Of course there is a difference between capital with leverage and capital without, I agree with you. The fact you can have the oppportunity to leverage, I calculate the return on that capital at risk versus the return against my capital without leverage. Because I wouldn’t be able to do it without the leverage 🙂

When I am saying you can run the algo with 1 or 2 K this after doing some basic validation of the risk of ruin. So for example the FTSE M5, my risk of ruin (losing all my capital) is virtually zero based on past transactions, even with an initial capital of 1 K.

Let’s think a little about risk again. Let’s assume you trade all 20 algos with a real value of about € 10.000 each, and all of them are long. That may well happen one day, as they all trade stock indices (except for one on oil). Now, for some reason, all stock indices worldwide lose 5%, which may happen tomorrow. If all algos run into stop loss, you lose 2 % of € 200.000 or € 4.000 at once. I don’t know how big the stop loss is for the algos on higher time scales than 2 minutes, but for 2 minutes it’s 2%, so I’d assume it is not lower for the higher time scales. For the 2 minutes algos, the trading principle is obviously that small losses are not permitted, but only winning positions or positions with 2% stop loss are allowed. If this is the trading principle for all algos, I’d think that sooner or later it will happen that all of them run into stop loss together one day, the question is only how long you’d have to wait for that day.

A really good post XORANDNOT. This is something those that sell these algos don’t speak about (at least I haven’t seen it). It would be so much trustworthy if that could be a part of the selling package.

Maybe the strategy is only run on 2min for faster execution but the core strategy is on a higher timeframe like 15min or 30min. In which case a 2% stoploss isnt too bad.

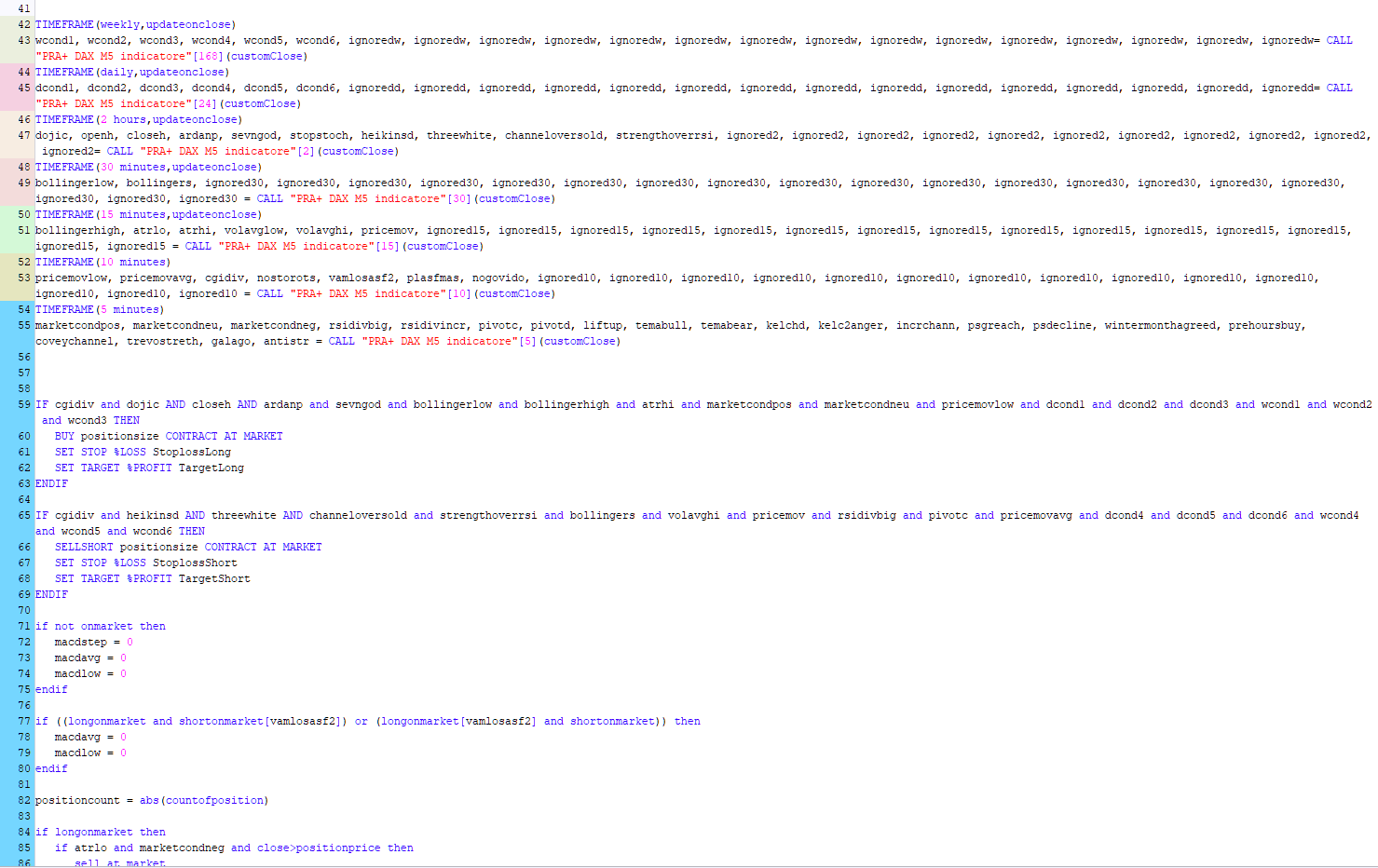

Can you see the code? Or do they hide everything?

Ive run strategies on a 1min for faster breakeven execution while my core strategy is on 15min as a MTF setup.

Im just saying if thats the case then we cant compare the short timeframes with their stoploss percentage.

Even if it is a 2min setup it could have variable exit conditions and 2% as just a hard stop failsafe.

It would be good if they can clarify this for sure.

You can only see some basic code and a trailing stop. The main parameters are of course hidden in an encrypted indicator. There is no multi-timeframe in the main code.

For the 2% stop loss on the 2 minute systems, look at

ProRealAlgos? Real or fake

and

ProRealAlgos? Real or fake

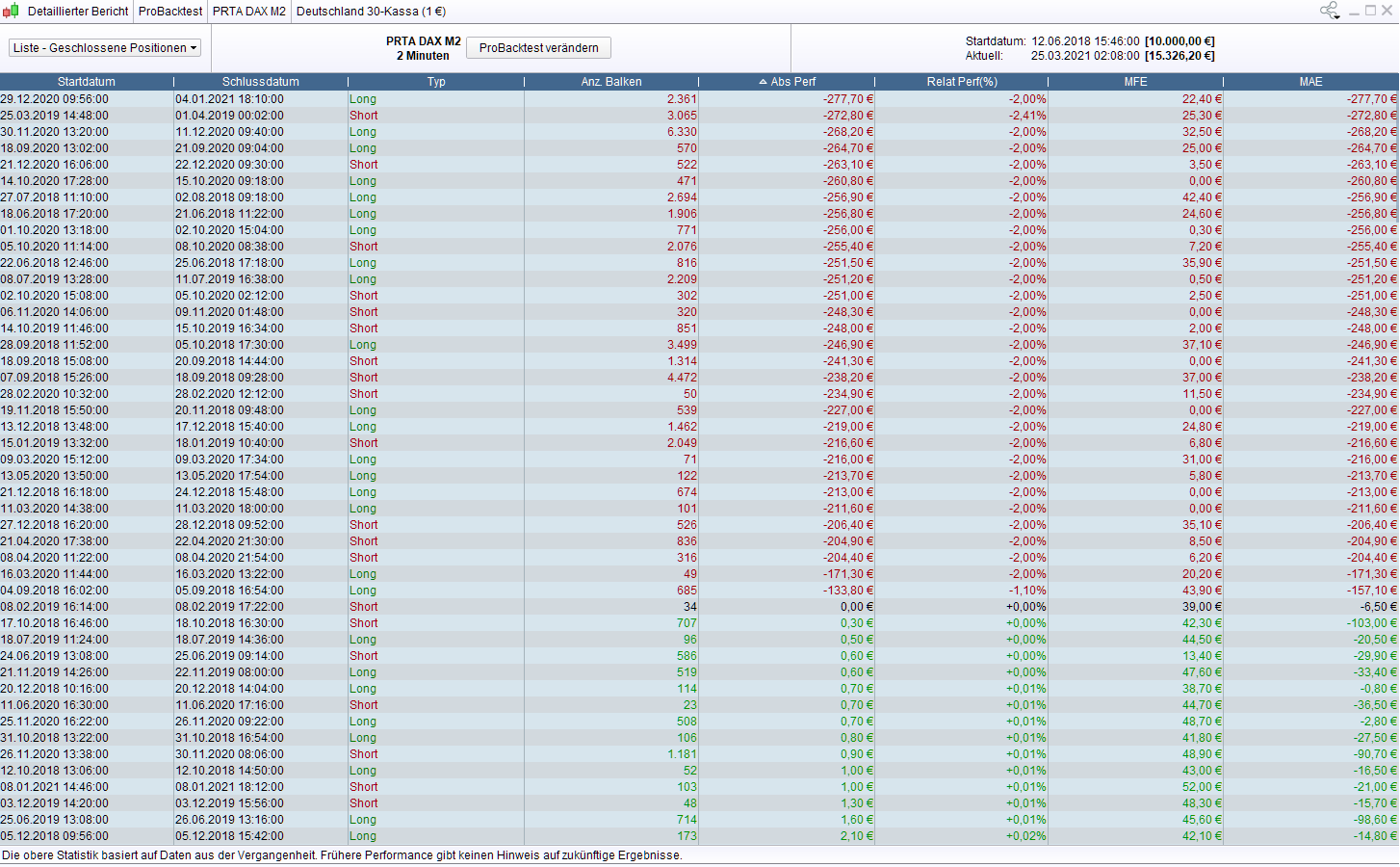

In the detailed reports of the backtests, you clearly see that there are only exits with winning positions or with 2% stop loss, nothing in between. Smaller losses (what you call “variable exit conditions”) are obviously excluded by the code.

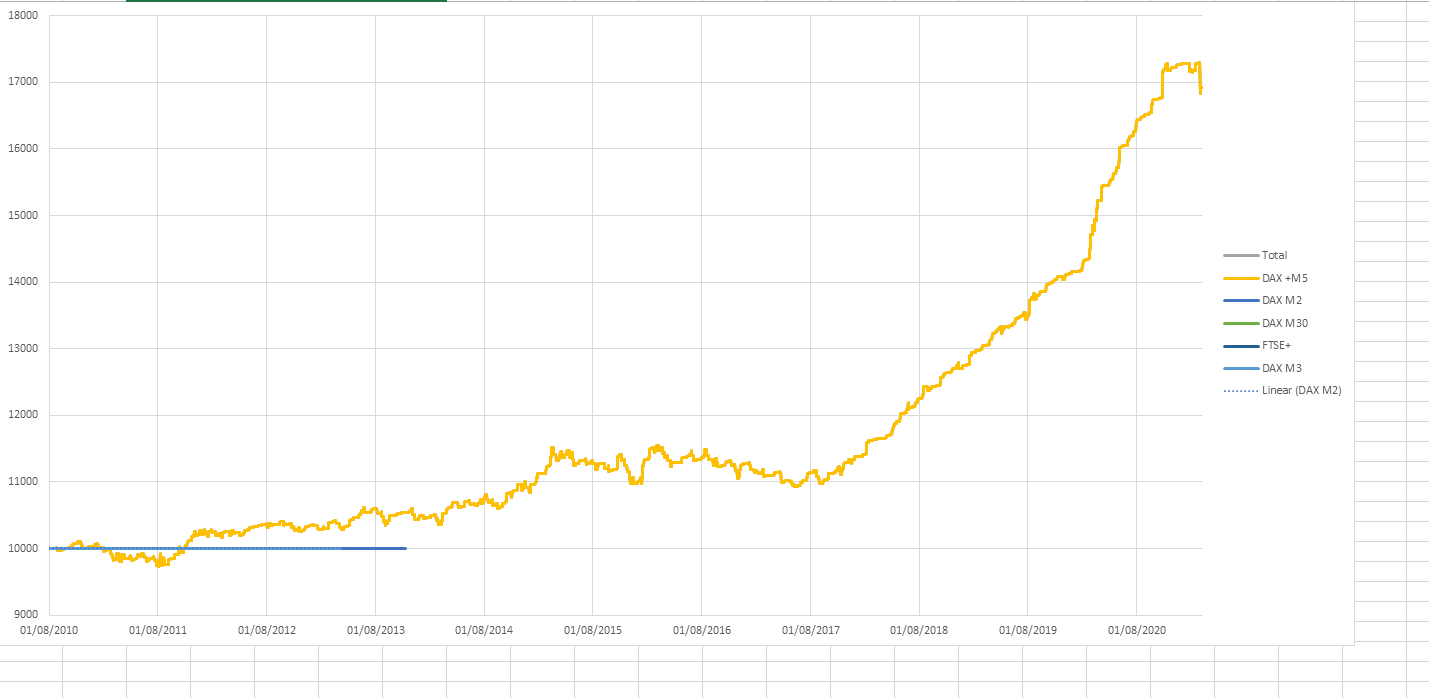

or look at this one : Losing and winning positions of PRTA DAX M2

All the new algos PRA+ are multi timeframes.

The fact that exits are only trailing stops and/or stop loss is not necessarily bad.

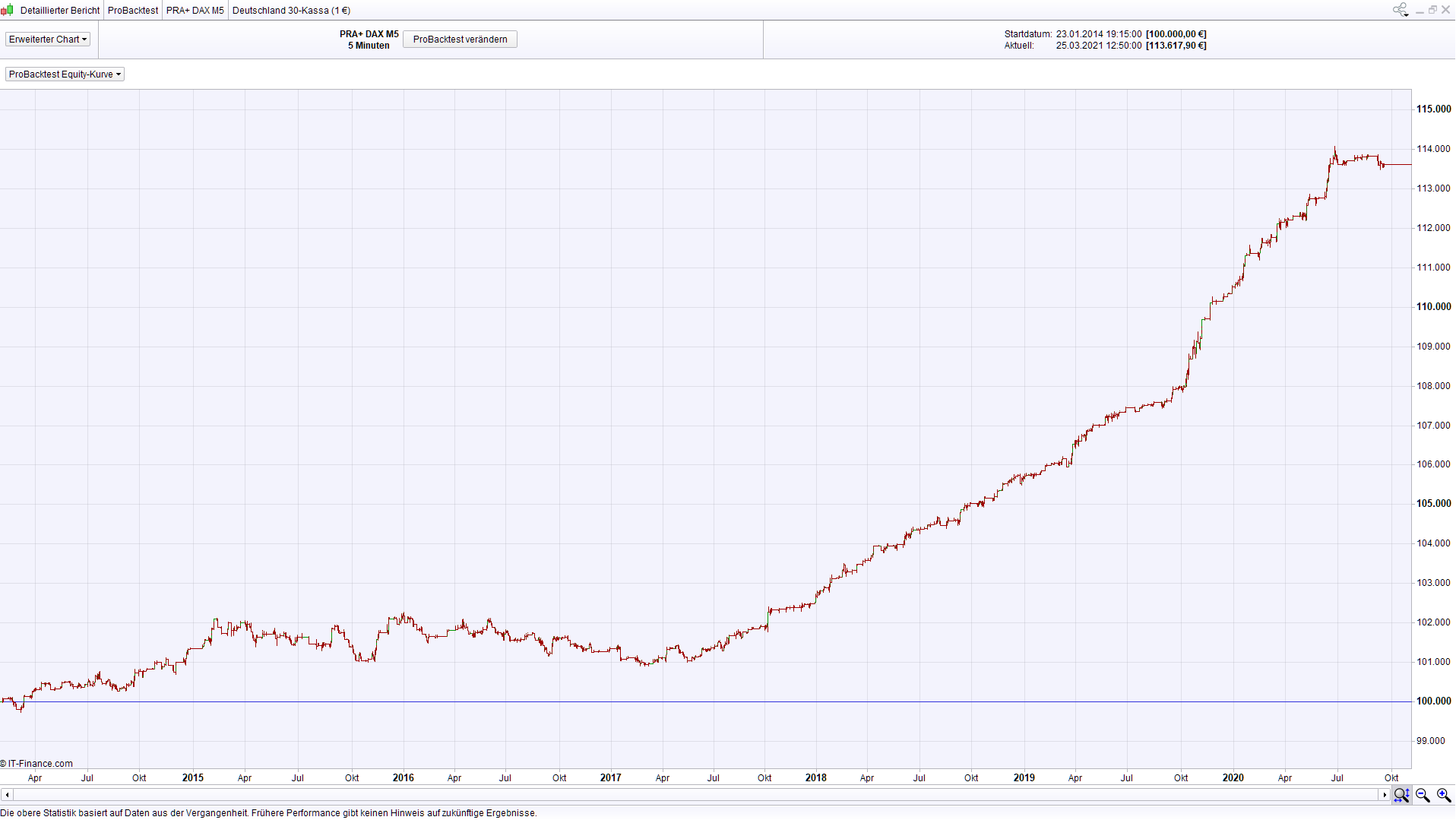

For me what is more worrying is that all the algos were optimised on a 200 K timeframe. When running those (especially the short timeframes) on 1 M bars, the equity curve in the OOS data is really not convincing .

I ran them all and none have a nice equity curve, some of them are not even profitable.

Many different timeframes indeed in PRA+ DAX 5 minutes, and many variables.

In the detailed report, I see that the density of losing positions is a lot higher in the non-optimized regions before 2017. Stop Loss is 1.7% here, and there are a few exits with smaller losses.

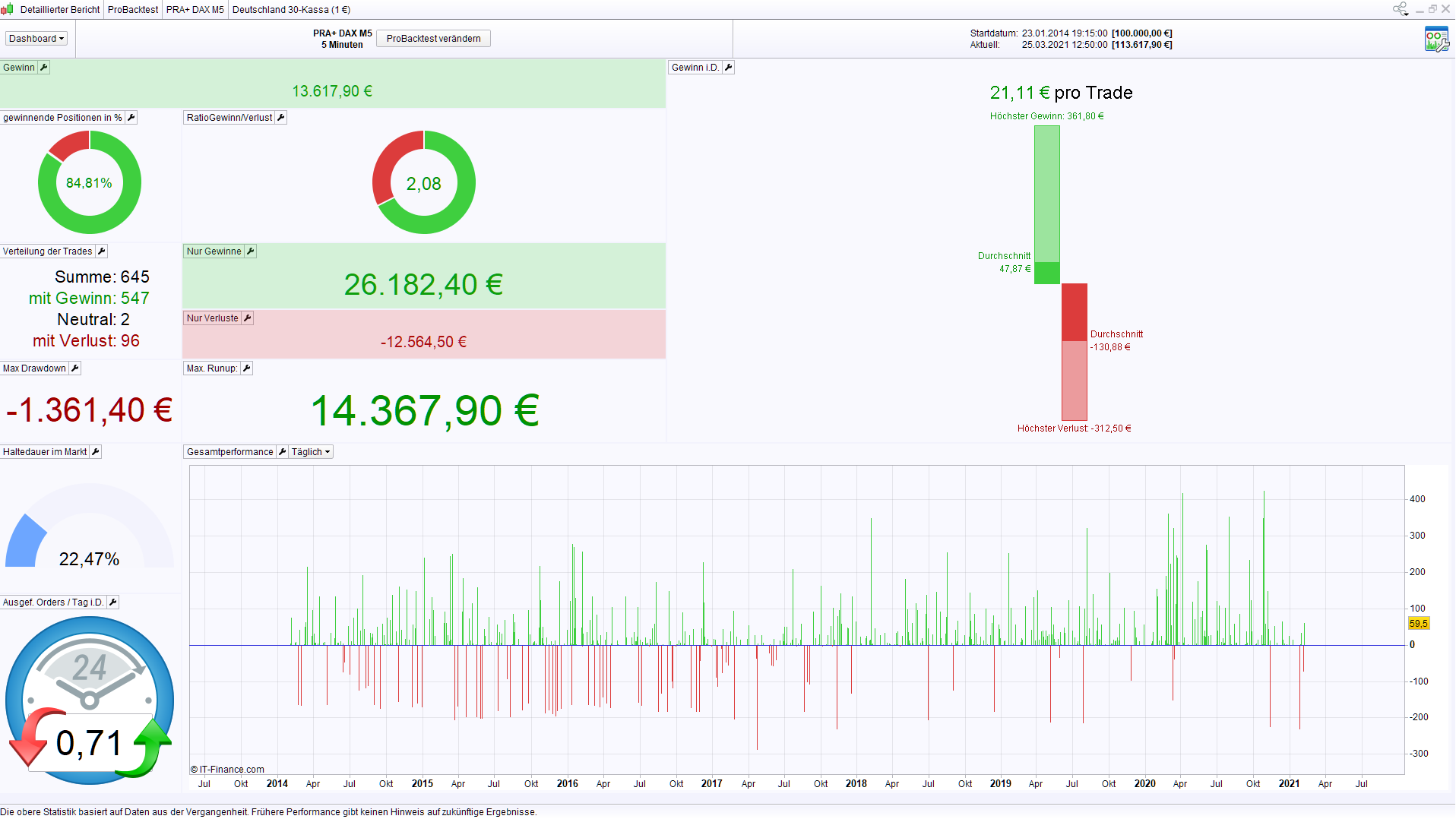

Backtest was done with 500.000 bars, and it took about an hour to complete.

Yes quite flat before 2017. Attached curve for 1 M bars

If I have time tomorrow I’ll attach the curve for all algos tomorrow (but similar type of curve)

Do they send regular update? Prior to v11, there were no possibility to backtest 1M bars, and with IG data, it is very recent. So we must admit that this OOS sample before that nice curve ascension is not so “bad”, even if it is almost flat.

If there are regular new optimization / validation for recent data, that equity curve does not surprise me.

I’m not sure how PRTA goes about delivering new parameters / algos to its customers, but if you receive a new update in the next few days/months, it is likely that the look of this backtest will be very different. Indeed, if we backtest a strategy with the recent parameters validated for the market closest to us in time, then the results of the past can be impacted and be considered bad.

This is the whole subject of optimization / validation in walk forward mode.

I am not a customer of PRA so I don’t really know how and if they provide regular updates, but I don’t believe so. The original algos like DAX M2 have remained untouched since originally developed (I believe early 2020). The new algos PRA+ have only been released quite recently, but my understanding is that the PRA team will soon release updates of the algos after having reoptimised on the 1 M bars.

I agree flat is not too bad, at least you are not losing money on the OOS. But not all of them are flat 🙂

One could argue that walk forward in the past could be a valid validation as walk forward in the future. History tends to repeat itself. I am not experienced enough to debate this topic !

but if you receive a new update in the next few days/months, it is likely that the look of this backtest will be very different.

Optimized on 1 M bars then and looking good back to 2010 ?

I wanted to mean that if we use variables optimized and validated over the last periods, as the use of the walk forward tells us, these variables would not be able to validate tests from X years ago. . This being the case, I have no indication on how these algorithms are optimized (or not?), X IS + OOS periods, in anchored mode or not, etc. Only the author could tell you, ask him the question 😉