Maz

MazParticipant

Veteran

Hi all,

As requested just creating a thread to discuss any suggestions, questions or forks of the strategy and indicator that I posted.

Strategy and info can be found here

Indicator and info can be found here

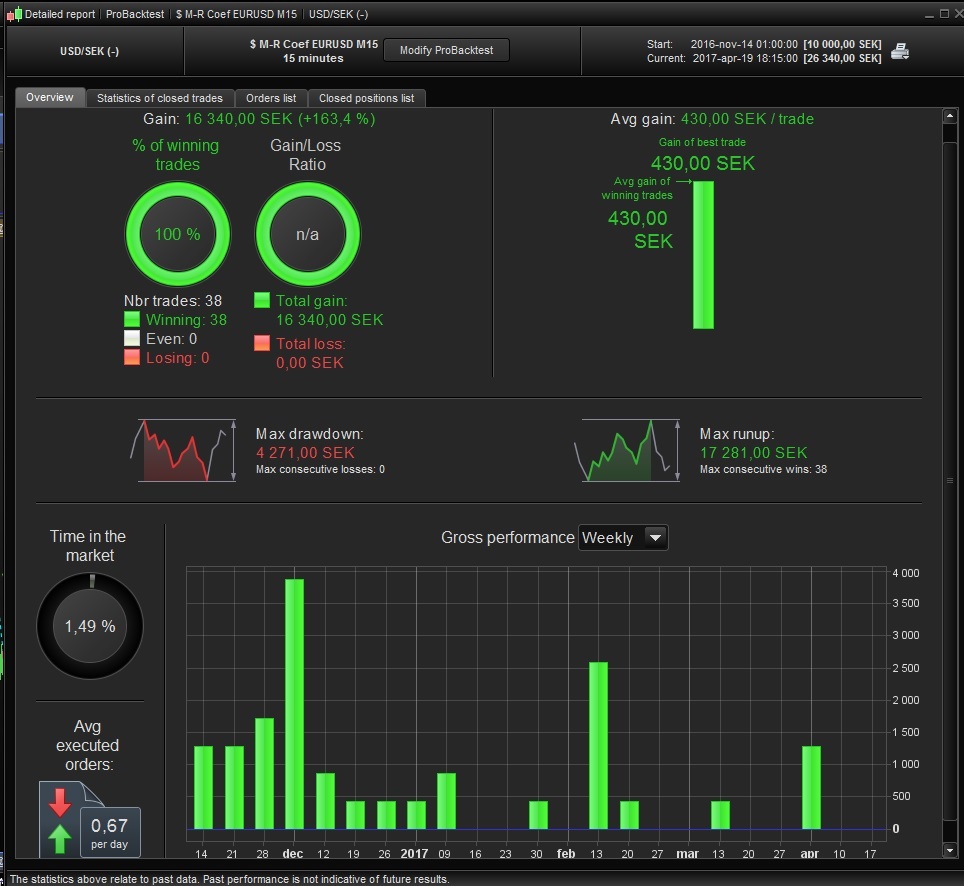

Thanks @Oskar Bergvall for looking at USD/SEK. Feel free to post results here. Note that considerable re-optimization is required for every market and asset class.

Best,

Maz

Yes this is back to Nov 2016 wit EURUSD. Haven’t changed your variables. Looks like it’s working very well 🙂 Losses seems to set it back alot though.

hello, would it be possible to have some guidance on how to code also the version that goes short? Thanks!

Maz

Thank you for the code. I really feel like I learnt something from going through it which is what I love about this site. In particular many thanks for the time you spent adding the notes and making it user friendly.

Just a small FYI / beginners question: in the code for the coeff version the lines for mcThreshold and rcThreshold have a “//” to cancel them out however later on in the buy conditions you have:

bc1 = bc1 and (mc >= mcThreshold)

bc1 = bc1 and (rc >= rcThreshold)

I see that you have optimised for mcThreshold and rcThreshold. Should the “//” be still in the code? I don’t think it matters as when I take the “//” out it gives the same result.

Thanks

MazParticipant

Veteran

Quick disclaimer

First off, please note the code is purely a PRT backtest. I don’t actually run our production systems in PRT! Again, please ensure you have added your necessary risk management and error handling code and done due diligence before running anything live. Any systems I post are more to open discussion and promote contribution of ideas around the general premise.

@ jonjon : Yep, just un-comment them. They are required. They were commented due to backtesting with optimizer.

@ GraHal @ Victormork // Division by zero error

My guess is division by zero error happens due to indicator doing a divide before necessary number of periods have passed. So…

if barIndex >= max(mcLongPeriod, rcLongPeriod) then

mShort = momentum[mcShortPeriod]

mLong = momentum[mcLongPeriod]

mc = max(0, (abs(mShort) / abs(mLong)) -1)

r = abs(range)

arLong = average[max(1, rcLongPeriod)](r)

arShort = average[max(1, rcShortPeriod)](r)

rc = max(0, (arShort / arLong) -1)

//rc = max(0, arShort - arLong)

endif

Something along those lines would probably do the trick.

All the best,

M

MazParticipant

Veteran

It would be particularly useful to see people’s optimization suggestions for a variety of markets and asset classes. Please post back test results and variable optimization sets here

Thank you Maz for clarifying. I’ll try to do my own testing and will come back when I have something useful.

ALE

ALEModerator

Master

Hi Maz, may have a detailed explanation of the concept, and what variations are possible to look for different market or time frame?

Closing down for the weekend now. If anyone would like to try this system on DOW 1H (wall street cash E1), here’s a starting point:

// ====================================== \\

// :: Optimizations --

// -------------------------------------- //

// Static Optimization for DOW E1 Contract 1 hour

// Jan 2013 - April 2017

// Spread 3 points

wintarget = 45 // Clip target to maximum of x points

minTradeTime = 16 // stay in trade for at least x bars

mcThreshold = 0.1 // Momentum coef or dif threshold

rcThreshold = 0.1 // Range coef or dif threshold

// try also 27

mcShortPeriod = 4 // Short period momentum

rcShortPeriod = 2 // Short period average range

mcLongPeriod = 100 // Long period momentum

rcLongPeriod = 70 // Long period average range

mcThreshold = 0.1 // 0.5 // Momentum coefficient threshold

rcThreshold = 0.55 // 1 // Range coefficient threshold

maShortPeriod = 5 // Short term moving average

maLongPeriod = 20 // Long term moving average

// ====================================== \\

// :: Indicators --

// -------------------------------------- //

// Momentum Coefficient and Range Coefficient ============= \\

if barIndex >= max(mcLongPeriod, rcLongPeriod) then

mShort = momentum[mcShortPeriod]

mLong = momentum[mcLongPeriod]

mc = max(0, (abs(mShort) / abs(mLong)) -1)

r = abs(range)

arLong = average[max(1, rcLongPeriod)](r)

arShort = average[max(1, rcShortPeriod)](r)

rc = max(0, (arShort / arLong) -1)

//rc = max(0, arShort - arLong)

endif

// ----------------------------------- //

// General Indicators ================= \\

upBar = close > open

maShort = exponentialAverage[maShortPeriod](Close)

maLong = exponentialAverage[maLongPeriod](Close)

// ----------------------------------- //

// ====================================== \\

// :: Entry Logic

// -------------------------------------- //

// long entry rules (buy condition)

bc1 = not longOnMarket

bc1 = bc1 and (mc >= mcThreshold)

bc1 = bc1 and (rc >= rcThreshold)

bc1 = bc1 and upBar

bc1 = bc1 and maShort > maShort[1]

// long exit rules (exit long conditions)

le1 = longOnMarket

le1 = le1 and ( barIndex >= barIndexAtBuy + minTradeTime)

le1 = le1 and (maLong < maLong[4])

// ====================================== \\

// :: Execution Handlers

// -------------------------------------- //

if bc1 then

buy 1 shares at market

set target pprofit wintarget

barIndexAtBuy = barIndex

endif

if le1 and longOnMarket then

sell at market

endif

SET STOP pLOSS 70

//trailing stop

trailingstop = 30

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

priceexit = 0

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

SELL AT priceexit STOP

endif

Default ‘Pre-Load bars’ are 200, would increasing this to 500 / whatever get us ‘ready to trade’ straight off and not get the divide by zero error re your fix below??

if barIndex >= max(mcLongPeriod, rcLongPeriod) then

endif

I’ll post variable optimization sets for other markets also.

Thanks

GraHal

Hi Guys,

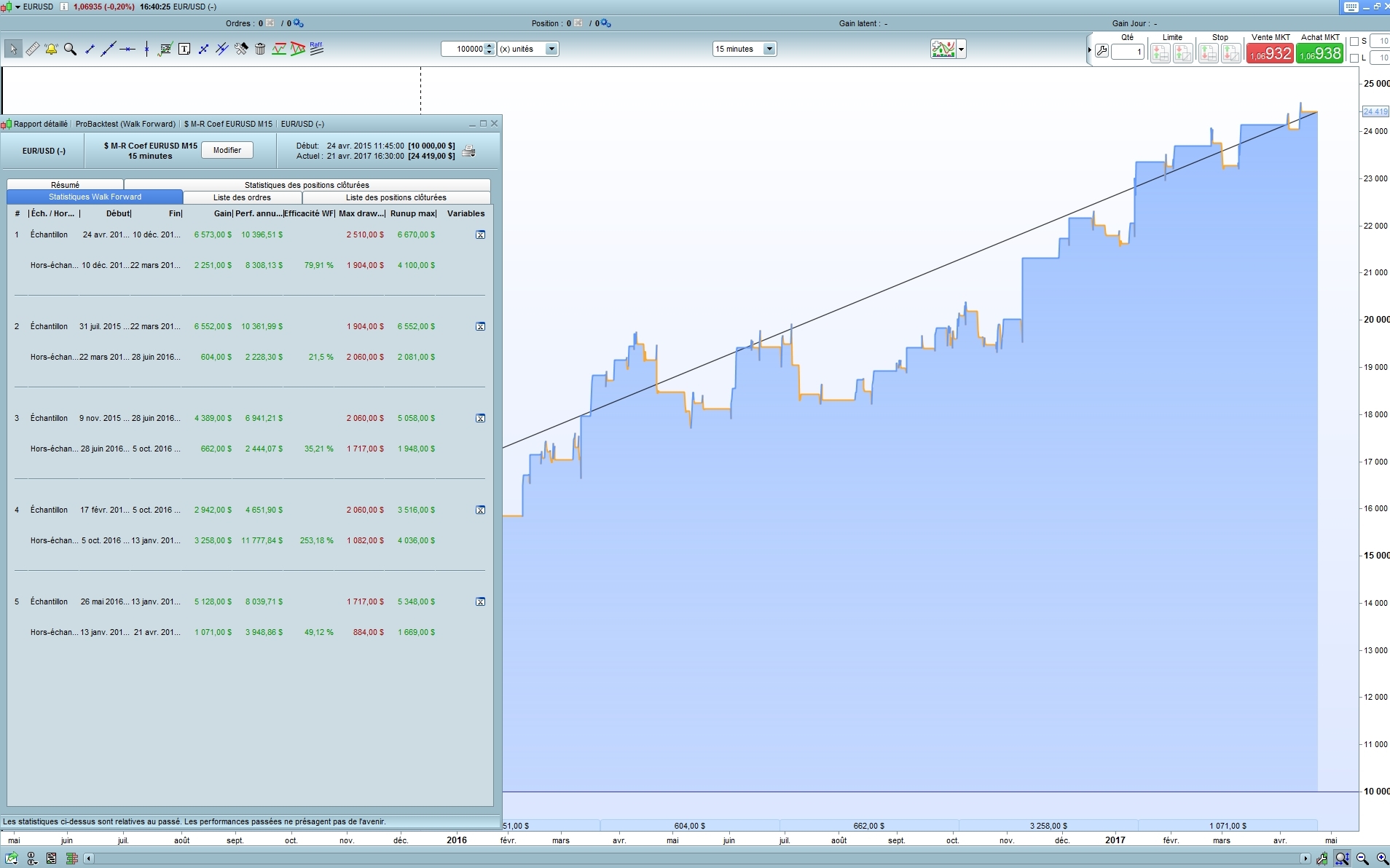

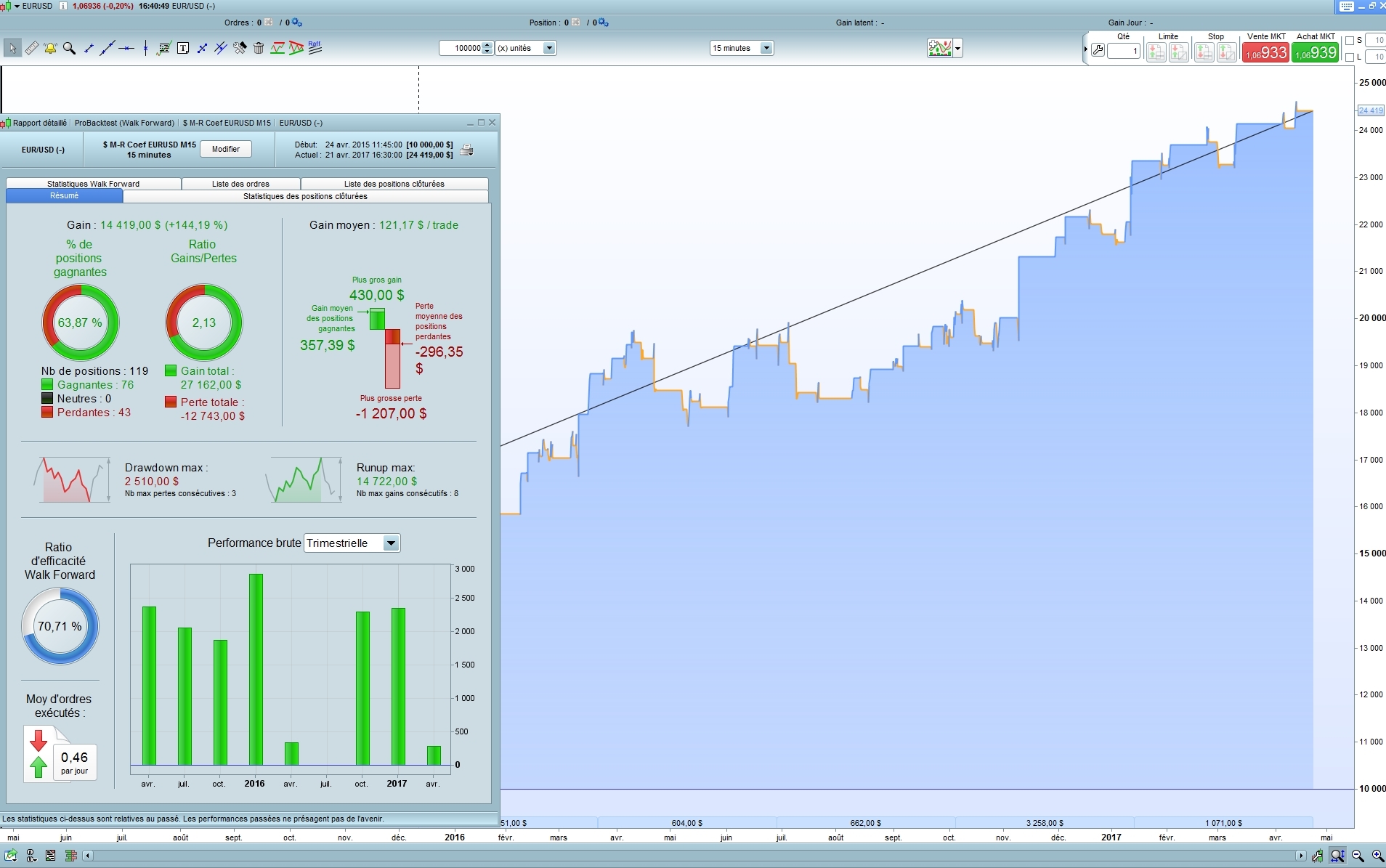

I do a Walk Forward on EUR/USD with the coef version (the other seems doesn’t work) and optimisation of wintarget, malongperiod and mashortperiod on 100 000 bars.

30 minutes after the results are not bad at all (It can probably optimized more)

WFE ratio =71 % (>50 % = Good)

WF efficacy >50 % for 2 of 5 periods (Normally 3/5)

And finish in Gain

Have a nice day

Zilliq

Might I suggest that we attach optimised .itf file still containing the variable sets / ranges used during optimisation (as per Maz’s file in the library?).

This enables those using the .itf file to see the range over which optimisation took place.

Or am I talking / asking a load of bs? You can say, it’s okay! 🙂

GraHal

Hi.

Like Zilliq and others I can’t get any trades when backetesting the Differential system on EURUSD mini 15 min TF.

what could be the problem?

Edit.. as I write- I ran the Coefficient backtest, and suddenly the as data in the Differential system

For the Coefficient system, how would you implement any MM systems when not running any stoploss?

Edit A quick optimization shows that a SL at 100 would be okay, but for an average gain of 20 it seem to be poor RR. Any suggestions?

Cheers Kasper

ALEModerator

Master

@Zilliq

can I test your version with 200.000 bars?

Thanks