Sorry ALE I have only 100 000 bars and it was very very long only with 3 variables

In fact I think you should WF on how many bars you want to use the code with an optimisation

For example if you want to keep the same optimisation every week 34*5=170 bars

If you test on 5 periods 5*170 is quite enough I think

Cheers

Hi. Has anyone tried this on a commodity? I’m trying it out on Mini Crude Oil and can’t get it to work. I’ve been trying to optimise all morning however getting nowhere. The code is working but think I’m not looking at the right range for the variables so that the best optimisation results are from o trades for 0% gain (the rest of the results are negative). I think it could be due to the different point size than for fx.

In particular, can anyone suggest variables for mcThreshold and rcThreshold? I’ve literally spent hours optimising various numbers but not getting anywhere.

I’m sure it’s a beginners error to do with adjusting for different point sizes. Any help appreciated.

Thanks

Issues like you experienced jonjon are partly why I suggest in post #32898 that we leave in the numbers for the variable sets when we attach an .itf file.

The other reason is that unless we can see the range of variables used by an optimiser submitting code and re-optimise a few ourselves then how can we have confidence in the values?

I’m sure we have all re-optimised Systems submitted on the various Threads and in the Library and found variable values that give better results?

Leaving the variable sets / range in the file makes it easier to do a confidence check?

GraHal

In system 2, why is the mcThreshold and rcThreshold defined twice? I have taken one set out on the code I'm testing now.

Maz

MazParticipant

Veteran

Hi guys,

Understanding the code (indicators) before you optimize

Before dumping the code base on a new asset class, you need to fully understand the code, how it’s working and what it does. Pull it apart. Make custom indicators from the indicator section. See how they work graphically on different instruments. This way it will make more sense as to what ranges you need to try.

Where to start optimizing for a new asset

Think about price action characteristics on the asset the system works well on – ATR, volatility, etc. Think about how that relates to the asset you want to move onto trying. For example if the new asset is less volatile, you’ll want to try variable ranges that make sense to reflect that. In this case smaller = less volatile.

Not a one-size-fits-all

Although the premise is market-agnostic, that PRT code I posted in the library is not a one-size-fits-all. Different asset classes will need different filters so you need to do the research. If you look at the filters I’ve used for the example (EUR/USD) you’ll see they may not make sense out of the box for stocks or for commodities due to the way stocks and commodities move. By filters I mean reasons NOT to take a (potentially weak) setup.

I have done a stress test and optimisation on DOW 1E 3p spread with 100 000 bar history and below is the result. I have also tried trailing stop, profit target and Donchian stop and they all give more or less the same result. If anyone have other suggestions on what I could try, please let me know!

Btw, there are a few things I don’t understand when I’m testing this code (keep in mind I’m a beginner).

The code have several commands for exit a trade: wintarget+trailing stop+mintradetime+MA long criteria. Will the system takes whatever happens first? I have tried to take some away and test each exit separately but with a poorer result. There are for example profits above the win target plus trades close before the mintradetime. Can anyone explain the reason for this?

// ====================================== \\

// DOW E1 Contract, TF 1H, Spread: 3p

// -------------------------------------- //

// Static Optimization for DOW E1 Contract 1 hour

// Jan 2013 - April 2017

// Spread 3 points

wintarget = 42 // Clip target to maximum of x points

minTradeTime = 16 // stay in trade for at least x bars

mcShortPeriod = 4 // Short period momentum

rcShortPeriod = 3 // Short period average range

mcLongPeriod = 100 // Long period momentum

rcLongPeriod = 80 // Long period average range

mcThreshold = 0.25 // 0.5 // Momentum coefficient threshold

rcThreshold = 0.5 // 1 // Range coefficient threshold

maShortPeriod = 5 // Short term moving average

maLongPeriod = 3 // Long term moving average

// ====================================== \\

// :: Indicators --

// -------------------------------------- //

// Momentum Coefficient and Range Coefficient ============= \\

if barIndex >= max(mcLongPeriod, rcLongPeriod) then

mShort = momentum[mcShortPeriod]

mLong = momentum[mcLongPeriod]

mc = max(0, (abs(mShort) / abs(mLong)) -1)

r = abs(range)

arLong = average[max(1, rcLongPeriod)](r)

arShort = average[max(1, rcShortPeriod)](r)

rc = max(0, (arShort / arLong) -1)

//rc = max(0, arShort - arLong)

endif

// ----------------------------------- //

// General Indicators ================= \\

upBar = close > open

maShort = exponentialAverage[maShortPeriod](Close)

maLong = exponentialAverage[maLongPeriod](Close)

// ----------------------------------- //

// ====================================== \\

// :: Entry Logic

// -------------------------------------- //

// long entry rules (buy condition)

bc1 = not longOnMarket

bc1 = bc1 and (mc >= mcThreshold)

bc1 = bc1 and (rc >= rcThreshold)

bc1 = bc1 and upBar

bc1 = bc1 and maShort > maShort[1]

// long exit rules (exit long conditions)

le1 = longOnMarket

le1 = le1 and ( barIndex >= barIndexAtBuy + minTradeTime)

le1 = le1 and (maLong < maLong[4])

// ====================================== \\

// :: Execution Handlers

// -------------------------------------- //

if bc1 then

buy 1 shares at market

set target pprofit wintarget

barIndexAtBuy = barIndex

endif

if le1 and longOnMarket then

sell at market

endif

SET STOP pLOSS 70

//trailing stop

trailingstop = 25

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

priceexit = 0

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

SELL AT priceexit STOP

endif

Thanks @Maz. A logical approach to finding the ranges. An obvious solution but I needed it pointing out!

I’ve created new indicators from Maz’s code which I’ve added to my charts to help and I put the code below as it may be of help to some. I’m already seeing that this should hopefully help me with my Oil query and I’ll let you know any positive results.

// Momentum Coefficient ============= \\

mcShortPeriod = 5

mcLongPeriod = 20

mShort = momentum[mcShortPeriod]

mLong = momentum[mcLongPeriod]

mc = max(0, (abs(mShort) / abs(mLong)) -1)

Return mc

// Range Coefficient ============= \\

rcShortPeriod = 5

rcLongPeriod = 20

r = abs(range)

arLong = average[max(1, rcLongPeriod)](r)

arShort = average[max(1, rcShortPeriod)](r)

rc = max(0, (arShort / arLong) -1)

Return r as "Range", rc

Just realised that my last post with the indicators is just a repitition of Maz’s first post and link to his indicator (which was done better than mine above).

Maz’s indicator can be found here

Hi MAZ, what version of PRT are you using? the IG or the Premium ver from PRT?

I still cannot get the DIFF system to generate any trades- So I might think there could be a difference in the compilers. I use the IG ver.

Cheers Kasper

Hi Again.

I did some troubleshooting- forked the bc1 into 5 indicators.

What I could see is

bc2 = (mc >= mcThreshold)

bc3= (rc >= rcThreshold)

is never gonna be true until I *pipsize the Thresholds.

It looks like this. Question is why do some get trades, and some don’t?

// ====================================== \

// :: MDif-RDif

// Long Name : Momentum Differential and Range Differential Accelleration

// Version : v1.11

// Author : Maz @ prorealcode.com

// Date : 07-04-2017

// Contact : prtmaz at gmail dot com

// -------------------------------------- //

// ====================================== \

// :: Optimizations --

// -------------------------------------- //

once optimization = 1 // 1 = EUR/USD M15

// Set to 0 for re-optimization and walk-forward

if optimization = 1 then

// Static Optimization for EUR/USD M15

// May 2015 - April 2017

wintarget = 43 // Clip target to maximum of x points

minTradeTime = 43 // stay in trade for at least x bars

// try also 27

mcShortPeriod = 5 // Short period momentum

rcShortPeriod = 4 // Short period average range

mcLongPeriod = 100 // Long period momentum

rcLongPeriod = 100 // Long period average range

mcThreshold = 2*pipsize // Momentum coefficient threshold

rcThreshold = 8.5*pipsize // Range coefficient threshold

maShortPeriod = 18 // Short term moving average

maLongPeriod = 53 // Long term moving average

// ( try also 150 / or 53 for 70% hit rate / or 51

elsif optimization = 2 then

// Insert your optimizations here

// wintarget = 43 // Clip target to maximum of x points

// minTradeTime = 43 // stay in trade for at least x bars

// ...

wintarget = 43 // Clip target to maximum of x points

minTradeTime = 43 // stay in trade for at least x bars

mcShortPeriod = 5 // Short period momentum

rcShortPeriod = 4 // Short period average range

mcLongPeriod = 100 // Long period momentum

rcLongPeriod = 100 // Long period average range

mcThreshold = 0.1*pipsize // Momentum coef or dif threshold

rcThreshold = 0.9*pipsize // Range coef or dif threshold

maShortPeriod = 18 // Short term moving average

maLongPeriod = 53 // Long term moving average

endif

// ====================================== \

// :: Indicators --

// xr = max(0, xr) // hide values below zero

// -------------------------------------- //

// Momentum Differential ============= \

mShort = momentum[mcShortPeriod]

mLong = momentum[mcLongPeriod]

mc = max(abs(mShort) - abs(mLong), 0)

// ----------------------------------- //

// Range Differential ================= \

r = abs(range)

arLong = average[max(1, rcLongPeriod)](r)

arShort = average[max(1, rcShortPeriod)](r)

rc = max(0, arShort - arLong)

// ----------------------------------- //

// General Indicators ================= \

upBar = close > open

maShort = exponentialAverage[maShortPeriod](Close)

maLong = exponentialAverage[maLongPeriod](Close)

// ----------------------------------- //

// ====================================== \

// :: Entry Logic

// -------------------------------------- //

// long entry rules (buy condition)

bc1 = not longOnMarket

bc2 = (mc >= mcThreshold)

bc3= (rc >= rcThreshold)

bc4 = upBar

bc5 = maShort > maShort[1]

// long exit rules (exit long conditions)

le1 = longOnMarket

le1 = le1 and ( barIndex >= barIndexAtBuy + minTradeTime )

le1 = le1 and (maLong < maLong[4])

// short entry rule

// -- na --

// short exit rules

// -- na --

// ====================================== \

// :: Execution Handlers

// -------------------------------------- //

if bc1 and bc2 and bc4 and bc3 and bc5 then

buy 1 shares at market

set target pprofit wintarget

barIndexAtBuy = barIndex

endif

if le1 and longOnMarket then

sell at market

endif

//graph mc COLOURED(255,0,0) AS "mc"//black

//graph mcThreshold COLOURED(0,255,0) AS "mcThreshold"//black

graph rc COLOURED(255,0,0) AS "rc"//black

graph rcThreshold COLOURED(0,255,0) AS "rcThreshold"//black

//graph bc3 COLOURED(0,0,255) AS "bc3"//black

//graph bc4 COLOURED(0,255,255) AS "bc4"//black

//graph bc5 COLOURED(255,255,0) AS "bc5"//black

MazParticipant

Veteran

Cheers. Will include the *pipsize for future code posts

MazParticipant

Veteran

…but mcthreshold and rcthreshold are not units of points or pips. So not sure what’s up with that.

Hi Maz, no, but rc and mc are, at least in my ver. and currency 🙂 they are exactly the pipsize factor smaller. I admit- it strange.

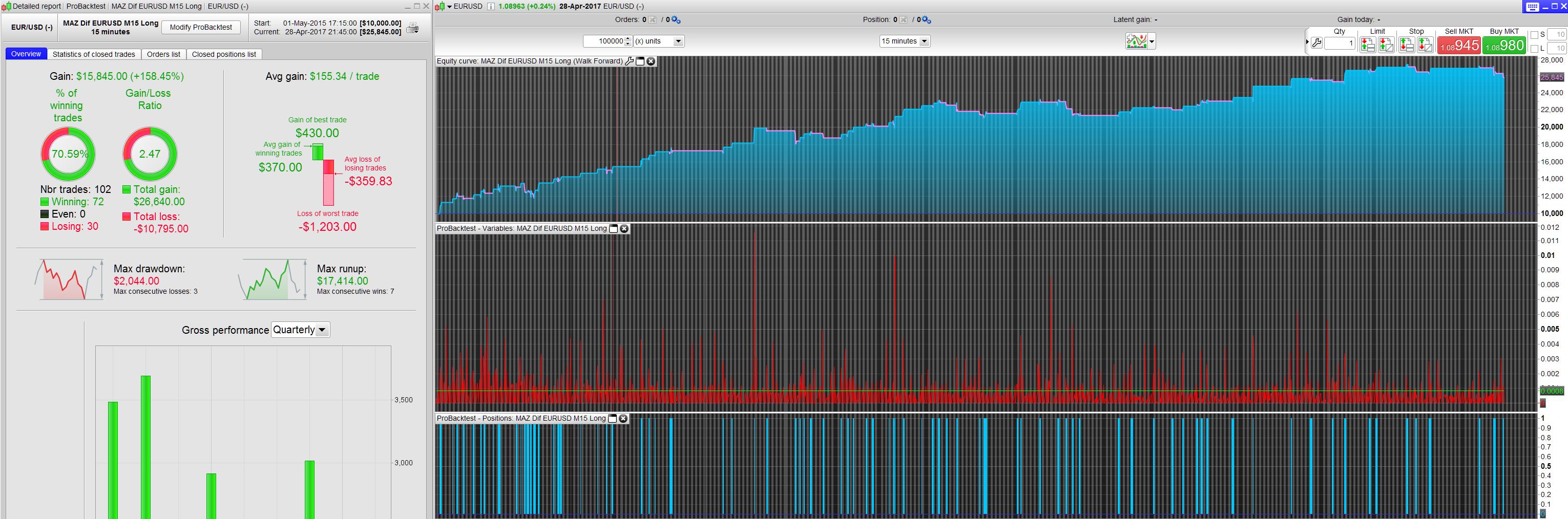

$ M-R Dif EURUSD M15 Long works good for me Kasper, attached results.

I cant recall making any changes, but my version is attached.

Site below is well easy to use for checks on code difference if you ever need it.

GraHal

https://www.diffchecker.com/

Hi GraHal, yes I know it works for most people, I did see some one else having the same problem though. I think it my PRT that has either a diffenent currency conversion or simpley another way of it own.. But when I seperated the Bc1 into every variable I could see the numbers would never match for the two variables tested. That why I never got any trades.

It’s definetely not Maz’s work that has the problem- It’s just depressing.

Cheers Kasper