Thank you for the link Vonasi … All this is not very reassuring ..

Thanks for the link Vonasi!

So it looks like I decided to start with the trading systems in the very best moment to get some trust 🙂

Hope everything is gonna get solved or at least IG give us some kind of valid answer

capgros – bear in mind that this is all on Demo. IG give low priority to demo. No one has reported trades stopped on live accounts as far as I know.

Hallo

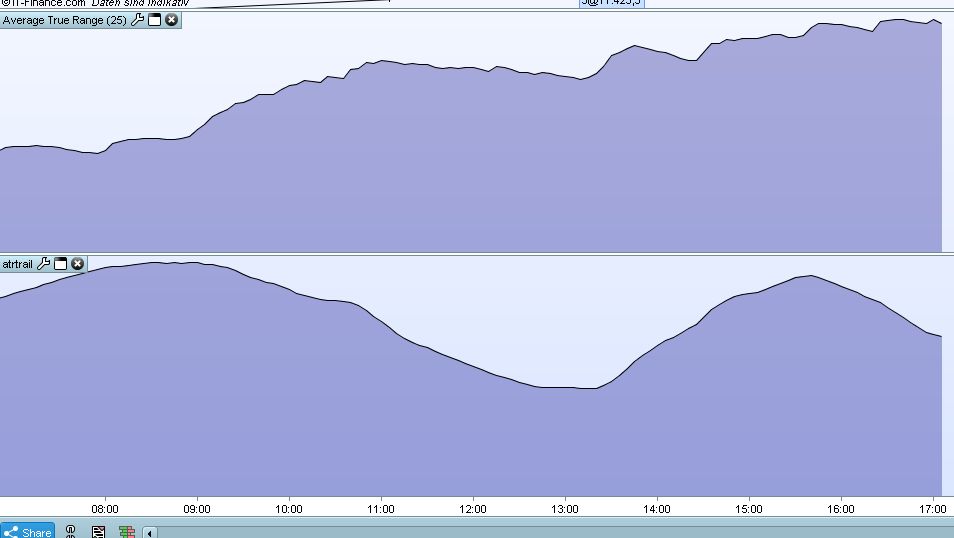

sorry, but can somebody me explaine the meaning of (close/10)

I can#t find this in the manual

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pipsize)/1000

close/10 is just the closing price divided by 10.

Sorry, this is not correct.

If yo make two diffent Indicators you can se it is not the same chart

this is not the close / 10

When using AVERAGETRUERANGE[25] it is not normally necessary to use the (close) part of the instruction to get a result. It appears that the closing price or close/10 within the () is somehow used in the calculation of the average true range. I can only guess at the moment that it is used in the true range calculation required. This seems wrong to me. I have highlighted it to Nicolas off forum and hopefully he can investigate with PRT how they use what is in the () in the calculation.

AverageTrueRange[N](price)

Calculation :

This represents the volatility of a stock.

True range is the highest data in absolute value among :

(today’s high – today’s low)

(today’s high – yesterday’s close)

(today’s low – yesterday’s close)

So if you replace the Close (which is the default data serie to calculate the ATR) with another variable, it will be used in the above calculation, comparing Close/10 to High and Low will obviously result of something peculiar! 😉

So it is as I thought. Which means that any value other than close is really a custom ATR indicator and not the standard ATR indicator.

I’m running the strategy since 1. of march on live account and it looks pretty stable. There was one trade last friday which went profitable on monday but the trailing did not get activated at all so I closed the position manually. However, I’m running a mixed version with an dax opening strategy so the problem might be there. I’m also currently looking into a position which got stopped out today altough a clear opposite trend was building up for a while. Maybe it makes sense to include an additional stop criteria.

@Zebra

What is the Dax Opening Strategy ?

Yes you can add a stop loss to the strategy like suggested by Paul on the first page of this forum discussion.

Hello, I have one question regarding the trailing stop used in the strategy. I know this is one of the existing trailing stop codes of the website.

I guess that both trailingstoplong and trailingstopshort variables have been optimized to fit the prices between mid 2016 and now, so for a DAX between 10000 and 13500.

So will the trailing stop be still this efficient outside this trading range, for instance for a DAX above 13500 or below 10000 ?

So will the trailing stop be still this efficient outside this trading range, for instance for a DAX above 13500 or below 10000 ?

Probably not or maybe!

This is a major problem whenever a strategy has an optimized SL or TP of any form IMHO. If the original strategy was developed on a section of data and then re-tested on an out of sample section of data and then still performed the same then you might be in with a fighting chance that it will work in the future – or the markets could just do something completely different in the future compared to the past and confound us all.

Often range can change with increase of price especially on indices making a fixed SL or TP or trailing stop variable seem irrelevant. Also range compared to price is not totally linear so even trying to adapt SL and TP relative to price does not always work – or ends up being just one more thing that you curve fitted.