USDJPY trading strategy - 1minTF - SAR and EMA

May 28, 2016, 7:09 PM

Strategies

78 Comments

{kind=link}

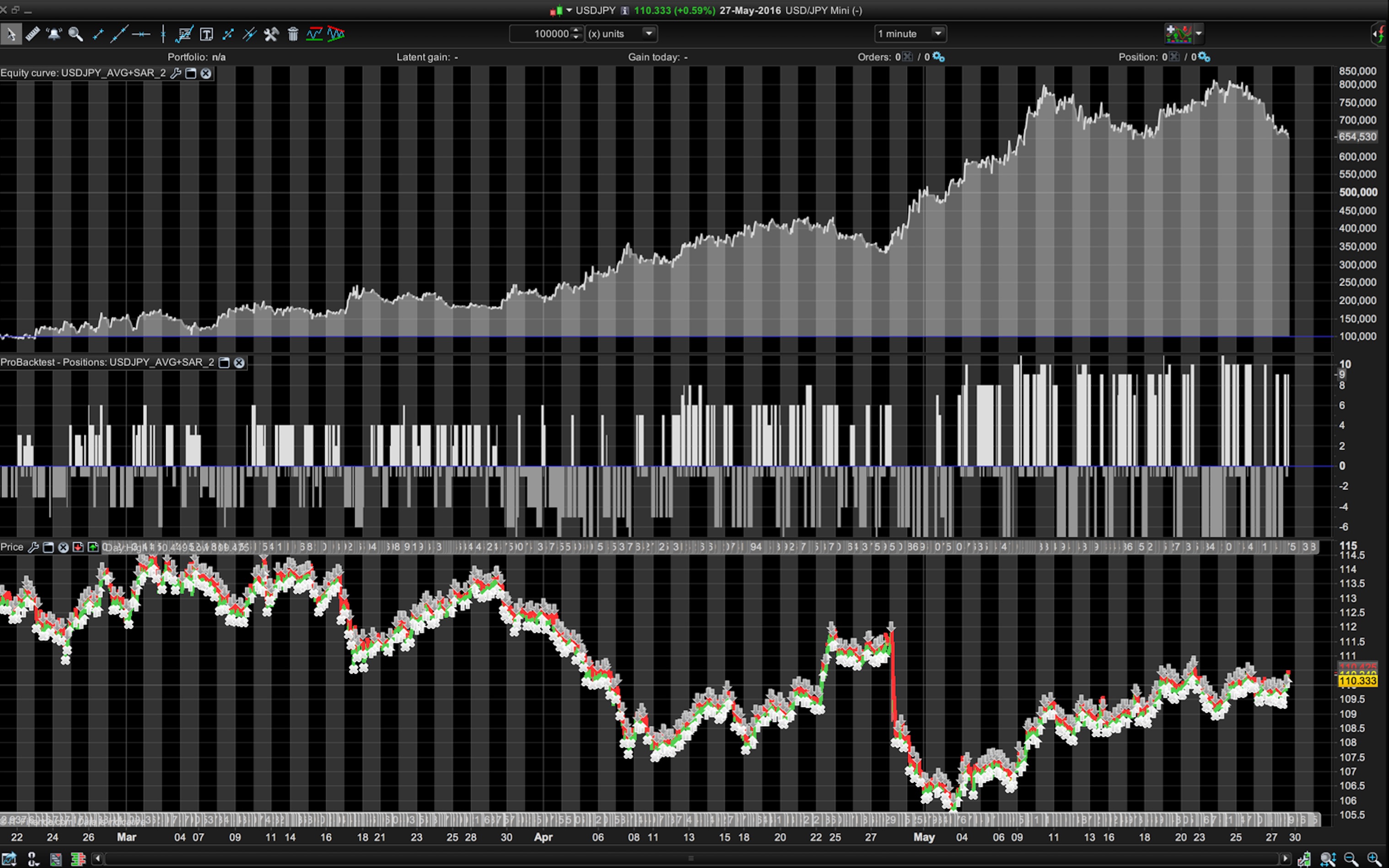

Hi everyone,

Wanted to share my simple Automated strategy for USD/JPY mini using a 1minute timeframe, with SAR and EMA indicators.

Code also includes money management to adjust for position sizes – adjust this for your liking etc.

Any thoughts or suggestion is welcome! Enjoy..

DEFPARAM CumulateOrders = false

//INDICATORS//

mm3= exponentialaverage[200*3]

mm2= exponentialaverage[200*1.5]

mm1= exponentialaverage[200*1]

PARABOLIC = SAR[0.001,0.001,0.2]

C1 = PARABOLIC>HIGH //RED SAR = SHORT

C2 = PARABOLIC<LOW //GREEN SAR = LONG

Spread = 1.1

//

//MONEY MGT//

Equity = (Strategyprofit+20000)

Risk = round(Equity/100000)

Losses = positionperf(1)<0 and positionperf(2)<0 and positionperf(3)<0

streak = positionperf(1)>0 and positionperf(2)>0 and positionperf(3)>0

if losses then

n = max(abs(round(max(3+risk-2,risk-2))),2)

elsif not losses then

n = max(abs(round(max(3+risk,risk))),2)

endif

if streak then

n = max(abs(round(max(5+risk,risk))),2)

endif

//

T1 = (barindex-tradeindex>=3)

T2 = (barindex-tradeindex>=3)

//ENTER LONG//

if (mm1>mm2 and mm2>mm3) and c2 AND T1 then

buy n contract at breakeven+spread*pipsize limit

breakeven = parabolic

if T2 and longonmarket then

sellshort at breakeven+spread*pipsize stop

endif

endif

//ENTER SHORT//

if (mm1<mm2 and mm2<mm3) and c1 and T1 then

sellshort n contract at breakeven-spread*pipsize limit

breakeven = parabolic

if T2 and shortonmarket then

exitshort at breakeven-spread*pipsize stop

endif

endif

{kind=link}

Average

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...