I’ve just opened a manual Long trade on Chicago Wheat because I think the market structure is right for an UP period.

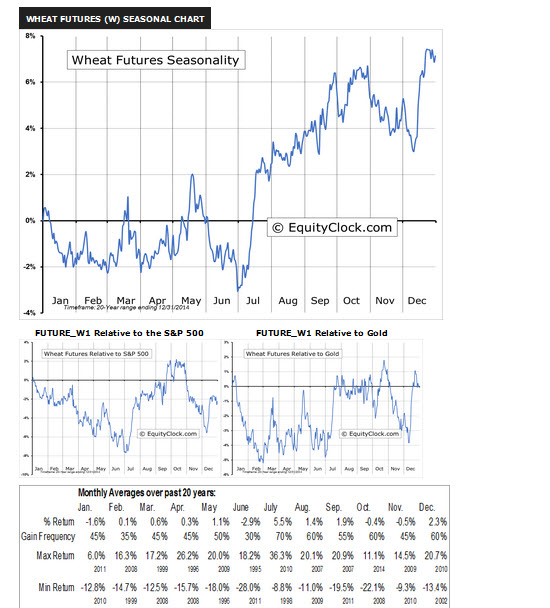

I thought I’d check on ‘wheat seasonality’ and I see that July is a good month historically … see attached.

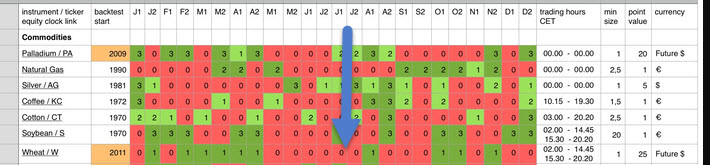

I then looked at the matrix on Page 1 for wheat seasonality and I note wheat gets a ‘0’ in July … see attached.

Am I reading something wrong or anybody got any thoughts please?

Thanks

GraHal

Gold closed long at 1am at 1200.1, loss from 1235.5.

@Patrick and everyone else interested

I got the answer from my IG contact that both CAC 1€ and EU Stocks50 1€ will be removed from PRT.

Best regards, David

@dajvop thank you

Your chart is 20 years to 2009 and my chart is 20 years to 2014. You wouldn’t think there be so much change in overall 12 month profile in 5 years?

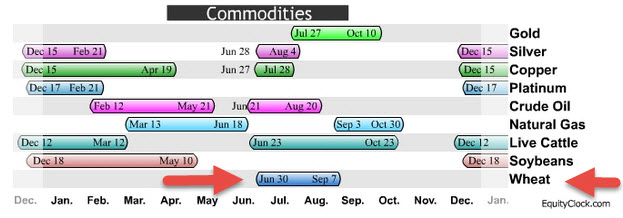

But there is also attached on equityclock.com shows latest on Seasonality … in their words

Identified below are the periods of seasonal strength for each market segment. Each bar will indicate a buy and sell date based upon the optimal holding period for each market sector/index.

Cheers

Grahal

PS How did you embed that chart in your post? I don’t appear to have that option (tried copy & paste and ctrl v etc)

Hi Grahal,

The page looks useful but unfortunately it is not solving the problem because the structure of the two codes are very different.

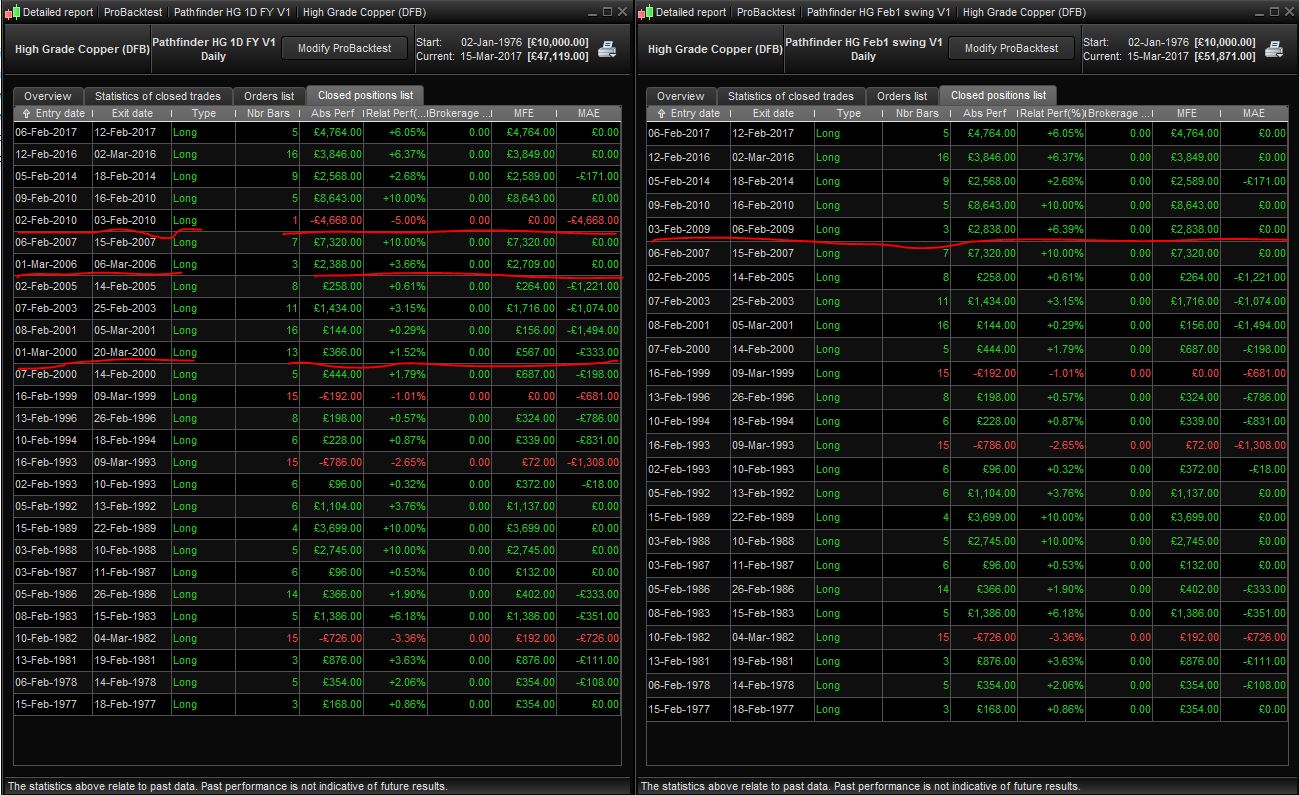

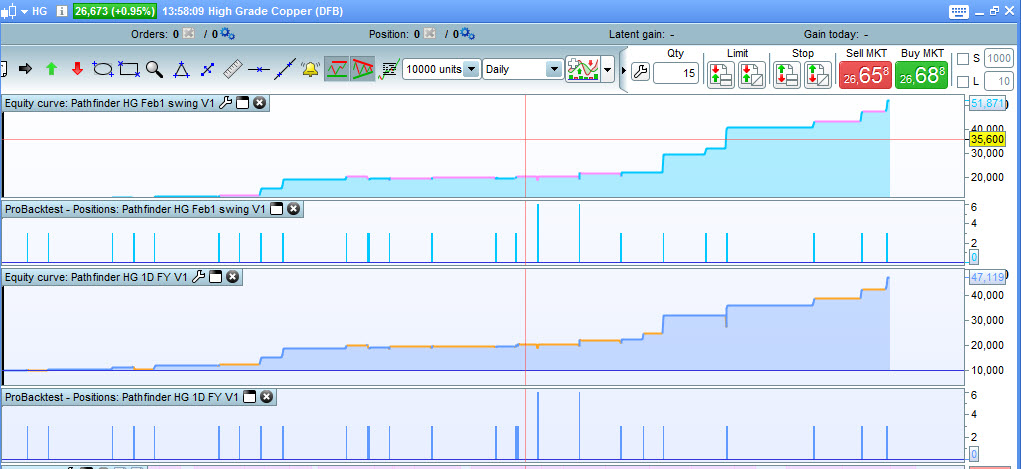

Attached again for a like for like comparison, the individual month of Feb1 and the full year algo, which only trades in the first half of February.

Would be nice if somebody could have a look because I think it would be very beneficial to use only a full year algo at the end of the day. (If we once finish the full year for all indices and commodities)

Regards

Oliver

Ah yeah I see what you mean O-jay8 … there’s ‘too much difference’ for the Code Diff checker to be useful.

Surely the Feb only version has to be better as there’s loads less Drawdown?? I’d be more comfortable with the Feb1 version … or am I missing something?

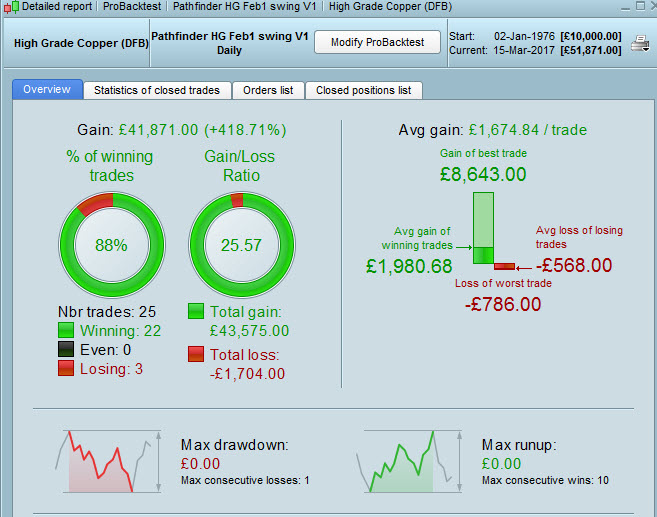

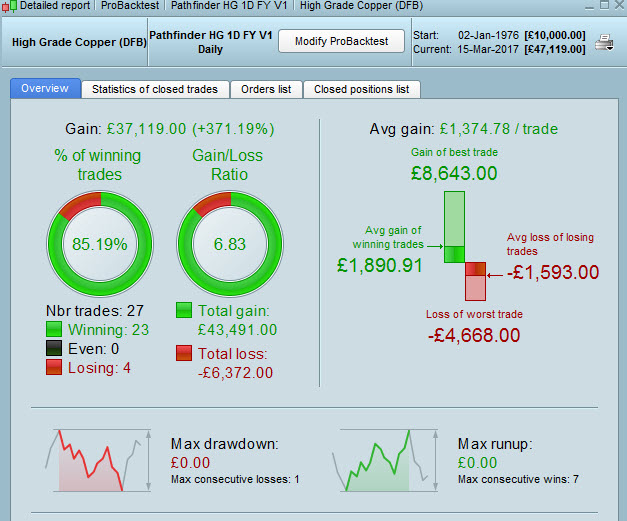

See attached for comparison since 2 Jan 1976

GraHal

[attachment file=”28640″]

[attachment file=”28641″]

Ignore 2 screen shots above showing zero drawdown (I didn’t wait for the PRT server to compute the figure).

2 on the right do show DD.

Attached are the curves for Feb1 and FY … very similar, but with 2 more trades in the FY system.

So what conclusion do we draw O-jay8 ?

GraHal

As you can see in my screenshot, highlighted with a red line, the FY V1 has 3 trades which do not occur for the Feb1.

And the Feb1 has one trade which does not occur in the FY V1.

The question is why, because in my opinion the results of the code should be the same. Only the structure is different.

Until we sort this out, I would of course rather trade the individual month of Feb1.

As it was the approach of Pfeiler with the full year algo, I would like to hear his opinion on this matter as well.

@ GraHal, another question, as I do spread betting as well, what do you use for corn and chicago wheat, DFB?

Regards

Oliver

@ojay: All I can offer right now is this link with an updated FY algo:

https://docs.google.com/spreadsheets/d/1pBoKX44kX_GSzHNc0CgueKdZAuWBCnauoK_bh8ht6j8/edit?usp=drivesdk

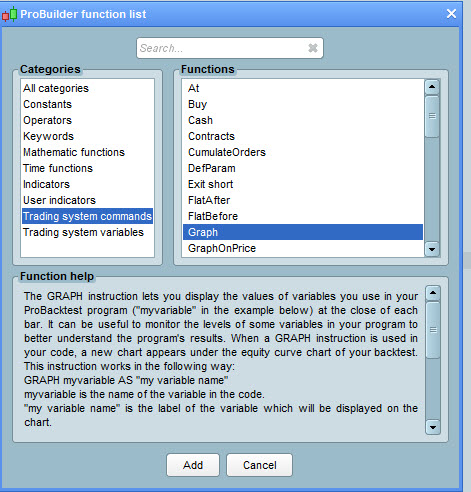

Please have a look at the calculation of ‘midofmonth’. The prt variable ‘Days’ does not count to the end of the month, so in this version it is calculated again (still not perfect but better, as you can see with the prt graph function

Hope this helps.

@ O-jay8 you’d need to isolate the 3 trades that are different and then examine the triggers and check out what is going on?

Use the GRAPH Function to isolate triggers … see attached.

Corn (DFB) Code C and Chicago Wheat(DFB) Code W … is that what you mean?

GraHal

@O-jay8

I have noted the following differences that does not appear in the other version:

FY: 2000-03-01, 2006-03-01, 2010-02-02

Feb1: 2009-02-03

Even though March1 is set to 0, there are 2 trades in that period for the FY version.

The differences in drawdown comes from the 2010-02-02 trade which was a loss.

@dajvop gold is still open for me!

@Bandido

Please upload your version.

Best regards, David

@dajvop

// Pathfinder Trading System based on ProRealTime 10.2

// Breakout system triggered by previous daily high/low crossings with smart position management

// Version 2 - long only

// Instrument: GOLD mini 1D, 0.3 points spread, account size 10.000 Euro

// Rating c

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5

ONCE periodSecondMA = 10

ONCE periodThirdMA = 6// x1 //nr 1 (between 1 -10)

// define filter parameter

ONCE periodLongMA = 10//x2 //nr 2 (check values beetween 10 -100)

// define position and money management parameter

Capital = 10000

Risk = 5 // in %

equity = Capital + StrategyProfit

maxRisk = round(equity * Risk / 100)

x= 1

PositionSize = x

ONCE stopLossLong = 5 //x1 nr 3 (between 5-10) in %

ONCE takeProfitLong = 5.25 //x2 nr 4 (between 3-10) in %

maxPositionSizeLong = MAX(15, abs(round(maxRisk / (close * stopLossLong / 100) / PointValue) * pipsize))

ONCE maxCandlesLongWithProfit = 11 //x1 nr 5 (between 5 - 15) take long profit latest after x candles

ONCE maxCandlesLongWithoutProfit = 14 //x2 nr 6 (between 5 - 15) limit long loss latest after x candles

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 0

ONCE January2 = 0

ONCE February1 = 0

ONCE February2 = 0

ONCE March1 = 3

ONCE March2 = 0

ONCE April1 = 0

ONCE April2 = 0

ONCE May1 = 0

ONCE May2 = 0

ONCE June1 = 0

ONCE June2 = 0

ONCE July1 = 0

ONCE July2 = 0

ONCE August1 = 0

ONCE August2 = 0

ONCE September1 = 0

ONCE September2 = 0

ONCE October1 = 0

ONCE October2 = 0

ONCE November1 = 0

ONCE November2 = 0

ONCE December1 = 0

ONCE December2 = 0

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// set saisonal multiplier

currentDayOfTheMonth = Date - ((CurrentYear * 10000) + CurrentMonth * 100)

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

// define trading filters

// use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

// long position conditions

l = signalline CROSSES OVER dailyHigh

// short position conditions

s = signalline CROSSES UNDER dailyLow

// long entry with order cumulation

IF (l AND f2) THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

IF (COUNTOFPOSITION + (positionSize * saisonalPatternMultiplier)) <= maxPositionSizeLong THEN

BUY positionSize * saisonalPatternMultiplier CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

IF (COUNTOFPOSITION + positionSize) <= maxPositionSizeLong THEN

BUY positionSize CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry means close long position

IF (s AND f1) THEN

SELL AT MARKET

ENDIF

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m2) THEN

SELL AT MARKET

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit