategyProfit

IF MoneyManagement = 1 THEN

PositionSize = Max(MinBetSize, Equity * (MinBetSize/Capital))

ENDIF

IF MoneyManagement = 2 THEN

PositionSize = Max(LastSize, Equity * (MinBetSize/Capital))

LastSize = PositionSize

ENDIF

IF MoneyManagement <> 1 and MoneyManagement <> 2 THEN

PositionSize = MinBetSize

ENDIF

IF RiskManagement THEN

IF Equity > Capital THEN

RiskMultiple = ((Equity/Capital) / RiskLevel)

PositionSize = PositionSize * (1 + RiskMultiple)

ENDIF

ENDIF

PositionSize = Round(PositionSize)

// TAILLE DES POSITIONS

PositionSizeLong = 1 * positionsize

PositionSizeShort = 1 * positionsize

//STRATEGIE

//VECTEUR = CALCUL DE L'ANGLE

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO)) //FONCTION ARC TANGENTE

CondBuy1 = ANGLE >= 20

CondSell1 = ANGLE <= - 24

//VECTEUR = CALCUL DE LA PENTE ET SA MOYENNE MOBILE

ONCE PeriodeB = 20

ONCE nbChandelierB= 35

lag = 1.5

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

CondBuy2 = (pente > trigger) AND (pente < 0)

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

//ENTREES EN POSITION

CONDBUY = CondBuy1 and CondBuy2 and CTimeA

CONDSELL = CondSell1 and CondSell2 and CtimeB

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSizeLong contract at market

SET STOP %LOSS 2

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSizeShort contract at market

SET STOP %LOSS 2

ENDIF

//VARIABLES STOP SUIVEUR

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE trailingstoplong = 4 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 14 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

//EXIT ZOMBIE TRADE

IF POSITIONPERF<0 THEN

IF shortOnMarket AND BARINDEX-TRADEINDEX(1)>= barshort THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

IF POSITIONPERF<0 THEN

IF LongOnMarket AND BARINDEX-TRADEINDEX(1)>= barlong THEN

SELL AT MARKET

ENDIF

ENDIF

Hi Winnie. Thanks for sharing your researchs

From my side I worked on an improved version based on Paul’s suggestions

I kept the values of original angles but I did a backtest using Walk Forward to optimize the variable “lag” and I’m OK like you for lag = 1.5.

Otherwise I added a 3rd condition for LONG and SHORT based on the orientation of a medium-term moving average :

CondBuy3 = average[100](close) > average[100](close)[1]

CondSell3 = average[20](close) < average[20](close)[1]

It gives less number of positions / less drawdown and a better profit factor.

Below are the results and the .ITF file.

It is quite possible that the algorithm is over fitted and over optimized. Reason why I put the code in account demo to observe its behavior over 6 months to 1 year…

I will it share it after….

// ROBOT VECTORIAL DAX v2

// M5

// SPREAD = 1

// by BALMORA 74 - APRIL 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//TRADING TIME

CtimeA = time >= 080000 and time <= 180000

CtimeB = time >= 080000 and time <= 180000

//POSITION SIZE

PositionSize = 1

//STRATEGY

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

ONCE PeriodeB = 20

ONCE nbChandelierB= 35

ONCE lag = 1.5

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO))

CondBuy1 = ANGLE >= 35

CondSell1 = ANGLE <= - 40

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

//BUY CONDITIONS

CondBuy1 = ANGLE >= 35

CondBuy2 = (pente > trigger) AND (pente < 0)

CondBuy3 = average[100](close) > average[100](close)[1]

CONDBUY = CondBuy1 and CondBuy2 and CondBuy3 and CTimeA

//SHORT CONDITIONS

CondSell1 = ANGLE <= - 40

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

CondSell3 = average[20](close) < average[20](close)[1]

CONDSELL = CondSell1 and CondSell2 and CondSell3 and CtimeB

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSize contract at market

SET STOP %LOSS 2

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSize contract at market

SET STOP %LOSS 2

ENDIF

//TRAILING STOP

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE trailingstoplong = 4 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 14 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

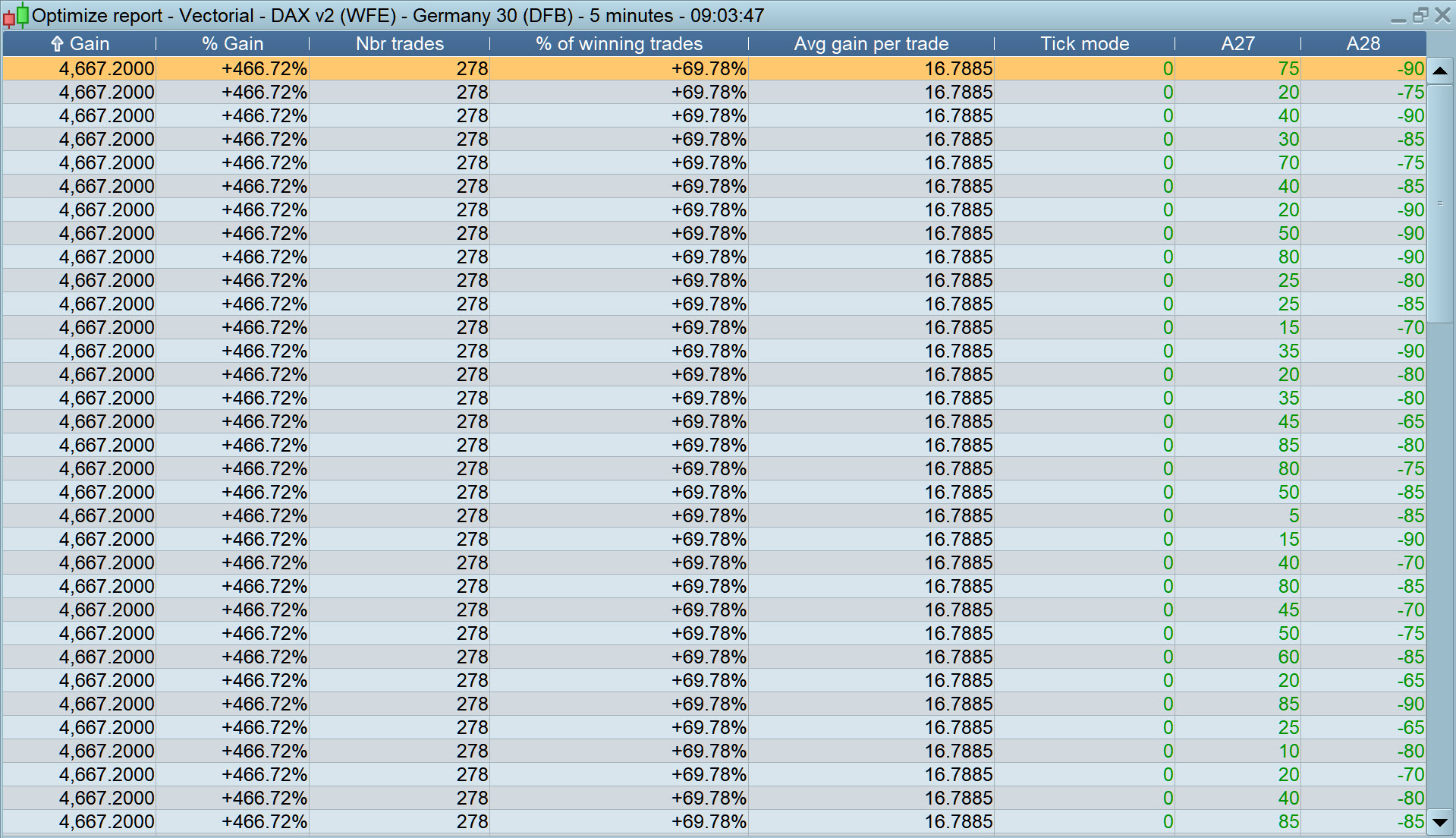

Is there redundant code in this strategy or can anybody offer a reason for the following please?

When I optimise the angles, it seems that almost any value gives the same figure for Gain … see attached.

Attached is related to the code version immediately above this post.

Hi Balmara74,

thanks for your improvment. I run it too. Another idea to improve tue strategy would be to include and test this part of code, very interesting…

https://www.prorealcode.com/blog/learning/how-to-improve-a-strategy-with-simulated-trades-1/

I tried to do it yesterday but i’m not a professionnal coder ;), so some difficulties and errors to do it. Could you try?

Did you test the strategy on 200K?

@Grahal

Maybe because you use a negative angle value for variable A28.

It could be interesting to use a value between 0 and +90 (knowing that the more one deviates from 45 and less positions we have).

EDIT POST – ERROR FOUND !!

I found a error on the code above !! Yes it’s redudant because LINES 27 and 28 are the same than LINES 34 and 40

So this is the good version of the code below (i have delete lines 27 and 28) :

// ROBOT VECTORIAL DAX v2

// M5

// SPREAD = 1

// by BALMORA 74 - APRIL 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//TRADING TIME

CtimeA = time >= 080000 and time <= 180000

CtimeB = time >= 080000 and time <= 180000

//POSITION SIZE

PositionSize = 1

//STRATEGY

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

ONCE PeriodeB = 20

ONCE nbChandelierB= 35

ONCE lag = 1.5

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO))

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

//BUY CONDITIONS

CondBuy1 = ANGLE >= 35

CondBuy2 = (pente > trigger) AND (pente < 0)

CondBuy3 = average[100](close) > average[100](close)[1]

CONDBUY = CondBuy1 and CondBuy2 and CondBuy3 and CTimeA

//SHORT CONDITIONS

CondSell1 = ANGLE <= - 40

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

CondSell3 = average[20](close) < average[20](close)[1]

CONDSELL = CondSell1 and CondSell2 and CondSell3 and CtimeB

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSize contract at market

SET STOP %LOSS 2

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSize contract at market

SET STOP %LOSS 2

ENDIF

//TRAILING STOP

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE trailingstoplong = 4 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 4 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 14 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

I am going to run this code live.

A little more fun then 🙂

In order for the losses not to be too large you can sell ex.. 0.5 contracts directly after a position is taken.

It will be lower DD as well.

How do you code this?

bullbear – Partial closure is not possible in live trading in ProOrder.

Vonasi

Sad to hear that.

I currently have 5 algo live on dax.

Unfortunately, they have gone bad at the same time and it is expensive.

I am going to run them on demo now instead.

I currently have 5 algo live on dax. Unfortunately, they have gone bad at the same time and it is expensive. I am going to run them on demo now instead.

I would suggest always running any strategies in a lengthy live forward test in demo to confirm that they are not curve fitted. Yes it is a bit boring and not as exciting as going live but your patience will save you from losing an awful lot of money in the long run. I have strategies that have had on test for a year or more now. They are very profitable but the draw down was bigger than in the in sample test and would have sucked my real account dry if I had just gone live with them. Patience pays!

vonsai

True!!

I tested your code on nasdaq.

changed sl and tp and time.

// ROBOT VECTORIAL DAX v2

// M5

// SPREAD = 1

// by BALMORA 74 - APRIL 2019

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 50000

//TRADING TIME

CtimeA = time >= 150000 and time <= 220000

CtimeB = time >= 150000 and time <= 220000

//POSITION SIZE

PositionSize = 1

//STRATEGY

ONCE PeriodeA = 10

ONCE nbChandelierA= 15

ONCE PeriodeB = 20

ONCE nbChandelierB= 35

ONCE lag = 1.5

MMA = Exponentialaverage[PeriodeA](close)

ADJASUROPPO = (MMA-MMA[nbchandelierA]*pipsize) / nbChandelierA

ANGLE = (ATAN(ADJASUROPPO))

MMB = Exponentialaverage[PeriodeB](close)

pente = (MMB-MMB[nbchandelierB]*pipsize) / nbchandelierB

trigger = Exponentialaverage[PeriodeB+lag](pente)

//BUY CONDITIONS

CondBuy1 = ANGLE >= 35

CondBuy2 = (pente > trigger) AND (pente < 0)

CondBuy3 = average[100](close) > average[100](close)[1]

CONDBUY = CondBuy1 and CondBuy2 and CondBuy3 and CTimeA

//SHORT CONDITIONS

CondSell1 = ANGLE <= - 40

CondSell2 = (pente CROSSES UNDER trigger) AND (pente > -1)

CondSell3 = average[20](close) < average[20](close)[1]

CONDSELL = CondSell1 and CondSell2 and CondSell3 and CtimeB

//POSITION LONGUE

IF CONDBUY THEN

buy PositionSize contract at market

SET STOP %LOSS 2

ENDIF

//POSITION COURTE

IF CONDSELL THEN

Sellshort PositionSize contract at market

SET STOP %LOSS 2

ENDIF

//TRAILING STOP

ONCE trailingStopType = 1 // Trailing Stop - 0 OFF, 1 ON

ONCE trailingstoplong = 8 // Trailing Stop Atr Relative Distance

ONCE trailingstopshort = 5 // Trailing Stop Atr Relative Distance

ONCE atrtrailingperiod = 30 // Atr parameter Value

ONCE minstop = 0 // Minimum Trailing Stop Distance

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl = round(atrtrail*trailingstoplong)

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

Sorry Vonsai. Wrong of me there.

It´s Balmora´s code 🙂

Balmora74, Vonasi and the others,

Could someone do this? Thanks 🙂

Another idea to improve tue strategy would be to include and test this part of code, very interesting…

https://www.prorealcode.com/blog/learning/how-to-improve-a-strategy-with-simulated-trades-1/

I tried to do it yesterday but i’m not a professionnal coder 😉

I’ve done a lot of coding with simulated trading ideas in the past but my conclusion after a lot of effort was that it wasn’t really worth the effort. Others may have a different point of view.

At the moment I am a bit busy with other projects and I don’t really enjoy converting other people’s codes (especially if a lot of the variable names are Italian!) so I’ll leave this one for someone else if that is OK.

Not my code!

Not even your name! 🙂

Couldn’t resist sorry … as you said Vonasi trading can be lonely and I do enjoy a laugh even if it me making myself laugh!