As always Reiner, thanks very much for sharing this and your hard work. Looks quite promising.

I noticed that there are a few big outliers in the results with respect to the length of time in the position. I was wondering whether it may make sense to limit that time and see what the results are ? 100 bars perhaps or even lower given that the average duration is around 23-25 bars. For eg. having a look at the top 5 longest duration positions, cutting them off would possibly reduce the overall profit by a small amount but they also experienced fairly large drawdowns in those positions as well so it depends at what point in the cycle they were cut off. The reason for limiting the time in the market is is that after taking into account overnight financing fees which we all have to pay, those top 5 would have perhaps resulted in losses rather than profits due to their exceptionally long duration.

Reiner

Haha keep sharing your magic!

I see. Not so strange then, could have saved you some time by reading the code 😀

@manel

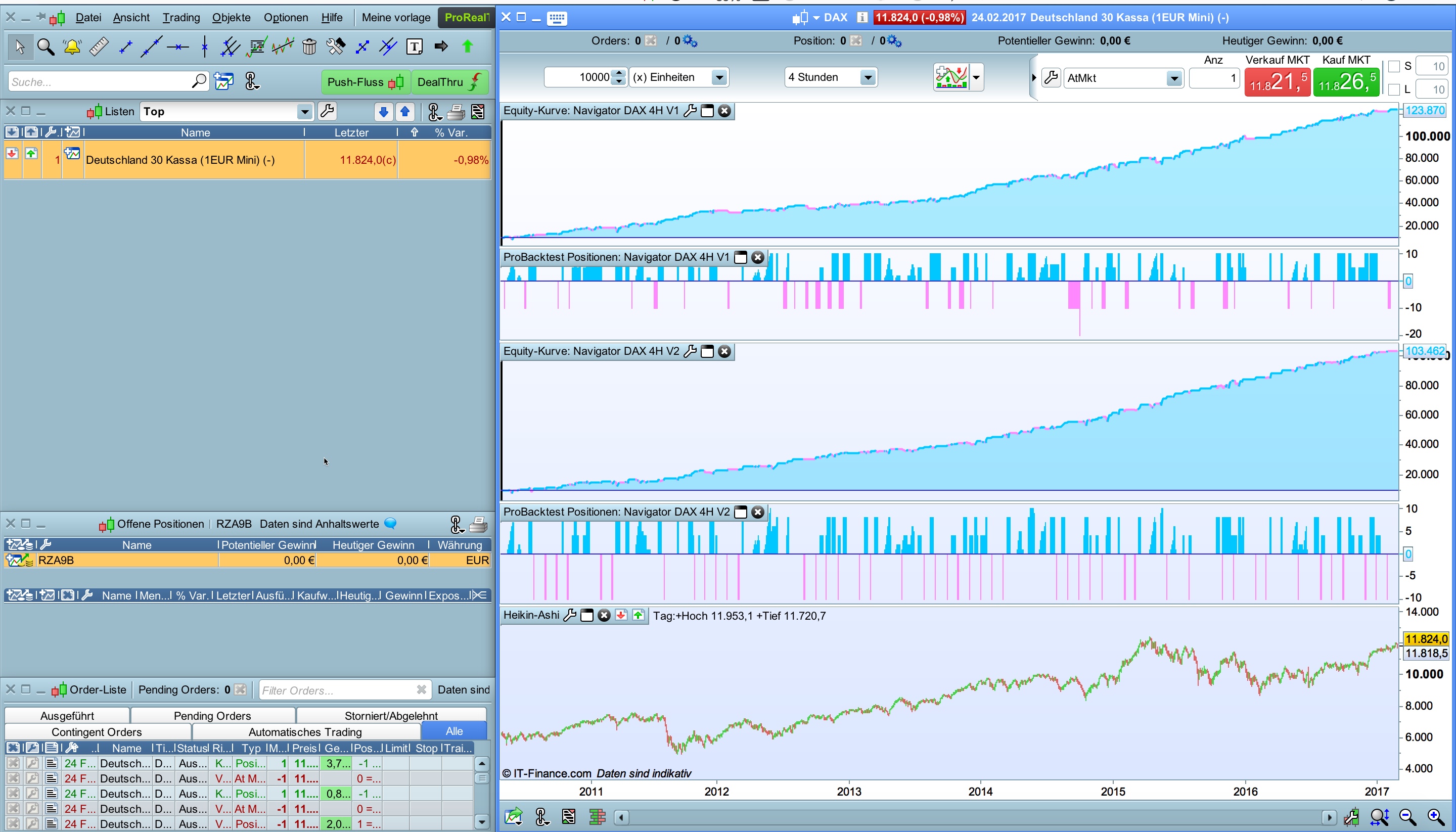

Navigator looks like a holy grail but of course it isn’t. The system has two issues:

- As you have already recognized, Navigator is relatively long time invested (in average 50% of the month) and this means significant overnight costs for cfd’s and potentialy a higher drawdown risk

- high stop loss value for long positions, backtest shows moderate losses but also a significant max drawdown which I really don’t like

In my opinion the Eurex 5 Euro mini future is a good instrument for that idea (no costs and suitable for accumulation) but of course requested this instrument a higher account size. I already reduced the drawdown with an averaging down mechanism but this does not solve all issues.

I’m still working on the system and as you also confirmed it looks really promising. I’ll verify your suggestion regarding maximal candle monitoring.

Best, Reiner

Thanks Reiner. I agree, the high draw is something I was not comfortable with as well and the wide stop losses give rise to higher volatility of running P&L which some may find hard to handle. But it’s early days yet, we can try and improve it as we go along, I’ll think of other ways as well. Your suggestion for using a future instead of cfd or spreadbet (if it makes tax sense to the individual) may be a good idea for some people here to avoid the holding costs.

@manel

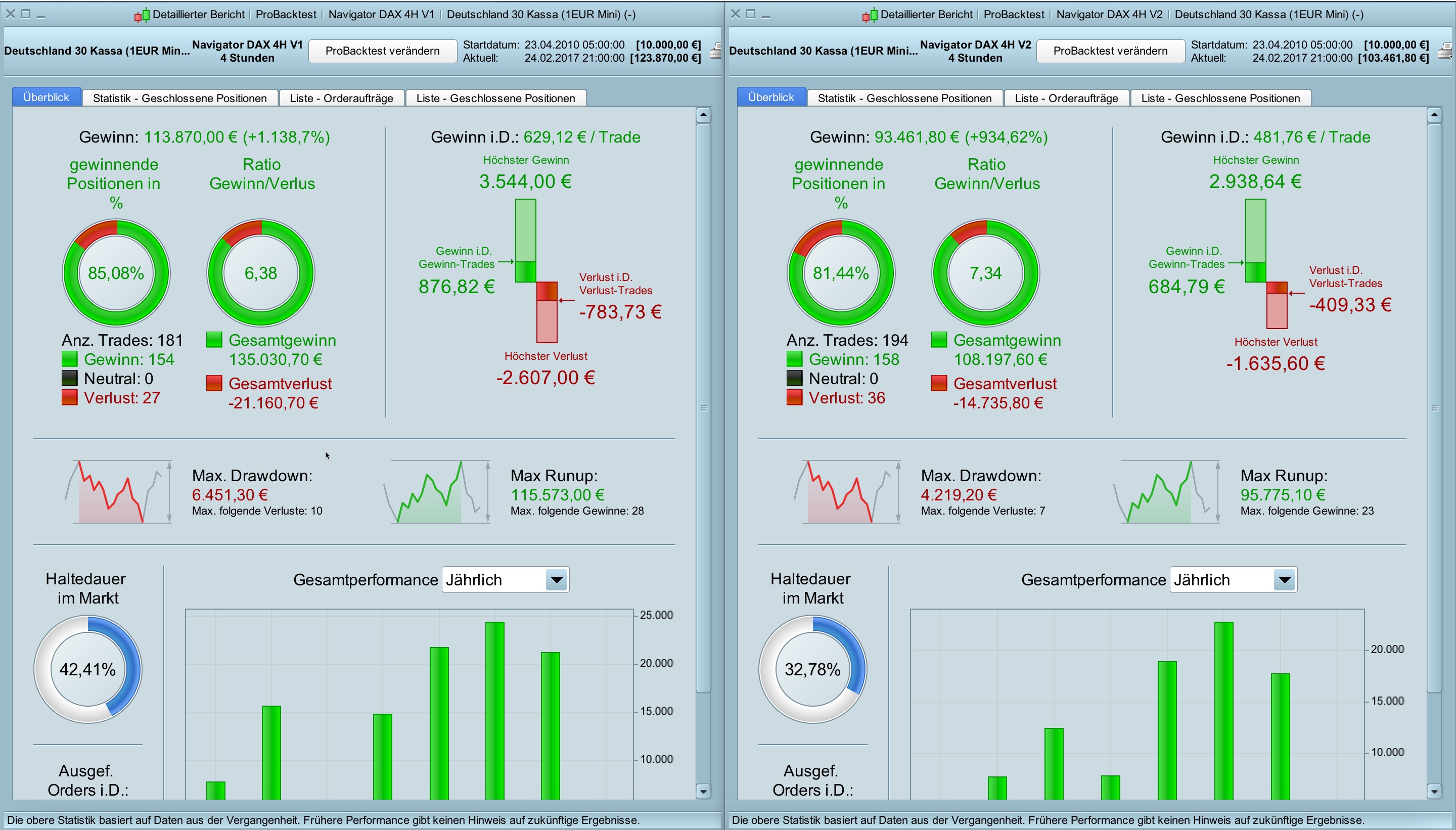

I have tested your suggestion. A maximum candle monitoring function reduce the time from 42,4% to 32,8%. Gain and number profitable trades are a little worse but max drawdown and highest loss are significant better. Equity curve is smoother as well.

I have adjusted all parameters with the aim to have the lowest drawdown. The question is what is the better approach?

Best, Reiner

Comparison of Navigator 4H V2 vs Pathfinder 4H v6 + 1D v3

(only on 100.000 bars)

Reiner……First of all a big thank you for the very important code!.

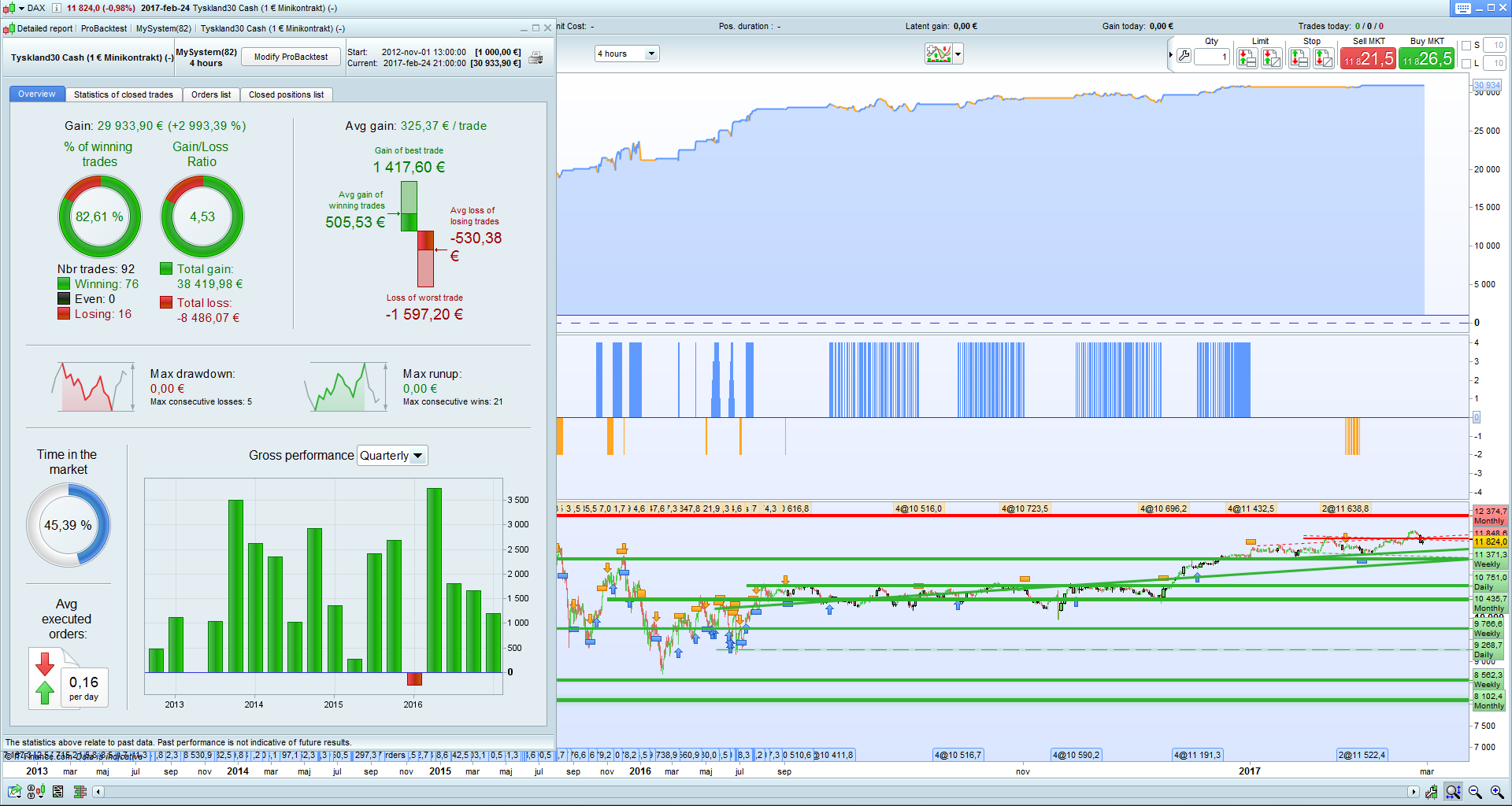

I add to Demo and wait .This is results for small Account 1000$.

i have live on demo and i wait for the first order to see if backtest is the same that live ….

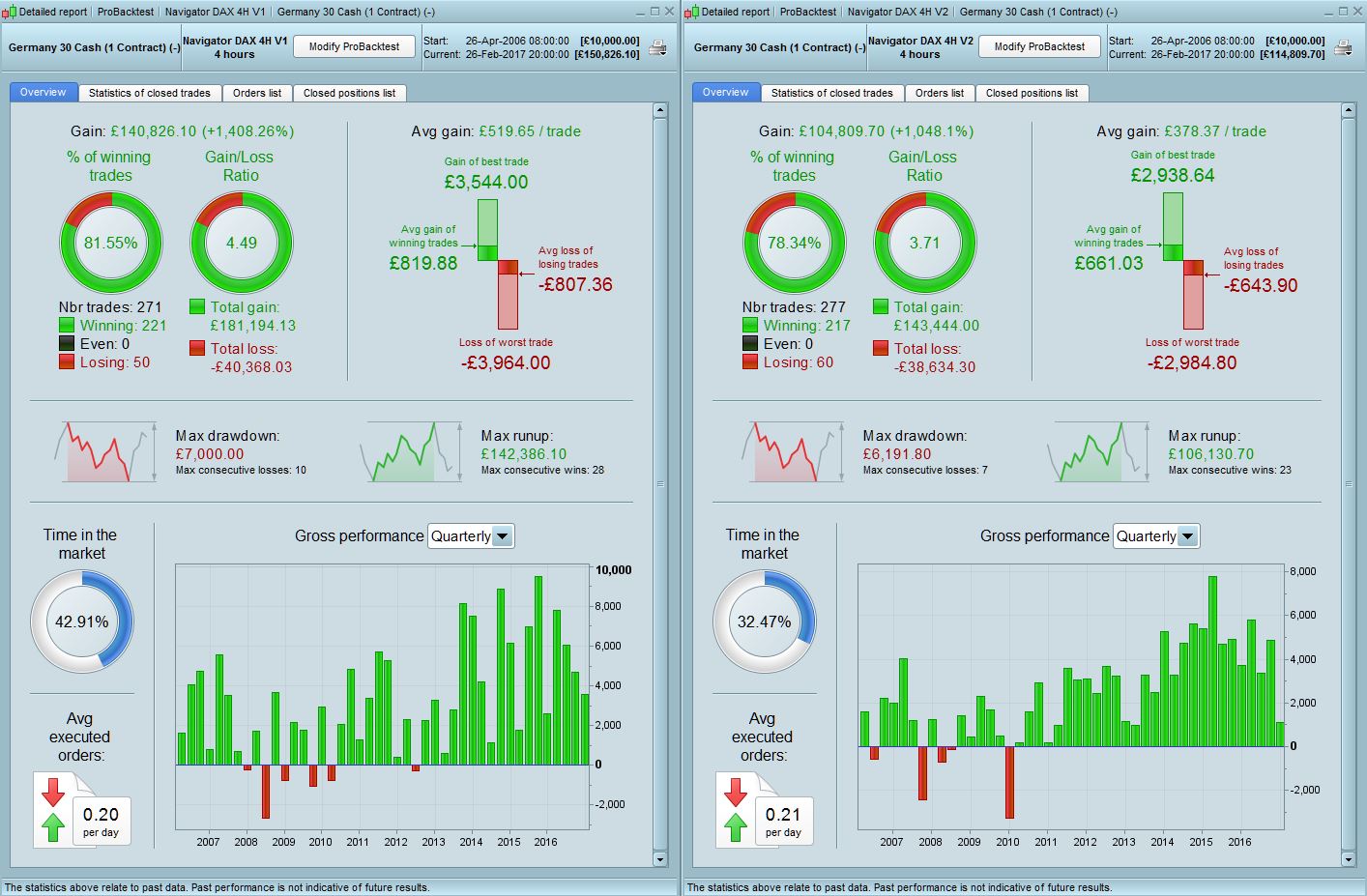

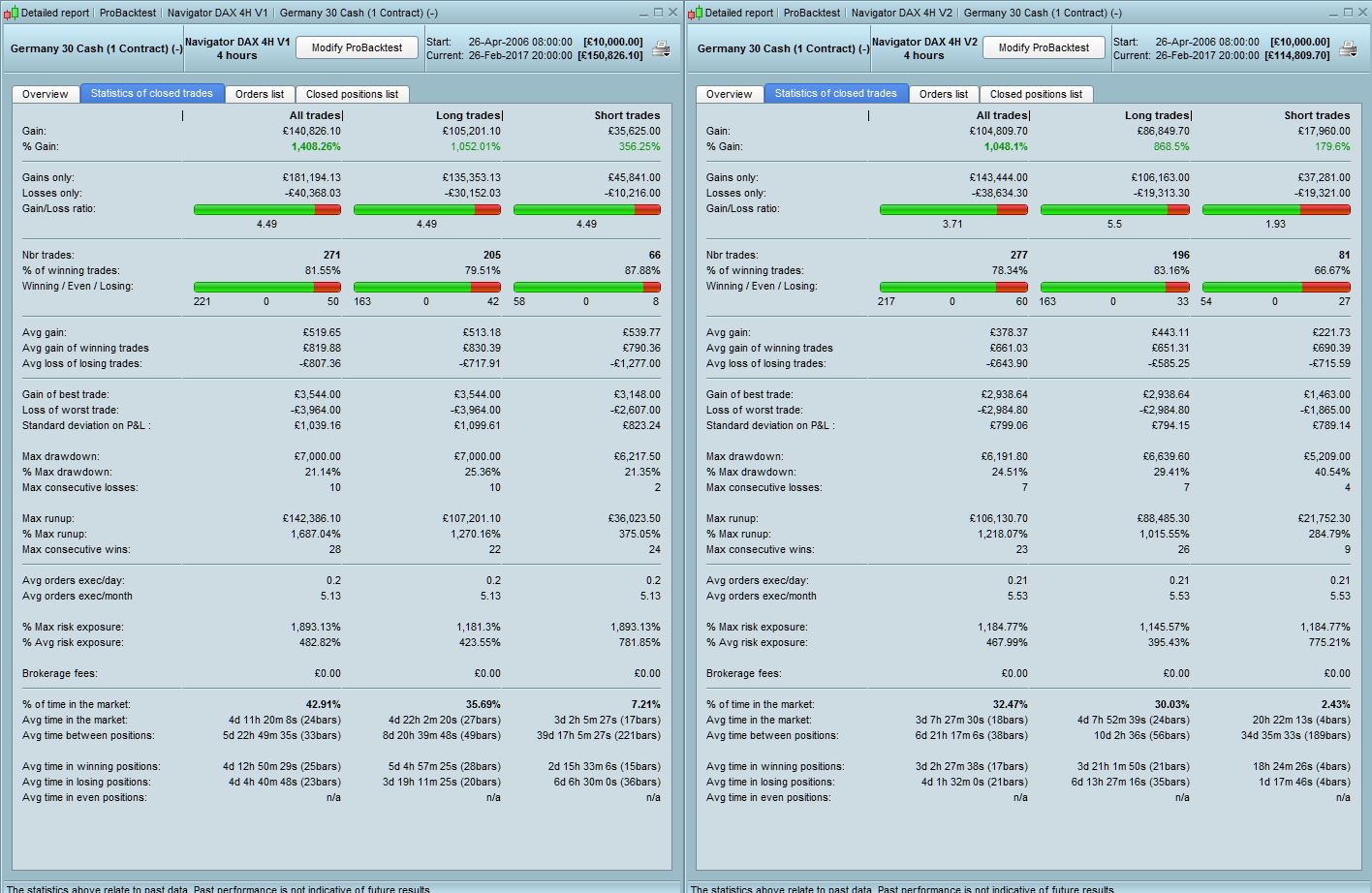

Reiner – Thanks for the adjusted v2 code. I have tested it over a longer period (04/06 – today) and results are shown below. There is not much difference in terms of draw (21% for v1 vs 24.5% for v2), but the max loss & consecutive losses are better for v2. And of course, average position time is reduced as expected. In the early years v1 performs better but in the last few years in relative % terms it appears they are both similar in returns.

I personally would start with v2 as over the last 5 yrs (with the exception of a couple of quarters in 2013) it performs more consistently – as shown in the Quarterly results comparison below. Especially as your results above confirm that in later years (ie more recent times incorporating current market conditions) the draw of v2 is also much better. I would take lesser volatility of earnings rather than increased profits at this stage. In the future we can always tweak the parameters if there are healthy profits already banked that give us more room for increased risk.

The high draw is still something that perhaps needs to be worked on but at least some other issues have been reduced in terms of risk which I think is a great start.

Hey Reiner,

the results look really nice, thank you for this! specially since it doesn´t need any indicators.

I wasn´t able to understand the code completely till now, but I am working on it 😉

But since the trades are only triggered by date / day of the month, why isn´t it on daily timeframe in order to have a better backtest result.

I tried to change the code, but I failed.

And I don´t understand why the trades are cumulated since they are triggered by a special day.

Is it possible/useful to cumulate the trades only if the position is positive?

Hi guys

A position has been opened in the Navigator DAX 4H V2 at 09:00 today, ten short contracts. No position was opened in the Navigator DAX 4H V1.

Regards

Hi guys

I can confirm an opened position in Navigator DAX 4H V2. And thanks to Reiner for another very interesting code.

Regards

Martin

@Reiner thanks for sharing, what would you change to start with 1k?

Thanks

I can also confirm a short position opened in Navigator v2 this morning @ 11,843.4 (with an attached stop of 12,790.9 and limit of 11,488.1). This is in IG Demo spreadbet.

@ Carlos – given that this is still a new strategy and in development with a relatively high draw, I would probably not recommend an account of that low amount (you would need at least E3-5k even with a reduced position size) as you could get a big draw at the beginning that wipes you out. If you still wish to go ahead I would reduce all the position sizing parameters to 1 but also keep monitoring closely at the beginning and be ready to step in.