Hi Reiner,

can you please share the programs for Natural Gas and Coffee as well?

I chewed the seasonal numbers but best results are only Natural Gas (409%/36%DD) and Coffee (795%/52%DD).

Hi Alco,

There are two easy approaches to estimate the required Pathfinder account size.

- multiply the maximum drawdown with 2 (or 3) and add the margin for the maximum position size or

- multiply the maximum position size with 1k.

With 10k and three running Pathfinder algos you have to reduce the position size. The default parameter settings for each Pathfinder version is for an 10k account.

Best, Reiner

Hi Pranik,

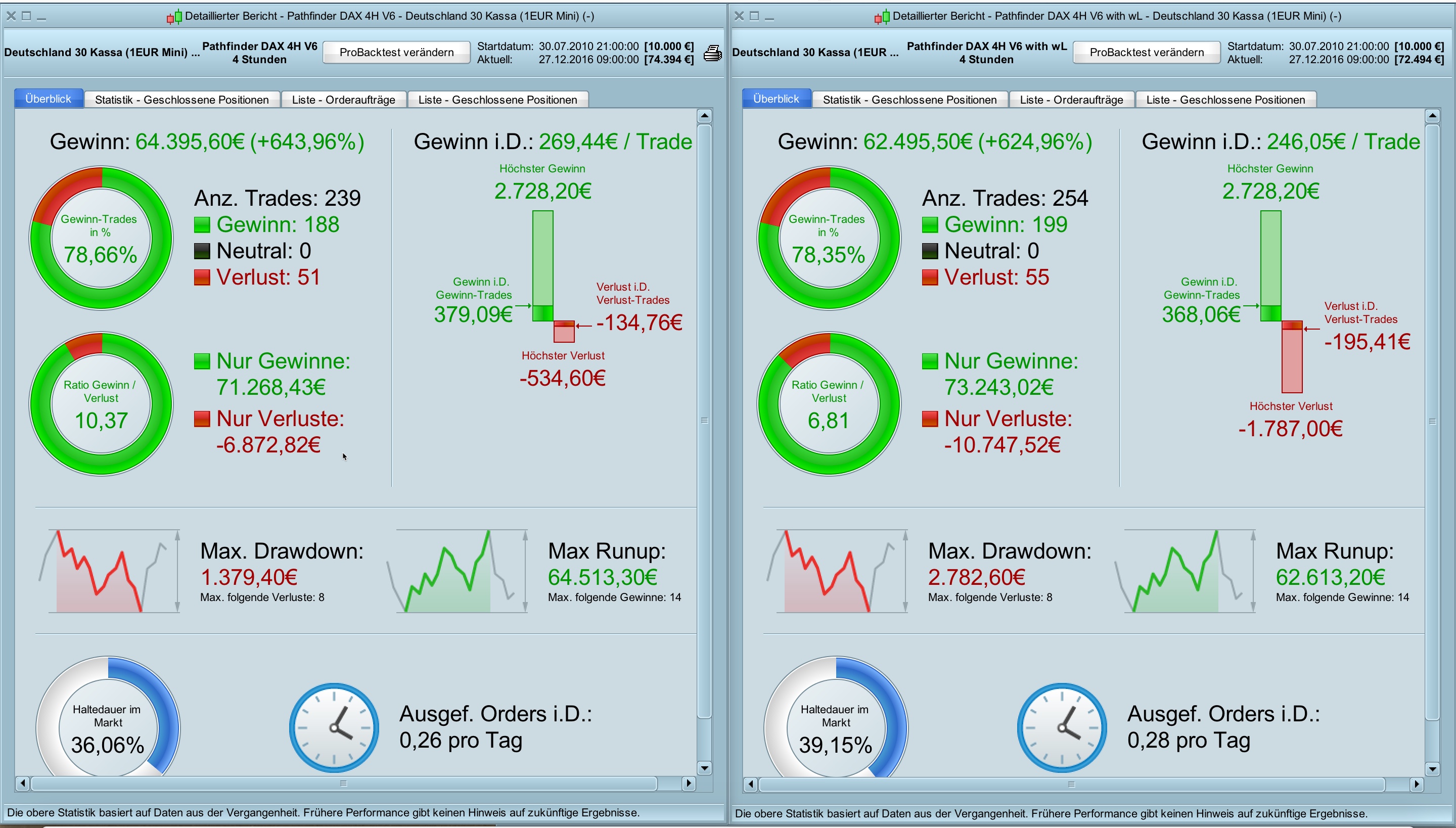

Thanks for your idea. In my opinion weekly low is a weak condition and doesn’t produce high quality signals. I have extended Pathfinder DAX 4H V6 with the weekly low setup and the result is worse especially the drawdown (double). Please find attached a comparison of original V6 and V6 adopt with weekly low setup.

Best, Reiner

Hi CKW,

I never had this error message and unfortunately I have no clue what is the reason. I suppose it has something todo with the preload bars settings. Try to reduce the default setting.

DEFPARAM PRELOADBARS = 10000

Maybe someone else can advise.

Best, Reiner

Hi Reddi and welcome,

In my experience with 5M timeframe the Pathfinder breakout algo has to many fake breakouts. Higher timeframes are working like filter and increase the quality of the trade signals. I will focus with Pathfinder on the daily timeframe for the swing trades and on 4H and 1H for the intraday trades.

I encourage you hereby to verify if Pathfinder works in 5M or 15M. Let me know when you find a profitable approach.

Best, Reiner

Hallo Pfeiler,

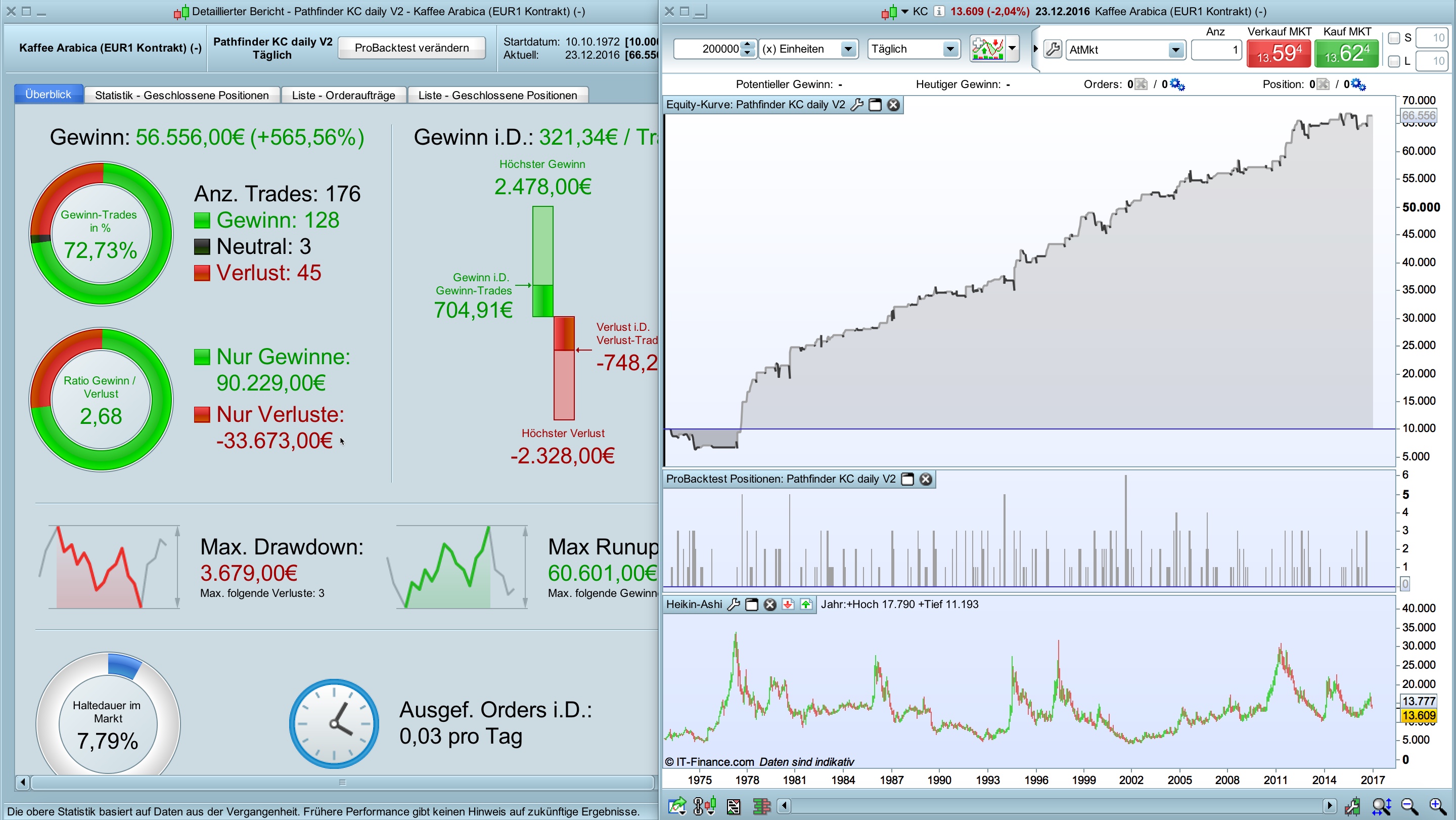

I just rework all the Pathfinder daily backtests and will publish all saisonal adjustments soon. NG and KC is already finished.

Thanks for your hint with the @Day-function. I have changed the code accordingly.

KC has a drawdown of 36% and doesn’t fulfill my quality Pathfinder requirements but is on the other side one of the profitable versions. I let it in the top list because of the drawdown was 1972.

Best, Reiner

Hi Reiner,

Thank you for sharing your code and the time you put into this. Can see a lot more members are getting on board and have different request which is great but getting a bit long and confusing. Perhaps can open individual forum for each indices/commodities (even forex), making it easier to follow the indices/commodities you are interested in trading now or maybe in the future, and for new members to pick up too.

Best regards,

Sylvester

Hey Reiner,

I am sure you are aware of this, but in the Excel I saw that there are big differences between the available history of the instruments. You mentioned that your ranking is based partially on the total performance. But if you look at the average annual performance you see that for example hangseng has a annual performance of 39% (based on the last 10 years) and coffee is 16.5 % (in 39 years).

Just as an idea for another performance criteria.

I am looking forward to see the rest of the systems. I will try to check how consistant the annual performance for the instruments is by calculate it for the single years.

mfg

flo

Dear Reiner. During the test of a more conservative management code, where I still add more position accordingly to the equity size I came across a small issue I could not explain. To simplify things the same issue is confirmed if I just adjust the max positionsize for 3 instead of 15 in the DAX V6. The issue is that the conservative closed the 2 position today at 9:01 and the original are still going with 4 position. Both codes started at 21 Dec. 9:00 with 2 positions. later the original added 2 pos at 23 Dec 9:00. I backtested manually both code and I can see the issue is ongoing- but not every time. I could understand if the original V6 DAX closed 2 of the 4 position today at 9:00 it would result in closing of all the 2 position today, but that’s not the case. Do you have any Idea of why this is happening? Maybe you could explain the exit strategy in details, or just say if you already have, I will find it 🙂

This is the changed lines

maxPositionSizeLong = MAX(3, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(3, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

Cheers Kasper

Update. I think I know why. when looking at the exit conditions, there is a

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

The posprofit would be higher with double the size of countofposition- so that why we are closing before the Original V6 DAX. but when I set out for making a more conservative code, I didn’t expect it to be on the gain side :-s Just a quick look and knowing that you properly optimized the exit strategy(maxCandlesLongWithProfit) I actually think that the original posProfit is general with higher gain. I would be nice if adjusting the maxposition size, still would follow the original posProfit -accordingly, other vice we are not only dealing with profit limited by positionsize but also missing out of profit because getting out to soon. Does this make sense?

Hey guys,

I tried to adapt the dow to version 6

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// Version 6

// Instrument: DAX mini 4H, 9-21 CET, 2 points spread, account size 10.000 Euro, from August 2010

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define intraday trading window

ONCE startTime = 90000

ONCE endTime = 210000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 7

// define filter parameter

ONCE periodLongMA = 160

ONCE periodShortMA = 5

// define position and money management parameter

ONCE positionSize = 1

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

ONCE stopLossLong = 5.5 // in %

ONCE stopLossShort = 1.5 // in % 1.5

ONCE takeProfitLong = 1.5 // in % 2/1.5

ONCE takeProfitShort = 0.5 // in 0.5%

maxPositionSizeLong = MAX(10, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

maxPositionSizeShort = MAX(10, abs(round(maxRisk / (close * stopLossShort / 100) / PointValue) * pipsize))

ONCE trailingStartLong = 1.25 // in %

ONCE trailingStartShort = 0.75 // in %

ONCE trailingStepLong = 0.2 // in %

ONCE trailingStepShort = 0.2 // in %

ONCE maxCandlesLongWithProfit = 17 // take long profit latest after 17 candles

ONCE maxCandlesShortWithProfit = 3 // take short profit latest after 4 candles

ONCE maxCandlesLongWithoutProfit = 40 // limit long loss latest after 40 candles

ONCE maxCandlesShortWithoutProfit = 11 // limit short loss latest after 11 candles

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3//3

ONCE January2 = 1//1

ONCE February1 = 2//2

ONCE February2 = 1//1

ONCE March1 = 2//2/3

ONCE March2 = 3//3

ONCE April1 = 2//2

ONCE April2 = 0//0

ONCE May1 = 0//0!

ONCE May2 = 0//0!

ONCE June1 = 3//3

ONCE June2 = 3//3

ONCE July1 = 0//0

ONCE July2 = 0//0

ONCE August1 = 0//0

ONCE August2 = 0//0

ONCE September1 = 3//3

ONCE September2 = 3//3

ONCE October1 = 0//0/1

ONCE October2 = 3//3

ONCE November1 = 1//1

ONCE November2 = 3//3

ONCE December1 = 1//0/1

ONCE December2 = 3//

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate weekly high/low

If DayOfWeek < DayOfWeek[1] then

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

// calculate monthly high/low

If Month[1] <> Month[2] then

//If Month <> Month[1] then

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

If Time < startTime then

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

EndIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal multiplier

currentDayOfTheMonth = Date - ((CurrentYear * 10000) + CurrentMonth * 100)

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF ( (l1 OR l4 OR l2 OR (l3 AND f2)) AND NOT alreadyReducedLongPosition) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry without order cumulation

IF NOT SHORTONMARKET AND ( (s1 AND f3) OR (s2 AND f1) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

IF (COUNTOFPOSITION + (positionSize * ABS(saisonalPatternMultiplier))) <= maxPositionSizeShort THEN

SELLSHORT positionSize * ABS(saisonalPatternMultiplier) CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

SELLSHORT positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function (convert % to pips)

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

stopLoss = stopLossLong * 0.1

takeProfit = takeProfitLong * 2

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

IF LONGONMARKET THEN

SELL AT newSL STOP

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT newSL STOP

ENDIF

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

ENDIF

Correction: “The posprofit would be higher with double the size of countofposition- so that why we are closing before the Original V6 DAX.”

The posprofit would actually be lower with the double size of countofposition- at least in the latest exit.

Sorry about the mistake.

Perhaps can open individual forum for each indices/commodities (even forex), making it easier to follow the indices/commodities you are interested in trading now or maybe in the future, and for new members to pick up too.

I approve! Maybe we could put this as a rule: create individual topic for each different instrument version of Pathfinder. This is Reiner’s topic, so I think he may also have something to say about this idea.

But if you look at the average annual performance you see that for example hangseng has a annual performance of 39% (based on the last 10 years) and coffee is 16.5 % (in 39 years).

Good point! Normalized annualized performances should be used in this case. I believe anyone could do this calculation with the Excel file, Reiner has shared.

I like to have everything in one topic. it is easier to stay uppdated and a lot of the things that are discussed here are general for all the systems.

just my opinion…

@flowsen123

I am having trouble getting anywhere close to your backtest.

I can only test from 30 aug 2012 and only get 57 trades (+48/-9) with time changed to 23.00 (instead of 21.00) and spread 2.8.

It seems as though I have done something wrong…

Regards, David