EURUSD volatility breakout strategy

June 6, 2017, 10:07 AM

Strategies

17 Comments

{kind=link}

Hi everyone.

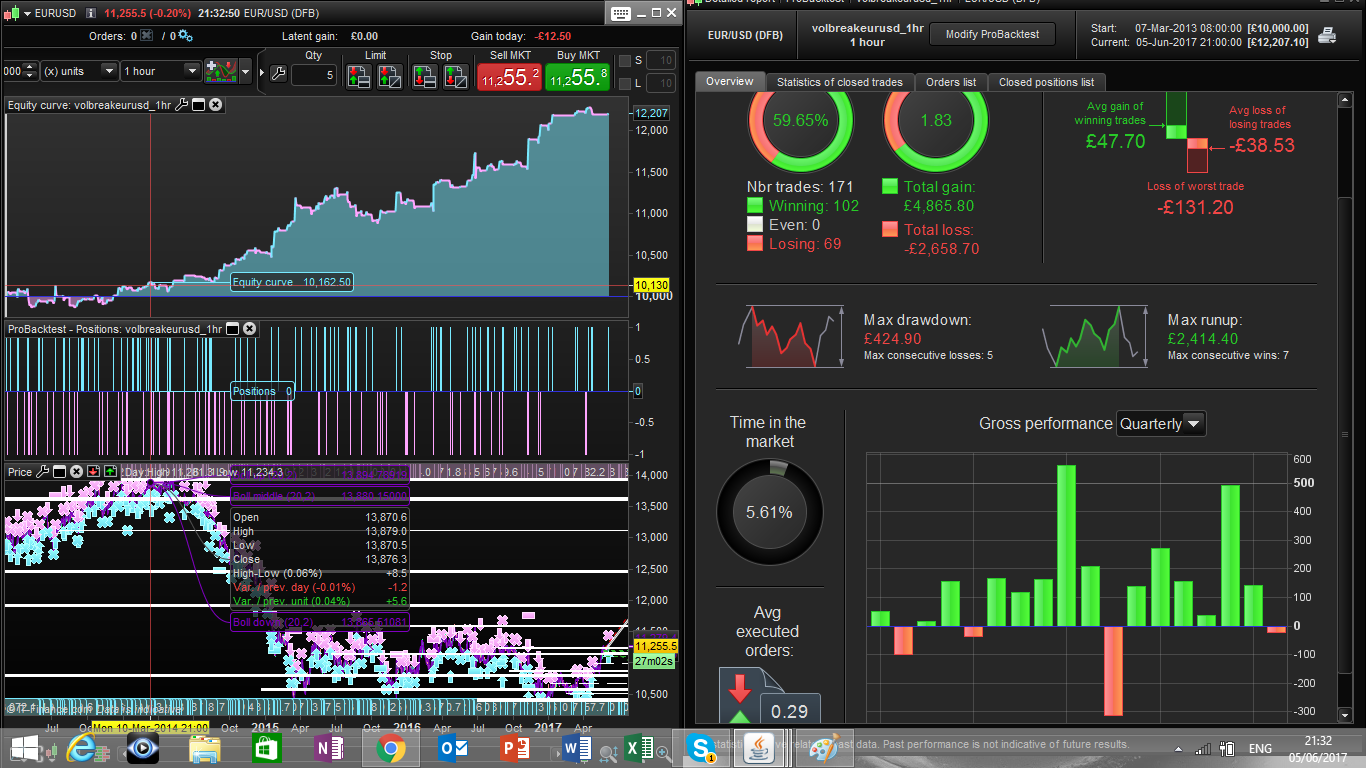

I came up with this relatively simple strategy that gives nice results on EUR/USD and DAX on a 1 hour and 30 min timeframes.

The idea behind is the following:

I define the quantity of averagerange that represent the average of the last 3 days high/low range on price.

- I take a long position if the 1 period ATR crosses above the averagerange with a corresponding bull candle (volatility break on the upside)

- I take a short position if the 1 period ATR crosses above the averagerange with a corresponding bear candle (volatility break on the downside)

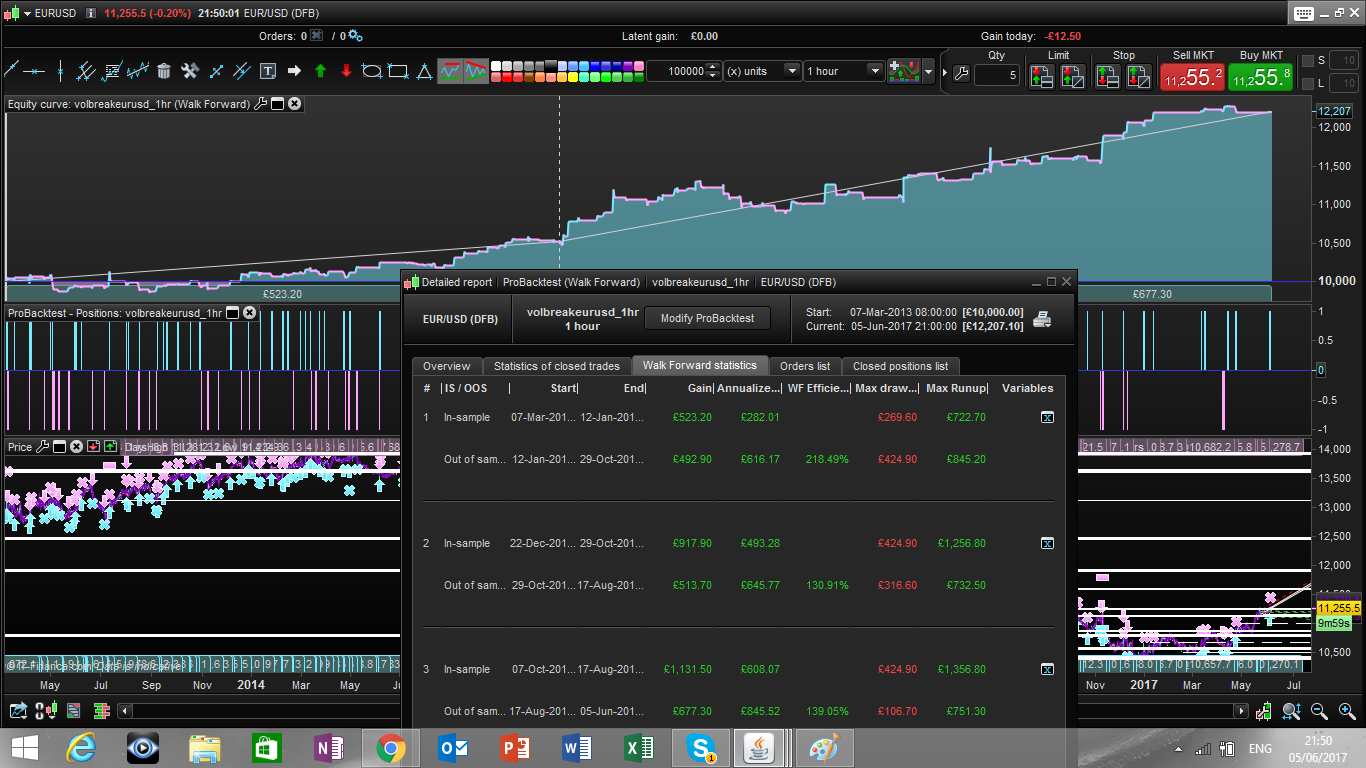

Walk forward results are attached

Best

Francesco

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

period = 72 //1hr time frame -> 3 days average

///optimized parameters

a= 9 //exit after a bars

l=0.9//factor that defines break conditions

b=1.9//dynamic profit factor multiplier

///definition of pricerange -> average of the daily high/low range

notmonday = opendayofweek = 2 or opendayofweek = 3 or opendayofweek = 4 or opendayofweek = 5

if notmonday then

dailypricerange = Dhigh(1) - Dlow(1)

endif

if opendayofweek = 1 then

dailypricerange = Dhigh(2)-Dlow(2)

endif

averagerange = average[period](dailypricerange)

////////

atr= AverageTrueRange[1](close)

pr = averagerange*b //profit factor proportional to averagerange

///trading conditions

downsidevolbreak = (atr >= l*averagerange) and close<open

upsidevolbreak= (atr >= l*averagerange) and close >=open

IF downsidevolbreak THEN

sellshort 1 PERPOINT AT MARKET

ENDIF

IF upsidevolbreak THEN

buy 1 PERPOINT AT MARKET

ENDIF

///exit conditions

set target pprofit pr

if longonmarket and barindex-tradeindex >=a then

sell at market

endif

if shortonmarket and barindex-tradeindex >= a then

exitshort at market

endif

Download

{kind=link}

Filename:

wf_eurusdvolbreak.png

Downloads:

279

Download

Filename:

volbreakeurusd_1hr.itf

Downloads:

610

Master

Currently debugging life, so my bio is on hold. Check back after the next commit for an update.

Author’s Profile

Loading...