Hi guys,

please wait for a little bit of time before pursuing the conversation until I have finished moving all the discussion since Pips-103 first post in this topic back into his original topic “Forex lot size” into a new topic (sorry had to create a new topic because “forex lot size” was in another forum and posts moves can only be done within same forum), where you’ll then be able to continue. Purpose is to keep current topic “Centralization of queries and suggestions on ProRealTime” looking more like a pure list for PRT guys without all the conversations derived from the suggestions.

Thanks

Edit: thanks for your patience, you can now continue there

Hi Nicolas and all fellow forum members,

one thing that would be really nice is if they could fix the % Drawdown Max item in the Backtest report.

After noticing some strange behavior, I’ve made myself a spreadsheet to derive all sorts of stratistics on a given strategy.

It appears that what they call the ” % Drawdown Max” is calculated as a % of the Drawdown Max in absolute terms, divided by the equity you had when it occurred. This is NOT the maxDD in % terms that you will encounter on your strategy’s life.

Let me give you an example (oversimplified and exagerrated to make my point clearer)

- you start a strategy with 1,000€

- you first hit 800€ then go up to 50,000€ in a straightline and finally down to 49,500€. End of strategy.

- Your max DD in absolute term as given by PRT is 500 (ie 50,000-49,500), and PRT gives you also a %MaxDD value of 500/50,000, ie 1%

- You think you hit the jackpot, and that this strategy could be leveraged at least 10x (ie for a potential maxDD of 10% at any given time)

- In reality your %MaxDD is 20% (ie 1,000 – 800 / 1,000), and if you leverage 10x you expose yourself to going bust very quickly.

So, in a nutshell, could PRT give us the real %MAXDD as calculated above instead of the % of theMacDD in absolute terms ?

Another question for Nicolas: how frequently do you have contacts with PRT to pass them on those suggestions ? Is there a follow-up process ?

Many thanks for this forum again,

B

@barnabear

Be sure that PRT techies are informed that this topic is now the main centralization of queries about the platform (in English language). They read it often, so don’t hesitate to add any ideas about what you consider a must have into the platform. About bugs reports, another topic is open there: PRT 10.3 bug reports

Hi GraHal

No I mean in the list of personal EAs on your platform. Where you modify an old robot for additional functionality this info would be useful. eg the date and time for excel spreadsheets is an example.

It would be great if we could access the spread to add into our code

IE If Spread > 2.5 then (etc).

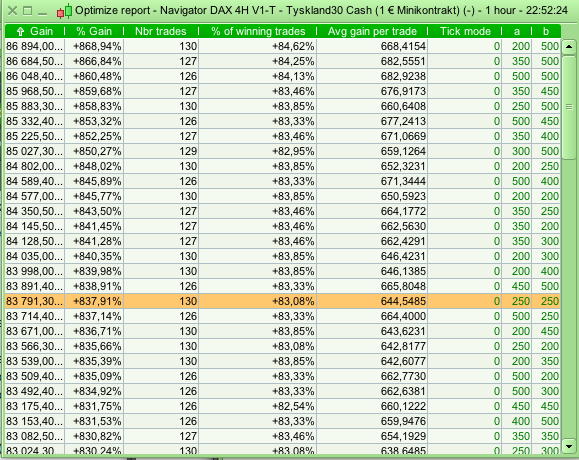

I think that it would be nice with a drawdown column in the optimization screen

Hi GraHal

No I’m looking for a last modified date time stamp for your own systems. I may be working on several ideas at once and it would give me an insight into which EA I was working on last or want to incorporate something from a few weeks back from an idea I discarded and it would certainly help me. The date would pinpoint for me which EAs to look at.

Hi John Yes I strongly agree with you … ‘beggars belief’ that PRT lacks these essential basic features.

I have updated my wish list in my second post here in this thread: https://www.prorealcode.com/topic/centralization-of-queries-and-suggestions-on-prorealtime/#post-23211

Now we can talk about about queries by their numbers, please. I plan to add yours in the list too.

About the 30/, this is how I see it:

defparam var1 myvariable1 as integer

defparam var2 myMovingAverage as MMtype

defparam var3 myvariable2 as double

This is the only instruction with the 3/ one, which is missing to completely copy/paste a prorealtime code without any errors.

Hi,

I always post my list for Santa claus (and some things are already implemeted, thanks PRT) . It is still missing :

1/ Multiframe !!!!!!!!!!!!!!!!!! +++++++++++

2/ SQN of Van Tharp on the backtest results : Very easy to add because all composent are already on

3/ Trading on others representation based on range : Range bar, Range Candle, Renko … +++++++++++++++++++++

4/ Better trailing stop/ Stop loss possibilities : Notably the possibility to put a stoploss, Trailing stop…for every position, not all positins at the same time

4 / Faster Walk Forward (many hours for a simple strategy, with 3-5 variables !)

Thanks

Zilliq

Why don’t you use the CALL instruction ?

I try what you write with defparam but don’t suceed. Do you have an example ?

Thanks

Zilliq

The tick by tick backtesting functionality is a great addition but I find it a bit hit and miss in terms of results and thus my confidence in it is still not 100%. There are three issues primarily that I would like to get fixed :

- Re. the error ” One or more candles could not be analysed with tick by tick data because this data was not available at that time” – I would prefer an option that overrides the “missing” days but gives you the option to test the rest of the timeframe (like 2) below). At present, if it encounters one or more missing candle data, it seems to stop testing the entire period using the tick by tick function.

- Limitation of 500 bars on tick by tick backtest – I find this limitation to be quite restrictive, it needs to be expanded to at least 2-3x the existing limit (if there needs to be a limitation imposed). If the data is available then its better for users to have access to it. At present, the solution is to break up the backtest into 6mth-1yr etc segments which is not ideal as then all the statistical data like draw %, losses etc is not representative for the entire period and you are unlikely to get an idea of how the overall strategy performs especially if you are using variable position sizing that depends upon previous results.

- When optimising, tick by tick is not available, you have to select the individual optimised line for that. This is again not ideal as how would you know which variables are definitely worth investigating if the table does not show the actual tick by tick results.

Many thanks

GRAPH function to allow more than 5 variables to be displayed, ideally this should be increased to at least 20.

Also would be good if there was the possibility of making a new specific window/s to display specific GRAPH variables that are related (whether by similar variables or scale etc.).

Thanks

P

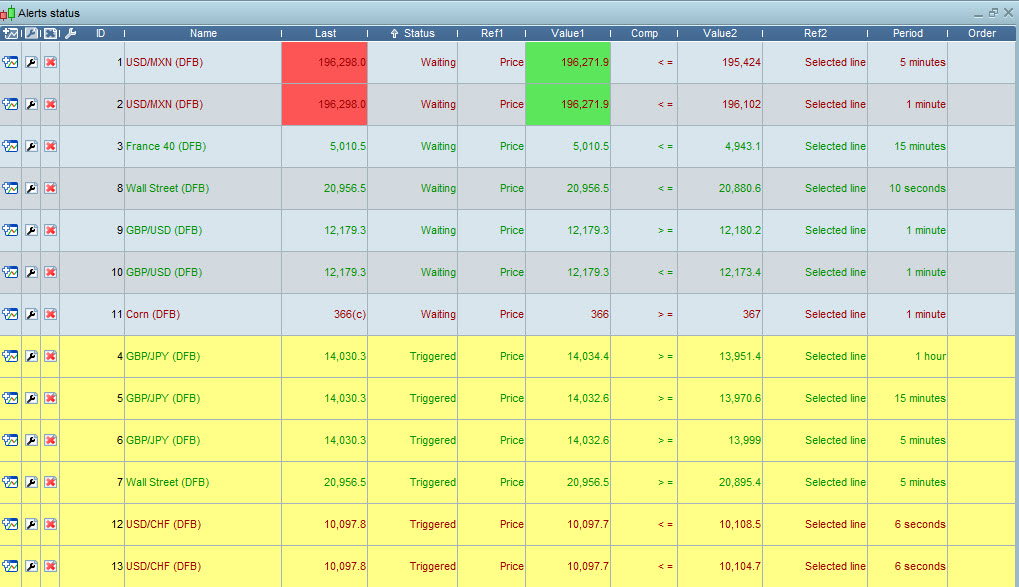

‘Alert Status List’ needs the option to add column ‘Time of Alert’ – see attached for example.

At times I have loads of Alerts set up and several David / Julia voices alerting me and loads of pop ups freezing my charts. So ‘voices and pop-ups’ don’t work for me (at times) and then I look at the Alert Status List, but I need to know which is the most recent Trigger.

Feeling pleased with myself, just made over £86 using alerts (across several markets) trading the Non-Farm Payroll, it was hectic (which I love) but the need for ‘Time of Alert’ jumped out as a clear need. I could then sort the list by Time of Alert.

Hope to make PRT even Better!

GraHal