Hello everyone,

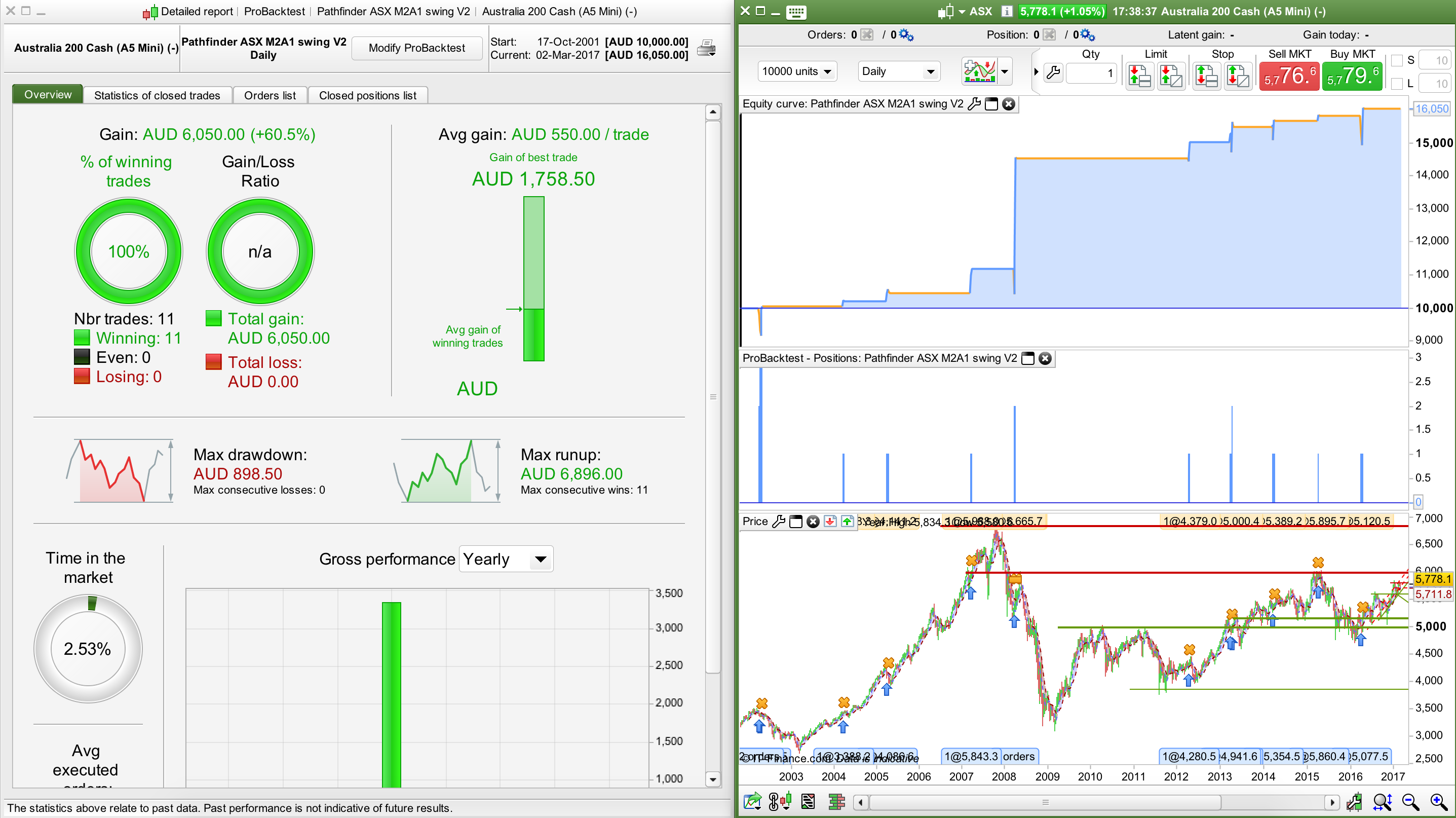

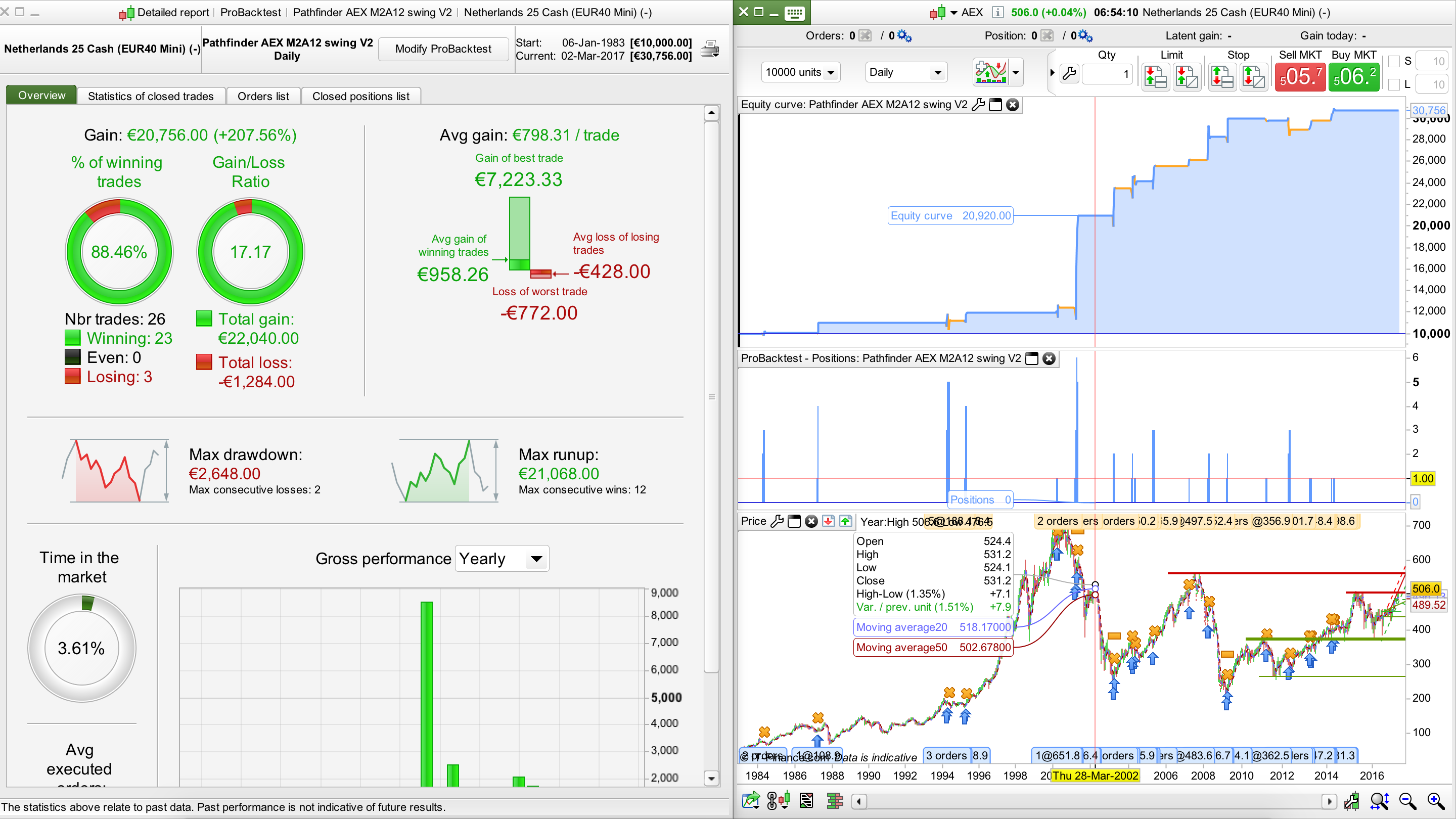

Firstly – big thanks to Reiner for sharing his work and to everyone that has since contributed. My friend (Billy) and I have been lurking in the forum shadows for a while now and think it is about time we offer to help out. We have completed most of the instruments for the upcoming season and thought we will share a couple. Note that we are more concerned with limiting the drawdown than making big profits as we have small accounts sizes, hence we sometimes choose slightly lower profits in favor of low DD – ASX being an example (attached). Our season multipliers are set to 1 as a default – again to limit the DD – but also to make comparison easy between different algos for the same instrument. Note this when comparing AEX (attached).

One thing I am unsure about is what version to use – I saw a while ago Reiner posted V2 and I have been using that, however everyone still seems to be using V1 – can someone please clarify?

Let me know your feedback on attached algos (chances are I’ve made a mistake) and if all is good I can post more.

Again – thanks for everyone’s input and look forward to working on this project with everyone!

Cheers

Jaco

@Patrick thanks for your last one. Below is what stuck in my mind, posted by Pfeiler here https://www.prorealcode.com/topic/pathfinder-swing-ts/page/35/#post-26612

Below left me thinking what happened to that 8.8 points difference / gap between March and May Corn Contracts? Or is below a typo and it should be 358.55?

27 Feb 2017 20:53:09 “Mais (MAR17)” closed long 1x @ 359.75 @ live system with -490,23€ profit

27 Feb 2017 20:53:09 “Mais (MAY17)” opened long 1x @ 368.55 @ live system

Thanks

GraHal

@GraHal

My Corn algo had the same, though my loss was 517 €.

we’ll trade futures only if a suitable mini contract isn’t available or mini contract has no data history. Rollover is something that we should avoid in the future because of losing algo monitoring.

@Patrick

do you mean the PF excel? There is or was a problem with the forum software with uploading excel sheets. Nicolas made a hotfix in the meantime and I’ll try to upload it again.

@Reiner

Another solution is to set that part of the month preceding the swith to zero.

I.e. trading February 1, but not February 2.

wp01

wp01Participant

Master

@GraHal,

Differences in futures has to do with the time until the future expires and the market spotprice.

The future is always related to the spotprice and the time till expiration. I’m not the expert, but i thought

it is the opposite of backwardation (contango). Attached a link with an explanation.

Maybe someone knows more about this than i do and can correct me if i’m wrong.

http://www.investopedia.com/terms/b/backwardation.asp

It is not your loss or profit when the future rolls over to the next month. You just have a new situation.

The movement from 8,8 points was also adjusted to the stoploss

and the takeprofit.

Regarding the results; maybe i was not completely clear:

Corn: future March loss -/- € 490,28

Wheat: future March loss -/- € 883,36

Corn: future May profit € 659,37 (rolled by IG and manually closed by me 28/02)

Wheat: future May profit € 588,97 (rolled by IG and manually closed by me 28/02).

All above trades was loss of € 125,30.

I hope it is clear.

Patrick

wp01Participant

Master

@Reiner,

It is actually an other forum, sorry moderator..:-) but in your resultoverview this morning it didn’t show a position in the DAX.

And the DAX Pathfinder 1 hour took a position yesterday at 18.00 hours. ( 12.064 ; at all time high….lol…..)

You once said that you also had the DAX hour running. It is not in your demo, so did you stop it and if you did why?

Thanks.

Patrick

@Patrick

For the track record I let run only all 4H and swing robots in my Pathfinder swing demo account

wp01Participant

Master

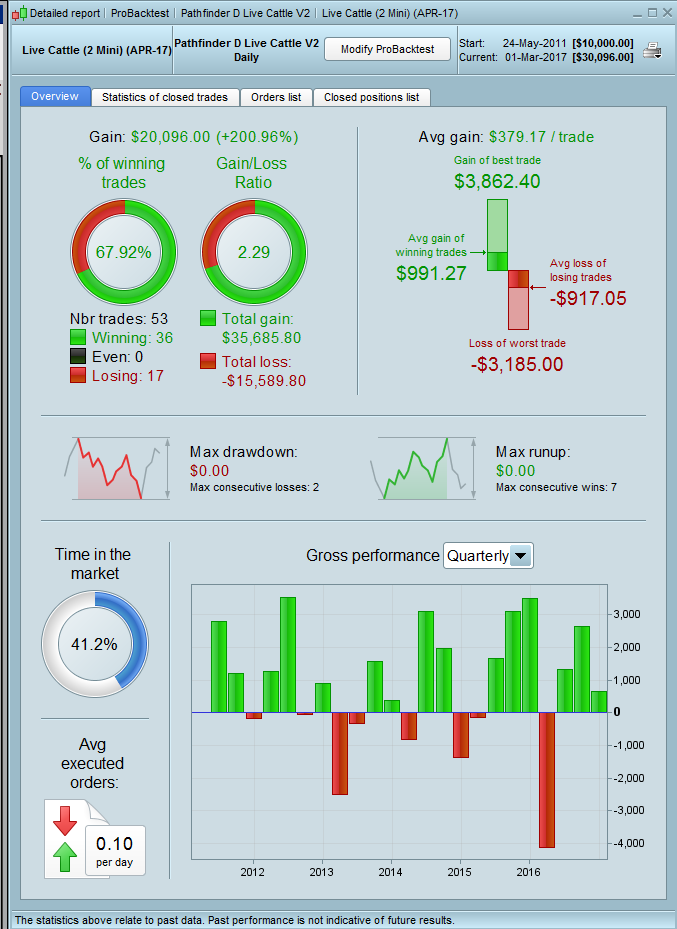

@Reiner,

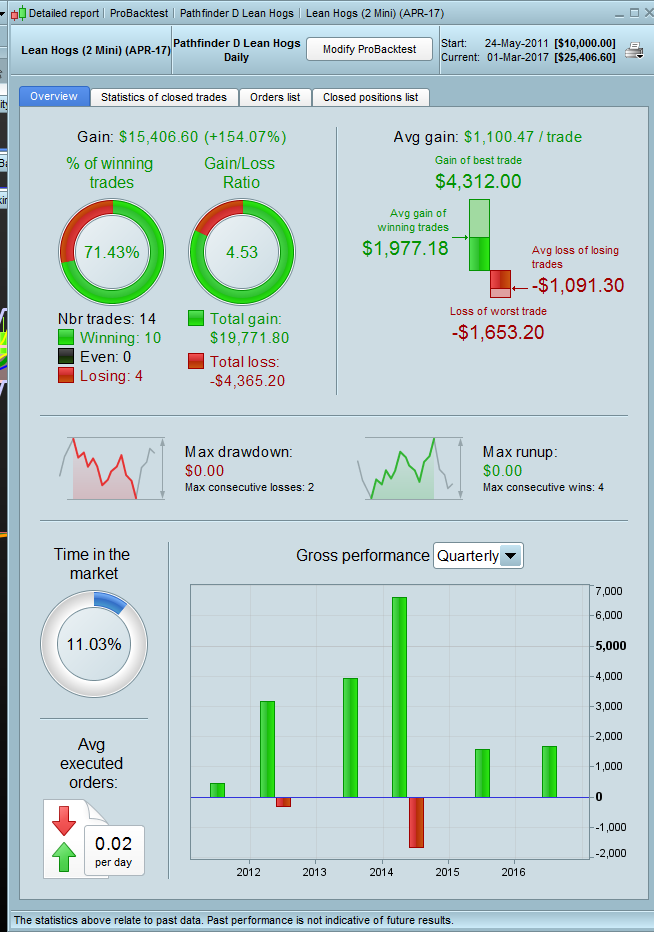

I’ve tried to make something from Live Cattle and Lean Hogs according to your seasonality.

http://charts.equityclock.com/live-cattle-futures-lc-seasonal-chart

I took for both the april future. In the June future (we need for the upswing there is less trade at the moment)

For Live Cattlte there is also a 1-EURO contract but with less history (06/’14).

For both futures the history goes back to 06/’11.

The normal tradinghours is from 15.30 till 20.05 CET.

Unfortunately my results are not as good as i hoped for. I hope you can improve it.

Best regards,

Patrick

Hi Jaco and Billy,

Welcome on board.

V1 is still the baseline for the robots. With V2 I have introduced an average down mechanism with a much better performance but also with higher drawdowns.

I’ll check your robots.

Best, Reiner

Alco

AlcoParticipant

Senior

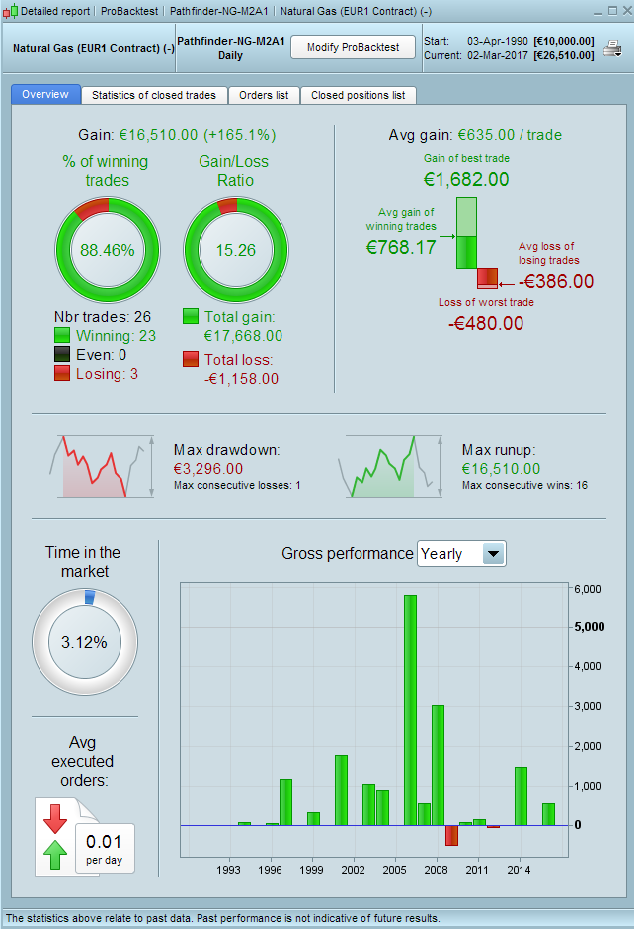

Hi Guys,

Here I have the results for natural gas.

Alco

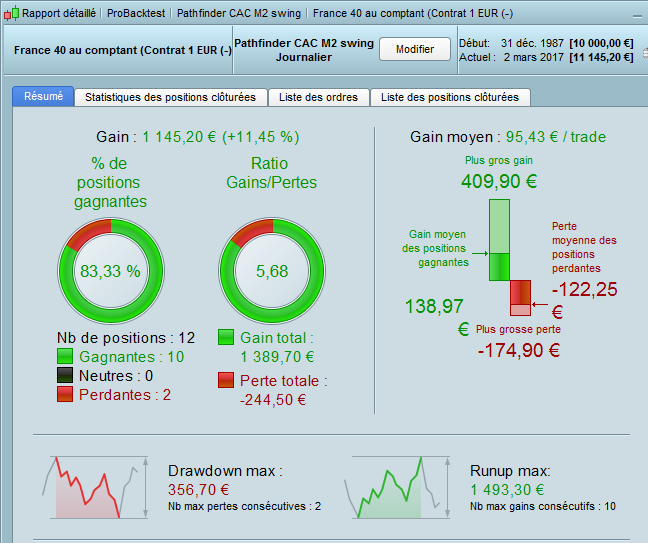

Hello,

Here is the swing CAC for March2..

Not so good, very few trades..

Arno

ArnoParticipant

Average

Hi Reiner,

We know that we have a statistical advantage to buy the market with Pathfinder swing TS entry. We known that a downward strategy averaging (inverted pyramid) is effective in this context of high probability of rise. When the p&n is negative following a Pathfinder swing TS entry, it would be interesting to take a second position at a lower price while respecting the pathfinder stops loss. I’m currently manually testing this idea.

What do you think ? It is an alluring idea no ? I don’t know well coded and i would like to know if you have tested this idea or if it’s already integrated to Pathfinder swing TS ?