Corn Long position was opened today 1/2am in Live @ 367

AleX

AleXParticipant

Senior

Here we are, what do you think?

@AleX

Personally I prefer your version since it has more trades for the few years available.

wp01

wp01Participant

Master

@Pfeiler,

Regarding the NG:

The code says minimum positionsize = 1, but the minimum amount of contracts to trade the mini NG at IG is 2,5.

So if you use the code for automatic trading a possible trade will be rejected due to the wrong amount of minimum contracts.

If you change the positionsize to 2,5 you get the following results:

PF: 11,27 vs 17,26 (1 contract)

DD: € 1.060 vs. € 886 (1 contract)

Regards,

Patrick

@Alex: Thx, you made a perfect comparison, to see which algo is preferable. You have successfully optimized PF-Swing for Mais. But the decision which algo we choose for the final package is not easy on these two. It very much depends on the risk/reward I am willing to trade.

Generally, I would like to stay under 1000€ DD, because if we are running 20 algos parallel and my budget is 20k, this would be enough for not getting blown out of my socks (help good I will not have to endure a 20k drawdown). But actually I am willing to risk a higher DD when the Gain% and Winning Trades% are exceptionally good.

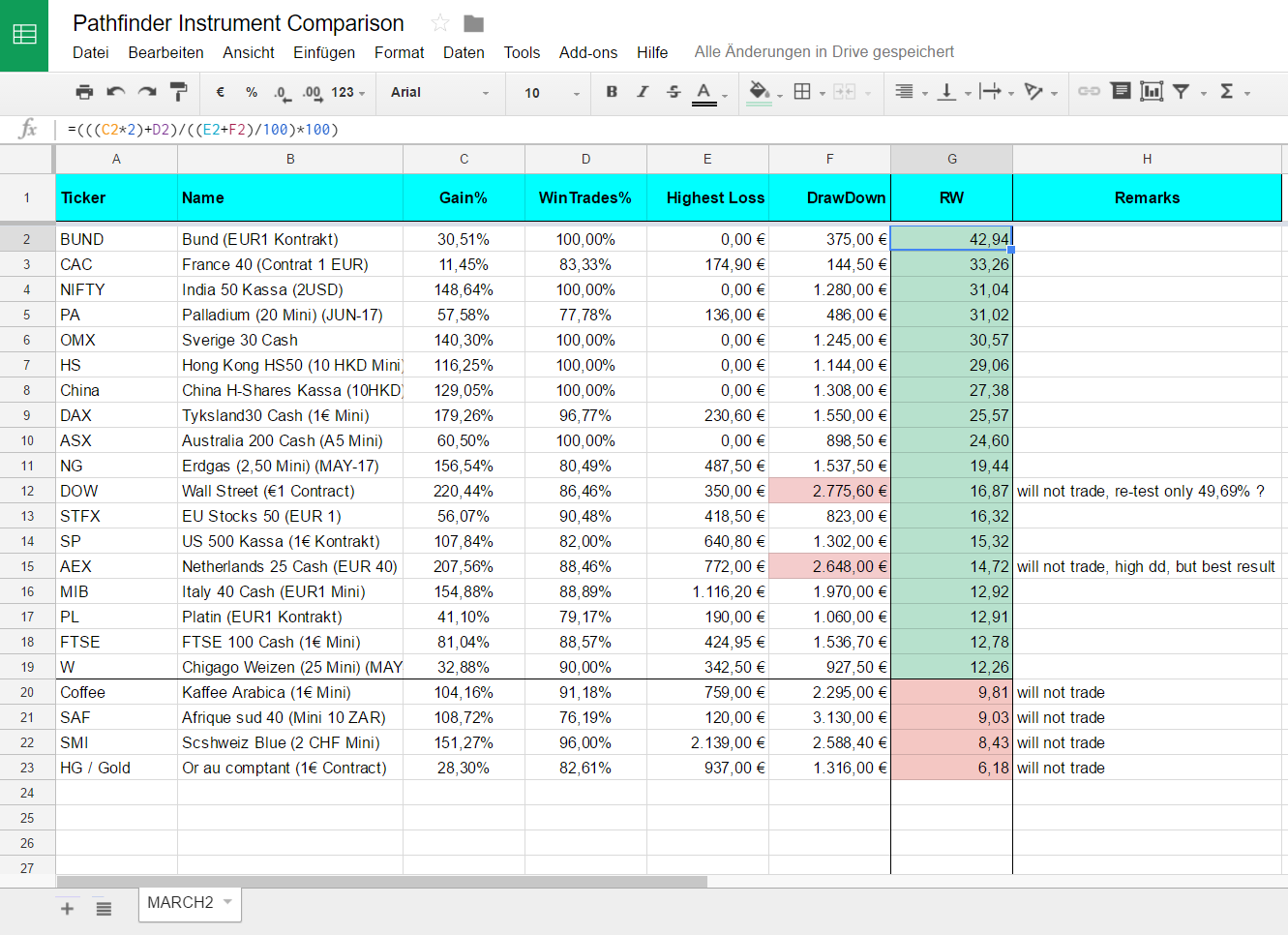

This would lead us to the following Risk/reward calculation, (RW = higher is better):

RW = (GAIN% + WINTRADES%) / DD%

So in the PL case:

Rainer Version: ( 57.58 + 77.78) / 4.86 = 27.85

Alex Version: (140.96 + 92,31) / 15.60 = 14,95

I know this is a very basic calculation and it very much favors a low DD. But since we are generating a lot of trades in a period, I would like to have a low drawdown.

As always, it is your decision. So I will make a directory /highroller with your algo Alex (and other algos with a high drawdown).

@Aloysius: Thx! I will move your SAF to highroller, since it has +100% but high DD.

@wp01: Thx for the advise for the min. contract for NG. The little details like this, is the reason, why it so much worth when we work together.

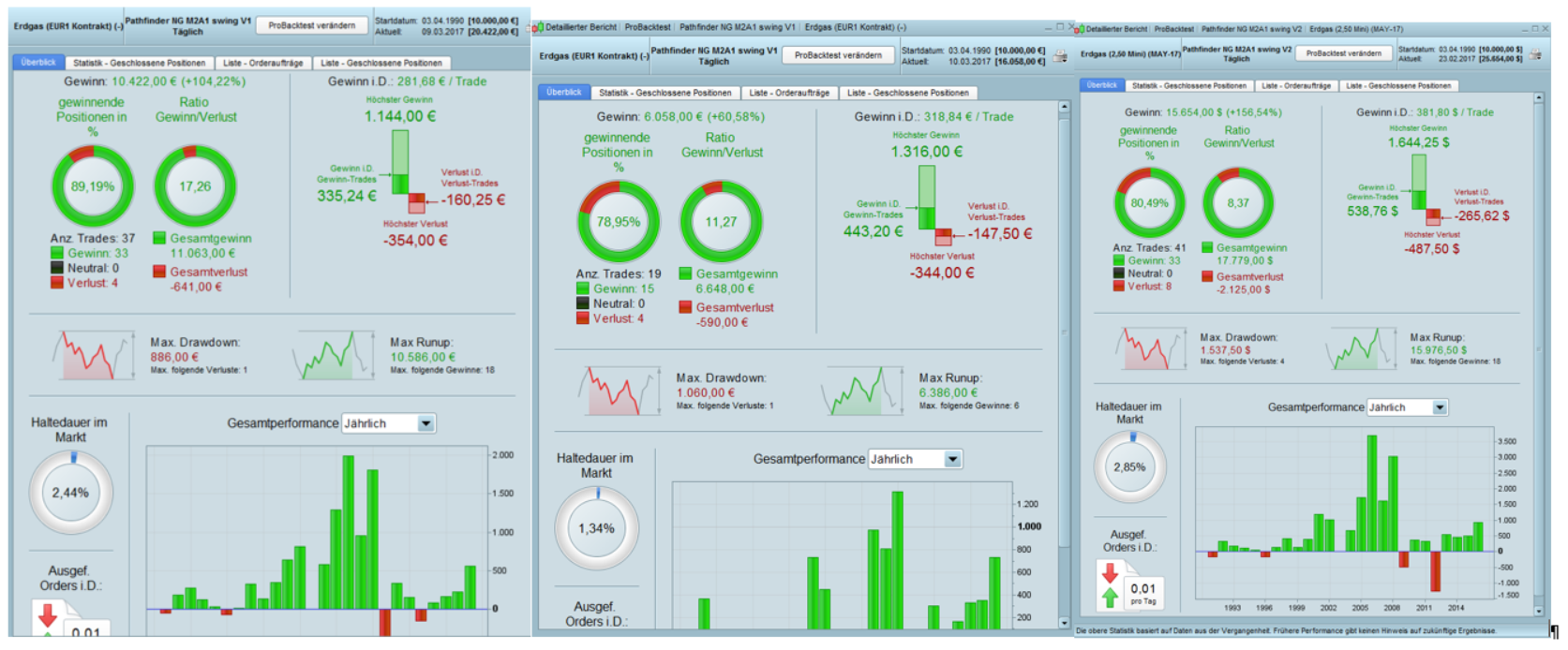

I checked the variations for NG, see attached image:

left=original: wont work

center=original with posSize=2.5: does not make sense with only 60% and 1k€ DD

right=Erdgas (2.50 Mini) (MAY-17): 156% and 1537€DD is definitly a highroller, but I will trade it unless we have a algo with less DD

I have uploaded the final package “Pathfinder Swing 03 MAR2 v02.ZIP” for MARCH2 in the Dropbox share (see link on first page or here).

Please check the attached package overview for more details and a (pretty alpha) risk/reward RW factor for comparison:

Link to overview

There are some modifications:

– new NG version (see post above)

– reduced DD for HS + SAF + DAX + NIFTY and moved the orig. algo to highroller (if you are a millionaire, this is your directory)

– couldn’t reproduce DOW results, but has a high DD anyway

All 16 algos from the comparison are running live on my account now.

Thanky you very much for your contributions.

Mark

MarkParticipant

Senior

Just a thought,

Has anyone been working on 1 algo per instrument? for example 1 algo for copper for the year, only active in the season according to the heat map? It would be much easier to manage than several different algos for for each instrument through the year.

China-H closed at 1am at 10066.3 with a loss.

Chicago Wheat long x 1 at 2am at 440.6.

wp01Participant

Master

Hi Mark,

The idea behind the roadmap is to find the best setups with the best potential chances for a profit. If you take a look at the roadmap you see a lot of red parts.

If you have a code optimized for the whole year you also have the periods optimized included with the red months where the potential advance for a profit is less than the

periods with lightgreen and darker green. For a full year optimalisation you also have to accept that the variables are also optimalized for the periods with less chances.

Regards,

Patrick

I started to ceate a algo for FY (full year) where you could put in the all numbers for the changing variables per season. It worked pretty good for PA .. but was horrible on other instruments.

I am still debugging to understand why it doesnt work, but can post a FY algo (beta) as soon as I am sitting in front of a pc again.

For the time being .. best and most reliable results come from algos per period.

MarkParticipant

Senior

@patrick

Yes im aware of the roadmap, i don’t mean create an algo that trades every month, i mean set the seasonality parameters to only trade the green of the roadmap using 0-1-2, but however this means the other parameters can not be set for each period. just wondered if it made much difference.

@Pfeiler

I also did a FY for palladium with very good results, this is why i mentioned it, i haven’t looked at any other instruments though

wp01Participant

Master

@Pfeiler,

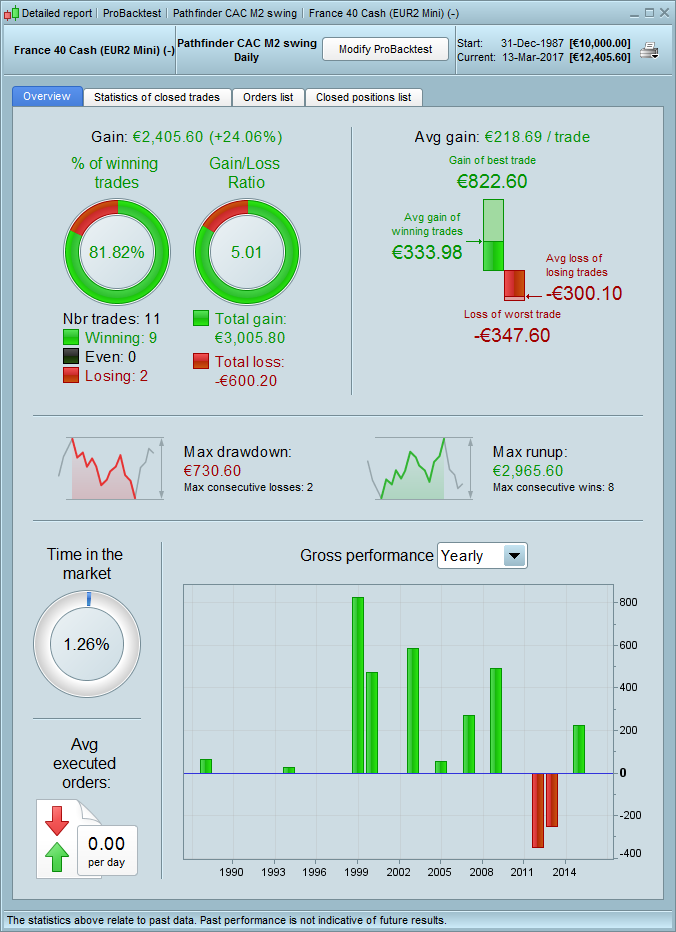

I have my doubts if you can trade the CAC EUR1 mini. It is in PRT, but i can not find it anymore in IG. I think it is deleted and you only have the EUR2 available for trading.

I don not think this is only in the Dutch version. But maybe others can check this as well.

If you adapt the code to the EUR2 you get the following results:

| CAC |

France 40 (Contract 2 EUR) |

24,06% |

81,82% |

347,60 € |

730,60 € |

12,05 |

Regards,

Patrick

@Patrick

In Sweden it is still available.

Best regards, David